Coherent Radar Market Size, Share & Industry Analysis, By Platform (Ground Based, Airborne, and Naval & Coastal), By Application (Air Surveillance & Defense, Fire-control & Radar Tracking, Counter-UAS & Perimeter Security, Air Traffic Control, & Others), and 28V DC), By Frequency Band (L/S Band, X Band, Ku/Ka Band, & Others), By Technology (Pulsed Coherent, Frequency Modulated Continuous Wave Coherent, and Phase-Coded Continuous Wave), By Component (Antenna, Receiver & Processor, Transmitter, & Others), By End Use (Defense & Security, Aerospace, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

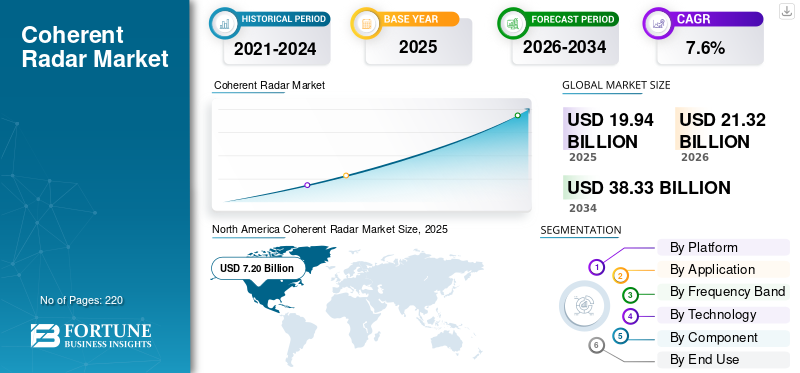

The global coherent radar market size was valued at USD 19.94 billion in 2025. The market is projected to grow from USD 21.32 billion in 2026 to USD 38.33 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period. North America dominated the global coherent radar market with a market share of 36.10% in 2025.

The global market is poised for robust expansion, fueled by escalating defense budgets, the surge in unmanned aerial systems (UAS), and growing needs for precise weather monitoring and air traffic management. Coherent radars, leveraging phase-coherent signal processing for superior Doppler velocity accuracy and clutter rejection, are increasingly vital for detecting low-observable targets, tracking hypersonic threats, and enabling synthetic aperture imaging in complex environments. Moreover, there is an increase in demand for advanced radar systems to provide advanced surveillance, and precise identification in defense applications, which is expected to drive the coherent market demand.

- For instance, in December 2025, Leonardo has secured a contract with Italy's TELEDIFE to develop and deliver four next-generation coherent radars Ground Based Radar (GBR) and Mobile Long Range Radar (MLRR) for the Michelangelo Dome defense system, targeting long-range ballistic threats up to 3,000 km.

Additionally, key players such as Raytheon Technologies, Thales Group, Lockheed Martin, and Hensoldt are advancing innovations such as AI-integrated beamforming, quantum-enhanced sensors, and compact AESA (Active Electronically Scanned Array) systems with software-defined capabilities for seamless upgrades and reduced lifecycle costs.

Download Free sample to learn more about this report.

Coherent Radar Market Key Takeaways

- 2025 Market Size: USD 19.94 billion

- 2026 Market Size: USD 21.32 billion

- 2034 Forecast Market Size: USD 38.33 billion

- CAGR: 7.6% from 2026–2034

- North America dominated the coherent radar market with a 36.10% share in 2025.

- The airborne segment is projected to grow at a CAGR of 8.6% during the forecast period.

- The counter-UAS & perimeter security segment is expected to register a CAGR of 9.4% over the forecast period.

Asia Pacific

Asia Pacific emerged as the second-largest regional market with a valuation of USD 4.55 billion in 2025.

North America

North America generated USD 7.20 billion in revenue in 2025 and is projected to reach USD 7.64 billion in 2026.

Europe

Europe is projected to register a CAGR of 9.0% during the forecast period.

U.S.

The U.S. coherent radar market was valued at approximately USD 6.57 billion in 2025.

Japan

Japan’s coherent radar market was valued at approximately USD 0.71 billion in 2025.

Read More

COHERENT RADAR MARKET TRENDS

Advancements in AI-Integrated, GaN-Enhanced Coherent Radar Technology is a Prominent Trend Observed in Market

Advancements in AI-integrated and GaN-enhanced coherent radar technology are gaining traction in the global radar market. Leading developers are embedding machine learning algorithms, cognitive signal processing, and software-defined architectures into coherent radars to boost the classification and efficiency of the radar systems. Moreover, GaN adoption drives coherent radar growth by boosting phase-coherent performance. These innovations also streamline deployment, cut lifecycle costs, and facilitate seamless upgrades for multi-mission operations in defense and air traffic control.

- For instance, in May 2025, RTX's Raytheon completed the first flight test of its PhantomStrike radar, a GaN-powered, air-cooled AESA fire-control system that tracked airborne targets.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Defense Budget and Modernization is Expected to Drive Market Growth

A primary driver for the coherent radar industry is the global surge in defense budgets and accelerated modernization initiatives.

- For instance, according to the Stockholm International Peace Research Institute (SIPRI), worldwide military expenditure hit USD 2.44 trillion in 2024, up 6.8% from 2023, with significant allocations for advanced radar systems. Moreover, as per NATO reports, member nations plan to invest in air defense upgrades by 2030.

Such defense modernization spending boosts demand for coherent radars with superior Doppler processing, clutter rejection, and multi-mission versatility. As militaries retrofit fleets, deploy networked sensor grids, and counter hypersonic threats, there's a rising need for fixed and mobile coherent systems to deliver precise tracking, early warning, and integration with missile defense architectures.

MARKET RESTRAINTS

High Development and Integration Costs to Limit Market Expansion

A significant restraint for the market is the significant investment required for R&D, GaN-based AESA manufacturing, and system integration into existing defense platforms. These technologically advanced radars demand specialized materials, rigorous testing for ballistic threat performance, and compatibility with multi-domain networks. These advanced radars demand specialized materials such as high-purity Gallium Nitride substrates, rigorous testing for ballistic threat performance over extreme ranges. Therefore, the cost structure discourages adoption by smaller defense forces and emerging markets, which is expected to restrain the coherent radar market growth.

MARKET OPPORTUNITIES

Evolving Spectrum Regulations and Demand for Resilient Surveillance Presents Growth Opportunities for Market Growth

Evolving spectrum management regulations from bodies such as the ITU and national authorities are driving the adoption of advanced coherent radars by mandating efficient use of congested electromagnetic spectrum and enhanced resilience against electronic warfare threats. The rise in demand for advanced radar systems for navigation, collision avoidance, and surveillance in adverse conditions is propelling market growth.

- For instance, in October 2024, Systematic successfully integrated Hensoldt's SharpEye Mk 11 coherent radar into SitaWare Headquarters, boosting maritime domain awareness for Ireland's Naval Service offshore patrol vessels.

Coherent radars enable precise Doppler processing and real-time threat discrimination without excessive bandwidth consumption, aligning with broader needs for spectrum-efficient surveillance. Such factors accelerate innovation and deployment of next-generation coherent radars across allied forces, presenting lucrative opportunities for market growth.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Critical Components Acts a Challenge for Market

A major restraint for the market stems from supply chain dependencies on specialized components such as Gallium Nitride (GaN) semiconductors and high-power RF modules. These materials require advanced fabrication processes prone to production challenges, geopolitical export restrictions, and supply chain hurdles. This vulnerability disrupts program timelines for systems such as next-gen defense radars, increases customization costs for military integrators, and hampers scalability for widespread deployment.

Segmentation Analysis

By Platform

Rising Defense Budgets and Geopolitical Tensions to Propel Segmental Growth

Based on the platform, the market is divided into ground based, airborne, and naval & coastal.

The ground based segment is anticipated to account for the largest coherent radar market share. The growth driven by the rising global defense budgets, which prioritize advanced surveillance and threat detection capabilities during geopolitical tensions. Moreover, urban security and border surveillance applications are accelerating adoption, as these radars offer clutter rejection in complex environments.

- For instance, in August 2025, Northrop Grumman will supply Paraguay with its AN/TPS-78 ADCAP long-range radars via the U.S. Foreign Military Sales program. The radar will enable precise detection and tracking of manned and unmanned aircraft.

The airborne segment is anticipated to rise with a CAGR of 8.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Defense Spending Surge and Development of ECM-Resistant Phased Arrays to Propel Segmental Growth

By application, the market is segmented into air surveillance & defense, fire-control & radar tracking, counter-UAS & perimeter security, air traffic control, and others.

The air surveillance & defense segment is anticipated to account for the largest market share, as the geopolitical tensions and rising defense expenditures worldwide are fueling procurement of advanced radar systems. Moreover, there is a rise in demand for phase array coherent radar systems for 3D air/surface surveillance, and Electronic Countermeasures (ECM) resistance which drives segment growth.

- For instance, in October 2023, HENSOLDT secured a USD 10M follow-on contract to equip the U.S. Coast Guard's Legend-class National Security Cutter with its advanced TRS-3D multi-mode naval radar. The radar detects small, low-altitude threats such as aircraft, missiles, and helicopters while supporting air/surface surveillance and warfare systems.

The counter-UAS & perimeter security segment is projected to grow at a steady annual growth rate (CAGR) of 9.4% over the forecast period.

By Frequency Band

High-Resolution Drone/Stealth Detection in Cluttered Environments Push Segment Growth

Based on frequency band, the market is segmented into L/S band, X band, Ku/Ka band, and others.

X band accounts for the largest market share of the industry due to high-resolution imaging capabilities, enabled by shorter wavelengths (8-12 GHz) that deliver accurate target discrimination for small objects such as drones and stealth threats in cluttered environments. The radars operating in X band are increasingly being procured for integrating with various platforms for precise on-the-move target tracking and classification.

- For instance, in July 2024, HENSOLDT secured a nearly USD 117.70 million contract from Rheinmetall Air Defense to supply SPEXER 2000 3D MkIII radars for the Skyranger 30 anti-aircraft gun tanks.

The Ku/Ka band segment is expected to grow with a fastest growth rate of 9.0% over the forecast period.

By Technology

Hypersonic Threat Response and High Doppler Precision Support Segment Growth

Based on technology, the market is segmented into pulsed coherent, frequency modulated continuous wave (FMCW) coherent, and phase-coded continuous wave (CW).

The pulsed coherent segment is forecasted to capture the largest market share. The segment leads the market due to its precise phase-coherent pulse compression techniques, which provide high range resolution and accurate Doppler velocity measurements. It is increasingly preferred for distinguishing slow-moving targets in defense surveillance applications. The rising demand from air defense networks and missile warning systems, driven by hypersonic threats is expected to support segment growth.

The frequency modulated continuous wave (FMCW) coherent segment is projected to emerge as the fastest-growing at a CAGR of 8.5% over the forecast period.

By Component

AESA Beam Steering Innovation and Initiatives for National Security Fuel Segment Growth

Based on component, the market is segmented into antenna, receiver & processor, transmitter, software, and others.

The antenna segment is expected to hold the largest market share in 2025. The segment is growing significantly due to its critical role in enabling high-gain, electronically scanned arrays (AESA) that deliver precise beam steering and multi-functionality for defense and surveillance applications. Moreover, countries are launching radar projects to counter escalating geopolitical tensions and terrorism threats.

- For instance, in April 2024, India's DRDO launches TDF project for shared aperture phased array antennas integrating radar, electronic warfare, and communication systems in 1-6 GHz and 5-18 GHz bands for coherent active electronically scanned array (AESA) radars.

The receiver & processor segment is projected to grow with a steady growth rate at a CAGR of 8.2% over the forecast period.

By End Use

Global Defense Budgets and 360° Drone/Missile Surveillance Integration Fuel Segment Growth

Based on end use, the market is segmented into defense & security, aerospace, automotive, maritime, and others.

The defense & security segment is expected to hold the highest market share in 2025. The factors attributing to segment growth are increase in global defense budget and rise in modernization of weapon and radar systems. Moreover, there is also a surge in integration of radar into defense systems for continuous 360° surveillance, detecting drones (up to 9-12 km for UAVs/micro-UAS), helicopters (36 km), missiles, and other targets.

- For instance, in April 2024, Germany advanced European defense leadership by expanding its Puma IFV fleet to 1,087 vehicles by 2035 for 17 mechanized battalions, paired with layered air defenses such as Skyranger 30. The radar in defense system is used to enable precise, jam-resistant tracking of low-signature threats such as quadcopters.

The aerospace segment is projected to grow with a steady growth rate at a CAGR of 8.9% over the forecast period.

Coherent Radar Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

North America

North America Coherent Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market dominated in 2025 with a valuation of USD 7.20 billion, growing to USD 7.64 billion in 2026, driven by defense investments in next-gen AESA systems for fighter jets and missile defense. The U.S. leads due to high defense budgets and widespread upgrades to coherent radars for superior Doppler processing in cluttered environments. Moreover, there is rising adoption of ground-based coherent radars for border security and wildfire detection, accelerating market expansion.

U.S Coherent Radar Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 6.57 billion in 2025. The country maintains its leading position due to accelerated funding for military radar retrofits and expansion of ATM infrastructure at major hubs, driving demand for high-resolution, jam-resistant coherent systems. The U.S. is investing in next-gen programs, encouraging more defense contracts and faster adoption across air forces.

- For instance, in December 2025, the U.S. Air Force is upgrading its experimental X-62 VISTA AI autonomy testbed with advanced radar and mission systems.

Europe

Europe is projected to record a growth rate of 9.0% during 2026 to 2034, which is the second highest among all regions. The market in the region grows due to surging defense budgets amid geopolitical tensions, with NATO members such as Italy investing heavily in systems such as Leonardo's Michelangelo Dome for ballistic missile defense.

Modernization programs across the U.K., France, and Germany prioritize GaN-AESA coherent radars for superior threat tracking and spectrum efficiency.

- For instance, in December 2025, German defense firm Hensoldt increased the production of its TRML-4D air surveillance radars to 30 units annually, driven by rising European demand and signals intelligence needs.

The rise of unmanned systems and counter-drone needs further accelerates adoption, as coherent processing is suitable in cluttered environments. In addition, collaborative European Union (EU) initiatives and national procurements ensure steady demand for these advanced surveillance technologies.

U.K Coherent Radar Market

The U.K. market in 2025 is estimated at around USD 0.67 billion, representing roughly 3.4% of global coherent radar revenues.

France Coherent Radar Market

France market is projected to reach approximately USD 0.63 billion in 2025, equivalent to around 3.1% of global coherent radar sales.

Asia Pacific

Asia Pacific market is estimated to reach USD 4.55 billion in 2025 and secure the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 0.05 billion and USD 0.10 billion, respectively in 2025. Asia Pacific represents the fastest-growing region for coherent radars, propelled by increased air traffic at airports. The region tensions and defense modernization efforts in countries such as China, India, and South Korea. Nations are increasing investments in air surveillance and maritime radars to counter threats which drives market growth in the region.

Japan Coherent Radar Market

The Japan market in 2025 is estimated at around USD 0.71 billion, accounting for roughly 3.6% of global coherent radar revenues. .

China Coherent Radar Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 1.85 billion, representing roughly 9.3% of global coherent radar sales.

India Coherent Radar Market

The India market in 2025 is estimated at around USD 1.01 billion, accounting for roughly 5.1% of global coherent radar revenues.

Latin America and the Middle East & Africa

Latin America and the Middle East and Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.00 billion in 2025, driven by expanding commercial aviation in Brazil and Mexico, where airports integrate coherent radars for severe weather monitoring and ATM resilience during the increased passenger traffic.

Saudi Arabia Coherent Radar Market

The Saudi Arabia market is projected to reach around USD 0.73 billion in 2025, representing roughly 1.4% of global coherent radar revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on AESA Radar Advancements and Defense Integrator Partnerships by Key Players to Propel Market Progress

The global coherent radars market remains consolidated, led by major players such as Raytheon Technologies, Lockheed Martin, Thales Group, and Leonardo S.p.A., which hold significant shares through innovations in high-resolution AESA radars and GaN-based (Gallium Nitride) phased-array systems. These firms advance market growth with strategic partnerships with defense ministries and OEM collaborations. They focus on the development of multi-function coherent radars for air defense, surveillance, and ATM integration through various strategies and alliances with other key players.

- For instance, in May 2025, Hensoldt signed a framework agreement with Rheinmetall Air Defence AG to supply SPEXER 2000 radars for systems such as the Skyranger 30 and drone defense through the 2030s.

Other prominent players operating in the market include Northrop Grumman, Saab, and L3Harris Technologies, which are prioritizing R&D in quantum-enhanced signal processing, joint ventures for next-gen fighter programs, and scalable production to capture rising demand from geopolitical tensions and airspace modernization mandates.

LIST OF KEY COHERENT RADAR COMPANIES PROFILED

- Hensoldt AG (Germany)

- RTX Corporation (U.S.)

- BAE Systems plc (U.K.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Saab AB (Sweden)

- L3Harris Technologies Inc. (U.S.)

- Israel Aerospace Industries Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

For Internal / External PRs:

- June 2025: U.S. Army mounted the EchoShield cognitive radar on a Stryker vehicle during Project Flytrap. The system is used to detect low-flying drones and delivered real-time location data to troops' devices, boosting C-UAS situational awareness.

- https://defence-blog.com/u-s-army-tests-new-drone-defense-radar/

- May 2025: The Indian Army plans to induct an advanced Low Level Lightweight Radar (LLLWR) featuring GaN-based AESA technology to detect low-observable threats.

- https://defence.in/threads/indian-army-to-boost-battlefield-vision-with-gan-based-aesa-radar-enhancing-tactical-surveillance-against-diverse-low-observable-modern-threats.14194/#google_vignette

- December 2025: Acconeer launched its multichannel A212 Pulsed Coherent Radar sensor and received USD 380,000 order from a European premium automaker set for H1 2026 rollout.

- October 2025: German defense firm Hensoldt announced a new production site in Ulm to manufacture TRML-4D air surveillance and Spexer ground/coastal radars, targeting 1,000 units annually from 2027 after a mid-double-digit million-euro investment.

- October 2025: Danish firm Systematic successfully integrated the Mk11 Sharpeye navigation radar into its SitaWare Headquarters C4ISR software for the Irish Naval Service's Samuel Beckett-class patrol vessels.

- May 2025: The Indian Army enhanced border surveillance with the next-generation LLLR(I), a pulse-Doppler software-defined radar featuring non-moving 360-degree phased-array coverage for low-level threat detection.

- August 2023: Hensoldt and ERAa-Tech announced a partnership to develop passive advanced air-surveillance and air-defense solutions, combining their coherent radar technologies for a comprehensive integrated air picture.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform, Application, Frequency Band, Technology, Component, End Use, and Region |

|

By Platform |

· Ground Based · Airborne · Naval & Coastal |

|

By Application |

· Air Surveillance & Defense · Fire-control & Radar Tracking · Counter-UAS & Perimeter Security · Air Traffic Control · Others |

|

By Frequency Band |

· L/S Band · X Band · Ku/Ka Band · Others |

|

By Technology |

· Pulsed Coherent · Frequency Modulated Continuous Wave (FMCW) Coherent · Phase-Coded Continuous Wave (CW) |

|

By Component |

· Antenna · Receiver & Processor · Transmitter · Software · Others |

|

By End Use |

· Commercial · Military |

|

By Region |

· North America ( By Platform, By Application, By Frequency Band, By Technology, By Component, By End Use, and Country) o U.S. (By End Use) o Canada (By End Use) · Europe ( By Platform, By Application, By Frequency Band, By Technology, By Component, By End Use, and Country) o U.K. (By End Use) o Germany (By End Use) o France (By End Use) o Russia (By End Use) o Rest of Europe (By End Use) · Asia Pacific ( By Platform, By Application, By Frequency Band, By Technology, By Component, By End Use, and Country) o China (By End Use) o Japan (By End Use) o India (By End Use) o South Korea (By End Use) o Rest of Asia Pacific (By End Use) · Latin America ( By Platform, By Application, By Frequency Band, By Technology, By Component, By End Use, and Country) o Brazil (By End Use) o Mexico (By End Use) o Rest of Latin America( By Aircraft Type) · Middle East & Africa ( By Platform, By Application, By Frequency Band, By Technology, By Component, By End Use, and Country) o UAE (By End Use) o Saudi Arabia (By End Use) o Rest of the Middle East & Africa (By End Use) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 19.94 billion in 2025 and is projected to reach USD 38.33 billion by 2034.

In 2024, the market value stood at USD 7.20 billion.

The market is expected to exhibit a CAGR of 7.6% during the forecast period.

By platform, the ground based segment is expected to lead the market.

The rise in defense budget and modernization are driving market expansion.

Hensoldt AG (Germany), RTX Corporation (U.S.), BAE Systems plc (U.K.), and Leonardo S.p.A. (Italy), among others are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us