Commercial Aircraft Gas Turbine Engine Market Size, Share & Industry Analysis By Engine Type (High-bypass Non Geared Turbofan, High-bypass Geared Turbofan, & Others), By Thrust Class (Up to 100 kN, 100–200 kN, 200–300 kN, and Above 300 kN), By Aircraft Type (Narrow & Wide-body, Regional Jets, & Others), By Lifecycle Stage (OEM Line-Fit Engines, Spare Engines & Modules, MRO, and Engine Upgrades & Modifications), By Component (Fan & Fan Case, Low & High Pressure Compressors, Combustor, High & Low Pressure Turbines, & Others), By Fuel Type, By Technology Type, and Regional Forecast, 2026-2034

Commercial Aircraft Gas Turbine Engine Market Size and Future Outlook

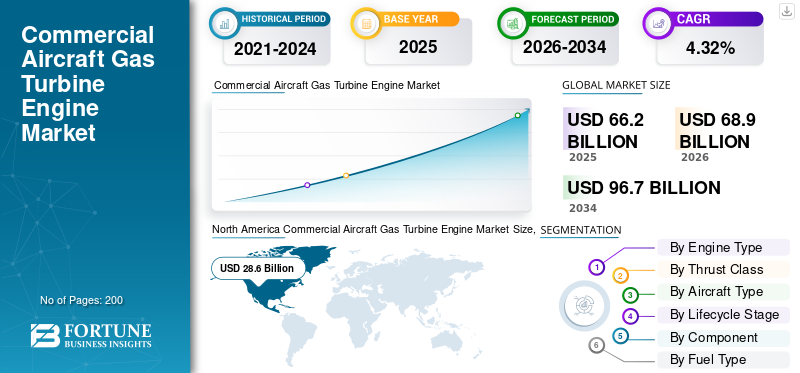

The global commercial aircraft gas turbine engine market size was valued at USD 66.2 billion in 2025. The market is projected to grow from USD 68.9 billion in 2026 to USD 96.7 billion by 2034, exhibiting a CAGR of 4.32% during the forecast period. North America dominated the global commercial aircraft gas turbine engine market with a market share of 43.2% in 2025.

Commercial aircraft gas turbine engine are internal combustion engines that compress air, mix it with fuel for combustion, and expand hot gases through turbines to generate thrust for propulsion. Key components include the inlet, compressor (axial or centrifugal stages), combustor chamber, turbine sections (high- and low-pressure), fan (in turbofans), and exhaust nozzle. Furthermore, primarily high bypass turbofans propel airliners at subsonic speeds, offering superior fuel efficiency and reduced noise over turbojets or low bypass engine types.

Major players in the market include GE Aerospace, Pratt & Whitney, Rolls-Royce, and other notable companies. These players are focused on developing new and advanced engines for wide body and narrow-body aircraft to gain a competitive edge in the market for commercial aircraft gas turbine engine.

Download Free sample to learn more about this report.

Commercial Aircraft Gas Turbine Engine Market Takeaways

- 2025 Market Size: USD 66.2 Billion

- 2026 Market Size: USD 68.9 Billion

- 2034 Forecast Market Size: USD 96.7 Billion

- CAGR: 4.32% from 2026–2034

- North America dominated the market with a 43.2% share in 2025.

- The high-bypass geared turbofan segment is projected to grow at the highest CAGR of 4.91% during the forecast period.

- The hybrid-electric assisted segment is expected to register the fastest growth, with a CAGR of 5.06% through 2034.

North America

North America led the market with USD 28.6 billion in 2025, supported by strong aircraft production and engine manufacturing capabilities.

Europe

Europe is expected to reach USD 15.4 billion in 2026, supported by advanced aerospace infrastructure and ongoing engine innovation programs.

Asia Pacific

Asia Pacific is projected to record the highest regional CAGR of 5.01% during the forecast period, driven by expanding airline fleets and rising air passenger traffic.

U.S.

The market is projected to reach USD 18.6 billion in 2026, driven by robust commercial aviation demand and OEM investments.

Japan

The market is anticipated to reach USD 3.6 billion in 2026, supported by aerospace modernization and increasing aircraft procurement activities.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rise in Fleet Modernization Programs to Drive Market Growth

Airlines are accelerating fleet modernization by replacing older aircraft with next generation models equipped with advanced turbofans such as the LEAP and GTF engines. This is driven by the surging passenger demand. This shift reduces the maintenance on aging fleets while adopting fuel efficient, lower emission engines to comply with regulations and cut costs. Furthermore, OEMs are ramping up the production of efficient wide body and narrow body jets, which in turn prompts increased engine demand. Additionally, modernization also enhances range, capacity, and sustainability, fueling market expansion.

MARKET RESTRAINTS

High Maintenance and Repair Costs Due to Complex Engine Designs to Hamper Market Growth

Advanced gas turbine engines have complex designs with components such as high bypass fans, multi stage compressors, and advanced materials, which drive maintenance expenses through frequent workshop visits and specialized repairs. Furthermore, frequent overhauls arise from early maintenance issues in innovative designs, demanding specialized labor and proprietary spares amid supply shortages. Additionally, airlines extend the life of older fleets, which amplifies unplanned repairs on aging engines while delaying profitability from new, efficient models. These factors restrain market growth by inflating direct operating costs and hindering fleet renewal.

MARKET OPPORTUNITIES

Hybrid-Electric Propulsion Systems Emerge as Opportunities for Market Players

Hybrid electric systems integrate gas turbine engines with electric motors and batteries, optimizing energy use on short-haul routes by reducing fuel consumption. For example,GE Aerospace advances hybrid electric technologies through a demonstrator engine, targeting commercial viability while meeting net-zero goals by 2050. Furthermore, electric boost during takeoff and climb reduces the reliance on fuel combustion, while turbines handle cruise for extended range flexibility. Benefits include lower emissions, quieter operations near airports, and simplified maintenance from fewer moving parts in electric components. This technology supports the development of sustainable aviation fuels and bridges the path to full electrification, creating retrofit markets and new regional aircraft segments.

COMMERCIAL AIRCRAFT GAS TURBINE ENGINE MARKET TRENDS

Use of Digital Twins and AI to Optimize Engine Performance is the Latest Trend in the Market

Digital twins create real time virtual replicas of gas turbine engines, integrating sensor data and AI analytics to continuously monitor performance, predict failures, and optimize operations. For instance, Rolls-Royce utilizes engine digital twins to identify performance irregularities through integrated sensors, enabling proactive maintenance scheduling that reduces unplanned downtime and enhances overall reliability. Furthermore, AI-driven simulations identify drag reduction opportunities and flight optimizations, accelerating design validation without physical prototypes. This trend transforms MRO, boosting fleet availability and sustainability.

MARKET CHALLENGES

Strict Emission Regulations and Certification Requirements Pose Adoption and Development Challenge in the Market

Stringent FAA and ICAO standards mandate fuel-efficient technologies in new jets post-2028, aligning with net-zero goals by 2050 and complicating engine certification for aircraft manufacturers. EASA's ReFuelEU requires 2% SAF blending from 2025, escalating to 70% by 2050, alongside EU ETS expansions for non-CO2 monitoring, delaying novel designs amid rigorous testing. CORSIA's mandatory phase from 2027 demands verifiable reductions, while complex approvals for advanced turbofans such as open-rotor concepts hinder rapid innovation. These barriers elevate R&D costs and timelines, restraining the market entry of sustainable propulsion.

U.S. Tariff War Impact:

The U.S. tariffs on imported engine components and raw materials inflate production costs for manufacturers dependent on international supply chains, disrupting complex global assembly processes. GE Aerospace and Pratt & Whitney face higher input prices due to tariffed components sourced from China and Japan, which is delaying the production ramps of LEAP and GTF amid Boeing’s delivery backlogs. Furthermore, MRO facilities face elevated spare parts expenses, as well as shifting maintenance demand to tariff-free regions in Europe and Asia.

Download Free sample to learn more about this report.

Segmentation Analysis

By Engine Type

Rising Narrow-Body Adoption to Drive the High-Bypass Non-Geared Turbofan Segment Growth

On the basis of engine type, the market is segmented into high-bypass non geared turbofan, high-bypass geared turbofan, and turboprop engines.

The high-bypass non geared turbofan segment accounted for the dominant commercial aircraft gas turbine engine market share in 2025. The growth of this segment is driven by the extensive adoption of narrow-body, single aisle aircraft by airlines that serve short haul routes. Furthermore, the increasing demand for fuel efficiency in low cost carrier operations also drives the dominance of the segment.

The high-bypass geared turbofan segment is expected to grow at the highest CAGR of 4.91% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Thrust Class

Rise in Narrow-Body Operations on High-Frequency Routes to Drive 100–200 kN Segment

In terms of thrust class, the market for commercial aircraft gas turbine engine is segmente Rise in Narrow-Body Operations on High-Frequency Routes to Drive 100–200 kN Segment

In terms of thrust class, the market for d into up to 100 kN, 100–200 kN, 200–300 kN, and above 300 kN.

The 100–200 kN segment captured the largest share of the market in 2025. The growth of this segment is fueled by expanding narrow-body operations on high-frequency domestic and regional routes where thrust ratings equal to efficient short to medium haul connectivity.

The 200–300 kN segment is expected to grow at a CAGR of 4.18% over the forecast period.

By Aircraft Type

Rise in High-Frequency Routes to Boost Narrow Body Segment Growth

Based on aircraft type, the market is segmented into narrow-body, wide-body, regional jets, regional turboprops, and dedicated freighters & P2F conversions.

The narrow-body segment held the dominating position in 2025. The growth of this segment continues to expand, driven by high frequency domestic and regional routes, which in turn drive the largest installed and in service engine base globally.

The wide-body segment is set to flourish and is growing at the highest CAGR of 4.58% during the forecast period.

By Lifecycle Stage

Extended Engine Lifecycles to Boost the MRO (Overhauls, LLP Replacement) Segment Growth

Based on lifecycle stage, the market for commercial aircraft gas turbine engine is segmented intoOEM line-fit engines, spare engines & modules, MRO (overhauls, LLP replacement), and engine upgrades & modifications.

The MRO (overhauls, LLP replacement) segment held the dominating position in 2025. The growth in this segment is driven by the rigorous maintenance cycles on diverse fleets including regional and wide body operators maintaining airworthiness through modular overhauls.

The OEM line-fit engines segment will witness the highest growth rate of 4.55% over the forecast period.

By Component

Continuous Improvement Cycles Drives the High Pressure (HP) & Low Pressure (LP) Turbines Segment Growth

Based on component, the market is segmented into Fan & fan case, Low Pressure (LP) & High Pressure (HP) compressors, combustor, High Pressure (HP) & Low Pressure (LP) turbines, exhaust & nozzle, accessory gearbox & accessories, and nacelle & thrust reverser.

The High Pressure (HP) & Low Pressure (LP) turbines segment held the dominating position in 2025. The growth of this segment is driven by continuous improvements in High-Pressure (HP) and Low-Pressure (LP) turbine technologies that enhance engine efficiency and durability.

The accessory gearbox & accessories segment will witness a growth rate of 4.55% growth over the forecast period.

By Fuel Type

Established Infrastructure and Certifications to Support Jet A/A-1 Conventional Segment Growth

Based on fuel type, the market is segmented into Jet A/A-1 conventional, SAF-ready / high blend capable, hybrid-electric assisted, and hydrogen-ready concepts.

The jet A/A-1 conventional segment held the dominating position in 2025. The growth of this segment is driven by the established airport fueling infrastructure, global availability, and mature supply chains. Moreover, existing engine certifications, operational familiarity, and pricing predictability further support its dominance.

The hybrid-electric assisted segment will witness the highest growth rate of 5.06% over the forecast period.

By Technology Type

High Replacement Costs, Low Profit Margins, and Strict Regulations Sustain Legacy In-Service Engines Segment Dominance

Based on technology type, the market is segmented into legacy in-service engines, new generation fuel efficient engines, and next-gen demonstrator engines.

The legacy in-service engines segment held the dominating position in 2025. The growth of this segment is driven by high replacement costs, low airline profit margins, and stringent safety rules that increases obstacles to entry for newer, unproven technology.

The next-gen demonstrator engines segment is anticipated to witness the highest growth rate of 5.50% over the forecast period.

Commercial Aircraft Gas Turbine Engine Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America held the dominant share in 2024, valued at USD 27.6 billion, and also maintained the leading share in 2025, with USD 28.6 billion. The market for commercial aircraft gas turbine engines in North America is expanding due to several factors, including the presence of large manufacturers such as GE Aerospace and Honeywell. Furthermore, in the U.S., growing international air travel, demand for new aircraft, and large R&D expenditures in cutting-edge, fuel-efficient engines primarily drive the regional share. In 2026, the U.S. market is estimated to reach USD 18.6 billion.

North America Commercial Aircraft Gas Turbine Engine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

the Asia Pacific

Regions such as Europe and the Asia Pacific are expected to experience notable commercial aircraft gas turbine engine market growth in the coming years. During the forecast period, the Asia Pacific market is projected to record a CAGR of 5.01% during the forecast period, which is the highest amongst all the regions. The market is expanding, driven by large fleet expansion orders from airlines in key economies such as China and India, as well as rising cargo demand from e-commerce. Backed by these factors, China is expected to record a valuation of USD 5.1 billion, Japan USD 3.6 billion, and India USD 4.2 billion in 2026.

Europe

After Asia Pacific, the market in Europe is estimated to reach USD 15.4 billion in 2026. The European regional market is growing owing to the region’s large passenger carrying commercial airline industry, which drives the demand for fuel-efficient engines to reduce operating costs. In the region, the U.K. and Germany are estimated to reach USD 3.8 billion and USD 3.4 billion, respectively, in 2026.

Rest of the World

Over the forecast period, the Middle East & Africa and Latin America regions are expected to witness moderate growth in this market. The Middle East & Africa market, in 2026, is set to record USD 2.6 billion as its valuation. Latin America is set to attain the value of USD 1.6 billion by 2026. The growth is driven by increased passenger volume, low-cost airline expansion, and deliberate fleet expansion in response to growing populations and economies.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Players Undertake Strategic Partnerships to Maintain their Market Positions

The commercial aircraft gas turbine engine market includes dominant players such as GE Aerospace, Pratt & Whitney, Rolls-Royce, and CFM International, among others. These key players focus on fuel-efficient turbofans and hybrid-electric technologies to maintain competitive advantage. Recent joint ventures and technology collaborations enhance production capabilities and SAF compatibility. Furthermore, advancements in open fan architectures alongside digital twin integration strengthen performance optimization. Additionally, industry leaders prioritize MRO expansions and supply chain resilience, with strong momentum in North America and Europe driven by fleet modernization programs and regulatory sustainability mandates

LIST OF KEY COMMERCIAL AIRCRAFT GAS TURBINE ENGINE COMPANIES PROFILED

- GE Aerospace (U.S.)

- Pratt & Whitney (U.S.)

- Rolls-Royce (U.K.)

- Safran Aircraft Engines (France)

- CFM International (France)

- MTU Aero Engines (Germany)

- Honeywell Aerospace (U.S.)

- IHI Corporation (Japan)

- Kawasaki Heavy Industries (Japan)

- Hanwha Aerospace (South Korea)

KEY INDUSTRY DEVELOPMENTS

- November 2025: At the Dubai Airshow 2025, Riyadh Air announced a definitive purchase for 120 CFM International LEAP-1A engines to power 60 Airbus A321neos. This agreement will support the Saudi airline's new narrow-body fleet.

- October 2025: Rolls-Royce and IndiGo reached an agreement for Trent XWB-84 engines to power IndiGo's fleet of A350-900 wide-body aircraft. This agreement is part of a broader order that supports IndiGo's long-haul international expansion by doubling its commitment to 60 A350-900 aircraft. Furthermore, this also includes a comprehensive TotalCare program, which is anticipated to provide long-term engine maintenance, monitoring, and support.

- September 2025: GE Aerospace and BETA Technologies Inc. announced a new strategic partnership and equity investment agreement that would combine GE Aerospace's global reach and experience with BETA's rapid innovation methodology to expedite the development of hybrid electric aircraft.

- June 2025: The Pratt & Whitney’s PW1100G-JM Geared Turbofan (GTF) engine has been selected by Wizz Air to power its 177 firm Airbus A321neo aircraft. Additionally, Wizz Air will also receive engine maintenance from Pratt & Whitney as part of a long-term EngineWise Comprehensive service agreement.

- July 2024: In collaboration with NASA, GE Aerospace developed a hybrid electric demonstrator engine that integrates electric motors and generators into a high bypass commercial turbofan to enhance output throughout various stages of operation.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It encompasses details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological innovations and advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.32% from 2026-2034 |

| Unit | Value (USD Billion ) |

| Segmentation | By Engine Type, Thrust Class, Aircraft Type, Lifecycle Stage, Component, Fuel Type, Technology Type, and Region |

| By Engine Type |

|

| By Thrust Class |

|

| By Aircraft Type |

|

| By Lifecycle Stage |

|

| By Component |

|

| By Fuel Type |

|

| By Technology Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 66.2 billion in 2025 and is projected to reach USD 96.7 billion by 2034.

In 2025, the market value stood at USD 28.6 billion.

The market is expected to exhibit a CAGR of 4.32% during the forecast period of 2026-2034.

The high-bypass non geared turbofan segment dominated the market by engine type in 2025.

The rise in fleet modernization programs is a key factor driving demand in the market.

GE Aerospace (U.S.), Pratt & Whitney (U.S.), Rolls-Royce (U.K.), Safran Aircraft Engines (France), CFM International (France), MTU Aero Engines (Germany), and Honeywell Aerospace (U.S.) are some of the key players in the market.

North America dominated market with the largest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us