Cognitive Electronic Warfare Market Size, Share & Industry Analysis, By EW Function (Electronic Support, Electronic Attack, & Others), By Platform (Airborne (Fighters, EW Pods, UAV Payloads), Naval (Surface Ships, Subs), Land (Tactical/Strategic Ground), and Space-adjacent (PNT Anti-jam, Satcom Protection)), By System (Pods & external Payloads, Integrated Suites, & Others), By Component (Sensors/Receivers (Wideband, DF), Effectors (Jammers/Decoys), & Others), By Cognitive Type), By Frequency (HF/VHF/UHF, L/S/C/X/Ku/Ka bands, & Others), By End User, and Regional Forecast, 2026-2034

Cognitive Electronic Warfare Market Size and Future Outlook

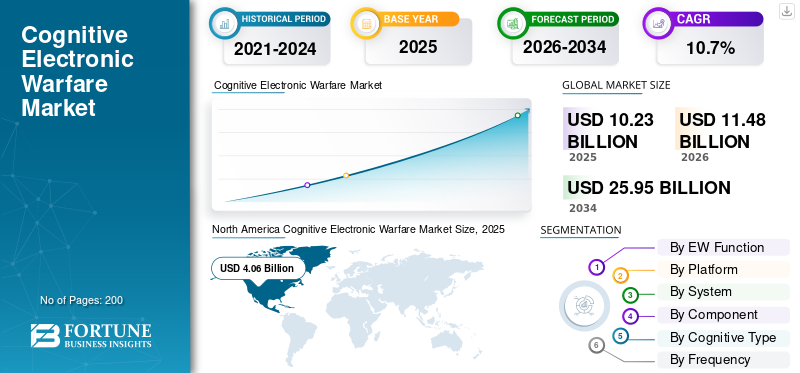

The global cognitive electronic warfare market size was valued at USD 10.23 billion in 2025. The market is projected to grow from USD 11.48 billion in 2026 to USD 25.95 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period. North America dominated the cognitive electronic warfare market with a market share of 39.69% in 2025.

The global market includes cognitive EW systems that can sense the electromagnetic environment, interpret signals, and adjust responses in real time. This goes beyond traditional electronic warfare techniques. The market is expanding as military forces are facing new threats, such as smarter radars, contested data links, and large numbers of unmanned aerial vehicles. They are increasingly investing in technologically advanced EWs that use artificial intelligence and machine learning for faster threat recognition, improved adaptive jamming, and better electronic protection across platforms.

On the supplier side, a few key players are driving the market forward by transforming cognitive ideas into usable, upgradeable systems. BAE Systems is leading with integrated EW suites and modernization pathways that link sensors, effectors, and mission systems for quicker decision-making. Elbit Systems is also a key player, providing airborne protection suites and EW payload upgrades. They focus on system integration and faster reprogramming so operators can respond to evolving threats without waiting for slow refresh cycles.

Download Free sample to learn more about this report.

COGNITIVE ELECTRONIC WARFARE MARKET TRENDS

AI and ML Driven Adaptive Jamming is Transforming Electronic Warfare into Fast-Learning Software-updated Capability

The cognitive electronic warfare market growth is driven by the shift from fixed, library-driven techniques to artificial intelligence and machine learning-assisted cognitive EW. The new approach can recognize unfamiliar emitters and adjust responses rapidly. The cognitive edge focuses less on a single jammer and more on the system operating in a loop: detect, decide, respond, assess, and update. Programs now emphasize rapid reprogramming, strong electronic protection, and mission software that can keep up with changing threats. This is especially important as radars and networks become more adaptable.

In April 2024, the U.S. Air Force awarded Southwest Research Institute (SwRI) a USD 6.4 million contract to explore cognitive electronic warfare algorithms, designed to detect and respond to unknown enemy radar threats in real time. This contract signals that adaptive, AI-like behavior is moving from concept to funded work.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Survivability Upgrades against Evolving Radar and Drone Threats Drive Market Growth

Modern platforms are operating in busier and hostile spectrum conditions. As a result, militaries are focusing on electronic warfare upgrades that improve survivability and keep up with changing threats. This demand for cognitive electronic warfare systems market stems from funded programs to modernize aircraft with technologically advanced electronic warfare sensor suites. These suites are key for cognitive behavior, along with the software and integration work needed to make them effective across missions.

In November 2025, Saab received orders from Airbus Defence and Space to deliver the Arexis Electronic Warfare sensor suite for the German Eurofighters. The total value of the contract is approx. USD 631.86 million, with deliveries scheduled from 2025 to 2028.

MARKET RESTRAINTS

Safety, Governance and Approval Rules to Slow Down the Deployment of Cognitive Autonomy

The increasing autonomy in electronic warfare decision-making presents a significant challenge. Cognitive behaviors must be validated, tested, and governed to prevent unintended consequences, such as hitting off-target, friendly interference, or unsafe escalation. This reality lengthens timelines, particularly when systems incorporate weapon-like capabilities or operate under strict engagement rules. In these situations, approvals, verification, and accountability are as crucial as performance.

In January 2023, the U.S. Department of Defense updated DoD Directive 3000.09, titled “Autonomy in Weapon Systems.” This update emphasized policies and oversight for autonomous and semi-autonomous functions. It also set requirements for development, governance, and senior-level approvals for certain autonomous weapon systems.

MARKET OPPORTUNITIES

Attritable Unmanned Stand-in Jammers to Pave Way for Cognitive Electronic Warfare (EW) Growth

A major chance lies in the shift toward low-cost, unmanned platforms that carry EW payloads. These platforms can be quickly updated and deployed in riskier airspace. This method offers a scalable approach for cognitive EW. Learning loops, rapid reprogramming, and smart technique selection become simpler with more nodes, faster iterations, and the ability to protect valuable crewed aircraft.

In May 2025, the UK’s Defence Equipment & Support (DE&S) announced the procurement of Tekever AR3 drones. These were integrated with Leonardo UK’s BriteStorm electronic warfare system.

MARKET CHALLENGES

Variable Changes Challenges Cognitive EW Systems work Efficiency During Missions

A key challenge is that cognitive EW systems may exhibit variable behavior as signal conditions, adversary tactics, and operational environments change. One-time testing is therefore insufficient. Armed forces require reliable methods to evaluate performance, survivability, and unexpected behaviors, including interference or inappropriate technique selection, across real mission scenarios. Continuous retesting is also necessary as software updates and machine learning models are refined over time. This extensive verification can delay deployment, making system integration and data readiness equally important to jammer hardware.

In December 2024, the U.S. Department of Defense issued DoD Manual 5000.101 on Operational Test and Evaluation (OT&E) and Live Fire Test and Evaluation (LFT&E) for AI-enabled and autonomous systems.

Impact of Russia Ukraine War

Russia–Ukraine War to Accelerate Demand for Rapidly Reprogrammable and Counter-UAS-Focused Cognitive EW Capabilities

The Russia-Ukraine war has turned electronic warfare into a daily contest, especially concerning GPS/PNT disruption, drone links, and radar survivability. This situation drives interest in cognitive EW, which are systems that can change quicker than static libraries.

Two main effects on the market are:

- Europe’s increased spending is creating more opportunities for EW modernization and control of the spectrum

- The fast “measure, adapt, retest” loop on the battlefield is pushing procurement towards reprogrammable, software-defined EW systems and counter-UAS EW, where cognitive behaviors are crucial.

In April 2025, SIPRI reported that European military spending, including Russia's, increased 17% to USD 693 billion in 2024. The war in Ukraine was a major factor, driving more funding for EW and CEW programs and upgrades.

In June 2025, Defense News reported on Europe’s developments with drone-based radar jammers, such as Denmark testing UAS and RF payload concepts.

Segmentation Analysis

By EW Function

Electronic Support (ES) Dominates Owing to the Need for Fast and Reliable Threat Detection

By EW function, the market is categorized into Electronic Support (ES), Electronic Attack (EA), Electronic Protection (EP), and Electromagnetic Battle Mgmt (EMBM/EMSO tools).

Electronic Support (ES) segment leads as it enables real time detection, classification and tracking of adversary signals, providing the situational awareness required for adaptive jamming and decision-making across the operational engagement cycle. Without wideband sensing, direction finding, and quick signal classification, friendly networks cannot be protected or the right countermeasure cannot be induced. As emitters become more agile and environments become noisier, operators focus on improving ES as it helps them build real-time awareness and provide better data for adaptive techniques.

In November 2025, Saab announced orders of roughly USD 638.21 million from Airbus Defence and Space for the Arexis Electronic Warfare (EW) sensor suite. This equipment is intended for German Eurofighters, with deliveries set between 2025 and 2028.

Electromagnetic Battle Mgmt (EMBM/EMSO tools) segment is expected to show fastest growth at a CAGR of 16.7% over the forecast period.

By Platform

Airborne Platforms Segment Leads due to the Need to Protect High-Value Aircraft and Strike Packages in Contested Airspace

On the basis of platform, the market is classified into Airborne (fighters, EW pods, UAV payloads), Naval (surface ships, subs), Land (tactical/strategic ground), and Space-adjacent (PNT anti-jam, satcom protection).

Airborne (fighters, EW pods, UAV payloads) segment held the largest share in 2025. The aerospace and defense domain often requires quick decisions for survival against modern radars, missiles, and complex air defenses. Fighters, EW pods, and UAV-carried payloads offer the fastest way to scale. The fleets can be upgraded with podded effects and software updates without redesigning the entire platform. This method maintains electronic protection and adjusts responses to match the latest threat behavior.

In May 2025, Raytheon (RTX) received a USD 580 million follow-on production contract from the U.S. Navy for the Next Generation Jammer Mid-Band (NGJ-MB). This contract includes additional airborne jamming pod shipsets, including pods for the Royal Australian Air Force, along with spares and support equipment.

Space-adjacent (PNT anti-jam, satcom protection) is expected to show fastest growth at a CAGR of 13.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By System

Integrated Suites (Aircraft/Ship) Lead Owing to Closer Connections Between Mission and the Need For Platform Survivability

Based on system, the market is segmented into, pods & external payloads, integrated suites (aircraft/ship), ground systems (vehicle/manpack), expendables/decoys (active), and training/test & reprogramming kits.

Integrated suites (aircraft/ship) segment holds the largest market share as modern electronic warfare (EW) extends beyond standalone jamming capabilities. It includes a coordinated mix of sensors, processing, countermeasures, and mission software that must work well with the host platform. When threats rapidly change, operators prefer integrated EW that can combine warnings, suggest responses, and offer protection without extra pods or additional demands on operators. This is crucial for frontline aircraft and high-value ships.

In July 2024, the U.S. Department of Defense announced a USD 520.4 million contract modification for the production of the F-16 Block 70/72 Viper Shield electronic warfare suite through Foreign Military Sales.

The expendables/decoys (active) is anticipated to be the fastest growing segment at a CAGR of 12.2% across the forecast period.

By Component

Quick Disruption of Enemy Radars and Links, Effectors, Jammers and Decoys Dominate Segmental Growth

Based on component, the market is segmented into, sensors/receivers (wideband, DF), Effectors (jammers/decoys), mission software & libraries, and others.

Effectors (jammers/decoys) segments dominated the market in 2025. Once a system detects and classifies a threat, its task is in its ability to jam, deceive, or distract the opponent. This is especially important for modern, fast-changing emitters. Defense budgets are heavily prioritizing investments in jamming technology and active decoys. They provide immediate survivability benefits and can improve through mission data and technique updates.

In September 2024, the U.S. Navy awarded L3Harris a five-year contract worth up to USD 587.4 million for the Next Generation Jammer, Low Band (NGJ-LB). This tactical jamming pod program updates airborne electronic attacks and shows a clear commitment to investing millions & billion in the cognitive electronic warfare systems market.

Mission software & libraries is the fastest growing segment in the market at a CAGR of 14.1% across the forecast period.

By Cognitive Type

Assisted (Human-In-The-Loop) is Preferred Due to Safety and Accountability Requirements

Based on cognitive type, the market is segmented into, assisted (human-in-the-loop), adaptive (rules + ML aids), cognitive (closed-loop adaptation), and swarm/collaborative EW (multi-platform).

Assisted (human-in-the-loop) segment held the largest global cognitive electronic warfare market share in 2025. As cognitive EW improves, the need for human operators is essential for action that leads to unintended interference, escalation, or friendly disruption. Assisted cognitive EW matches as militaries use autonomy AI/ML can enhance detection, recommendations, and technique options, but humans remain responsible for final intent and control, particularly in complex rules-of-engagement situations.

Swarm/collaborative EW (multi-platform) is the fastest growing segment, depicting a CAGR of 26.4% across the forecast period.

By Frequency

Prevalence of Radar and Datalink Threats Allow L/S/C/X/Ku/Ka bands Dominance

Based on frequency, the market is segmented into, HF/VHF/UHF, L/S/C/X/Ku/Ka bands, Multi-band / wideband, and others.

L/S/C/X/Ku/Ka bands segment held the largest market share in 2025, as most difficult issues in electronic warfare are generated due to air-defense radars, fighter fire-control radars, missile seekers, and many tactical datalinks. They are mostly found in the L frequency through Ka-band range. The electronic warfare effectiveness is most apparent as the system needs to classify, sense quickly and counter rapidly changing signals in the same bands that affect neutralization probability.

The multi-band / wideband is the fastest growing segment, registering a CAGR of 14.4% across the forecast period.

By End User

Defense Organization are Leading End users Owing to National Modernization Budgets

Based on end user, the market is segmented into defense organization, R&D agencies, and prime contractors/OEM integration.

Defense organization segment dominated the market in 2025, in cognitive EW, defense groups such as Ministries of Defense and armed services take charge as they control operational needs and major procurement cycles. These cycles involve platform upgrades, survivability kits, and large-scale deployment. Even when industry and laboratories work on research and development, the market activity emerges. Air forces, navies, and armies fund acquisition, installation, and long-term maintenance to keep EW effective against evolving threats.

Prime contractors/OEM integration segment is expected to show fastest growth at a CAGR of 16.4% across the forecast period.

Cognitive Electronic Warfare Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World (Middle East, Africa, and Latin America).

North America

North America Cognitive Electronic Warfare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America’s cognitive electronic warfare market holds the largest share of the market. The U.S. is at the forefront as it maintains the largest and most consistent flow of EW upgrades across aircraft, ships, ground systems, and the associated software and reprogramming. This level of funding, along with a strong focus on survivability and spectrum dominance, pushes the region ahead in both capability and ongoing purchases. In April 2025, SIPRI reported that U.S. military spending reached USD 997 billion in 2024. The U.S. contributed up to 37% of global military spending, giving North America a structural advantage in leading investments in EW and cognitive EW.

U.S. Cognitive Electronic Warfare Market

The U.S. market’s dominance within the region generated a revenue of USD 3.82 billion in 2025, and will progress at a CAGR of 9.0% over the forecast period.

Europe

Europe’s market size was second largest in 2025 at USD 2.67 billion and will register a CAGR of 11.8% in the coming years. Europe has become one of the most active regions for cognitive electronic warfare as the environmental threat is imminent. SIPRI reports that Europe's military spending, including Russia, has risen up to 17% at a valuation of USD 693 billion in 2024. Russia's spending is estimated at USD 149 billion, with significant increases throughout the continent. This pattern of spending encourages the quick development of electronic warfare defense capabilities, such as improved electronic support (sensing and direction finding), stronger electronic protection, and more tools for electronic maneuver warfare and electronic spectrum operations to coordinate spectrum actions among joint forces.

U.K. Cognitive Electronic Warfare Market

The U.K. market is third largest globally and is anticipated to register a CAGR of 12.7% in the coming years.

Germany Cognitive Electronic Warfare Market

Germany’s market size is estimated at around USD 0.49 billion in 2026, representing roughly 15.88% of Europe’s revenues.

Asia Pacific

Asia Pacific market size achieved USD 2.27 billion in 2025 and is anticipated to show fastest growth of 12.7% during the forecast period. The region’s demand is influenced by large-scale modernization and ongoing regional tensions. This means electronic warfare is observed as a key support, not just a specialty. SIPRI notes that China’s spending is expected to reach USD 314 billion in 2024, which is a 7% increase. Meanwhile, Japan’s spending rose 21% to USD 55.3 billion, its largest annual increase since 1952. This situation naturally drives cognitive electronic warfare priorities: faster signal recognition, adaptability across multiple bands, and the protection of networks and sensors in air and maritime operations.

China Cognitive Electronic Warfare Market

China’s market is projected to be one of the largest with 2025 revenues estimated at around USD 0.92 billion, representing roughly 40.31% of Asia Pacific sales.

India Cognitive Electronic Warfare Market

India’s market in 2025 is estimated at around USD 0.31 billion, accounting for roughly 13.69% of Asia Pacific’s revenue.

Rest of the World

The rest of the world (Middle East, Africa and Latin America), has a comparatively smaller share and will grow at a CAGR of 8.9%. The Middle East tends to move faster, Africa grows from a smaller base, and Latin America is selective and budget-sensitive. SIPRI reports that military spending in the Middle East reached about USD 243 billion in 2024, which is an increase of 15% of Africa's total spending of USD 52.1 billion in 2024. Latin America showcases mixed results, but SIPRI points out examples such as Mexico, where spending rose by 39% to USD 16.7 billion in 2024. These spending trends indicate a near-term demand for practical electronic warfare outcomes, such as counter-UAS, platform survivability kits, and upgrades that can be integrated quickly.

Middle East Cognitive Electronic Warfare Market

The market size in the Middle East accounted for USD 0.81 billion in 2025, and is expected to reach USD 1.90 billion in 2034, representing roughly 65.88% of the world sales.

Africa Cognitive Electronic Warfare Market

This region’s market size captured USD 0.14 billion in 2025, and is expected to reach USD 0.33 billion in 2034.

Latin America Cognitive Electronic Warfare Market

In 2025, Latin America reached USD 0.28 million in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players to Succeed with Fast Integration and Reprogrammable Effects

The cognitive electronic warfare market is increasingly consolidating around major players capable of delivering comprehensive capabilities, including wideband sensing, real-time processing, and operational effects. These companies also ensure their systems remain updated through rapid software upgrades and mission data updates. In practice, buyers are increasingly less focused on acquiring the single most effective jammer and more concerned with whether a supplier can seamlessly integrate electronic warfare capabilities into the platform and sustain their relevance as waveforms and tactics evolve.

In North America, the airborne electronic attack market is influenced by projects such as Raytheon’s NGJ Mid-Band, and L3Harris’ NGJ Low-Band. In Europe, there are large sensor modernization efforts witnessed in Saab’s Arexis orders for German Eurofighters. The U.K. is testing unmanned stand-in jammer concepts through StormShroud, which includes Tekever AR3 and Leonardo’s BriteStorm payload. Meanwhile, BAE Systems is leading in integrated fighter electronic warfare systems. Elbit Systems is also expanding its self-protection suite installs through USD 175 million EW and DIRCM contracts.

LIST OF KEY COGNITIVE ELECTRONIC WARFARE COMPANIES PROFILED

- BAE Systems plc. (U.K.)

- RTX Corporation (Raytheon) (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- HENSOLDT AG (Germany)

- Airbus Defence and Space (Europe)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries (IAI) / ELTA Systems (Israel)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Indra Sistemas, S.A. (Spain)

- ASELSAN A.Ş. (Türkiye)

- Bharat Electronics Limited (BEL) (India)

- Hindustan Aeronautics Limited (HAL) (India)

- Hanwha Systems Co., Ltd. (South Korea)

- Mitsubishi Electric Corporation (Japan)

- Collins Aerospace (U.S.)

- QinetiQ Group plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: India’s Ministry of Defence signed a contract with Bharat Electronics Limited (BEL) valued at USD 277.85 million. This contract involves EW suites, aircraft modification kits, and installation on IAF Mi-17 V5 helicopters.

- December 2024: Elbit Systems won two contracts totaling around USD 175.00 million. These contracts are for supplying EW and DIRCM self-protection suites for a NATO European customer’s Embraer C-390 and Airbus H225M fleets.

- December 2024: The U.S. Air Force Life Cycle Management Center awarded Pacific Defense and Perceptronics a follow-on contract to develop AI and machine learning-enabled electronic warfare mission systems. The work involves integrating machine-learning algorithms to process RF emitters. It will also demonstrate the capability through flight testing using open-architecture EW pods that meet Sensor Open Systems Architecture and Open Mission Systems standards.

- September 2024: The U.S. Navy awarded L3Harris a five-year contract worth up to USD 587.40 million. This contract is for Next Generation Jammer Low Band (NGJ-LB) engineering and manufacturing development.

- April 2024: The U.S. Air Force contracted Southwest Research Institute (SwRI) for work on cognitive electronic warfare (CEW) algorithms. The focus was on smarter sensing and decision cycles, along with faster adaptation to contested RF environments.

- April 2023: BAE Systems received contracts worth USD 491.00 million from Lockheed Martin. These contracts produce Block 4 F-35 electronic warfare systems from the AN/ASQ-239 family. This major program continues to expand the EW hardware and software upgrade pipeline.

REPORT COVERAGE

The global cognitive electronic warfare market analysis provides an in-depth study of the market size, company profiling & forecast and all the market segments included in the report. It includes details on the market dynamics and expected trends in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The report also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By EW Function

|

|

By Platform

|

|

|

By System

|

|

|

By Component

|

|

|

By Cognitive Type

|

|

|

By Frequency

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights the global market value is anticipated at USD 11.48 billion in 2026 and is projected to reach USD 25.95 billion by 2034.

In 2025, North Americas market value stood at USD 4.06 billion.

The market is expected to exhibit a CAGR of 10.7% during the forecast period of 2026-2034.

The Airborne (fighters, EW pods, UAV payloads) led the market by Platform.

Rapid survivability upgrades against evolving radar and drone threats are driving growth in the CEW market.

BAE Systems, RTX (Raytheon), and L3Harris Technologies for large-scale airborne and joint-domain electronic attack and jamming portfolios, alongside integrated mission-systems and technologically advanced EW suite leaders such as Lockheed Martin, Northrop Grumman, and Leonardo for platform-embedded cognitive EW architectures and upgrade pathways, and major European champions including Thales, Saab, and HENSOLDT for wideband sensing, EW sensor suites, and electromagnetic battle management capabilities, with additional strength from Elbit Systems, Israel Aerospace Industries (ELTA), and Rafael for combat-proven self-protection, digital EW payloads, and rapid reprogrammable effects, among others, are the top companies in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us