Commercial Aircraft Engine Fuel Control & Ignition Systems Aftermarket Growth, Size, Share, and Analysis, By Component (Engine Fuel Control (Pumps, Heaters, Control Units, and Nozzles) and Ignition System (Igniters, Exciters, and Ignition Leads)), By Offering (MRO Services and Refurbished Parts (USM and PMA)), By Aircraft Family (Airbus A220 (ex-CSeries), Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Sukhoi Superjet 100, & Others), and Regional Forecast 2025-2045

KEY MARKET INSIGHTS

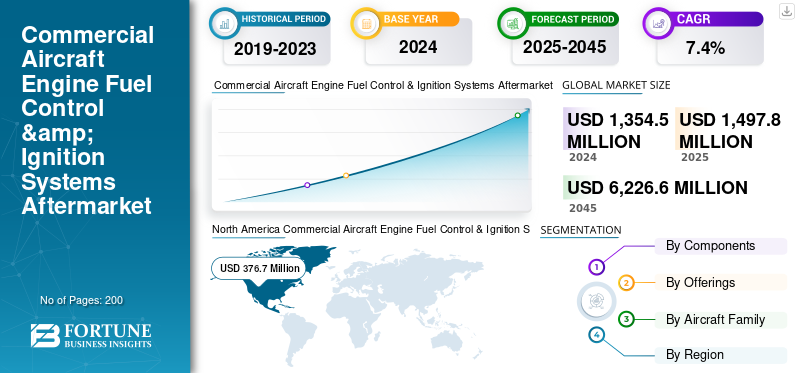

The global commercial aircraft engine fuel control & ignition systems aftermarket size was valued at USD 1,354.5 million in 2024. The market is projected to grow from USD 1,497.8 million in 2025 to USD 6,226.6 million by 2045, exhibiting a CAGR of 7.4% during the forecast period. North America dominated the global commercial aircraft engine fuel control & ignition systems aftermarket with a market share of 27.81% in 2024.

The ignition systems supply the spark or energy required to start and maintain engine combustion. Fuel control systems manage the delivery, mixture, and flow of fuel to the turbine engine, guaranteeing ideal combustion, thrust, and efficiency. The aging global aircraft fleet is driving the growth of the commercial aircraft engine fuel control & ignition systems aftermarket by raising demand for component overhauls and repairs. Operators are reconditioning, and USM-based solutions are increasing the importance of cost efficiency among airlines. Predictive maintenance and digital diagnostics developments increase productivity and reduce turnaround times.

Key players such as Pratt & Whitney, GE Aerospace, Safran, Honeywell, Rolls-Royce, Lufthansa Technik, MTU Maintenance, StandardAero, and Heico are driving the market growth by providing cutting-edge MRO services, increasing repair capacity, and delivering reasonably priced refurbished parts.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increase in Global Air Travel and Fleet Utilization is Driving the Growth of Market

The increase in global air travel and fleet utilization, which increases the frequency of maintenance cycles for fuel pumping and ignition components, is driving the market for commercial aircraft engine fuel control & ignition systems. Refurbished and PMA-certified parts are gaining popularity due to the industry's growing focus on sustainability and circular economy principles.

Furthermore, there are consistent aftermarket prospects for commercial aircraft engine fuel control & ignition systems, driven by the growth of Low-Cost Carrier (LCC) engine operations and robust demand from expanding markets in the Middle East and Asia Pacific.

- For instance, in September 2023, ST Engineering secured a multi-year Maintenance-By-the-Hour contract with Japan Airlines, offering a comprehensive suite of component services including repair, overhauls, pooling, health monitoring, and logistics for Boeing 737-800 fleets.

This deal demonstrates how the expansion of MRO services for fuel control and ignition components is expected to accelerate rapidly in the coming years.

Market Restraints

Reliance on OEMs for Propriety Repair Technologies and Certifications to Hinder the Market Growth

The market is constrained by the strong reliance on OEMs for propriety repair technologies and certifications, which reduces the options available to independent MROs and suppliers of reconditioned parts. Additionally, adoption is slowed by stringent general aviation safety and regulatory compliance standards, which frequently lengthen approval periods for PMA and reconditioned parts.

Furthermore, a lack of specialized tools and skilled people limits the ability to repair. The ongoing supply chain interruptions and rising raw material prices increase turnaround times and maintenance costs, which limit overall commercial aircraft engine fuel control & ignition systems aftermarket growth.

- For instance, in January 2025, Aengus Kelly, CEO of AerCap, warned that modern aircraft, despite their advanced technologies and improved fuel efficiency, are less durable, leading to higher maintenance demands, shortages in parts and labor, and greater engine operational disruptions.

Market Opportunities

Airlines and Leasing Firms Increasingly Use Remanufactured and USM Parts to Counter Rising OEM Spare Costs and Supply Problems, the Sector Offers Remarkable Potential.

Consistent MRO needs for fuel and ignition systems are being driven by growing fleets in the Middle East and Asia Pacific as well as rising demand from low-cost carriers. Additionally, MRO companies have the opportunity to offer quicker, data-driven overhauls due to the industry's shift toward predictive maintenance and the use of digital twins. The resulting demand for reconditioned parts is also rising due to an increased focus on sustainability and circular economy principles, creating new sources of income for independent MROs and aftermarket providers.

- For instance, in July -2024, Asia Digital Engineering (ADE) in Malaysia reported a sharp increase in demand for aircraft and engine repair services due to a global shortage of new planes. This surge has led ADE to double its revenues to USD 123 million in 2023, with service slots fully booked through 2025. ADE is also investing in predictive maintenance software and launching Aerotrade, an online parts marketplace, to serve MRO facilities and operators.

Commercial Aircraft Engine Fuel Control & Ignition Systems Aftermarket Trends

Incorporation of Predictive Maintenance and Digital Technologies is Shaping the Market Growth

A key trend shaping this market for commercial aircraft engine fuel control & ignition systems is the integration of predictive maintenance programs and digital technologies into MRO procedures for ignition and fuel control systems. AI-driven diagnostics, digital twins, and health monitoring systems are increasingly being utilized by airlines and MRO providers to predict faults, minimize downtime, and optimize overhaul schedules.

Additionally, as supply chain delays and pricing pressures make OEM spares more difficult to get, there is a growing preference for certified refurbished and USM parts. The drive for sustainability further accelerates this inclination, as operators seek more affordable and environmentally friendly options while maintaining system dependability.

- For instance, in July 2024, GE Aerospace announced a USD 1 billion investment over five years to upgrade its global MRO facilities and optimize turnaround times by 30%, by adding advanced engine test cells.

The program features modern upgrades that enhance diagnostics and predictive maintenance capabilities, which are crucial in managing complex systems, such as fuel control and ignition units.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine Conflict

Russia And Ukraine Caused Major Disruptions in the Aerospace Supply Chain

Access to crucial turbine engine control, fuel, and ignition system components is limited due to trade restrictions and sanctions, resulting in longer lead times and increased procurement costs. International operators increasingly seek refurbished parts and MRO services as affordable and accessible options. Moreover, Russian airlines, shut off from OEM spares and MRO support, are forced to rely on uncertified vendors or refurbished parts from grounded aircraft. Although it presents difficulties in guaranteeing safety and compliance, this has increased the role of aftermarket participants.

For Instance, in February 2024, Reuters reported that sanctions on Russia are significantly impacting the availability of titanium and other essential engine materials, which is having a significant impact on MRO operations and part refurbishment cycles for global aerospace providers.

SEGMENTATION ANALYSIS

By Component

Fuel Efficiency, Digital Controls, and Maintenance Demand Drive Engine Fuel Control Systems

By component, the market is segmented into the Engine Fuel Control (Pumps, Heaters, Control Units, and Nozzles) and Ignition System (Igniters, Exciters, and Ignition Leads).

Engine fuel control systems segment dominates the market and is anticipated to be the fastest growing segment during the forecast period. This growth is driven by the system’s importance for controlling fuel flow, maximizing combustion efficiency, and guaranteeing engine performance under various flight conditions. Additionally, these systems require frequent maintenance, calibration, and part replacement due to their complexity, which features mechanical, electrical, and increasingly digital FADEC-based controls. The need for advanced, reconditioned, and improved fuel pumping units has increased due to global fuel prices and airlines’ emphasis on fuel economy and pollution reduction. As a result, the segment is expected to show remarkable growth during the forecast period. Furthermore, next-generation aircraft programs and retrofits are accelerating the adoption of digital and AI-enabled fuel control units.

- For Instance, in October 2023, Honeywell and Triumph Group signed a long-term contract for the production and maintenance of fuel pumps, electronic control units, and hydro mechanical fuel controls for various Honeywell engine platforms, including the HTF7000 business jet engines and T55 helicopter engines.

This agreement shows the importance and demand for fuel control parts in both commercial business and military applications.

By Offering

MRO Service Segment Dominates the Market with High Frequency of Inspection, Overhaul, and Maintenance Cycles

By offering, the market is classified into MRO services and refurbished parts (USM and PMA).

MRO service segment dominates the market due to the high-maintenance, safety-critical components that require strict adherence to regulatory standards, as well as routine overhauls and inspections. Moreover, there is a constant need for certified servicing compared to other subsystems, as fuel control units and ignition systems are directly related to engine performance, fuel efficiency, and pollution control.

Additionally, the number of maintenance cycles is increasing due to the global aging of the fleet. The trend toward predictive maintenance, digital diagnostics, and service contracts further supports this segment’s growth.

- For example, in February 2025, the Royal Netherlands Air Force (RNLAF) awarded AAR a three-year MRO contract to service and refurbish F-16 jet fuel starters at its facility in Amsterdam. Over the past thirty years, AAR has maintained more than 3,500 gasoline starters for RNLAF, demonstrating its expertise in vital fuel-related parts.

By Aircraft Family

Boeing 737 Family Dominates the Market Due to Large Fleet Size, High Utilization, and Regulatory-Driven System Upgrades

Further, the market is segmented by Airbus A220 (ex-CSeries), Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Boeing 737 Family segment dominates the market. As Boeing 737 Family is the best-selling commercial airliner, accounting for almost 20% of the world's in-service commercial fleet. Its widespread use by full-service and low-cost airlines guarantees a consistent flow of maintenance cycles and aftermarket demand, mainly for high-usage parts, such as fuel metering units, pumps, and ignition systems, which results in high temperatures.

Moreover, Airlines are spending a significant amount of money on upgrades, retrofits, and refurbishments of their current systems to prolong service life and meet more stringent emission and fuel efficiency regulations as a result of ongoing fleet modernization, particularly the switch from 737 NG to 737 MAX.

- For example, in September 2023, ST Engineering was awarded a five-year maintenance, repair, and overhaul (MRO) contract to supply LEAP-1B services for the Boeing 737 MAX fleet operated by Lion Air Group.

Commercial Aircraft Engine Fuel Control & Ignition Systems Aftermarket Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Commercial Aircraft Engine Fuel Control & Ignition Systems Aftermarket Size, 2024 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America holds the largest commercial aircraft engine fuel control & ignition systems aftermarket share, due to its large commercial fleet, robust MRO infrastructure, and presence of OEMs such as GE Aviation, Honeywell, and Collins Aerospace. The U.S. market for commercial aircraft engine fuel control & ignition systems is the keep-it-flying ecosystem that supports a large, high-utilization fleet. This is common for narrowbody aircraft, which accumulate many cycles each day. The market includes everything from line troubleshooting and AOG swaps to shop-level repair and overhaul of fuel metering and control hardware, valves, actuators, and ignition components. It also covers exciters, leads, and igniters, as well as test and bench calibration, and necessary paperwork and traceability.

Asia Pacific, Europe, Middle East, and Latin America

The Asia Pacific region is anticipated to be fastest growing segment, driven by the quick development of fleets in China and India as well as rising OEM-regional MRO provider alliances. The dominance of international airlines, such as Emirates and Qatar Airways benefits the Middle East and creates a consistent demand for high-cycle MRO services. Moreover, despite Latin America being smaller markets, the region is witnessing an increase in demand for reconditioned parts as their airlines prioritize cost reduction and aircraft longevity.

- For example, in May 2025, IndiGo and Bengaluru International Airport signed a USD 133 million deal to build a new MRO facility at Kempegowda International Airport. The 31-acre facility will have four hangars that can service narrow- and wide-body aircraft, including parts for the ignition and fuel control systems that are essential to planned maintenance.

Europe holds the second position in market for commercial aircraft engine fuel control & ignition systems, with the help of Airbus fleets, maintenance regulations, and powerful companies, such as Pratt Whitney, Safran and Lufthansa Technik.

Competitive Landscape

Key Industry Players

Established OEMs and MRO Leaders Lead the Market and Digital Upgrades and Refurbished Parts Open New Opportunities

OEMs, component experts, and integrated MRO providers are the main players in the commercial aircraft engine fuel control & ignition systems aftermarket. In addition to providing aftermarket services, OEM companies, such as Pratt Whitney, GE Aerospace, Rolls-Royce, Woodward, and Unison Industries use proprietary technologies in their fuel metering units, pumps, and ignition components. Operators can choose from more affordable options due to PMA-approved and refurbished parts from component specialists, such as Honeywell, TransDigm, Champion Aerospace, and Electroair.

Engine subsystem full-service MRO suppliers, such as Lufthansa Technik, MTU Maintenance, ST Engineering, Delta TechOps, and VSE Corporation, ensure the reliability and availability of the component, offering repair, overhaul, and logistics solutions across fleets.

LIST OF KEY COMMERCIAL AIRCRAFT ENGINE FUEL CONTROL & IGNITION SYSTEMS COMPANIES PROFILED

|

SR. No |

|

MRO Service & Refurbished Parts Company |

MRO Service Providers |

Refurbished Parts Suppliers |

|

|

1 |

|

Lufthansa Technik |

Champion Aerospace |

|

|

|

2 |

|

TransDigm Group |

MTU Maintenance |

FADEC International LLC. |

|

|

3 |

|

ST Engineering |

Kelly Aerospace |

|

|

|

4 |

|

Unison Industries (GE) |

Delta TechOps |

SureFly Partners |

|

|

5 |

|

Electroair |

VSE Corporation |

Continental Aerospace Technologies |

|

KEY INDUSTRY DEVELOPMENTS

For Instance, in August 2025, ST Engineering and SF Airlines inaugurated a new airframe MRO facility in Ezhou, Hubei, China, developed through their joint venture, aiming to provide high-quality MRO services to SF Airlines and global third-party customers.

For Instance, in March 2025, GE Aerospace committed to investing nearly USD 1 billion in its U.S. manufacturing facilities and supply chain, focusing on innovative parts and materials to strengthen engine safety, quality, and delivery.

For Instance, in August 2024, Woodward entered into a five-year Maintenance, Repair, and Overhaul (MRO) agreement with Lufthansa Technik. Under this agreement, work on aircraft engine components will be provided at Woodward’s Rockford, Illinois, and Prestwick, U.K., locations.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphases key aspects such as key players, offerings, objects, and end-user of aircraft engine fuel control and ignition systems. Moreover, the report deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 7.4% from 2025 to 2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component · Engine Fuel Control o Pumps o Heaters o Control Units o Nozzles · Ignition System o Igniters o Exciters o Ignition Leads |

|

By Offerings · MRO Services · Refurbished Parts o USM o PMA |

|

|

By Aircraft Family · Airbus A220 · Airbus A320 Family (CEO/NEO) · Airbus A330 (CEO/NEO) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

|

By Region · North America (By Component, By Offerings, By Aircraft Family, and by Country) o U.S. (By Component) o Canada (By Component) · Europe (By Component, By Offerings, By Aircraft Family, and by Country) o U.K. (By Component) o Germany (By Component) o France (By Component) o Russia (By Component) o Rest of Europe (By Component) · Asia Pacific (By Component, By Offerings, By Aircraft Family, and By Country) o China (By Component) o India (By Component) o Japan (By Component) o South Korea (By Component) o Rest of Asia Pacific (By Component) · Middle East & Africa (By Component, By Offerings, By Aircraft Family, and By Country) o Saudi Arabia (By Component) o Israel (By Component) o Turkey (By Component) o Rest of the Middle East (By Component) · Latin America (By Component, By Offerings, By Aircraft Family, and By Country) o Brazil (By Component) o Rest of Latin America (By Component) |

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 1,354.5 million in 2024 and is anticipated to be USD 6,226.6 million by 2045.

The market is likely grow at a CAGR of 7.4% over the forecast period (2025-2045).

The top ten players in the industry are Honeywell Aerospace, Lufthansa Technik, TransDigm Group, MTU Maintenance, Woodward, Inc., ST Engineering, Unison Industries (GE), Delta TechOps, Electroair, VSE Corporation based on parameters such as Services Portfolio, Regional Presence, and Industry Experience.

North America dominated the market in 2024.

Increase in global air travel and fleet utilization are the driving factors of the market.

Reliance on OEMs for propriety repair technologies and certifications are the restraining factors of the market.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us