Coaxial Cable and Tools & Equipment Market Size, Share & Industry Analysis, By Tool Type (Coaxial Cable, Telecom Tools, COAX Cable Tools, Cable Pulling Tools, Fiber Optic Tools, and Electrical Test Equipment), By Application (Internet Data Transfer, Video Distribution, and Radio Frequency Transfer), By End-Use Industry (Telecommunications & Broadband Service Providers, Broadcasting & Satellite, Fiber Optic Networks, Defense & Aerospace, Industrial & Utilities, and Others), and Regional Forecast, 2026-2034

Coaxial Cable and Tools & Equipment Market Size and Future Outlook

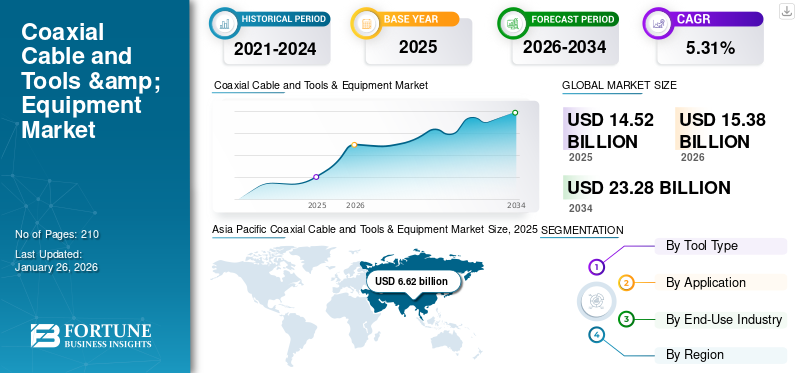

The global coaxial cable and tools & equipment market size was valued at USD 14.52 billion in 2025 and will reach USD 15.38 billion in 2026. The market is projected to exhibit a CAGR of 5.31% during the forecast period and reach USD 23.28 billion by 2034. Asia Pacific dominated the coaxial cable and tools & equipment market with a market share of 45.57% in 2025. Asia Pacific accounts for the largest market revenue share owing to the presence of robust HFC Networks in the region.

The coaxial cable and tools & equipment market is defined by the production, distribution, and sale of coaxial cables and the specialized tools and connectors required for their installation, maintenance, and termination. Coaxial cables are used to transmit high-frequency electrical signals with minimal external electromagnetic interference across a wide range of applications.

The market is primarily driven by the increasing demand for high-speed broadband and internet connectivity, fueled by data-intensive applications such as 4K/8K streaming, online gaming, and cloud services. The ongoing expansion of telecommunication infrastructure and hybrid fiber-coaxial (HFC) networks, along with increasing investments in 5G and Internet of Things (IoT) technologies, sustains the need for reliable, cost-effective coaxial cables for last-mile connectivity and specialized applications.

- In February 2025, Optimum announced network upgrade plans to deliver multi-gigabit internet speeds across 65% of its service footprint by 2028. The multi-gigabit hybrid-coax network is expected to double the availability of multi-gigabit speeds over the next three years.

TE Connectivity (TE) is a highly prominent and significant player in the market for coaxial cable and tools & equipment, particularly in high-performance and specialty segments. The company is a global leader in connectivity solutions, and its prominence is demonstrated through a robust product portfolio in the industry.

Download Free sample to learn more about this report.

Coaxial Cable and Tools and Equipment Market KEY TAKEAWAYS

- 2025 Market Size: USD 14.52 billion

- 2026 Market Size: USD 15.38 billion

- 2034 Forecast Market Size: USD 23.28 billion

- CAGR: 5.31% from 2026–2034

- Asia Pacific dominated the coaxial cable and tools & equipment market with a 45.57% share in 2025.

- The coaxial cable segment accounted for the largest market share in 2026, holding 53.12%.

- The internet data transfer segment is projected to hold a 62.7% share in 2026.

Asia Pacific

Valued at USD 6.62 billion in 2025, driven by broadband expansion, HFC deployments, and government digitalization initiatives.

North America

Valued at USD 3.76 billion in 2025, supported by extensive HFC infrastructure and strong broadband demand.

Europe

Valued at USD 2.65 billion in 2025, driven by widespread HFC networks and investments in satellite and defense communications.

U.S.

Projected to reach USD 3.64 billion by 2026, supported by continued broadband infrastructure development.

Japan

Projected to reach USD 1.14 billion by 2026, driven by expanding broadband and digital connectivity projects.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Telecommunications and Broadband Expansion Drive Market Growth

The rapid expansion of telecommunications and broadband networks serves as a significant driver for the coaxial cable and tools & equipment market growth. The increase in demand for high-speed internet connectivity, driven by the rising bandwidth-intensive applications such as high-definition video streaming and cloud computing, is compelling telecom operators and broadband service providers to accelerate the deployment and enhancement of their network infrastructures. Moreover, the deployment of advanced initiatives such as DOCSIS 3.1 and the ongoing transition toward DOCSIS 4.0, designed to deliver multi-gigabit symmetrical speeds, necessitate extensive installation, maintenance, and repair efforts.

- For instance, in July 2025, Mediacom and Hitron Technologies Americas announced a trial for DOCSIS 4.0 eMTA Trial Deployments in the U.S by utilizing a new generation of hybrid fiber coax technology.

Hybrid Fiber-Coaxial Network Upgrades to Fuel Demand for Advanced Tools

The advancement of hybrid fiber-coaxial (HFC) networks is expected to substantially boost the demand for coaxial cable and tools & equipment. Cable operators are increasingly focused on enhancing upstream bandwidth capacity to support emerging next-generation services such as multi-gigabit internet and enterprise-grade connectivity. These network enhancements necessitate comprehensive field operations involving node segmentation, plant expansions, and overall system optimization.

Such activities require the utilization of highly reliable and precise tools specifically designed for the preparation, termination, and diagnostic testing of coaxial cable connections. The deployment of these specialized tools is critical to ensuring adherence to quality standards and regulatory compliance throughout the network upgrade and rollout processes. In February 2025, Optimum announced network upgrade plans to deliver multi-gigabit internet speeds across 65% of its service footprint by 2028. Moreover, the multi-gigabit hybrid-coax network is expected to double the availability of multi-gigabit speeds over the next three years.

MARKET RESTRAINTS

Intense Competition from Alternative Technologies to Limit Market Growth

The coaxial cable and tools & equipment market growth is restrained by the emergence of alternative technologies, notably fiber optic and wireless solutions. Fiber-to-the-home (FTTH) and passive optical network (PON) architectures are distinguished by their superior bandwidth capacity, minimal latency, and scalability, rendering them the preferred infrastructure choice for new broadband deployments across both mature and emerging markets. Hence, telecom operators’ strategic emphasis on fiber network upgrades has resulted in a decline in investments related to coaxial cable infrastructures and their associated tooling.

MARKET OPPORTUNITIES

Growth of DAS, Public Safety, and Private Networks Create Bright Opportunities for Coaxial Tools

The rapid expansion of Distributed Antenna Systems (DAS), public safety communication networks, and private wireless installations presents substantial growth opportunities for the coaxial cable and tools & equipment market. While fiber optic cabling predominantly supports core network transport, coaxial cables remain critical for connectivity within in-building wireless systems, primarily serving feeder and jumper cable functions. Hence, the ongoing expansion and regulatory emphasis on DAS infrastructure significantly augment demand for specialized coaxial cable tools and reinforce their integral role in modern wireless communication deployments.

- For Instance, In November 2024, Verizon announced deployment of its first interoperable multi-vendor O-RAN DAS system at The University of Texas Moody Center and the Austin Convention Center in Texas, U.S. Furthermore, these systems are first of its kind DAS systems commercially deployed in the network of Verizon which utilizes O-RAN interfaces between the various components of the cellular Radio Access Network from different vendors.

MARKET CHALLENGES

Emergence of Wireless Technology Create Obstacles for Market Growth

Wireless solutions such as 5G, Wi-Fi, and satellite connectivity are viable alternatives for high-speed internet and high-definition video distribution. As consumers and businesses increasingly favor wireless solutions, the demand for coaxial cables in traditional applications such as television and internet access is challenged. Moreover, the existence of low-cost, low-quality counterfeit products affect the reputation and sales of established vendors. This is especially prevalent for cable assemblies and other components.

COAXIAL CABLE AND TOOLS & EQUIPMENT MARKET TRENDS

Deployment of Hybrid Fiber-Coaxial (HFC) Networks is emerging as a Key Trend

Cable operators are actively upgrading HFC networks to support DOCSIS 4.0, which expands spectrum usage up to 1.8 GHz and introduces higher upstream splits. This evolution demands tools and test equipment capable of operating at wider frequency ranges and tighter tolerances. Installers increasingly require high-precision compression and crimp tools, calibrated torque drivers, and advanced signal meters that measure MER, BER, and ingress at extended frequencies.

- For instance, in September 2025, Mediacom Communications announced its first successful DOCSIS 4.0 customer deployment in Mediacom’s Moline, Illinois system with a hybrid-fiber coaxial (HFC) network in collaboration with ATX Networks, Harmonic, and Hitron.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

In 2024 and 2025, tariffs on metals, tool parts, and electronic devices raised the costs of making and importing coaxial cable tools. This led to higher prices for compression tools, torque drivers, and testing meters, putting pressure on distributors and contractors. To manage these costs, manufacturers shifted some production to Mexico, Vietnam, and Eastern Europe. Many also offered service packages and calibration deals to soften the price impact. Despite the tariffs, demand held steady thanks to DOCSIS upgrades and ongoing network maintenance needs.

By 2028, if tariffs remain in place, supply chains will adjust more permanently. Manufacturers are likely to expand local production in India, Vietnam, and parts of Europe to reduce dependency on tariff-heavy imports. While costs may stay higher than before tariffs, companies will focus on offering durable, repairable, and modular tools to give buyers better long-term value. Hence, contractors may choose bundled coax-and-fiber toolkits to balance budgets, while suppliers will use bulk contracts and localized sourcing to stay competitive.

SEGMENTATION ANALYSIS

By Tool Type

Coaxial Cables’ High Usage is led by the Robust Deployment of HFC networks globally

Based on tool type, the market is segmented into coaxial cable, telecom tools, COAX cable tools, cable pulling tools, fiber optic tools, and electrical test equipment. The coaxial cable dominated the market with a market share of 53.43% in 2024 due to the extensive installed HFC infrastructure and its critical role in broadband, television, and in-building connectivity. Operators continue to invest in maintenance and DOCSIS 4.0 upgrades, which sustain demand for coaxial strippers, compression tools, and test meters. The coaxial cable segment is projected to dominate the market with a share of 53.12% in 2026.

- In May 2024, Qorvo launched the QPC7330, the industry’s first single-chip variable inverse cable equalizer, simplifying DOCSIS 4.0 CATV network upgrades. The IC eliminates the need for plug-ins or complex setups, enables automated programming, and streamlines installation.

Furthermore, fiber optic tools segment emerged as the fastest-growing at a CAGR of 7.24%, driven by accelerating FTTH deployments, government-backed broadband initiatives, and rising demand for high-speed, low-latency internet. Fusion splicers, cleavers, and optical testers are increasingly adopted as operators transition networks to fiber, creating rapid growth opportunities alongside coaxial’s strong maintenance-led demand.

By Application

Internet Data Transfer Dominates Due to Rising Demand for High Speed Broadband Services

Based on application, the market is segmented into internet data transfer, video distribution, and radio frequency transfer. Internet data transfer segment dominated the coaxial cable and tools & equipment market share in 2024 with a 63.08% revenue, driven by surging demand for high-speed broadband to support streaming, cloud services, remote work, and IoT applications. Operators rely on coaxial infrastructure for last-mile connectivity, ensuring strong demand for precision tools and advanced testers. The internet data transfer segment is projected to dominate the market with a share of 62.7% in 2026.

- In August 2025, Rogers announced the expansion of its WiFi 7 service to customers in Canada through its 5G Home Internet, supporting over 200 connected home devices simultaneously. This rollout follows launches in Calgary and Atlantic Canada, aiming to provide Canadians with enhanced home internet experiences over Rogers’ 5G and hybrid fiber coax networks.

The video distribution and radio frequency (RF) transfer segments are emerging. Rising adoption of high-definition and 4K/8K video in broadcast, hospitality, and pro-AV environments sustains video-related tool demand. Meanwhile, RF transfer growth is fueled by aerospace, defense, and 5G applications, requiring specialized coaxial connectors, torque tools, and test equipment to ensure performance.

By End-Use Industry

Telecommunications and broadband service providers Segment to dominate the Market Owing to the large-scale expansion of Telecom Services across the Globe.

Based on end-use industry, the market is segmented as telecommunications & broadband service providers, broadcasting & satellite, fiber optic networks, defense & aerospace, industrial & utilities, and others. The telecommunications and broadband service providers dominated in 2024 with a market share of 34.66%. The segment’s growth is majorly driven by large-scale deployments, DOCSIS upgrades, and ongoing maintenance drive continuous demand for strippers, compression tools, torque wrenches, and advanced test meters. Their vast technician workforce and strict quality standards ensure steady, recurring purchases. The telecommunications & broadband service providers segment is projected to dominate the market with a share of 34.92% in 2026.

- In September 2025, Harmonic and Comcast announced a collaboration to expand fiber broadband access as Comcast grows its network into new markets. In 2024, Comcast added over 1 million new locations and plans to add 1.2 million more by the end of 2025.

On the other hand, broadcasting and satellite are emerging as the fastest-growing segments. The rise of ultra-high-definition (4K/8K) broadcasting, expansion of direct-to-home satellite services, and growth in ground infrastructure for satellite communications are fueling demand for high-precision coaxial tools and RF testing equipment, particularly in regions with expanding media consumption and aerospace connectivity projects.

To know how our report can help streamline your business, Speak to Analyst

COAXIAL CABLE AND TOOLS & EQUIPMENT MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Coaxial Cable and Tools & Equipment Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 45.57% of the global market, reaching a valuation of USD 6.62 billion, and is projected to grow to USD 7.06 billion in 2026. Asia Pacific’s coaxial cable and tools & equipment market emerged as the largest in 2025, valued at USD 6.62 billion primarily driven by China, India, South Korea and Japan. Large-scale broadband expansion, hybrid fiber-coaxial deployments, and government-led digitalization initiatives created strong demand for strippers, compression kits, torque wrenches, and advanced testers. The Japan market is forecast to reach USD 1.14 billion by 2026, the China market is set to reach USD 3.51 billion by 2026, and the India market is likely to reach USD 0.71 billion by 2026.

- In February 2024, Prysmian and Telstra partnered for the expansion of Prysmian's optical cable manufacturing plant in Dee Why, Australia, to support Telstra's intercity fibre network. The advanced, sustainable technology aims to enhance production capacity and reduce environmental impact, future-proofing Australia's connectivity for 20+ years.

North America

North America accounted for USD 3.76 billion in 2025, representing 25.89% of the global market share, and is projected to reach USD 3.97 billion in 2026. North America’s coaxial cable and tools & equipment industry gained USD 3.76 billion in 2025 with an estimation of USD 3.97 billion for 2026. This leadership stems from the region’s vast installed hybrid fiber-coaxial (HFC) infrastructure, continuing to serve millions of households for broadband and cable television. The U.S. market is estimated to reach USD 3.64 billion by 2026.

Europe

The Europe market was valued at USD 2.65 billion in 2025, capturing 18.27% of global revenue, and is estimated to reach USD 2.79 billion in 2026. Europe is expected to account for third third-largest market share for coaxial cable and tools & equipment with a valuation of USD 2.52 billion, driven by a large cable television subscriber base, and continues to use hybrid fiber-coaxial (HFC) networks to deliver broadband services to millions of households. Beyond residential broadband, Eastern European countries’ significant investments in satellite communications, military and aerospace, and defense further reinforce their dominance. The Russian market is estimated to reach USD 0.49 billion in 2025. The UK market is expected to reach USD 0.25 billion by 2026, while the Germany market is anticipated to reach USD 0.38 billion by 2026.

Middle East & Africa

Middle East & Africa contributed approximately USD 0.89 billion to the global market in 2025, accounting for 6.10% share, and is expected to reach USD 0.93 billion in 2026. The market in the Middle East & Africa is driven by ongoing venue, stadium, and rail developments, which demand DAS/public-safety coverage, sustaining the need for torque-calibrated tools, compression systems, leakage meters, and high-frequency analyzers. Furthermore, Latin America is experiencing moderate growth with a CAGR of 3.72%. The vast legacy HFC footprint across dense urban corridors (São Paulo–Rio–Belo Horizonte) sustains high replacement and maintenance cycles for compression/crimp tools, torque drivers, SLMs, TDRs, and leakage meters.

Latin America

The Latin America region captured 4.16% of the global market in 2025, generating USD 0.6 billion in revenue, and is projected to reach USD 0.63 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Engaged in Strategic Collaboration and Campaigns to Increase Market Share

The competitive landscape of coaxial cable and tools & equipment is fragmented, and key competitive players, including Klein Tools, Milwaukee Tools, Fluke Corporation, and Dewalt, are focused on continuous technological advancements and brand recognition activities. For instance, in June 2025, DEWALT partnered with SkillsUSA, the largest student-led workforce development organization in the U.S., to support future tradespeople. DEWALT will donate USD 100,000 in tools to the SkillsUSA Championships in Atlanta, where 6,800 students compete across over 100 skilled trades categories. This collaboration is part of DEWALT's USD 30 million Grow the Trades initiative to close the skilled trades gap by 2027, having already awarded nearly USD 20 million in scholarships, grants, and tools. The market is driven by ongoing infrastructure maintenance and expansion, especially for last-mile and Hybrid Fiber-Coaxial (HFC) network connections that are essential for high-speed broadband, 5G, and IoT applications.

List of the Key Coaxial Cable and Tools & Equipment Companies Profiled:

- Klein Tools, Inc. (U.S.)

- Milwaukee Tool (U.S.)

- Fluke Corporation (U.S.)

- Triplett Test Equipment & Tools. (U.S.)

- DEWALT (U.S.)

- Greenlee (U.S.)

- Jameson (U.S.)

- VIAVI Solutions (U.S.)

- RUS Industries (U.S.)

- TE Connectivity (Ireland)

KEY INDUSTRY DEVELOPMENTS:

- September 2025-Milwaukee Tool announced a USD 42 million expansion in Menomonee Falls, Wisconsin. This project, supported by USD 4.5 million in performance-based tax credits from the Wisconsin Economic Development Corporation, includes the purchase of a 22-acre property. The expansion reflects Milwaukee Tool’s ongoing investment in innovation and manufacturing excellence, reinforcing Wisconsin’s role as a central hub for the company’s growth and advanced production capabilities.

- September 2025-InCoax Networks AB highlighted the shift brought by the U.S. BEAD program’s updated tech-neutral rules, removing fiber-first preference. This change enables smarter, faster, and cost-effective broadband solutions over existing in-building coaxial cables, especially for multi-dwelling units (MDUs).

- July 2025-Smiths Interconnect launched EZiCoax, a single-piece, compression-mount, 50-ohm RF coaxial contact designed for board-to-board signal transmissions with data frequencies up to 40GHz. This innovative solution targets high-value aerospace and defense applications, including satellite communications and advanced radar systems.

- In March 2025-TDK Electronics expanded its ADL3225VF series of wire-wound inductors for automotive power-over-coax (PoC). PoC technology enables simultaneous power and data transmission over a single coaxial cable, simplifying vehicle wiring, reducing weight, and improving fuel efficiency.

- January 2025-Junkosha unveiled its latest ultra-phase stable interconnect advancements at DesignCon 2025, including the MWX161, MWX001, MWX002, and MWX004 Microwave/mmWave Coaxial Cable Assemblies. Designed for 5G/6G digital applications, these cables reach up to 67 GHz and feature skew matching within 1 psec.

REPORT COVERAGE

The coaxial cable and tools & equipment market research reports delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the market. Besides, the report offers regional insights and global market trends & technology, and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.31% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Tool Type

|

|

By Application

|

|

|

By End-Use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per Fortune Business Insights study, the market size was USD 14.52 billion in 2025.

The market is likely to grow at a CAGR of 5.31% over the forecast period (2026-2034).

The telecommunications & broadband service providers segment is expected to lead the market over the forecast period.

The market size of Asia Pacific stood at USD 6.62 billion in 2025.

Telecommunications and broadband expansion drive market growth.

Some of the top players in the market are Klein Tools, Inc., Milwaukee Tool, Fluke Corporation, Triplett Test Equipment & Tools, and DEWALT.

The global market size is expected to reach USD 23.28 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us