Special Mission Aircraft Market Size, Share & Industry Analysis by Point of Sale (OEM and Aftermarket), By Aircraft Type (Narrow-Body, Wide-Body, Regional Jet, and Turboprop Aircraft), By Mission Type (ISR (Intelligence, Surveillance, Reconnaissance), Maritime Patrol & ASW (Anti-Submarine Warfare), Electronic Warfare (SIGINT/ELINT/COMINT), Airborne, Early Warning & Control (AEW&C), Search & Rescue/MedEvac/Firefighting, and Special Operations & Tactical Transport), By End-User (Defense & Military Forces, Homeland Security), and Regional Forecast, 2026-2034

Special Mission Aircraft Market Size and Future Outlook

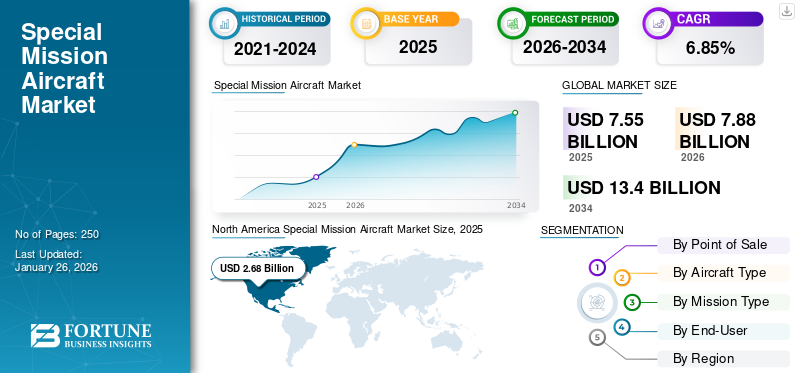

The global special mission aircraft market size was valued at USD 7.55 billion in 2025 and is projected to grow from USD 7.88 billion in 2026 to USD 13.40 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 6.85% during the forecast period. North America dominated the special mission aircraft market with a market share of 35.56% in 2025.

Special mission aircraft represent highly customized air platforms engineered to perform operations beyond conventional passenger or cargo transport roles. These aircraft are configured with mission-specific systems such as advanced radar, electro-optical sensors, communication suites, and electronic warfare equipment, enabling them to execute tasks including intelligence surveillance and reconnaissance (ISR), maritime patrol, search and rescue (SAR), electronic intelligence (ELINT), and medical evacuation (MEDEVAC). They serve as critical enablers for national defense, homeland security, and strategic response missions that demand persistent situational awareness and rapid deployment capability.

The market is expanding steadily driven by a confluence of defense modernization programs, evolving security threats, and rising importance of information-centric warfare. Heightened geopolitical tensions, especially across maritime and border regions, have intensified the demand for special mission aircraft capable of long-endurance surveillance and precision targeting. Furthermore, advancements in sensor fusion, AI-driven mission management systems, and satellite connectivity are enhancing operational efficiency, allowing these platforms to deliver real-time intelligence and interoperability across domains. Governments are increasingly focusing on replacing aging fleets with multi-role aircraft offering modular payload configurations, while civil applications such as environmental monitoring, disaster management, and firefighting further augment market potential.

A mix of established aerospace primes and specialized integrators defines industry leadership. Major players in the market, such as Boeing, Airbus Defence and Space, Lockheed Martin Corporation, Northrop Grumman Corporation, Saab AB, Leonardo S.p.A., and Textron Aviation, dominate through extensive product portfolios and upgrade programs. Collaborations between OEMs and system integrators such as Thales Group, L3Harris Technologies, and Elbit Systems continue to shape the competitive landscape, emphasizing modular architecture, multi-mission adaptability, and cost-effective fleet sustainment. Overall, the sector’s growth trajectory aligns closely with the global trend toward data-driven defense ecosystems and next-generation airborne intelligence capabilities.

Download Free sample to learn more about this report.

Special Mission Aircraft Market KEY TAKEAWAYS

- 2025 Market Size: USD 7.55 billion

- 2026 Market Size: USD 7.88 billion

- 2034 Forecast Market Size: USD 13.40 billion

- CAGR: 6.85% from 2026–2034

- North America dominated the special mission aircraft market with a 35.56% share in 2025.

- The OEM segment is projected to account for the largest market share of 87.08% in 2026.

- The narrow-body segment is expected to hold a leading market share of 41.57% in 2026.

North America

North America market was valued at USD 2.68 billion in 2025 and is projected to reach USD 2.77 billion in 2026.

Europe

Europe accounted for 19.15% of the global market in 2025, reaching USD 1.45 billion, and is expected to grow to USD 1.51 billion in 2026.

Asia Pacific

Asia Pacific represented 28.10% of global revenue in 2025 with a market value of USD 2.12 billion and is projected to reach USD 2.24 billion in 2026.

U.S.

U.S. The special mission aircraft market is projected to reach USD 2.65 billion by 2026.

Japan

Japan The Japan market is projected to reach USD 0.33 billion by 2026

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growing Demand for Real-Time Surveillance and Intelligence Capabilities to Propel Market Expansion

The primary driver for special mission aircraft market growth is the escalating need for persistent intelligence, surveillance, and reconnaissance (ISR) capabilities to ensure national security and operational readiness. Governments worldwide are prioritizing information dominance across land, air, and maritime domains to counter asymmetric warfare, border infiltration, and maritime incursions. The increasing complexity of hybrid threats has made ISR-equipped aircraft indispensable for early warning and decision superiority. Additionally, rising defense budgets in key economies have enabled the modernization of legacy fleets and the adoption of multi-role aircraft capable of conducting continuous intelligence operations. This heightened focus on situational awareness has become a core pillar of military transformation strategies across the globe.

- August 2024 – South Korea’s Defense Acquisition Program Administration (DAPA) announced a contract to procure additional surveillance aircraft to enhance the monitoring of North Korean military activity, reflecting an increasing investment in airborne ISR capabilities.

MARKET RESTRAINTS:

High Acquisition and Lifecycle Maintenance Costs to Constrain the Market

Despite their strategic importance, special mission aircraft programs are often constrained by high upfront procurement costs and long-term sustainment expenses. These platforms require extensive mission integration—custom avionics, multi-mode radars, and high-end sensor suites—that demand regular calibration and upgrades. Furthermore, maintaining operational readiness necessitates specialized technical teams and costly spare-part inventories, which strain defense budgets. Smaller nations face additional fiscal pressure in balancing modernization priorities with the maintenance of existing fleets. Consequently, many governments are exploring joint procurement and leasing models to offset capital expenditure.

- March 2025 – The Irish Department of Defence disclosed a spending of over EUR 1 million (USD 1.16 million) on maintenance for a single surveillance aircraft, sparking public debate about the sustainability of high-cost airborne assets in limited defense budgets.

MARKET OPPORTUNITIES:

Adoption of Modular Architecture and System Upgrade Flexibility to Offer Growth Opportunities

A significant market opportunity lies in the adoption of modular mission architectures that allow the easy integration or replacement of sensors, communication systems, and electronic warfare modules without requiring a full fleet replacement. This shift toward open-system designs enables aircraft to stay mission-relevant through incremental technology insertions while reducing downtime and lifecycle costs. Furthermore, such modularity promotes interoperability across allied forces and enhances adaptability for dual-use operations such as environmental monitoring or disaster management. OEMs are increasingly investing in scalable frameworks that can accommodate new payloads or mission types with minimal redesign.

- June 2025 – Boeing’s E-7 Wedgetail underwent its first flight with an upgraded surveillance sensor suite, demonstrating how modular systems can extend platform longevity and operational capability without requiring a new airframe.

SPECIAL MISSION AIRCRAFT MARKET TRENDS:

Integration of AI, Data Fusion, and Multi-Domain Connectivity to Act as a Major Technological Trend

The technological landscape of the market is rapidly, with an inclination toward AI-enabled mission systems, advanced sensor technology fusion, and network-centric operations. These aircraft are increasingly functioning as real-time data nodes, capable of autonomous threat detection, pattern recognition, and predictive analytics. The integration with satellite networks and ground command systems is enhancing the speed and precision of intelligence dissemination. The transition from isolated platforms to interconnected multi-domain networks reflects a broader push toward digitalized defense ecosystems. As AI models mature, they are expected to optimize resource allocation, target tracking, and decision cycles, significantly enhancing mission outcomes.

- September 2025 – The U.S. Department of Defense initiated the deployment of a next-generation satellite network aimed at linking air, space, and ground sensors into a unified command architecture, underscoring the move toward integrated multi-domain ISR operations.

MARKET CHALLENGES:

Skilled Workforce Shortage and Rapid Threat Evolution Present Threats to Market Growth

One of the most pressing challenges for this market is the shortage of trained personnel and technical specialists capable of operating, maintaining, and upgrading sophisticated mission systems. As the complexity of onboard avionics and electronic warfare suites increases, training pipelines struggle to keep pace. Simultaneously, adversaries are developing advanced countermeasures such as jamming, spoofing, and stealth tactics that challenge the operational effectiveness of existing platforms. The accelerated evolution of threats necessitates continual upgrades and adaptive training programs, placing additional strain on procurement and operational cycles. The ability to sustain technical readiness while responding to emerging threats remains a defining obstacle for both established and emerging operators.

- July 2025 – NATO officials highlighted capability gaps in training and electronic warfare resilience during joint air exercises, emphasizing the need for skilled human capital to exploit advanced ISR assets fully.

Download Free sample to learn more about this report.

Segmentation Analysis

By Point of Sale

OEM Segment Leads Driven by Fleet Modernization and Point of Sale Integration

On the basis of point of sale, the market is classified into OEM and aftermarket.

The OEM segment will account for a dominating market share with 87.08% in 2026. The OEM segment is expected to dominate the market during the forecast period, primarily due to large-scale fleet modernization programs and rising demand for mission-specific configurations. Defense forces and government agencies are increasingly procuring new aircraft platforms integrated with next-generation ISR, EW, and communication suites directly from original equipment manufacturers to ensure seamless mission readiness and technology standardization. OEMs are also investing heavily in modular architectures and digital twin-based lifecycle management, enabling clients to customize payloads while reducing integration risks.

Moreover, strategic collaborations between airframe producers and avionics suppliers are accelerating turnkey deliveries, making OEM-built platforms more cost-effective over the long term compared to extensive retrofits. This growing focus on indigenous manufacturing and self-reliant defense procurement further strengthens OEM dominance globally.

- May 2025 – Airbus Defence and Space secured a contract with Spain’s Ministry of Defence to deliver additional C295 maritime patrol aircraft equipped with next-generation mission systems, reinforcing OEM-led fleet modernization initiatives.

The aftermarket segment is poised to depict a CAGR of 4.10% over 2025 to 2032.

By Aircraft Type

Fleet Modernization and Multi-Mission Flexibility to Drive Narrow-Body Segment Growth

On the basis of aircraft type, the market is classified into narrow-body, wide-body, regional jet, and turboprop aircraft.

The narrow-body segment is projected to account for a dominating market share with 41.57% in 2026. The segment is projected to dominate the global special mission aircraft market share over the forecast period, supported by the rising demand for versatile, long-range, and cost-efficient platforms that can perform multiple mission profiles such as maritime patrol, ISR, and AEW&C. Governments and defense organizations are increasingly favoring narrow-body conversions—derived from proven commercial airframes such as the Boeing 737 and Airbus A320—owing to their balanced payload capacity, mission endurance, and established global maintenance ecosystem.

These aircraft provide the ideal middle ground between wide-body strategic assets and short-range turboprops, making them suitable for both large-scale defense operations and coastal surveillance missions. Additionally, their adaptability for modular mission systems and sensor integration is accelerating procurement decisions across NATO and Indo-Pacific countries.

- April 2025 – Boeing was awarded a USD 1.8 billion contract by the U.S. Navy for additional P-8A Poseidon maritime patrol aircraft, underscoring the sustained global demand for narrow-body platforms in ISR and anti-submarine warfare missions.

The regional jet segment is anticipated to expand at a CAGR of 6.56% over the forecast period.

By Mission Type

Rising Geopolitical Tensions to Fuel ISR Mission Segment Growth

On the basis of mission type, the market is classified into ISR (Intelligence, Surveillance, Reconnaissance); maritime patrol & ASW (Anti-Submarine Warfare); Electronic Warfare (SIGINT/ELINT/COMINT); Airborne Early Warning & Control (AEW&C); search & rescue/MedEvac/firefighting, and special operations & tactical transport.

The ISR (Intelligence, Surveillance, Reconnaissance) segment is expected to account for a dominating market share with 37.54% in 2026. The segment is expected to dominate the market during the forecast period, driven by the increasing emphasis on situational awareness, real-time intelligence, and cross-domain threat detection. Governments are investing heavily in ISR platforms to strengthen border surveillance, maritime domain awareness, and strategic reconnaissance in response to escalating regional conflicts and transnational security threats. The integration of advanced electro-optical sensors, synthetic aperture radars, and AI-enabled analytics has transformed ISR aircraft into data-driven assets capable of continuous monitoring and autonomous target identification. Furthermore, the growing shift toward network-centric warfare and multi-domain operations has reinforced the strategic necessity for modern ISR fleets. As defense forces replace aging reconnaissance aircraft with multi-role, long-endurance systems, the ISR segment will continue to outpace other mission categories in investment and deployment.

- June 2025 – The U.S. Air Force announced plans to expand its ISR fleet with next-generation platforms under its “Deep Look” modernization initiative. The move is aimed at enhancing global surveillance and targeting capabilities across contested environments.

To know how our report can help streamline your business, Speak to Analyst

The electronic warfare (SIGINT/ELINT/COMINT) segment is estimated to surge at a CAGR of 6.91% over the forecast period.

By End-User

Defense Modernization and Strategic Deterrence to Drive Military Segment Growth

Based on end-user, the special mission aircraft market is segmented into defense & military forces, homeland security, law enforcement and government, and civil & commercial.

The defense & military forces segment is estimated to hold a dominating position in 2026 with a share of over 67.36%. The segment is projected to remain the dominant end-user in the market throughout the forecast period, primarily due to ongoing modernization initiatives, increasing defense budgets, and the demand for enhanced situational awareness in multi-domain operations. Nations are investing in fleet renewal and next-generation mission systems to maintain air superiority and intelligence advantage in rapidly evolving threat environments. The integration of electronic warfare capabilities, AI-powered data analytics, and networked ISR systems is reshaping how militaries conduct surveillance, targeting, and tactical coordination. Additionally, the proliferation of regional conflicts and the strategic pivot toward deterrence in contested airspaces are compelling armed forces to expand their inventories of multi-role special mission aircraft. OEM collaborations with defense ministries to co-develop indigenous platforms are further strengthening this segment’s long-term growth outlook.

- April 2025 – The U.S. Department of Defense awarded Northrop Grumman a multi-year contract to enhance and expand its fleet of E-2D Advanced Hawkeye aircraft, reinforcing the focus on sustained airborne early warning and command capabilities.

The civil & commerce segment is anticipated to expand at a CAGR of 4.60% over the analysis period.

Special Mission Aircraft Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Special Mission Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 2.68 billion in 2025, capturing 35.56% of global revenue, and is estimated to reach USD 2.77 billion in 2026. North America remains the largest market for special mission aircraft, driven by strong defense budgets, active modernization programs, and technological leadership in ISR, electronic warfare, and early-warning systems. The U.S. Air Force and Navy continue to invest heavily in next-generation platforms integrating AI-driven analytics and multi-domain connectivity to maintain global dominance. Canada’s focus on Arctic surveillance and maritime patrol also contributes to regional demand. The presence of key OEMs such as Boeing, Lockheed Martin, and Northrop Grumman sustains a robust innovation ecosystem. The U.S. market is projected to reach USD 2.65 billion by 2026.

- May 2025 – The U.S. Air Force awarded Boeing a contract to upgrade its RC-135 Rivet Joint ISR fleet with advanced sensor and communication systems, reinforcing North America’s leadership in airborne surveillance modernization.

Europe

In 2025, Europe held 19.15% of the global market, reaching a valuation of USD 1.45 billion, and is projected to grow to USD 1.51 billion in 2026. Europe’s special mission aircraft market is witnessing strong growth driven by joint defense projects, border monitoring initiatives, and the modernization of existing fleets. The ongoing conflict in Eastern Europe has prompted NATO members to strengthen ISR and maritime patrol capabilities. Collaborative programs such as the Future Combat Air System (FCAS) and cross-border procurement of AEW&C and electronic intelligence aircraft are enhancing regional interoperability. Moreover, the European Union’s defense fund continues to support indigenous R&D and technology integration among member states. The UK market is projected to reach USD 0.17 billion by 2026, and the Germany market is projected to reach USD 0.02 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 2.12 billion in 2025, representing 28.10% of total market revenue, and is projected to reach USD 2.24 billion in 2026. The region is emerging as the fastest-growing due to escalating maritime disputes, cross-border surveillance needs, and increasing focus on indigenous defense manufacturing. Countries such as India, Japan, China, and South Korea are investing in ISR and maritime patrol aircraft to ensure domain awareness and strategic deterrence. Regional governments are also emphasizing technology transfer and local assembly partnerships with global OEMs to reduce dependence on foreign suppliers. The push for integrated, multi-role aircraft tailored for regional environments underpins this expansion. The Japan market is projected to reach USD 0.33 billion by 2026, the China market is projected to reach USD 0.27 billion by 2026, and the India market is projected to reach USD 0.27 billion by 2026.

Rest of the World

In the rest of the world, Latin America & Africa and the Middle East regions would witness moderate growth in this market. In 2025, Rest of the World generated USD 1.3 billion, contributing 17.19% to global market revenue, and is projected to grow to USD 1.37 billion in 2026. The regional growth is led by defense modernization, counter-terrorism operations, and border surveillance initiatives. The Middle Eastern nations are enhancing ISR and electronic warfare fleets to safeguard airspace amid regional instability, while African and Latin American countries are investing in cost-effective, multi-role aircraft for reconnaissance, disaster response, and internal security missions. Strategic partnerships with Western OEMs are facilitating technology transfer and fleet upgrades.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations and Technology Integration to Drive Market Leadership of Key Players

The global special mission aircraft market is characterized by a highly consolidated competitive landscape, with a few major aerospace and defense OEMs dominating through diversified mission portfolios, proprietary sensor technologies, and strong government partnerships. Leading players such as Boeing, Airbus Defence and Space, Lockheed Martin, Northrop Grumman, Saab AB, Leonardo S.p.A., and Textron Aviation command significant market share by delivering multi-role, modular platforms tailored for ISR, electronic warfare, maritime patrol, and airborne early warning operations. These OEMs maintain a competitive edge through continuous innovation in sensor fusion, AI-driven mission systems, and open architecture integration, enabling flexible upgrades and reduced lifecycle costs. System integrators such as Thales Group, L3Harris Technologies, and Elbit Systems complement this ecosystem by providing advanced avionics, communication suites, and data analytics capabilities that enhance mission adaptability.

Collaborative defense programs, such as joint NATO procurement initiatives and national fleet modernization efforts, are reshaping competitive dynamics, emphasizing interoperability and rapid deployment. Furthermore, the surge in indigenous manufacturing programs across Asia and the Middle East is encouraging OEM partnerships with local industries for technology transfer and co-production. As defense agencies prioritize network-centric and data-driven mission capabilities, competition is increasingly centered on digital transformation, sustainability, and multi-domain operational readiness.

- April 2025 – Saab AB and the UAE Ministry of Defense announced a partnership to co-develop advanced variants of the GlobalEye surveillance aircraft, reinforcing the trend toward collaborative, multi-role mission capability development among top-tier OEMs.

LIST OF KEY SPECIAL MISSION AIRCRAFT COMPANIES PROFILED:

- The Boeing Company (U.S.)

- Airbus Defence and Space (France)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Textron Aviation (U.S.)

- L3Harris Technologies (U.S.)

- Thales Group (France)

- Elbit Systems Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS:

- June 2025 – Northrop Grumman Corporation received a contract extension from the U.S. Navy to continue upgrading the E-2D Advanced Hawkeye fleet with advanced radar and electronic warfare capabilities.

- May 2025 – Airbus Defence and Space secured a multi-year contract with Spain’s Ministry of Defence to deliver additional C295 maritime patrol aircraft equipped with updated mission suites for coastal surveillance and anti-submarine operations.

- April 2025 – Saab AB partnered with the UAE Ministry of Defense to co-develop an advanced variant of the GlobalEye Airborne Early Warning & Control (AEW&C) aircraft, emphasizing enhanced sensor integration and localized manufacturing.

- March 2025 – Boeing was awarded a contract by the U.S. Air Force to upgrade its RC-135 Rivet Joint fleet with next-generation ISR and communications systems to enhance data-sharing and real-time situational awareness capabilities.

- November 2024 – Leonardo S.p.A. signed a strategic agreement with South Korea’s Korea Aerospace Industries (KAI) to collaborate on special mission aircraft configurations tailored for ISR and maritime patrol roles.

- September 2024 – Textron Aviation announced the delivery of King Air 360ER aircraft to the Royal Canadian Air Force under a modernization contract for intelligence, surveillance, and reconnaissance operations.

- February 2024 – L3Harris Technologies completed the acquisition of MAG Aerospace’s airborne ISR business segment, strengthening its portfolio of mission systems and global defense integration capabilities.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

| Estimated Year | 2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.85% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Point of Sale

By Aircraft Type

By Mission Type

By End-User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.88 billion in 2026 and is projected to reach USD 13.40 billion by 2034.

In 2025, the North America market value stood at USD 2.68 billion.

The market is expected to exhibit a CAGR of 6.85% during the forecast period of 2026-2034.

In 2025, the OEM segment led the market by point of sale.

The growing demand for real-time surveillance and intelligence capabilities is a key factor propelling the market.

Airbus Defence and Space (France), Lockheed Martin Corporation (U.S.), and Northrop Grumman Corporation (U.S.) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us