Combat Support Vehicles Market Size, Share & Industry Analysis, By Vehicle Type (Recovery, Maintenance, Combat Engineering, Crossing), By Platform (Tracked, Wheeled, Amphibious, Trailer-Based, Modular Mission, Robotic & Air-Transportable), By Weight Class (Ultra-Light, Light, Medium, Heavy, & Very Heavy), By Protection Level (Soft-Skin, Protected Cab, Armored), By Propulsion (Diesel ICE, Electric, Auxiliary, & Powertrain), By Procurement Model (New-Build Vehicles, Platform Conversion, Retrofit), By End User (Army, Marine, Operations) and Regional Forecast 2026-2034

COMBAT SUPPORT VEHICLES Market Size and Future Outlook

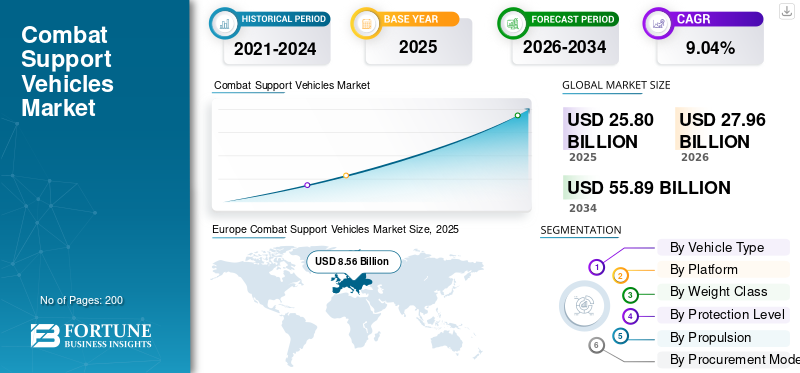

The global combat support vehicles market size was valued at USD 25.80 billion in 2025. The market is projected to grow from USD 27.96 billion in 2026 to USD 55.89 billion by 2034, exhibiting a CAGR of 9.04% during the forecast period. Europe dominated the combat support vehicles market with a market share of 33.17% in 2025.

The combat support vehicles market covers military vehicles that enable frontline forces to move, survive, recover, resupply, communicate, bridge obstacles, evacuate casualties, and sustain operations. It includes armored recovery vehicles, engineer/mine-clearing vehicles, bridge laying vehicles, command/mission vehicles, armored ambulances, tactical trucks, and protected utility/logistics platforms.

Demand is being pushed by replacement of aging fleets such as the U.S. Army’s M113-to-AMPV transition, battlefield lessons from Ukraine around recovery, bridging, and logistics support, and higher defense investment across NATO/EU countries.

Market expansion is further accelerated by force modernization initiatives, rising survivability requirements, mobility in contested terrain, rapid repair/recovery needs, research and development and multi-role modularity. Modern armies are no longer buying only truck-like support vehicles; they increasingly require protected, networked, mission-configurable platforms capable of operating close to the forward edge of battlefield.

Key players include BAE Systems pls, General Dynamics Land Systems Corporation, Rheinmetall AG, KNDS, and Oshkosh Defense Corporation. Overall, these companies are focusing on common chassis families, modular mission kits, localized production/JVs, export/FMS opportunities, digital vehicle architecture, lifecycle sustainment, and add-on protection/autonomy-ready capabilities.

Download Free sample to learn more about this report.

Combat Support Vehicles Market KEY TAKEAWAYS

- 2025 Market Size: USD 25.80 billion

- 2026 Market Size: USD 27.96 billion

- 2034 Forecast Market Size: USD 55.89 billion

- CAGR: 9.04% from 2026–2034

- Europe dominated the combat support vehicles market with a 33.17% share in 2025

- The C4ISR/surveillance support vehicles segment is projected to grow at the fastest CAGR of 11.50%

- The tracked platforms segment accounted for the largest market share of 54.59% in 2025

Asia Pacific

Asia Pacific reached USD 6.26 billion in 2025, driven by military modernization.

North America

North America reached USD 7.34 billion in 2025, supported by defense modernization programs.

Europe

Europe held a 33.19% market share in 2025, driven by NATO modernization initiatives.

U.S.

U.S. reached USD 6.86 billion in 2025, fueled by advanced defense vehicle demand

Japan

Japan is driven by growing defense modernization and regional security initiatives.

Read More

Combat Support Vehicles Market Trend

Rising Focus on Autonomy-ready Logistics Vehicles to Drive Industry Expansion

A major trend in the trend is the shift from single-role platforms to vehicles built toward common chassis, modular payloads, open architecture, and rapid capability kits. Militaries want support vehicles that can be upgraded throughout their lifecycle without requiring the entire platform. BAE’s AMPV strategy reflects this clearly, the company says it is investing in a more modular chassis to support quick integration of next-generation technologies. The AMPV family already covers medical, command, mortar, and general-purpose roles. Oshkosh Defense is advancing the modernization of its heavy tactical vehicles portfolio with a focus on autonomy-readiness capabilities. Its July 2025 U.S. Army FHTV order included HEMTT A4 variants and the autonomous-ready PLS A2, reinforcing the military’s focus on air-defense system integration and tactical logistics.

For instance, in April 2026, National Defense reported that the Army is examining autonomy across its wheeled vehicle fleet, with the Autonomous Transport Vehicle System identified as a critical component of future autonomous logistics operations, particularly on platforms such as the Palletized Load System.

Market Dynamics

MARKET DRIVER

Download Free sample to learn more about this report.

Growing Importance of Armored Support Fleets to Support Industry Growth

The main driver for the combat support vehicles market is the urgent need to replace aging military vehicles fleets that can survive in high-threat, drone-observed, artillery-heavy battlefields. Armed forces are investing in armored ambulances, medical evacuation vehicles, mission command vehicles, recovery vehicles, bridge layers, protected tactical trucks, and logistics platforms that can operate alongside combat formations rather than remain far behind them. The U.S. Army’s AMPV program is a clear example of this trend. BAE Systems states that the AMPV is replacing the Vietnam-era M113 family of vehicles and supports five mission variants: general purpose, mortar carrier, mission command, medical treatment, and medical evacuation. Furthermore, BAE received a USD 754 million AMPV contract, with production scheduled for the March 2026-February 2027 period. This investment highlights the growing importance of armored support fleets, which are increasingly being treated as core combat enablers rather than secondary assets.

MARKET RESTRAINT

High Cost and Complexity of Vehicle Sustainment to Hinder Industry Development

The biggest restraint on the global combat support vehicles market growth is the rising cost and complexity of vehicle sustainment. Modern combat support vehicles are increasingly equipped with digital communications, remote weapon stations, advanced sensors, power-management systems, protection kits, enhanced drivetrains, and, in some cases, hybrid-electric or autonomy-ready architectures. While these technologies upgrades improve battlefield survivability, but they also increase maintenance cost, training needs, spare-parts pressure, and depot workload. The GAO also found that Army and Marine Corps ground vehicles face sustainment challenges including lack of parts and materiel, missing or outdated technical data, shortage of trained maintainers, service-life issues, and unplanned maintenance. It also found that Army depot overhauls dropped sharply from FY2015 to FY2024, while maintenance costs rose for most selected ground vehicles.

MARKET OPPORTUNITIES

Rising Development of Autonomous and Semi-Autonomous Platforms to Present Several Growth Opportunities

The strongest opportunity in the combat support vehicles market lies in the development of autonomous and semi-autonomous platforms for applications such as last-mile resupply, casualty evacuation, convoy support, and forward logistics. Militaries are increasingly seeking to reduce soldier exposure in areas where drones, artillery, loitering munitions, and precision fires have made routine logistics significantly more dangerous. This trend is creating opportunity for OEMs that can integrate autonomy kits, teleoperation, sensor fusion, GPS-denied navigation, beyond-line-of-sight communications, and modular payload systems onto existing vehicle families. The U.S. Army’s GVSC also identified autonomous systems, power and mobility, survivability, cyber/software integration, digital engineering, and logistics-burden reduction as core ground vehicle technology priorities.

For instance, in April 2026, Army Times reported that the U.S. Army is seeking a “last mile” robot for medevac and resupply missions. The proposed system is expected to support requirements autonomous navigation, teleoperation, beyond-line-of-sight communications, off-road operation, GPS-denied movement, low signature, and casualty evacuation capabilities.

MARKET CHALLENGES

Integration of Additional Protection Kits Increase Vehicle Weight and Maintenance Requirements to Deter Industry Expansion

The combat support vehicles market faces a significant operational challenge: support vehicles must operate closer to the front line, yet these area are becoming increasingly dangerous. Resupply trucks, casualty evacuation platforms, recovery vehicles, and engineering vehicles are increasingly now routinely exposed to drones, mines, artillery, electronic warfare, and long-range precision fires.

This forces militaries to demand more protection, better mobility, lower signatures, better communications, and faster repair and recovery times. However, the integration of additional protection kits, autonomy systems, sensor, or power-management technologies often increase vehicle weight, cost, software burden, and maintenance requirements. As a result, defense procurement agencies are looking for a balance between survivability and affordability rather than procuring heavier and more heavily armored vehicles.

SEGMENTATION ANALYSIS

By Vehicle Type

Increasing Need for Real-Time Battlefield Data Movement to Lead C4ISR/Surveillance Segment Growth

By vehicle type, the global market is classified into armored recovery vehicles, armored repair & maintenance vehicles, combat engineering vehicles, bridging & gap-crossing vehicles, mine-clearing/route-clearance vehicles, armored command & control vehicles, communications/ signal support vehicles, C4ISR/surveillance support vehicles, CBRN vehicles, protected logistics vehicles, ammunition resupply vehicles, heavy equipment transporters, and others.

The C4ISR/surveillance support vehicles segment is estimated to be the fastest-growing segment, registering the highest CAGR of 11.50% during the forecast period. Growth is being driven by the increasing need for mobile command, intelligence, surveillance, reconnaissance, targeting support, and real-time battlefield data movement. These vehicles are becoming increasingly important as militaries shift from platform-heavy operations to sensor-led, networked, drone-supported, and multi-domain operations.

The armored recovery vehicles segment accounted for the largest market share of 18.35% in 2025 and is projected to grow at a CAGR of 7.65% during the forecast period.

By Platform

Unmanned/Robotic Platforms Segment to Dominate due to Increasing Logistics Operations in High-Risk Zones

By platform, the global market is classified into tracked platforms, wheeled platforms, amphibious platforms, trailer-based platforms, modular mission platforms, unmanned/robotic platforms, and air-transportable platforms.

The unmanned/robotic platforms is poised to be the fastest-growing segment, registering the highest CAGR of 13.21% during the forecast period. Growth is being supported by increasing demand for robotic resupply, casualty evacuation, mine clearance, route reconnaissance, surveillance, and logistics operations in high-risk zones. Militaries are increasingly seeking to reduce soldier exposure while improving the efficiency and resilience of support operations in battlefields characterized by persistent drone-observed and artillery-threats.

The tracked platforms segment accounted for the largest market share of 54.59% in 2025 and is projected to grow at a CAGR of 8.10% during the forecast period.

By Weight Class

Rapid Deployment and Balanced Protection Are Causing Medium-Light (10–20 Tons) Vehicles to Become the Leading Growth

By weight class, the global market is classified into ultra-light (Below 2 tons), Light (2–10 tons), medium-light (10–20 tons), medium (20–35 tons), medium-heavy (35–50 tons), heavy (50–70 tons), and very heavy (Above 70 tons).

The medium-light (10–20 tons) segment is estimated to be the grow at a fastest growing with a highest CAGR of 10.67% during the forecast period. This category benefits from a strong balance between mobility, payload, protection, deployability, and affordability. These vehicles are heavy enough to carry mission systems, armor, sensors, weapons, or medical/logistics modules, but still light enough for faster deployment and easier operational movement.

The medium (20–35 tons) segment captured the largest market share of 23.22% in 2025 and is projected to grow at a CAGR of 9.72% during the forecast period.

By Protection Level

Growing Need to Protect Combat Support Vehicles from Anti-Armor Weapons to Dominate Active/Soft-Kill Protection Segment Growth

By protection level, the global market is classified into unarmored/soft-skin, protected cab, light armored, medium armored, heavy armored, MRAP-class protection, add-on protection, active/ soft-kill protection, and environmental protection.

The active/soft-kill protection segment is poised to be the fastest-growing segment, registering a highest CAGR of 11.19% during the forecast period. Growth is being driven by the growing need to protect combat support vehicles from anti-armor weapons, drones, loitering munitions, and guided threats without simply adding more passive armor weight. This segment has strong future potential as survivability moves from steel protection to sensor-based and electronic protection.

The medium armored segment accounted for the largest market share of 19.45% in 2025 and is projected to grow at a CAGR of 10.09% during the forecast period.

By Propulsion

Increasing Need for Silent Watch Capabilities to Drive Hybrid-Electric Segment Growth

By propulsion, the global market is classified into diesel ICE, hybrid-electric, electric, auxiliary power, and emerging powertrain.

The hybrid-electric is estimated to be the fastest-growing segment, registering the highest CAGR of 12.11% during the forecast period. Growth is being driven by increasing need for silent watch capabilities, reduced acoustic signature, lower fuel consumption, exportable power, and the rising power needs of sensors, communications, electronic warfare, and command systems. The opportunity is especially strong in command vehicles, surveillance vehicles, robotic platforms, and support vehicles that need power without the need to run their engines continuously.

The diesel ICE segment accounted for the largest market share of 78.89% in 2025 and is projected to grow at a CAGR of 8.47% during the forecast period.

By Procurement Model

Supply-Chain Security and Defense Industrial Policy Are Causing Local Manufacturing to Grow Fastest

By procurement model, the global market is classified into new-build vehicles, platform conversion, retrofit/upgrade, mission module procurement, sustainment/MRO, local manufacturing, and government-to-government.

The local manufacturing segment is estimated to be the grow at a fastest growing with a highest CAGR of 11.36% during the forecast period. Growth is being driven by national security priorities, local content rules, offset requirements, wartime supply-chain concerns, and the need to sustain vehicle fleets domestically. For OEMs, this means growth will increasingly depend on partnerships, licensed production, joint ventures, technology transfer, and local assembly rather than simple export sales.

The new-build vehicles sub-segment is accounted for the largest market share of 28.33% in year 2025. In addition, the sub-segment is projected to grow at a CAGR of 10.14% during the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Logistics & Sustainment Segment to Lead due to Increasing Battlefield Exposure

By end user, the market is classified into army/land forces, marine/amphibious forces, special operations forces, combat engineers, logistics & sustainment units, and border/internal security forces.

The logistics & sustainment units is poised to be the fastest-growing segment, registering a highest CAGR of 10.45% during the forecast period. Growth is being driven by the increasing recognition that logistic vehicles, repair units, fuel supply, ammunition movement, and casualty evacuation assets are increasingly exposed to direct battlefield threats. As a result, sustainment is evolving into a frontline capability, driving demand for protected, connected, modular, and partially autonomous support vehicles.

The army/land forces segment accounted for the largest market share of 43.20% in 2025 and is projected to grow at a CAGR of 9.19% during the forecast period.

Combat Support Vehicles Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

Europe Combat Support Vehicles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the second largest share in 2025, valued at USD 7.34 billion, and is expected maintain the leading share in 2026, with USD 7.87 billion. The primary drivers are high defense spending, ongoing modernization programs, and the need to replace aging legacy vehicle fleets with technologically advanced, network-centric, and highly mobile support platforms.

U.S. Combat Support Vehicles Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 6.86 billion in 2025 and is estimated to grow at a CAGR of 7.72% during the forecast period.

Europe

Europe is projected to grow at fastest growth rate of 10.61% during the forecast period. In addition, the region held the largest global combat support vehicles market share of 33.19% in 2025, driven by heightened defense budgets and NATO modernization initiatives to counteract evolving geopolitical threats, requiring modular vehicles for reconnaissance, medical evacuation, and command-and-control. The ongoing war in Ukraine has reshaped European defense strategies, accelerating long-term fleet modernization programs across both Nordic and continental NATO nations.

Germany Combat Support Vehicles Market

The Germany’s market was valued at USD 1.62 billion in 2025 and is estimated to grow at a rate of 11.18% during the forecast period.

Eastern Europe Combat Support Vehicles Market

The market was valued at USD 2.12 billion in 2025 and is estimated to grow at a rate of 13.21% during the forecast period.

Rest of Europe Combat Support Vehicles Market

The market was valued at USD 1.91 billion in 2025 and is estimated to grow at a rate of 5.24% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 6.26 billion in 2025 and secures the position of the third-largest region in the market. This growth is primarily driven by rising regional border security disputes, massive military modernization programs to replace aging fleets, and an increasing demand for highly mobile, versatile armored logistics, and troop-transport platforms.

China Combat Support Vehicles Market

The China market was valued at USD 2.42 billion in 2025 and is estimated to grow at a rate of 6.93% during the forecast period.

India Combat Support Vehicles Market

The Indian market in 2025 was valued at USD 1.18 billion and is estimated to grow at a rate of 11.17% during the forecast period.

South Korea Combat Support Vehicles Market

The South Korea market in 2025 was valued at USD 0.68 billion and is estimated to grow at a rate of 10.84% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market was valued at USD 1.06 billion in 2025. The market is experiencing steady growth, driven by military modernization efforts and regional security threats. Armed forces are modernizing fleets with advanced C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems to boost situational awareness and network-centric warfare capabilities.

The Middle East & Africa market was valued at USD 2.58 billion in 2025. The market’s growth is driven by heightened conflicts and regional instability, particularly in the Gulf region, which have compelled nations to urgently prioritize national security and defense modernization. Militaries across the region are aggressively replacing aging/Soviet-era vehicles, upgrading to next-generation modular platforms (such as 8x8 wheeled combat and support carriers), and modernizing fleets to defend against (Improvised Explosive Device) IEDs and modern drone threats.

Gulf Countries Combat Support Vehicles Market

The market in 2025 was valued at USD 0.92 billion and is estimated to grow at a rate of 9.19% during the forecast period.

Brazil Combat Support Vehicles Market

The Brazil market in 2025 was valued at USD 0.39 billion and is estimated to grow at a rate of 6.27% during the forecast period.

COMPETITIVE ANALYSIS

Key Industry Players

Major Players Focus on Expanding Regional Production Footprints to Gain Competitive Edge

The competitive landscape of the combat support vehicles market is becoming more technology- driven and program-focused, rather than solely price- or platform-driven. Major defense vehicle manufacturers are increasingly building common chassis families that can support recovery, command, medical, engineering, logistics, and surveillance missions with fewer platform changes. This trend is visible in the industry’s shift toward modular open systems, autonomy kits, digital vehicle architecture, and exportable power solutions. Examples included the autonomous AMPV prototype using Forterra’s Auto Drive system and Oshkosh’s autonomous-ready PLS A2 heavy tactical vehicle platform.

Competition is also moving toward local manufacturing, sustainment control, and defense-industrial partnerships, as governments seek greater domestic capacity, faster repair cycles, and secure supply chains during conflict. As a result, OEMs are expanding regional production footprints, acquiring specialized vehicle-component suppliers, and positioning themselves for large long-term modernization programs rather than one-time vehicle procurement contracts.

LIST OF KEY COMBAT SUPPORT VEHICLES COMPANIES PROFILED

- BAE Systems plc (U.K.)

- General Dynamics Land Systems Inc. (U.S.)

- Rheinmetall AG (Germany)

- KNDS Deutschland GmbH & Co. KG (France)

- FNSS Savunma Sistemleri A.Ş. (Turkey)

- Patria Oyj (Finland)

- Iveco Defence Vehicles (Italy)

- Oshkosh Defense, LLC (U.S.)

- Otokar Otomotiv ve Savunma Sanayi A.Ş. (Turkey)

- Hyundai Rotem Company (South Korea)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Paramount Group (South Africa)

- Tata Advanced Systems Limited (India)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Textron Systems Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: General Dynamics Land Systems received a USD 716.25 million U.S. contract for sustainment services covering the Abrams family, Joint Assault Bridge, Assault Breacher Vehicle, and FMS requirements.

- March 2026: DRS Sustainment Systems received a USD 44.98 million contract to procure 20 Joint Assault Bridge systems and associated spares.

- January 2026: KNDS Deutschland signed a contract with the Belgian Ministry of Defence for eight LEGUAN bridge layers mounted on 10x10 wheeled chassis, including 17 bridges, logistics, and tools.

- December 2025: Patria and Germany signed two CAVS procurement contracts valued at over USD 2.2 billion, covering up to 876 Patria 6x6 armored vehicles in four variants.

- December 2025: Denmark’s DALO awarded KNDS a contract to supply three latest-generation LEGUAN bridge layers mounted on TATRA 10x10 wheeled chassis, valued at around USD 33 million.

REPORT COVERAGE

The global combat support vehicles market provide a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the global market dynamics and combat support vehicles market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key defense industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.04% from 2026 to 2034 |

| Unit | USD Billion |

|

Segmentation |

By Vehicle Type

By Platform

By Weight Class

By Protection Level

By Propulsion

By Procurement Model

By End User

By Geographic

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 25.80 billion in 2025 and is projected to reach USD 55.89 billion by 2034.

In 2025, the North America market value stood at USD 7.34 billion.

The market is expected to exhibit a CAGR of 9.04% during the forecast period.

The logistics & sustainment units segment is expected to hold the highest CAGR over the forecast period.

Growing importance of armored support fleets are the key factors driving market growth.

BAE Systems pls, General Dynamics Land Systems Corporation, Rheinmetall AG, KNDS, and Oshkosh Defense Corporation are the top key players in the market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us