Commercial Aircraft Fuel Systems Aftermarket Size, Share & Industry Analysis, By component (Fuel Feed and Transfer Subsystem, Fuel Measurement and Indication, Refueling and Defueling System, Fuel Tank Inerting, Venting, Drainage and Water Management, By Offerings (MRO Services & Refurbished Parts (PMA & USM)), By Aircraft Family (Airbus A220 , Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, and others, and Regional Forecast, 2025-2045

KEY MARKET INSIGHTS

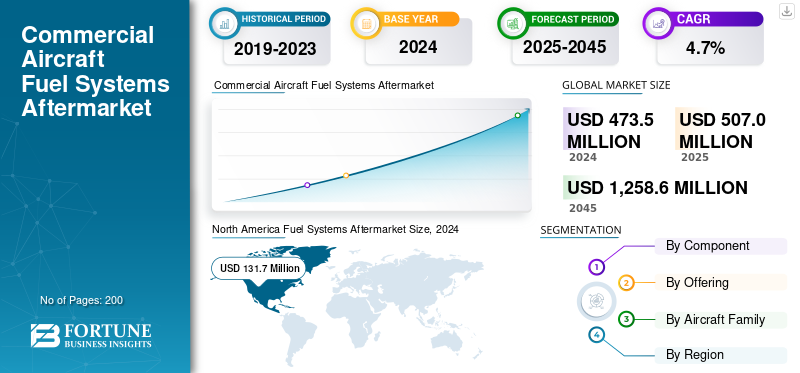

The commercial aircraft fuel systems aftermarket size was valued at USD 473.5 million in 2024. It is projected to grow from USD 507.0 million in 2025 to USD 1,258.6 million by 2045, exhibiting a CAGR of 4.7% during the forecast period. North America dominated the global Commercial Aircraft Fuel Systems Aftermarket with a market share of 27.81% in 2024.

The aircraft fuel systems aftermarket spans inspection, repair, overhaul and certified reuse of pumps, tanks, valves, sensors and transfer units. Airlines depend on MRO cycles to meet safety requirements for leak-proofing, contamination checks and pump reliability, while refurbished parts provide cost relief where OEM-approved certification exists. For operators, fuel-system integrity directly affects dispatch reliability and safety. With global fleets expanding flight hours maintenance intervals are accelerating. For instance, in 2024 Eaton and VSE Aviation expanding authorized service coverage in the Americas, while Lufthansa Technik reported record component revenues, highlighting the ongoing demand for fuel-system servicing with higher utilization rates.

Furthermore, the aftermarket encompasses several major players with Collins Aerospace, Honeywell Aerospace, Thales Group, and Safran Electronics & Defense at the forefront. Broad portfolio with innovative product launch and strong geographic presence expansion have supported the dominance of these companies in the global aftermarket.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Fleet Utilization & SAF Readiness Leads to Higher Product Demand

Aging fleets, rising utilization and regulatory inspection intervals are key drivers. Fuel tanks and pumps, scavenge systems and valves has to face high wear, requiring scheduled overhauls. Airlines preparing for Sustainable Aviation Fuel (SAF) blends are also replacing seals, filters and testing pumps for compatibility. For example, in 2024, Delta began SAF trials at scale, prompting engineering adjustments across subsystems including fuel delivery. As operators adopt SAF at higher blends, maintenance demand for compatible parts will increase. Additionally, OEM partnerships, such as Eaton’s authorized service agreements with Air Support in Europe, shows the drive to localize repair, improving turnaround and lowering downtime. These developments demonstrate how fuel-system MRO is both safety-critical and strategically aligned with sustainability initiatives.

MARKET RESTRAINTS

Certification and Supply Chain Hurdles is a Major Restraint

Despite the rapid growth, various significant restraints challenges the aftermarket. Certification hurdles restricts the use of refurbished components unless backed by OEM documentation and EASA/FAA approvals, limiting cost flexibility. Independent repair shops often face difficulty accessing proprietary manuals or test equipment, which keeps OEMs in a gatekeeper role. Moreover, precision machining and specialty materials for pumps and valves have been vulnerable to supply chain delays since 2021, creating longer lead times. For instance, Lufthansa Technik has warned of longer turnaround times for complex modules, partly due to part shortages. These issues increase costs for airlines, as they may resort to purchasing new OEM spares at premium pricing when refurbished inventory is limited.

MARKET OPPORTUNITIES

Authorized Service Growth & SAF Retrofits Offers Lucrative Opportunity

Beneficial opportunities are arising from expanded authorized repair networks and SAF transition. Eaton in 2024 appointed VSE Aviation in the Americas and Air Support in EMEA as authorized fuel and hydraulics repair providers significantly broadening certified capacity. This allows operators to service components locally rather than shipping units overseas, cutting downtime. Meanwhile, the SAF transition requires ongoing retrofits, as seals, filters and pump components need to be validated for biofuel blends, creating fresh aftermarket opportunities. Airlines piloting SAF flights (United, Delta, KLM) are testing long range durability of fuel systems, driving demand for inspection and modification. Independent MROs that partner with OEMs for authorized capabilities and invest in SAF-compatible test benches are best positioned to capture these contracts.

MARKET CHALLENGES

Skilled Labor & AOG Costs Spikes Deters Aftermarket Expansion

The biggest challenge for the aftermarket lies in skilled labor shortages and the cost of AOG events tied to fuel-system failures. Even with record results, Lufthansa Technik noted pressure to scale workshops and recruit engineers in 2024 as demand surged across components. Fuel-system repairs require highly trained specialists and safety-critical testing, which cannot be easily outsourced. AOG incidents caused by leaking pumps or clogged valves can cost airlines tens of thousands per hour in delays. Additionally, shifting toward SAF and hydrogen adds a layer of training complexity for MRO staff, stretching the limited capacity. These issues emphasize the urgency for both OEMs and independent MROs to invest in workforce development and equipment upgrades to prevent bottlenecks.

COMMERCIAL AIRCRAFT FUEL SYSTEMS AFTERMARKET TRENDS

Hydrogen & Predictive Diagnostics Are Upcoming Technological Trend Reshaping Aftermarket Growth

Emerging technologies are expected to reshape the aftermarket in future. Hydrogen propulsion programs in Europe (HyFIVE consortium, Parker Aerospace involvement) are developing cryogenic fuel pumps, valves and sensors, creating the need for new servicing expertise. For current fleets, predictive diagnostics is becoming more common as onboard sensors and digital twin models feed data into predictive maintenance systems to forecast pump or valve wear before failure. In 2024, several airlines began deploying expanded predictive analytics platforms across A320 and B737 fleets, enabling component swaps before AOG events. MRO shops investing in specialized test rigs, digital calibration and data integration will capture early mover advantage as both hydrogen and digital maintenance ecosystems mature.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

High Demand for Safety Roles Contributed to Interphone and Passenger Address (PA) Systems Segment Growth

On the basis of component, the aftermarket is classified into Fuel Feed and Transfer Subsystem (Boost Pump, Fuel Transfer Pump, Crossfeed Valve, Fuel Shutoff Valve, Low Pressure Valve, Center Tank Fuel Pump), Fuel Measurement and Indication (Fuel Quantity Processor and Fuel Quantity Indicator), Refueling and Defueling System (Refuel/Defuel Panel and Overflow Prevention System), Fuel Tank Inerting and Venting (Nitrogen Generation System (NGS), Fuel Tank Inerting Controller, Vent Pressure Regulator, Vent Surge Tank, and Integrated Vent Controller), and Drainage and Water Management (Main Tank Drain Valve, Water Separator Drain, Scavenge Drain System, and Composite Drain Manifold).

Fuel Tank Inerting and Venting leads the aftermarket, accounting for a dominating commercial aircraft fuel systems aftermarket share and amounting to USD 182.1 Million in 2024. This dominance is attributed to stringent safety regulations that mandate the installation and continuous maintenance of these systems, coupled with the need to retrofit existing aircraft fleets.

- In 2024, Astronics launched an upgraded digital PA/interphone solution optimized for narrowbody aircraft, targeting retrofit programs among low-cost carriers. As cabin refurbishment remains a key investment area; encouraged by passenger experience upgrades, MRO demand for interphone and PA components is expected to grow steadily.

To know how our report can help streamline your business, Speak to Analyst

By Offerings

Increasing Focus on Preventive Maintenance and Inspection Fuels MRO Segment Growth

In terms of offerings, the aftermarket is categorized into MRO services and refurbished parts.

The MRO services segment captured the largest share of the aftermarket in 2024. In 2025, the segment is anticipated to dominate the aftermarket. MRO services dominate over refurbished parts due to regulatory requirements for periodic inspection and testing of communication systems to ensure compliance with FAA/EASA safety directives. Unlike other components, PA and radio systems must be fully operational for an aircraft to be dispatched, resulting in frequent removal and bench-testing. Airlines prioritize reliability, making certified MRO services the preferred choice over refurbished inventory.

In 2023, Lufthansa Technik announced a 15% year-on-year rise in component services revenue, largely driven by avionics and communication modules. Similarly, Collins Aerospace expanded its communication systems repair facility in North America to support higher fleet demand. As fleets age and utilization rises, airlines are expected to allocate greater budgets to specialized MRO contracts covering avionics and comms.

By Aircraft Family

Widespread Usage of Standard Fuel Systems MRO & Refurbished Parts Supplemented Segment Growth

Based on aircraft family, the aftermarket is segmented into Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Airbus A320 Family (CEO/NEO) dominates the aftermarket due to its massive global fleet size, unmatched popularity across all airline types (LCCs to full-service), and the sheer volume of aircraft needing ongoing maintenance, upgrades (such as sharklets), parts, and eventual engine servicing for both reliable CEO models and fuel-efficient NEOs. This creates a huge, consistent demand for specialized fuel system expertise, parts, and support. CEO (Current Engine Option) reliable, lower upfront cost, perfect for LCCs or short routes, generating consistent demand for existing parts. NEO (New Engine Option) offers significant fuel savings (up to 20%), lower emissions, longer range, and newer tech (sharklets, new engines), attracting new orders and driving aftermarket for advanced systems.

- In June 2024, Ryanair placed additional orders for 150 Boeing 737 MAX 10 aircraft, directly boosting the installed base requiring communication system servicing. With LCCs worldwide prioritizing narrowbody expansion, demand for MRO and refurbished communications parts in this segment will continue to dominate.

The COMAC C919 segment is anticipated to be the fastest-growing segment with registering highest CAGR of 18.9% during the forecast period. This is due to its rapid entry into China's massive domestic market (replacing older planes) and its competitive pricing challenging Airbus/Boeing. The COMAC's aggressive production ramp-up targeting significant fleet growth also drives demand for new parts and maintenance services, especially as international certification slowly rolls out, creating a large initial base of aircraft needing support.

Commercial Aircraft Fuel Systems Aftermarket Regional Outlook

By geography, the aftermarket is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Fuel Systems Aftermarket Size, 2024 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America held the dominant share in 2023 valuing at USD 127.5 million and also took the leading share in 2024 with USD 131.7 Million. The North American commercial aircraft fuel systems aftermarket is a growing sector driven by fleet modernization, increasing air travel, and the push for fuel efficiency with Sustainable Aviation Fuels (SAF). Key players such as Honeywell, Eaton, and AMETEK provide advanced fuel sensors, management systems, and MRO (Maintenance, Repair, Overhaul) services, while companies including VSE Corp handle distribution and specialized repairs, focusing on reliability, health monitoring, and compliance with strict FAA regulations for next-gen fuel solutions.

Europe and Asia Pacific

Europe and Asia Pacific collectively represent fastest growing regions. Europe and Asia Pacific are witnessing robust growth, driven by fleet modernization and rising passenger traffic. European carriers focus on cabin refurbishments and EASA safety compliance, while Asia Pacific benefits from rapid fleet expansion in China, India, and Southeast Asia. Airbus’ strong presence in Europe also supports demand for certified communication MRO.

Latin America & Africa and Middle East

Over the forecast period, Latin America and Middle East & Africa regions would witness a moderate growth in this aftermarket space. Latin America & Africa aftermarket in 2025 is set to record USD 37.3 Million as its valuation in 2024. The Latin America, Africa, and Middle East (LAM & AME) commercial aircraft fuel systems aftermarket is booming, driven by aging fleets needing MRO, growing air traffic, and new sustainability mandates pushing upgrades for SAF (Sustainable Aviation Fuels). Key segments include maintenance/repair/overhaul (MRO) of pumps, valves, tanks, and monitoring systems, with strong demand in the MEA hub nations (UAE, Qatar) and Brazil. Focus is on efficiency, digital solutions, and retrofitting older planes for new fuel types, creating significant opportunities in component replacement, advanced coatings, and fuel management upgrades.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings Coupled with Strong Distribution Network of Key Companies Supported their Leading Position

The competitive landscape for commercial aircraft fuel systems aftermarket is a dynamic mix of large OEMs (Honeywell, Safran, Parker, Eaton, Triumph, Collins Aerospace) and specialized players (Woodward, Meggitt, Cobham, GKN), driven by aging fleets needing upgrades, stricter emission rules (SAF, inerting systems), and digital integration for efficiency, with a strong aftermarket focus on maintenance, retrofits, and component MRO (Maintenance, Repair, Overhaul) for cost-effective fleet life extension and performance improvement.

LIST OF KEY COMMERICAL AIRCRAFT FUEL SYSTEMS COMPANIES PROFILED

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Thales Group (France)

- Safran Electronics & Defense (France)

- Liebherr-Aerospace (Germany/France)

- Moog Inc. (U.S.)

- Parker Aerospace (U.S.)

- Spirit AeroSystems (U.S.)

- ST Engineering Aerospace (Singapore)

- Lufthansa Technik (Germany)

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.7% from 2025-2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component, Offering, Aircraft Family and Region |

|

By Component |

· Fuel Feed and Transfer Subsystem o Boost Pump o Fuel Transfer Pump o Crossfeed Valve o Fuel Shutoff Valve o Low Pressure Valve o Center Tank Fuel Pump · Fuel Measurement and Indication o Fuel Quantity Processor o Fuel Quantity Indicator · Refueling and Defueling System o Refuel/Defuel Panel o Overflow Prevention System · Fuel Tank Inerting and Venting o Nitrogen Generation System (NGS) o Fuel Tank Inerting Controller o Vent Pressure Regulator o Vent Surge Tank o Integrated Vent Controller · Drainage and Water Management o Main Tank Drain Valve o Water Separator Drain o Scavenge Drain System o Composite Drain Manifold |

|

By Offering |

· MRO Services · Refurbished Parts o PMA o USM |

|

By Aircraft Family |

· Airbus A220 · Airbus A320 Family (ceo/neo) · Airbus A330 (ceo/neo) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

By Geography |

· North America (By Component, Offering, Aircraft Family, and Country) o U.S. o Canada · Europe (By Component, Offering, Aircraft Family, and Country ) o Germany o U.K. o Germany o France o Russia o Rest of Europe · Asia Pacific (By Component, Offering, Aircraft Family, and Country) o China o India o Japan o Australia o Rest of Asia Pacific · Latin America & Africa (By Component, Offering, Aircraft Family, and Country) o Brazil o Mexico o Rest of Latin America · Middle East (By Component, Offering, Aircraft Family, and Country) o UAE o Saudi Arabia o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global aftermarket value stood at USD 473.5 million in 2024 and is projected to reach USD 1,258.6 million by 2045.

In 2024, the aftermarket value stood at USD 131.7 million.

The aftermarket is expected to exhibit a CAGR of 4.7% during the forecast period of 2025-2045.

The MRO services segment led the aftermarket by offering.

Fleet utilization & SAF readiness Leading to Higher MRO Demand

Collins Aerospace (U.S.), Honeywell Aerospace (U.S.), and Thales Group (France) are some of the prominent players in the aftermarket.

North America dominated the aftermarket in 2024.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us