Coastal Surveillance Market Size, Share & Industry Analysis, By Component (Sensors (Radars, Automatic Identification System (AIS), Electro Optics, Radio Direction Finers, VHF radio), Command and Control Subsystems (Remote Operating Stations (ROS), Joint Operations Centers (JOC), and Sensor Fusion & Software Platforms), and Others), By Application (Surveillance & Reconnaissance, Search & Rescue, Command & Control (C2), Border Protection, Environmental Monitoring, and Others) By Platform (Fixed and Mobile), By End User (Navy, Coast Guards, & Port Authorities), and Regional Forecast, 2026-2034

Coastal Surveillance Market Size and Future Outlook

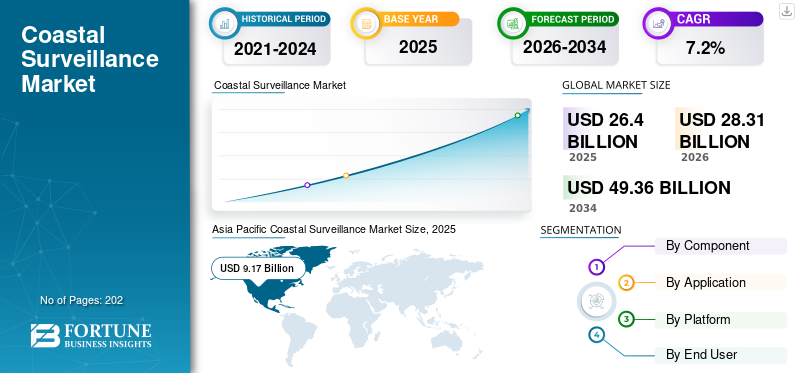

The global coastal surveillance market size was valued at USD 26.40 billion in 2025. The market is projected to grow from USD 28.31 billion in 2026 to USD 49.36 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. Asia Pacific dominated the global coastal surveillance market with a market share of 34.73% in 2025.

Coastal surveillance is a mission-critical system that provides real-time monitoring and situational awareness of maritime activities along a country's coastline and territorial waters. It integrates advanced radar, electro-optical sensors, cameras, and communication technologies to detect, track, and identify vessels, including small and high-speed targets, under all weather conditions. The system helps prevent illegal activities such as smuggling, piracy, illegal fishing, and terrorism while protecting critical maritime infrastructure and the environment.

The major players in the coastal surveillance systems market include Thales Group (France), Raytheon Technologies Corporation (U.S.), Lockheed Martin Corporation (U.S.), Indra Sistemas S.A. (Spain), and Kongsberg Gruppen ASA (Norway) among others. These key companies offer integrated coastal surveillance systems including radars, electro optical sensors, command & control software, and AIS integration. They focus on development of hardware and software solutions catering to naval, coast guard, and port security sectors.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Maritime Security Requirements Expected to Drive Market Growth

Rising incidents of illegal activities such as smuggling, piracy, illegal fishing, and terrorism has increased the need for advanced coastal surveillance to protect national borders and economic zones. Governments across the globe are boosting defense budgets to deploy real-time monitoring systems during geopolitical tensions and territorial disputes. This demand drives coastal surveillance market growth, as countries are making rapid investments in naval & coastal surveillance systems to maintain national security and manage maritime traffic.

MARKET RESTRAINTS:

High Costs of Deployment and Maintenance to Limit Market Expansion

The substantial high costs of the radars, sensors, command centers, and integration limit the adoption of the market, particularly in budget-constrained developing nations. Moreover, the high expenses for maintenance, upgrades, and skilled personnel further add to the overall costs, limiting scalability. In addition, there are complex installation processes involved in remote coastal areas which adds up logistical challenges and elevate total ownership costs. Such high cost of deployment and additional maintenance and installation costs hampers the growth of the market.

MARKET OPPORTUNITIES:

Integration of AI and Advanced Sensors Presents Growth Opportunities for Market Growth

AI-driven analytics is being used in surveillance systems for automated threat detection, behavioral analysis, and predictive monitoring. There is rise in integration of AI technology into coastal surveillance systems to enhance their ability to detect, analyze, and respond to maritime threats with greater accuracy and speed. Collaborations between governments and tech firms accelerate innovation and deployment, which is expected to present significant opportunities for the market growth.

MARKET CHALLENGES:

Integration Diverse Subsystems and Security Vulnerabilities Acts a Challenge for the Market

The integration of diverse sensors, legacy systems, and multi-vendor data formats creates interoperability issues, leading to data silos, inefficient agency sharing, and deployment delays with high customization costs. Moreover, these interconnected networks simultaneously expose systems to cybersecurity threats such as hacking, and data manipulation.

COASTAL SURVEILLANCE MARKET TRENDS:

Integration of Unmanned Aerial and Underwater Vehicles (UAVs/UUVs)

Unmanned systems such as drones and underwater vehicles are increasingly integrated into coastal surveillance for extended coverage beyond fixed sensors. UAVs provide real-time aerial imagery and rapid deployment to verify radar detections, while UUVs monitor underwater threats and seabed activities in shallow coastal zones. This trend reduces personnel risk, lowers operational costs, and enables persistent surveillance in harsh or remote areas.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Rising Sensor Innovations and Multi-Sensor Fusion Drives Sensors Segment Growth

By component, the market is segmented into sensors, command and control subsystems, and others. The sensors are further divided into Radars, Automatic Identification System (AIS), electro optics, radio direction finers, and VHF radio. Moreover, the command and control subsystems include Remote Operating Stations (ROS), Joint Operations Centers (JOC), and sensor fusion and software platforms. The others sub-segment comprises of electronic warfare support measures, detection sonar systems, and others.

The sensors segment holds the largest coastal surveillance market share driven by increasing demand for early threat detection and real-time monitoring across expansive Exclusive Economic Zones (EEZs). Advances in radar, electro-optical/infrared (EO/IR), and acoustic sensors provide enhanced target accuracy and extended detection ranges, critical for addressing diverse maritime threats including small high-speed boats and underwater incursions.

Command and control systems is the fastest growing segment and its growth is fueled by the necessity for integrated maritime domain awareness, accurate data from disparate sensor networks into cohesive operational pictures. Moreover, the increasing complexity of coastal security operations requires sophisticated software platforms with AI-driven analytics, enabling rapid decision-making and multi-agency coordination.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Demand for Real-Time Situational Awareness Demand for Surveillance & reconnaissance Segment

Based on application, the market is segmented into surveillance & reconnaissance, search & rescue, command & control (C2), border protection, environmental monitoring, and others.

Surveillance & reconnaissance will remain the largest application segment as it is the core mission of coastal surveillance, directly tied to continuous monitoring of EEZs, vital sea lanes, and critical coastal infrastructure. Defense and homeland security agencies prioritize wide-area situational awareness against smuggling, piracy, and asymmetric threats, driving sustained investment in long-range radars, EO/IR sensors, and AIS integration.

Environmental monitoring is expected to be the fastest-growing application as governments and regulators tighten oversight on marine pollution, offshore energy projects, and climate-related coastal risks. Coastal surveillance infrastructure is increasingly repurposed to track oil spills, illegal dumping, fishing activity, and coastal erosion, creating increased demand for the market.

By Platform

Investment in Fixed Infrastructure & Control Systems Support Fixed Segment Growth

Based on platform, the market is segmented into fixed and mobile.

Fixed platforms account for the majority of spending because shore-based radar sites, sensor towers, and permanent command centers form the backbone of national coastal surveillance architectures. They provide persistent 24/7 coverage over high-priority coastlines and approaches to major ports, with high reliability and long service life.

Mobile platforms, including vehicle-mounted systems, UAVs, patrol craft payloads, and quickly deployable sensor kits, are projected to grow fastest as users seek flexibility to cover blind spots and emerging hotspots. These solutions enable rapid response, event-based surveillance, and temporary coverage for high-risk operations without the cost and lead time of new fixed installations. In addition, advances in unmanned systems, compact radars, and secure mobile communications further propel the mobile platforms demand.

By End User

Increase in Defense Budget and Increasing Naval Modernization Drive Navy Segment Growth

Based on end user, the market is segmented into navy, coast guards, port authorities, and commercial infrastructure operators.

Navy holds the largest coastal surveillance market share, as maritime domain awareness is central to naval strategy, fleet protection, and blue-water operations. Naval forces typically lead national programs, own the main command centers, and integrate coastal surveillance feeds with wider C4ISR and fleet management systems. High defense budgets, complex mission profiles, and requirements for integrated radar, EW, and ISR suites is expected to support segment growth.

Coast guards are expected to be the fastest-growing end-user segment as responsibilities for law enforcement, SAR, anti-smuggling, and fisheries protection expand. Many countries are professionalizing and re-equipping their coast guards, shifting routine coastal security and civil missions.

Coastal Surveillance Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific Coastal Surveillance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America dominates the market with the largest revenue share, driven by substantial U.S. defense budgets exceeding for Navy and Coast Guard modernization programs. The U.S. Coast Guard uses advanced AESA radars, AI analytics, and unmanned systems to counter narcotics trafficking, illegal immigration, and piracy along extensive coastlines. Moreover, the huge investments in satellite surveillance in the region to enhance monitoring for regional maritime domain awareness drives market growth.

Europe

Europe holds a significant market position, fueled by established defense contractors such as Thales Group and Kongsberg Gruppen. In addition, the strong initiatives made by European Union (EU) for maritime border security fuels further growth. The U.K., France, and Germany invest heavily in hybrid EO/radar systems and quantum-resistant cybersecurity to protect North Sea trade routes and Mediterranean migration challenges.

Asia Pacific

Asia Pacific emerges as the fastest-growing region with a highest CAGR, propelled by escalating geopolitical tensions in the South China Sea and Indian Ocean. China and India are experiencing massive naval expansions. Moreover, these countries are deploying national-scale radar chains and AI-enhanced surveillance for enhanced security.

Latin America

Latin America represents an emerging market with moderate growth, primarily driven by Brazil and Mexico's efforts to combat drug trafficking via coastal radar networks and UAV patrols. Budget constraints limit large-scale deployments, however the increasing maritime trade through Panama Canal is driving investments in port security and Exclusive Economic Zone (EEZ) monitoring.

Middle East & Africa

The Middle East & Africa exhibits steady growth, due to increase in demand for surveillance systems for coastlines and investments in integrated surveillance to protect strategic chokepoints such as the Strait of Hormuz. Saudi Arabia and UAE deploy advanced EO/IR systems and command centers during regional instability. The threats from counter-terrorism and IUU fishing initiatives is also expanding market opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Innovation, Integration of AI, and Product Upgrade Drive Competitive Dynamics in the Market

The market is characterized by companies, including Thales Group (France), Raytheon Technologies Corporation (US), Lockheed Martin Corporation (U.S.), and others. These firms offer integrated surveillance solutions such as coastal radars, electro-optical/infrared sensors, AIS systems, command and control platforms, and AI-powered analytics software. Market leaders pursue continuous innovation and development of high-performance, scalable systems to meet escalating demands from naval forces, coast guards, port authorities, and maritime security sectors.

In addition, to strengthen their market position, key players are making strategic investments in R&D, collaborations with defense research institutions, and adoption of advanced cybersecurity technologies to ensure robust, reliable, and precise threat detection in challenging maritime environments.

LIST OF KEY COASTAL SURVEILLANCE COMPANIES PROFILED:

- Thales Group (France)

- Raytheon Technologies Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Kongsberg Gruppen ASA (Norway)

- Elbit Systems Ltd. (Israel)

- Saab AB (Sweden)

- Indra Sistemas S.A. (Spain)

- BAE Systems (U.K.)

- Leonardo S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS:

- July 2025: Blue Cloud Softech Solutions (BCSSL) won a USD 9.36 million contract via a U.S. client for developing and implementing a customized coastal surveillance system along South America's coastline over 18 months.

- May 2025: European Union proposed establishment of a dedicated “Black Sea Maritime Security Hub” to offer real-time, space-to-seabed monitoring and early-warning capability.

- May 2025: Odisha Police (India) initiated procurement of drones for coastal surveillance covering the state’s 480 km coastline. The drone-based aerial monitoring system will complement marine police stations,

- February 2025: Saab launched the Coast Control Radar, a next-generation phased-array, non-rotating, software-defined radar for coastal surveillance.

- February 2025: IAI ELTA unveiled the “C‑catcher (ELM-2025)” airborne surveillance radar system at IDEX/NAVDEX, a multi-mode AESA maritime-surveillance radar designed for maritime patrol aircraft.

REPORT COVERAGE

The global coastal surveillance market analysis provides an in-depth study of market size & forecast by all the segments included in the report. It includes details on the market dynamics, and trends expected to drive the market in the forecast period. The report includes Porter’s five forces analysis which illustrates the potency of buyers and suppliers in the market. The forecast also offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. Furthermore, the analysis also encompasses detailed competitive landscape with information on the market share and profiles of key major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Application, Platform, End User, and Region |

|

By Component |

· Sensors o Radars o Automatic Identification System (AIS) o Electro Optics o Radio Direction Finers o VHF radio · Command and Control Subsystems o Remote Operating Stations (ROS) o Joint Operations Centers (JOC) o Sensor Fusion and Software Platforms · Others |

|

By Application |

· Surveillance & Reconnaissance · Search & Rescue · Command & Control (C2) · Border Protection · Environmental Monitoring · Others |

|

By Platform |

· Fixed · Mobile |

|

By End User |

· Navy · Coast Guards · Port Authorities · Commercial Infrastructure Operators |

|

By Geography |

· North America (By Component, Application, Platform, End User, and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Component, Application, Platform, End User, and Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Component, Application, Platform, End User, and Country) o China (By End User) o Japan (By End User) o India (By End User) o South Korea (By End User) o Rest of Asia Pacific (By End User) · Latin America (By Component, Application, Platform, End User, and Country) o Brazil (By End User) o Mexico (By End User) o Argentina (By End User) o Rest of Latin America( By Platform) · Middle East & Africa (By Component, Application, Platform, End User, and Country) o UAE (By End User) o Saudi Arabia (By End User) o South Africa (By End User) o Rest of the Middle East & Africa (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 26.40 billion in 2025 and is projected to reach USD 49.36 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 9.17 billion.

The market is growing at a CAGR of 7.2% during the forecast period.

The sensors segment led the market by component in 2025.

The key factors driving the market are growth of market are increasing maritime security requirements.

Thales Group (France), Raytheon Technologies Corporation (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.) and among others are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us