Cold Chain Telematics Market Size, Share & Industry Analysis, By End-User Industry (Pharmaceuticals & Biologics, Food & Beverages, Chemicals, and Healthcare & Clinical Logistics), By Component (Hardware, Software, and Services), By Mode of Transport (Road, Rail, Sea/Waterways, and Air), By Connectivity Technology (Cellular, Satellite, LPWAN, and RFID & Short-Range Communication), and Regional Forecast, 2026-2034

Cold Chain Telematics Market Size and Future Outlook

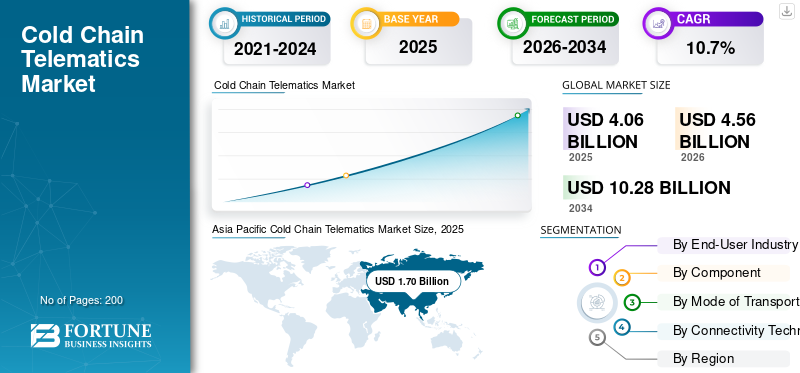

The cold chain telematics market size was valued at USD 4.06 billion in 2025. The market is projected to grow from USD 4.56 billion in 2026 to USD 10.28 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period. Asia Pacific dominated the cold chain telematics market with a market share of 41.87% in 2025.

Cold chain telematics refers to the use of connected tracking devices, sensors, and software to monitor management of temperature sensitive goods during storage and transport. It provides real-time visibility into temperature, location, humidity, door events, and shocks, enabling alerts, compliance reporting, and reduced spoilage. The market growth is driven by stricter regulations related to food and pharma for maintaining product quality requirements, rising volumes of biologics and vaccines, and expanding refrigerated transport and cold storage infrastructure. Companies need real time visibility to prevent temperature excursions, cut waste, and improve traceability. Digitalization of logistics, wider cellular IoT coverage, and demand for analytics also accelerate adoption across road, sea, air, and warehouses.

Major players include ORBCOMM Inc., Controlant, Sensitech Inc., DeltaTrak, Tive, Roambee Corporation, Geotab Inc., Samsara Inc., Carrier Transicold (Lynx), and Thermo King. Few key trends are bundled telematics with refrigeration equipment, cloud-based monitoring platforms, multi-sensor visibility (temp/door/shock), automated compliance reporting, and higher use of real-time alerts and analytics to reduce losses.

Download Free sample to learn more about this report.

Cold Chain Telematics Market Takeaways

- 2025 Market Size: USD 4.06 billion

- 2026 Market Size: USD 4.56 billion

- 2034 Forecast Market Size: USD 10.28 billion

- CAGR: 10.7% from 2026–2034

- Asia Pacific dominated the cold chain telematics market with a 41.87% share in 2025.

- The Food & Beverages segment held the largest market share due to the high volume of temperature-sensitive products requiring continuous monitoring.

- The Road segment dominated the market, while the Sea/Waterways segment is projected to grow at the fastest 11.5% CAGR during the forecast period.

North America

The mature market continues to expand through widespread adoption of IoT-enabled fleet management, cloud monitoring platforms, and predictive analytics.

Europe

Strong growth is supported by pharmaceutical exports, advanced cold storage networks, and stringent regulatory compliance for food and medicine transportation.

Asia Pacific

The region is the largest and fastest-growing market, driven by expanding cold storage infrastructure, pharmaceutical production, and food exports.

U.S.

The market is projected to reach USD 1.01 billion in 2026, supported by its extensive refrigerated logistics network and pharmaceutical distribution infrastructure.

Japan

The market was valued at USD 0.18 billion in 2024, driven by advanced cold chain standards and strong seafood and pharmaceutical trade.

Read More

COLD CHAIN TELEMATICS MARKET TRENDS

Expansion of Smart, Real-Time Monitoring Platforms Accelerates Digital Transformation

Cold chain telematics is increasingly shifting from standalone data loggers to integrated, cloud-based real-time monitoring platforms. Companies currently demand centralized dashboards, automated alerts, predictive analytics and remote diagnostics for assets across fleets and warehouses. Integration with IoT sensors connectivity and API-based supply chain systems enables end-to-end visibility and faster response to temperature excursions. This transformation improves compliance documentation and reduces manual intervention, making telematics a core operational system rather than a tracking add-on. The trend is particularly visible in multimodal logistics, where continuous monitoring across road, sea, and air is critical.

- In October 2023, Thermo King announced TracKing telematics would be included as standard on certain trailer units, reflecting OEM-level integration of connected monitoring.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Pharmaceutical and Biologics Distribution Increases Product Adoption

The global expansion of biologics, specialty medicines, and temperature-sensitive vaccines is significantly driving the cold chain telematics market growth. Biologics often require narrow temperature ranges and continuous documentation throughout transport and storage. Regulatory frameworks emphasize traceability, excursion reporting, and validated monitoring systems. As pharmaceutical trade volumes rise and supply chains become more globalized, real-time telematics solutions help reduce product loss and ensure regulatory compliance. This driver is particularly strong in cross-border shipments and clinical trial logistics, where shipment integrity is critical.

- In April 2024, Eurostat reported that the U.S. accounted for 33.2% of EU extra-EU pharmaceutical exports in 2023, highlighting the scale of temperature-sensitive cross-border pharma trade.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity Constrain Market Deployment

Despite long-term cost savings, the upfront costs of hardware devices, connectivity subscriptions, integration with refrigeration systems, and team member training can be substantial, especially for small and mid-sized logistics operators. Integration with legacy fleet management systems and cold storage infrastructure may require customization and IT upgrades. In emerging markets, limited digital infrastructure and fragmented cold chain networks further slows product adoption. Concerns about cybersecurity and data privacy also complicate deployment decisions. These financial and operational barriers can delay telematics investments, particularly in cost-sensitive food and beverage distribution sector where margins are thin and capital expenditure is closely controlled.

MARKET OPPORTUNITIES

Emerging Cold Chain Infrastructure in Developing Economies Creates Untapped Potential

Rapid expansion of cold storage facilities and refrigerated logistics networks in developing regions presents significant growth opportunities for market. As infrastructure scales, operators increasingly seek digital monitoring to improve efficiency and preventing spoilage losses. Governments and private investors are modernizing food supply chains, supporting higher adoption of connected monitoring systems. Growing organized retail, pharmaceutical manufacturing, and export-oriented agriculture further strengthen this opportunity. As connectivity coverage improves, cloud-based and mobile-enabled telematics platforms can be deployed more cost-effectively across distributed assets and facilities.

- In February 2023, GCCA reported that global cold storage capacity reached 719 million cubic meters, reflecting substantial infrastructure expansion worldwide.

MARKET CHALLENGES

Data Management, Interoperability, and Standardization are Key Industry Challenges

Cold chain telematics systems generate large volumes of temperature, location, and event data. Managing, analyzing, and securely storing this data across different hardware brands, transport modes, life science and software platforms remains complex. The lack of universal interoperability standards can limit seamless data sharing among logistics partners, shippers, and regulatory requirements authorities. Inconsistent reporting formats and varying compliance requirements across countries further complicate cross-border operations. Without standardized frameworks, companies may end up with duplicated systems or data silos, thereby reducing efficiency gains. Addressing interoperability and cybersecurity risks will be critical as global supply chains become more digitally connected and reliant on real time monitoring.

Segmentation Analysis

By End-User Industry

Demand for Cost-Efficient and Temperature-Sensitive Food Distribution Drives Food & Beverages Segment Growth

Based on end-user industry, the market is segmented into pharmaceuticals & biologics, food & beverages, chemicals, and healthcare & clinical logistics.

Food & beverages segment held highest cold chain telematics market share due to the sheer volume of temperature sensitive products such as dairy, seafood, meat, frozen foods, and fresh produce moving across domestic and international supply chains. Large-scale refrigerated transport fleets and cold storage facilities require continuous monitoring to reduce spoilage and ensure products compliance with food safety regulations. Rising cross-border agri-food trade further amplifies the deployment of telematics in reefer containers and trucks.

- In June 2023, the WTO reported that global agricultural trade reached a record USD 2.1 trillion in 2022, highlighting the scale of temperature-controlled food movement worldwide.

To know how our report can help streamline your business, Speak to Analyst

The healthcare & clinical logistics segment is projected to grow at a 12.5% CAGR over the forecast period.

By Mode of Transport

High Fleet Density and Last-Mile Requirements Propel Road Segment Growth

Based on mode of transport, the market is segmented into road, rail, sea/waterways, and air.

Road segment dominates the market, with refrigerated trucks and trailers forming the backbone of domestic and cross-border cold chain distribution. Telemetry devices provide real-time temperature and location tracking for last-mile and regional deliveries. The high number of road-based reefer vehicles compared to other modes ensures the largest installed telematics base.

In 2023, the International Institute of Refrigeration noted that refrigerated road transport accounted for the largest share of temperature-controlled logistics assets globally.

The sea/waterways segment is projected to grow at a CAGR of 11.5% over the forecast period.

By Component

Large-Scale Deployment of Sensors and Tracking Units Leads to Hardware Segment Leadership

Based on component, the market is segmented into hardware, software, and services.

Hardware dominates as telematics deployment begins with the physical installation of temperature sensors, telematics control units, GPS devices and RFID tags across fleets and cold storage facilities. Growth in refrigerated warehouse capacity and transport assets directly translates into higher hardware demand. Replacement cycles and calibration needs also sustain recurring device sales.

- In May 2024, the U.S. Department of Agriculture reported that total refrigerated warehouse capacity reached 3.70 billion cubic feet in 2023, reflecting expanding infrastructure that requires monitoring hardware.

The software segment is projected to grow at a CAGR of 12.7% over the forecast period.

By Connectivity Technology

Widespread Mobile Network Coverage Enhances Cellular Telematics Adoption

Based on connectivity technology, the market is segmented into cellular, satellite, LPWAN, and RFID & short-range communication.

Cellular dominates due to its broad coverage, real-time data transmission capability, and compatibility with cloud-based monitoring platforms. The rapid expansion of LTE-M, NB-IoT, and 5G networks enables scalable and cost-efficient telematics integration across fleets and warehouses.

The cellular segment is projected to grow at a CAGR of 11.1% over the forecast period, while LPWAN is expected to grow at a CAGR of 10.1%.

COLD CHAIN TELEMATICS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

Asia Pacific Cold Chain Telematics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America represents a mature yet steadily expanding market, supported by extensive refrigerated transport fleets, large warehouse infrastructure, and strong regulatory oversight in food and pharmaceutical logistics. High adoption of IoT-enabled fleet management and cloud-based monitoring platforms drives recurring software revenues. Cross-border food trade within the U.S., Canada, and Mexico further strengthens demand for real-time visibility and compliance documentation. Market growth is progressively driven by analytics integration, predictive maintenance, and automated reporting solutions rather than first-time hardware deployment, reflecting a transition toward data-driven cold chain optimization.

U.S. Cold Chain Telematics Market

The U.S. market leads with estimated value of USD 1.01 billion in 2026 due to its vast refrigerated warehouse capacity, extensive long-haul trucking network, and significant pharmaceutical distribution volume. Stringent food safety and drug distribution regulations accelerate telematics integration across fleets and storage facilities. This adoption is vital in biologics logistics, grocery retail distribution, and third-party cold storage operators implementing advanced monitoring platforms.

Europe

Europe is experiencing strong market growth driven by high pharmaceutical export activity, well-structured cold storage networks, and strict compliance frameworks governing food and medicine transport. The region benefits from well-developed multimodal logistics systems integrating road, rail, and sea routes. The increasing digitalization of supply chains and the emphasis on sustainability reporting further encourage the adoption of telematics. Growth is concentrated in pharmaceutical monitoring and cross-border EU trade, where real-time temperature tracking and audit-ready documentation are essential for regulatory compliance and operational transparency.

U.K. Cold Chain Telematics Market

The U.K. market benefits from strong pharmaceutical distribution, advanced retail cold chains, and high import-export activity in temperature-sensitive goods. Post-Brexit customs controls have increased the need for real-time shipment visibility and compliance documentation. Cold storage operators increasingly deploy integrated telematics platforms to manage multi-site temperature monitoring and maintain supply chain efficiency. U.K. is expected to contributed to a share of 12.0% of the revenue in the 2026.

Germany Cold Chain Telematics Market

Germany is a key European logistics hub, with robust pharmaceutical manufacturing and industrial chemical transport, and is expected to maintain the highest CAGR of 9.0% during the forecast period. Its advanced rail and road infrastructure supports multimodal cold chain movement. Export-oriented pharma distribution, stringent compliance standards, and digital transformation initiatives across the logistics and manufacturing sectors drive demand for telematics.

Asia Pacific

Asia Pacific is the fastest-growing and dominant regional market, supported by expanding cold storage capacity, rising pharmaceutical production, and rapidly growing food exports. Increasing urbanization and the growth of organized retail drive demand for refrigerated transport monitoring. The region’s dominance in containerized trade further strengthens adoption in maritime cold chain logistics. Governments and private operators are modernizing supply chain infrastructure, creating strong opportunities for integrated telematics solutions. Growth is particularly dynamic in emerging economies where digital cold chain systems are being implemented alongside new infrastructure development.

China Cold Chain Telematics Market

China dominated Asia Pacific market with 40.42% in 2025 due to its large cold storage footprint, strong export-driven food trade, and expanding biologics manufacturing sector. Growing domestic e-commerce grocery distribution and improvements in pharmaceutical supply chain standards are accelerating the deployment of telematics across warehouses and transport fleets.

Japan Cold Chain Telematics Market

Advanced cold chain standards and strong seafood and pharmaceutical trade characterize Japan’s market, valued at USD 0.18 billion in 2024. As an island economy, maritime transport plays a major role in temperature-controlled logistics. Companies emphasize precision monitoring, automation, and compliance documentation, sustaining demand for integrated telematics systems.

India Cold Chain Telematics Market

India’s market is experiencing rapid cold chain expansion, with a 14% CAGR, driven by agricultural modernization, vaccine distribution, and growth in organized food retail. Infrastructure development initiatives and increasing pharmaceutical exports are strengthening the adoption of real-time monitoring technologies across transport and storage networks.

Rest of the World

The Rest of the world including Latin America, the Middle East & Africa, shows steady growth from a smaller base. Expanding food export industries, improving healthcare supply chains, and investments in cold storage infrastructure support telematics demand. Adoption remains uneven due to infrastructure gaps, but modernization initiatives and increasing trade connectivity are driving the gradual penetration of monitoring solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated IoT Platforms, Real-Time Visibility and Strategic Partnerships Define Cold Chain Telematics Competition

The global cold chain telematics market trends are characterized by rapid digitalization, increasing IoT penetration, and strong collaboration between technology providers, refrigeration OEMs, and logistics operators. Leading players such as ORBCOMM Inc., Sensitech Inc., Controlant, Tive, Roambee Corporation, DeltaTrak, Geotab Inc., Samsara Inc., Carrier Transicold, and Thermo King compete through end-to-end monitoring platforms that combine multi-parameter sensors, GPS tracking, cloud dashboards, and predictive analytics. Companies differentiate themselves through pharmaceutical-grade compliance capabilities, real-time alert systems, multimodal tracking, and scalable SaaS models. Strategic expansion of global monitoring centers and integration with fleet management and warehouse systems strengthen competitive positioning. Partnerships with telecom operators and cloud providers enhance connectivity, reliability, and cybersecurity resilience. Vendors are increasingly bundling telematics with refrigeration equipment and offering subscription-based service models, shifting competition toward data-driven insights, interoperability, and value-added analytics rather than standalone hardware sales.

LIST OF KEY COLD CHAIN TELEMATICS COMPANIES PROFILED

- Sensitech Inc. (U.S.)

- ORBCOMM Inc. (U.S.)

- Controlant (Iceland)

- Emerson Electric Co. – Copeland (U.S.)

- Carrier Transicold (U.S.)

- Thermo King (U.S.)

- Monnit Corporation (U.S.)

- ELPRO-BUCHS AG (Switzerland)

- Berlinger & Co. AG (Switzerland)

- Testo SE & Co. KGaA (Germany)

- Rotronic AG (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Roambee Corporation (U.S.)

- Geotab Inc. (Canada)

- Samsara Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: DeltaTrak launched a new generation of FlashLink NOW real-time loggers to strengthen inbound compliance programs for increasing consumer demand for fresh suppliers. The offering is positioned to meet tightening retailer acceptance requirements by expanding shipment visibility beyond basic temperature logging, supporting more proactive quality control, and faster exception handling during refrigerated distribution.

- February 2026: DHL Group announced an expansion of its dedicated Airfreight Cold Chain Network to advance global health logistics. The initiative aims to increase controlled capacity and improve reliability for temperature-sensitive medicines, vaccines, and cell & gene therapies, reinforcing demand for continuous monitoring, documented compliance, and real-time shipment control in air-mode cold chains.

- January 2026: Thermo King expanded its TracKing connectivity platform with new AI-driven capabilities, introducing Ask TracKing and ColdChain Link. The upgrade targets faster access to operational insights, streamlined fleet tasks, and stronger traceability for refrigerated transport customers across EMEA, shifting competition toward smarter decision support, not just device data collection.

- January 2026: CSCS and SYNTRA announced a strategic partnership to unify real-time cargo visibility with agentic AI-driven orchestration. By combining SYNTRA’s shipment/sensor data with CSCS’s SCOTI platform, the collaboration aims to deliver end-to-end supply chain intelligence, faster exception cold chain management, and actionable alerts for cold-chain operations requiring rapid intervention.

- November 2025: Delta Cargo launched Pulse, a new shipment tracking and visibility solution powered by Trackonomy. The platform is designed to improve transparency and real-time location visibility across Delta’s airfreight network, supporting tighter control for time and temperature-sensitive cargo and raising expectations for digital visibility in air logistics service offerings.

REPORT COVERAGE

The cold chain telematics market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The cold chain telematics market forecast provides a comprehensive competitive landscape, encompassing the largest market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By End-User Industry, By Component, By Mode of Transport, By Connectivity Technology, and By Region |

| By End-User Industry |

|

| By Mode of Transport |

|

| By Component |

|

| By Connectivity Technology |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.06 billion in 2025 and is projected to reach USD 10.28 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.70 billion.

The market is expected to grow at a CAGR of 10.7% during the forecast period of 2026-2034.

The cellular led the market share in the connectivity technology segment.

Growing pharmaceutical and biologics distribution drives monitoring adoption.

Top players in the market include ORBCOMM Inc., Controlant, Sensitech, DeltaTrak, Tive, Roambee Corporation, Geotab Inc., and Samsara Inc.

Asia Pacific accounted for the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us