Maritime Patrol Aircraft Market Size, Share & Industry Analysis, By Type (Armored and Unarmored), By Platform Class (Heavy Jet MPA (Turbofan), Medium Turboprop MPA, Light Turboprop/Business-twin Conversions, Amphibious/Seaplane MPA, and MALE UAV MPA), By Solution (OEMs and Retro Fit/Upgradation), By Systems (Sensors, Communication/Data Links Systems, Armament Interfaces, Self-Protection Systems, Navigation/Avionics Systems, and Others), By Application (Surveillance and Reconnaissance, Combat Support, Search and Rescue, and Coastal Patrolling), and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

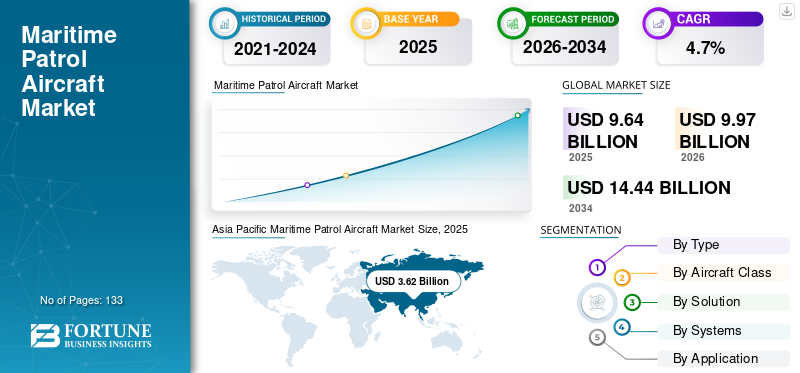

The global maritime patrol aircraft market size was valued at USD 9.64 billion in 2025. The market is projected to grow from USD 9.97 billion in 2026 to USD 14.44 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the maritime patrol aircraft market with a industry share of 37.55% in 2025.

Maritime patrol aircraft are a class of fixed-wing aircraft designed particularly to operate for hours over open ocean and coastal waters. These multi-mission platforms differ fundamentally from mainstream military aircraft in terms of their architecture, accommodating long endurance, advanced sensor integration, and comfort for the crews for sustained operations. An MPA is a dedicated platform that can house a number of crew members along with relief flight crew for comfortable operations extending for many hours with, very often, in-flight refueling possibilities. These aircraft typically feature pressurized, environmentally controlled cabins and are equipped with expansive payloads to carry sophisticated mission systems and weaponry.

Beyond traditional military applications, maritime patrol aircraft are now addressing an increasingly diverse range of operational requirements. Maritime law enforcement missions, such as anti-piracy operations, counter-smuggling, counter-drug trafficking, and illegal immigration prevention, have gained increasing prominence.

- For instance, in July 2025, L3Harris Technologies provided the initial refurbished P-8A Poseidon aircraft to the Naval Air Systems Command (NAVAIR), aiding in the U.S. Navy's readiness objectives. The company expects to induct as many as nine aircraft in the first year of the contract. Currently, L3Harris is refurbishing seven aircraft, all of which are scheduled for delivery within this year.

Piracy and maritime crime also pose sustained security challenges that drive MPA demand in various global regions. The Gulf of Aden continues to face episodic piracy threats, requiring sustained maritime surveillance operations. The piracy and complex maritime security challenges of the Gulf of Guinea include illicit fishing and oil infrastructure disruption, keeping persistent demand for the cost-effective maritime surveillance and interdiction platforms, further accelerating the global market growth.

The players in the maritime patrol aircraft market size are consolidated with holding exceptional market share by major key players such as The Boeing Company (U.S.), Airbus SE (France), Leonardo S.p.A. (Italy), Kawasaki Heavy Industries, Ltd. (Japan), and Lockheed Martin Corporation (U.S.), among others are top players in the market.

Download Free sample to learn more about this report.

Maritime Patrol Aircraft Market Key Takeaways

- 2025 Market Size: USD 9.64 Billion

- 2026 Market Size: USD 9.97 Billion

- 2034 Forecast Market Size: USD 14.44 Billion

- CAGR: 4.7% from 2026–2034

- Asia Pacific dominated the maritime patrol aircraft market with a 37.55% share in 2025.

- The unarmored segment accounted for a 73.52% share in 2025.

- The surveillance & reconnaissance segment held a 42.27% share in 2025.

Asia Pacific

Asia Pacific generated USD 3.62 billion in 2025 and is projected to reach USD 5.94 billion by 2034.

North America

North America remains a key market, supported by sustained investments in maritime surveillance, fleet modernization, and defense procurement programs.

Europe

Europe generated USD 2.05 billion in 2025 and is projected to reach USD 2.86 billion by 2034.

U.S.

Continued investments in the P-8A Poseidon fleet, including aircraft procurement and long-term sustainment programs.

Japan

Rising investments in maritime surveillance and regional security are supporting demand for advanced maritime patrol aircraft.

Read More

MARKET DYNAMICS

Market Driver

Accelerating Defense Budget Allocations toward Naval Modernization Drives Market Growth

The market is witnessing continued demand acceleration propelled by escalating territorial disputes in strategically relevant oceanic territories. The South China Sea is the hotspot of these disputes, where conflicting territorial claims among China, Philippines, Vietnam, and other Southeast Asian nations have driven significant MPA acquisition programs. Further, piracy and maritime terrorism are long-term operational drivers witnessed to sustain MPA demand over the coming years in various parts of the world.

The threats of Somali piracy in the Gulf of Aden continue to demand coordinated maritime surveillance operations from international coalitions. It is the sustained defense spending increase, especially concentrated within regional emerging economies, that provides essential financing mechanisms for substantial MPA fleet expansions.

- For instance, in October 2025, India's Defense Ministry issued a Request for Proposal for 15 C-295, configured as maritime patrol aircraft for Navy and Coast Guard operations, representing a capital investment of USD 3.5 billion in maritime surveillance infrastructure.

Market Restrain

Complex Procurement Bureaucracy and High Operational and Maintenance Cost Hinders Market Growth

The maritime patrol aircraft industry faces serious operational constraints related to long procurement cycles in defense, marked by regulatory complexity, many layers of approval, and long development-to-delivery timelines. Long gestation periods in defense procurement present significant challenges to capital expenditure planning for naval forces, which have to weigh the risk of rapid obsolescence of technology against fiscal constraints and budgetary competition for rival defense priorities.

The lifecycle cost of a maritime patrol aircraft-which includes acquisition, operation, maintenance, and personnel training-threatens defense budgets and hampers fleet modernization efforts. The specialized nature of MPA mission systems, integrating sophisticated sensors, acoustic processing equipment, communication suites, and weapons integration, demands highly trained maintenance personnel and specialized maintenance facilities equipped with advanced diagnostic and calibration equipment, thus limiting maritime patrol aircraft market growth.

Market Opportunities

Growing Adoption of Unmanned and Autonomous Maritime Patrol System Development Catalyze Market Opportunities

Emerging technological capabilities in autonomous aerial systems and long-endurance unmanned platforms create transformative market opportunities that will enable extended surveillance persistence while reducing pilot fatigue and the risk of operational exposure. Integrating hybrid-electric and sustainable propulsion technologies creates further, differentiated market positioning opportunities as environmental regulation and operational sustainability requirements reshape platform design considerations.

- For instance, in August 2025, India's DRDO launched an indigenous High-Altitude Long-Endurance (HALE) UAV development program with the objective of achieving performance parity with MQ-9B platforms to bridge strategic capability gaps created by limited procurement allocations for MQ-9B aircraft (31 aircraft distributed across Navy, Air Force, and Army).

These autonomous platform developments fundamentally alter the acquisition economics, enabling the procurement of multiple extended-endurance systems that support continuous coverage patterns. This emerging market opportunity presents itself for those OEMs that develop autonomous mission system architectures compatible with existing naval command-and-control infrastructure.

Maritime Patrol Aircraft Market Trends

Advanced Sensor Fusion and Artificial Intelligence Integration Leading To Directly Support Maritime Domain Awareness

The sector is at the core of its transformation, where sensor integration in multi-modalities and machine learning algorithms allow for previously unimaginable threat detection, classification, and engagement decision support. Artificial intelligence-enabled radar systems using convolutional neural networks achieve up to seven-fold improvement in object localization compared to conventional classical methods, fundamentally amplifying detection accuracy and operational effectiveness.

Multi sensor fusion architectures integrating optical, thermal, radar, and acoustic sensors through neural network processing create unified operational pictures from disparate data streams, enabling operators to maintain comprehensive environmental situational awareness across contested maritime zones. These sensor fusion capabilities directly support maritime domain awareness missions by enabling automated threat classification, reducing operator cognitive workload during extended surveillance operations, and improving the quality of engagement decisions through physics-informed AI processing of complex oceanographic and atmospheric phenomena affecting acoustic and electromagnetic sensor performance.

Predictive analytics and machine learning together enable proactive maritime security by identifying new threat patterns and vessel behavior anomalies indicative of smuggling, piracy, or illegal fishing. Machine learning algorithms in autonomous maritime systems perform real-time map creation, identification, and classification of objects underwater, and perform real-time route planning for networked patrol assets independently. This, in turn, is expected to fuel market growth through the forecast period.

Market Challenges

Regulatory Compliance and Interoperability Standards Integration Complexity Hinders Market Growth

The integration complexity in ensuring compatible command-and-control architectures, data link protocols, and sensor-to-shooter integration across multinational operating environments places a substantial engineering burden on platform developers. India's Defense Procurement Procedure lays down strict offset and technology transfer requirements pertaining to domestic production participation and the incorporation of indigenous technology as preconditions to foreign defense system procurement thereby directly constraining MPA platform standardization and supply chain economies of scale.

Exporting MPA platforms to international customers requires navigating complex technology transfer regulations, as well as bilateral security agreements and third-party flag-state protocols, significantly extending acquisition timelines and introducing diplomatic coordination requirements.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Cost Effectiveness and Growing Demand for Surveillance Application Anticipate Segmental Growth

The global market by type segment is further classified into armored and unarmored

The unarmored segment captures the largest share of market revenue valued at USD 7.09 billion in 2025 with market share of 73.52%. In addition the segment is estimated to be the fastest growing during the forecast period with highest CAGR of 5.2%. The growth is driven fundamentally by superior cost-effectiveness, lower operational expense profiles, and versatile capability architecture addressing peacetime maritime surveillance requirements across global defense establishments. In addition, unarmored platforms provide substantially lower acquisition costs compared to armed variants, with unit procurement prices potentially 30-40% below equivalent armed configurations through the elimination of armor protection systems, integrated weapons pylons, and associated hardening modifications.

- For instance, in August 2023, the fourth and final P-8A Poseidon aircraft arrived at the Royal New Zealand Air Force’s (RNZAF) Base Ohakea. The Poseidon fleet is set to perform multiple roles, such as aerial surveillance, resource protection, disaster relief, and search and rescue missions, working alongside partners in the Pacific.

The segment of armored witnessed moderate growth in the market includes platforms with integrated weapons systems, armor protection, and anti-surface/anti-ship engagement capabilities, showing the steady growth CAGR during the forecast period due to fundamental transformation in global maritime security threat perceptions and tactical requirements.

By Aircraft Class

Exceptional Growth Trajectory and Autonomous Operations Advantages of MALE UAVs Catalyze Segmental Growth

The market by aircraft class segment is further classified into Heavy Jet MPA (Turbofan), medium turboprop MPA, light turboprop/business-twin conversions, and MALE UAV MPA.

The segment of MALE UAV maritime patrol shows the fastest CAGR in the aircraft class segmentation, at highest CAGR of 5.8% up through 2034, as artificial intelligence-enabled autonomy matures and manned-unmanned teaming operational viability gets validated through military exercises and operational deployments. MALE UAV maritime patrol platforms ultimately record continued growth in the market place with technological maturation that enables extended endurance greater than 30 hours without refueling and cost-effectiveness at total system costs ranging.

- For instance, in November 2025, Singapore plans to enhance its unmanned surveillance capabilities by substituting its Elbit Systems Hermes 450 fleet with the larger and more advanced Hermes 900 model after thorough evaluations of maritime patrol aircraft.

The Heavy Jet MPA (Turbofan) segment holds established market dominance with 47.24% market share in 2025. Its market dominance represents the most operationally capable and combat-proven maritime patrol solutions available globally. Heavy jet-powered platforms offer turbofan engine propulsion systems that allow cruise velocities over 500 knots, facilitating rapid deployment to emerging maritime crises, extended operational ranges over 4,000 nautical miles supporting trans-oceanic patrol missions, and superior high-altitude performance characteristics enabling sustained surveillance at 25,000-30,000 feet operational ceilings.

By Solution

Comprehensive Mid-Life Extension, Sensor System Integration, and Technological Advancement Preservation Drives Retrofit/Upgradation Segment Growth

The global market by solution segment is further classified into OEMs and retro fit/upgradation.

The retrofit/upgradation segment presents the fastest CAGR within market solutions. It is due to recognition that cost-effective modernization programs could extend existing aircraft service lives to represent a substantially more economical approach than any complete platform replacement. Mid-life upgrade programs extend structural service life. Equally, modern retrofit architecture is introducing next-generation detection and targeting capabilities through new antennas, sensors, and software enhancements to computer processing, communications, and situational awareness systems that enable aircrews to detect, identify, and target advanced submarines with unprecedented precision.

- For instance, in September 2025, the first upgraded P-3B Orion aircraft of the Hellenic Navy successfully carried out its initial test flight, signifying a significant achievement in the Mid-Life-Upgrade (MLU) Program. The flight confirmed the functionality of the aircraft’s onboard systems, including its advanced glass cockpit and mission data interfaces, which will improve the Hellenic Navy’s capabilities in maritime surveillance and anti-submarine warfare.

Original equipment manufacturer services and support demonstrate a high growth trajectory, underpinned by strategic OEM expansion to aftermarket services, utilizing intellectual property control and proprietary maintenance data repositories, ensuring the capture of growing sustainment revenues throughout aircraft operational life.

By Systems

Countermeasure Dispensing Systems and Electronic Warfare Integration Drives Market Growth

The global market by systems segment is further classified into sensors, communication/data links systems, armament interfaces, self-protection systems, navigation/avionics systems, and others.

The self-protection systems sub-segment realizes the highest compound annual growth rate within the segmentation of such systems, driven by increasing awareness that maritime patrol aircraft operating in contested or high-threat maritime environments require comprehensive protection against anti-aircraft fire, missile debris, and hostile engagement scenarios. The architecture of Saab's countermeasure dispensing systems is industry-leading self-protection technology, including electromechanical BOL (Ballistic On-board Launcher) systems with intelligent counter-RF and counter-IR threat capabilities in pre-emptive and reactive dispensing modes, coupled with pyrotechnical BOP (Ballistic On-board Pod) dispensers providing chaff and flare countermeasures at optimized effectiveness against radar and infrared guided threats.

The sensors sub-segment has dominance in the market positioning within systems used in maritime patrol aircraft, with the largest revenue contribution that is driven by basic operational need for comprehensive environmental surveillance, threat detection, and identification in diversified oceanic operational environments.

By Application

Escalating Geopolitical Tensions and Territorial Disputes Increasing Activity of Surveillance and Reconnaissance

The global market size by application segment is further classified into surveillance and reconnaissance, combat support, search and rescue, and coastal patrolling.

The surveillance and reconnaissance sub-segment is the largest and one of the fastest-growing segments of the global market, and accounted for about 42.27% market share in 2025 and reflecting the highest growth trajectory throughout the forecast period. That dominance reflects fundamental shifts in priorities within maritime security, the integration of technological advancement, and changing geopolitical dynamics that are raising demands for improved maritime domain awareness capabilities across territorial waters and exclusive economic zones worldwide. The intensification of geopolitical rivalries and territorial contests across critical maritime regions has fundamentally transformed surveillance and reconnaissance into the cornerstone application for the deployment of maritime patrol aircraft.

- In November 2025, Airbus Defense and Space delivered two C295 Maritime Surveillance Aircraft to Angola, completing a landmark contract that established Angola as the first African nation to operate the C295 in dedicated maritime surveillance configuration.

Combat support is the second-biggest application category in the market, representing a significant market presence due to evolving global security dynamics and the operational imperative for the naval forces to project power, protect maritime interests, and maintain sea control across contested operational environments. This segment includes anti-submarine warfare, anti-surface warfare, naval fire support, and maritime strike operations, among other critical mission sets that enable maritime patrol aircraft to function as force multipliers within integrated naval task forces.

Maritime Patrol Aircraft Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America

Asia Pacific

Asia Pacific Maritime Patrol Aircraft Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the largest market share in global maritime patrol aircraft market share driven by unprecedented territorial contestation, exclusive economic zone imperatives to control, and accelerating naval modernization programs among regional powers. The region commanded a market value of approximately USD 3.62 billion in 2025 and is projected to reach approximately USD 5.94 billion by 2034, representing the fastest-growing regional segment with a CAGR potentially 5.8% through the forecast period. China accounts for the largest regional market revenue, while India, Japan, and South Korea collectively represent emerging tier-one procurement drivers establishing sustained market growth momentum. Vast exclusive economic zones extending across contested maritime corridors raise the imperative for extended-endurance maritime patrol capabilities that allow for persistent surveillance across oceanic territories spanning millions of square kilometers.

- For instance, in July 2025, South Korea will be receiving six Boeing P-8A Poseidon aircraft, which is regarded as a strategic watershed event to change region-wide submarine detection capabilities and establish interoperability on platforms with U.S. Navy assets throughout the Indo-Pacific.

North America

North America projected second-fastest growth in global market dominance through U.S. Navy fleet strength and expanding allied procurement commitments, positioning the region for sustained growth despite mature P-8A Poseidon market penetration.

The U.S. Navy awarded Boeing a contract modification in November 2024 worth USD 1.68 billion for seven additional Lot 13 P-8A Poseidon aircraft, participating in foreign military sales with both Canada and Germany, extending the completion of work until September 2030. This buy reflects the commitment of the U.S. Navy to maintaining a robust maritime patrol presence across multiple global theaters in support of both allied Five Eyes platform standardization and NATO defense integration requirements. In addition, The U.S. Navy had also awarded Naval Supply Systems Command Weapon Systems Support (NAVSUP WSS) a five-year firm-fixed-price contract worth USD 54.7 million in October 2025 for the repair, overhaul, and upgrade of 351 various commercial components used throughout the P-8A fleet through June 2030 to ensure the availability of critical parts and continued fleet readiness in its mid-life sustainment period.

Europe

The market size in Europe demonstrates significant growth momentum, with a projected CAGR of 3.9% from 2026 to 2034, with valued USD 2.05 billion in 2025 to a market valuation of USD 2.86 billion, driven by factors such as increased maritime security threats, increasing defense expenditures, and technological advancements across allied nations. The U.K., France, Germany, and Italy together anchor the European MPA market, as the increased allocation of the defense budget supports aircraft procurement and modernization under the European Defense Fund and NATO strategic initiatives.

Middle East & Africa

The Middle East market continues its measured but strategic growth driven by Persian Gulf security imperatives, exclusive economic zone protection requirements, and emerging maritime infrastructure expansion throughout the Arabian Peninsula and Levantine regions. Saudi Arabia formally commenced negotiations with Leonardo over maritime patrol aircraft procurement for strategic enhancement of the Kingdom's maritime domain awareness and anti-submarine warfare (ASW) capabilities, driven by the strategic competition in the Persian Gulf, maritime chokepoint security concerns, and newly emerging regional naval capabilities among competitors.

Latin America

The Latin American market for maritime patrol aircraft reflects moderate growth, constrained by the imperatives of protecting the Exclusive Economic Zone (EEZ), the need to interdict with illegal fishing, and aspirations toward submarine-based power projection emerging among regional maritime powers. Strategic naval modernization pursued by Brazil focuses on a "Blue Amazon" surveillance framework, encompassing a wide range of maritime platforms such as Offshore Patrol Vessels, Scorpène-class submarines, and an aircraft carrier capability to be used in projecting power across extensive Atlantic maritime approaches and the strategic region of the South Atlantic.

Competitive Landscape

Key Market Players

Market Leadership and Dominant Platform Positioning By Major Key Players Leads Market Growth

The competitive landscape remains dynamic, with established platform manufacturers leveraging installed base advantages, comprehensive sustainment infrastructure, and continuous technology integration to maintain market leadership against emerging competitors pursuing cost-based differentiation strategies targeting resource-constrained defense establishments. Geopolitical tensions, territorial disputes, maritime security threat proliferation, and sustained defense budget allocations toward naval modernization have created favorable market conditions that support multiple competitive platforms addressing diverse operational requirements, capability specifications, and economic constraints across a global customer base.

- For instance, in February 2025, the French Defense Procurement Agency (Direction Générale de l'Armement) has signed a contract with Airbus Defense and Space, collaborating with Thales, to conduct a risk-assessment study for the upcoming maritime patrol aircraft initiative.

Alliance standardization imperatives, interoperability requirements, and network-centric warfare doctrines, however, create competitive advantages for platforms achieving critical adoption mass among allied nations, thereby reinforcing Boeing P-8A Poseidon market dominance while constraining alternative platform penetration opportunities absent compelling technological differentiation or substantial cost advantages.

List of Key Maritime Patrol Aircraft Companies Profiled

- The Boeing Company (U.S.)

- Airbus SE (France)

- Leonardo S.p.A. (Italy)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Lockheed Martin Corporation (U.S.)

- Embraer S.A. (Brazil)

- Saab AB (Sweden)

- Textron Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- RTX Corporation (U.S.)

- Thales Group (France)

- L3Harris Technologies, Inc. (U.S.)

- HENSOLDT AG (Germany)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- General Dynamics Corporation (U.S.)

- BAE Systems plc (U.S.)

- Honeywell International Inc. (U.S.)

- Hindustan Aeronautics Limited (HAL) (India)

KEY MARKET DEVELOPMENTS

- November 2025: Boeing announced a new contract with Australian company AW Bell for castings supporting 737 and 777 programs, including commercial derivatives such as the P-8 Poseidon. The contract represents Boeing's participation in the Australian Government's Global Supply Chain Program, supporting high-tech jobs and establishing pathways for small and medium-sized enterprises to participate in Boeing's global business following RAAF's receipt of its thirteenth maritime patrol aircraft.

- October 2025: The U.S. Navy inducted the first upgraded P-8A Poseidon maritime patrol aircraft under a contract awarded on September 30, 2024, for support to 139 P-8A aircraft. L3Harris's contract for maintenance covers structural refurbishment, avionics upgrade, systems testing, and component overhauls, with as many as nine aircraft slated for overhaul in the first contract year running through 2029. The July 2025 delivery of the first overhauled aircraft marked the first instance of depot-level MRO completion under the contract.

- October 2025: The Indian Ministry of Defense issued a formal Request for Proposal to the Tata Advanced Systems-Airbus joint venture for the supply of 15 C-295 maritime patrol aircraft valued at approximately USD 3.5 billion. The RFP requires nine in the Medium-Range Maritime Reconnaissance configuration for the Indian Navy and six in the Multi-Mission Maritime Aircraft configuration for the Indian Coast Guard, with most of the manufacturing being done at Vadodara Final Assembly Line under the Make in India framework, targeting up to 78% indigenous content.

- August 2025: Terma and Boeing inked a Memorandum of Understanding to explore cooperation regarding Maintenance, Repair, and Overhaul support for P-8 maritime patrol aircraft in Denmark. Announced at DALO Industry Days, the agreement aims to explore options for a dedicated P-8 MRO capability in Denmark while supporting national defense readiness through industrial collaboration and robust sustainment services.

- August 2025: India took delivery of the final C-295 military transport aircraft from Spain on August 2, 2025, two months in advance, in an important milestone to boost India's defense capabilities. Of the 56 aircraft ordered by India in a deal valued at USD 2.5 billion, 16 were delivered from Spain, while the remaining 40 are to be manufactured in India by Tata Advanced Systems, Vadodara facility, in the first Make in India project in the defense aircraft sector.

REPORT COVERAGE

The global maritime patrol aircraft market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.7% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Type · Armored · Unarmored By Aircraft Class · Heavy Jet MPA (Turbofan) · Medium Turboprop MPA · Light Turboprop/Business-twin Conversions · MALE UAV MPA By Solution · OEMs · Retro Fit/Upgradation By Systems · Sensors · Communication/Data Links Systems · Armament Interfaces · Self-Protection Systems · Navigation/Avionics Systems · Others By Application · Surveillance and Reconnaissance · Combat Support · Search and Rescue · Coastal Patrolling By Region

· U.S. (By Solution) · Canada (By Solution)

· U.K. (By Solution) · Germany (By Solution) · France (By Solution) · Russia (By Solution) · Nordic Countries (By Solution) · Rest of Europe (By Solution)

· China (By Solution) · India (By Solution) · Japan (By Solution) · South Korea (By Solution) · Australia (By Solution) · Rest of Asia Pacific (By Solution)

· Israel (By Solution) · Iran (By Solution) · United Arab Emirates (By Solution) · Saudi Arabia (By Solution) · South Africa (By Solution) · Rest of the Middle East & Africa (By Solution)

· Brazil (By Solution) · Argentina (By Solution) Rest of Latin America (By Solution) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.64 billion in 2025 and is projected to reach USD 14.44 billion by 2034.

In 2024, the market value stood at USD 3.16 billion

The market is expected to exhibit a CAGR of 4.7% during the forecast period.

The MALE UAV MPA sub-segment is expected to hold the highest CAGR over the forecast period.

Escalating geopolitical tensions and territorial disputes emerging governments are accelerating defense budget allocations toward naval modernization drives the market growth.

The Boeing Company (U.S.), Airbus SE (France), Leonardo S.p.A. (Italy), Kawasaki Heavy Industries, Ltd. (Japan), and Lockheed Martin Corporation (U.S.), among others are top players in the market.

Asia Pacific dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 133

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us