Commercial Vehicle Remote Diagnostics Market Size, Share & Industry Analysis, By Vehicle Type (Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, and Buses & Coaches), By Component (Hardware, Software, & Services), By Deployment Type (Cloud-Based & On-Premise), By Connectivity Type (Embedded Systems, Tethered Systems, & Integrated Aftermarket Systems), By Application (Core Vehicle Diagnostics, Predictive Maintenance & Health Monitoring, & Others), By End User (Freight & Logistics Fleet Operators, Public & Passenger Transport Operators, & Others), and Regional Forecast, 2026-2034

Commercial Vehicle Remote Diagnostics Market Size and Future Outlook

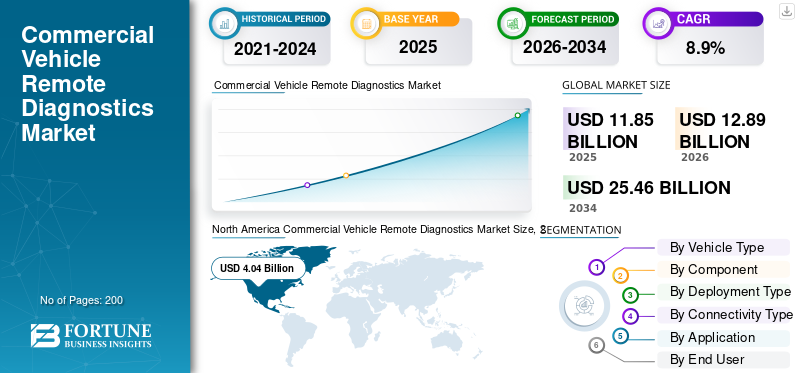

The global commercial vehicle remote diagnostics market size was valued at USD 11.85 billion in 2025. The market is projected to grow from USD 12.89 billion in 2026 to USD 25.46 billion by 2034, exhibiting a CAGR of 8.9% during the forecast period. North America dominated the commercial vehicle remote diagnostics market with a market share of 34.09% in 2025.

The global commercial vehicle remote diagnostics market covers digital tools and services that let fleets, OEMs, and service networks check a truck or van’s condition without physically plugging into it at a workshop. Using onboard sensors, telematics units, and cloud platforms, remote diagnostics can read fault codes, track performance signals, and trigger alerts for maintenance teams. This improves diagnostic capabilities and supports real-time vehicle health monitoring across engines, transmissions, after-treatment systems, batteries, and critical safety modules.

The market will evolve from fault-code reading to predictive and prescriptive maintenance over the forecast period. Fleets are under constant pressure to reduce maintenance costs, improve uptime, and meet stringent regulatory requirements for vehicle compliance. As a result, the increasing demand for connected services is accelerating the adoption of remote diagnostic platforms that combine analytics, workflow automation, and service scheduling. Remote diagnostics also strengthen fleet management solutions by linking health insights with routing, driver behavior, parts planning, and warranty decisions, helping operators improve efficiency and reduce operational costs.

Applications span core fault detection, remote troubleshooting, predictive maintenance, compliance reporting, and service orchestration for both light commercial vehicles and heavy commercial vehicle fleets. Growth is also supported by wider OTA software management, connected powertrains, and digital service ecosystems built by OEMs and Tier-1 suppliers.

In short, market growth is being shaped by data-driven operations and proactive maintenance. Many providers aim to hold the global commercial vehicle remote diagnostics industry through bundled subscriptions, integrated portals, and AI-enabled insights. In parallel, OEMs and telematics vendors such as Bosch, Volvo, and Mack Trucks are expanding platform features, partnerships, and service integrations to strengthen the remote diagnostics market analysis footprint and improve the market size over time.

Download Free sample to learn more about this report.

COMMERCIAL VEHICLE REMOTE DIAGNOSTICS MARKET TRENDS

AI-Assisted Fault Interpretation Becomes a Mainstream Feature

Remote diagnostics is shifting from raw fault codes to guided decision support. Platforms increasingly use AI to explain faults in plain language, prioritize repairs, and recommend next actions. This trend improves technician productivity and strengthens fleet management solutions, helping fleets reduce maintenance costs and speed cycle times. As this scales, it drives the global commercial vehicle remote diagnostics industry toward higher-value subscriptions and differentiated analytics.

- For instance, in June 2025, Samsara highlighted AI tools to simplify vehicle diagnostics, including clearer fault explanations intended to accelerate repairs and improve first-time fix efficiency for fleets.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Uptime Pressure and Cost Inflation Drive Remote Diagnostics Adoption

Rising downtime, parts delays, and technician shortages are pushing fleets to monitor faults earlier and fix vehicles faster. Remote diagnostics supports proactive maintenance, improves first-time fix rates, and helps operators’ efficiency and reduce operational costs by minimizing road calls and unplanned stops. This growing demand for remote diagnostic solutions is central to market size expansion as fleets standardize connected workflows across mixed vehicle populations.

- For instance, in March 2025, Volvo Trucks announced automated remote programming in Volvo Connect, enabling proactive software deployment to opt-in fleets to improve uptime and reduce workshop visits.

MARKET RESTRAINTS

Cybersecurity and Software-Update Compliance Raise Cost and Complexity

As vehicles become connected computers, remote diagnostics must meet stricter cyber and software update controls. Compliance requires secure architectures, documentation, and governance, increasing implementation time and cost, especially for multi-brand fleets and smaller service providers. This can slow the adoption of remote diagnostic solutions in price-sensitive markets. This is expected to hinder the commercial vehicle remote diagnostics market growth in the coming years.

- For instance, in November 2025, the U.K. VCA said new type-approval provisions introduce UN R155 cybersecurity and UN R156 software updating, with mandatory implementation dates beginning in June 2026.

MARKET OPPORTUNITIES

Plug-and-Play Connectivity Expands Coverage Beyond Factory Telematics

A major opportunity is connecting vehicles that lack embedded telematics, especially in older fleets and fragmented regions. Plug-and-play devices and open interfaces let fleets digitize faster, scale remote troubleshooting, and standardize health data without long retrofit projects. This broadens addressable demand for vehicle remote diagnostics and supports market growth by accelerating multi-vehicle rollouts across diverse fleet types.

- For instance, in April 2025, Continental introduced VDO Link, a plug-and-play solution enabling real-time remote retrieval of tachograph and vehicle data without installing a fixed telematics unit.

MARKET CHALLENGES

Data Standardization Gaps Reduce Diagnostic Accuracy at Scale

Commercial fleets run mixed OEM models, model years, and proprietary code libraries. When platforms cannot fully interpret brand-specific faults, the output becomes less actionable, reducing trust in recommendations and slowing workflow automation. This challenge impacts diagnostic capabilities and limits cross-fleet benchmarking. It can weaken the business case for the adoption of remote diagnostic tools, especially where operators expect one pane of glass across diverse assets.

- For instance, in April 2025, Geotab noted some manufacturers use proprietary engine codes not included in standard libraries, which can appear as Unknown Diagnostic faults in telematics outputs.

Segmentation Analysis

By Vehicle Type

Light Commercial Vehicles Lead the Market as They Operate High-utilization Routes

On the basis of vehicle type, the market is segmented into light commercial vehicles, medium & heavy commercial vehicles, and buses & coaches.

Light commercial vehicles dominate as they operate high-utilization routes with frequent stop-start cycles, making uptime and repair speed critical. LCV fleets also adopt telematics earlier for routing, compliance, and maintenance planning, thereby increasing the attach rates for remote diagnostics tools. Their high unit volumes and service intensity accelerate subscriptions and data usage, supporting steady platform expansion across urban logistics and service fleets.

- For instance, in February 2025, Verizon Connect launched solutions including DVIR tools designed to streamline inspections and compliance while supporting fleets with insights that can help reduce vehicle-related operating burden.

The medium & heavy commercial vehicle segment is expected to grow at a CAGR of 10.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Software Leads as It Constantly Improves Models and Dashboards

On the basis of component, the market is segmented into hardware, software, and services.

Software dominates the commercial vehicle remote diagnostics market share as fleets want actionable insights, not just devices. Analytics layers translate signals into prioritized faults, recommended actions, and automated maintenance workflows. Software also scales across vehicles and regions, continuously improving models and dashboards. As fleets focus on outcomes such as uptime and cost control, software monetization expands faster than hardware, reinforcing leadership in connected diagnostics ecosystems.

- For instance, in July 2025, Bosch launched FleetME, a platform that connects vehicle data, predictive analytics, and maintenance scheduling workflows to help fleets manage upkeep holistically.

The services segment is expected to grow at a CAGR of 8.5% over the forecast period.

By Deployment Type

Cloud-based Segment Dominates Through Scalability and Rapid Feature Delivery

On the basis of deployment type, the market is segmented into cloud-based and on-premise.

The cloud-based segment dominates as fleets need fast rollouts, centralized dashboards, and continuous updates across thousands of vehicles. Cloud platforms also enable AI models, benchmarking, and integration with parts and service networks. This structure improves response time for faults and supports enterprise workflows, strengthening ROI for large operators managing distributed fleets.

- For instance, in March 2025, Volvo Connect enhancements streamlined remote programming by proactively sending software updates to opted-in fleets, enabling seamless deployment across trucks to boost uptime.

The on-premise segment is expected to grow at a CAGR of 3.9% over the forecast period.

By Connectivity Type

Embedded Systems Hold Dominance as They Improve Remote Fault Detection

On the basis of connectivity type, the market is segmented into embedded systems, tethered systems, and integrated aftermarket systems.

Embedded systems dominate as factory-installed connectivity provides continuous, secure data capture and deeper access to vehicle subsystems. This improves remote fault detection, supports OTA updates, and reduces dependence on driver devices or aftermarket wiring. Embedded architectures also simplify lifecycle support, enabling OEMs and platforms to deliver consistent diagnostics across large fleet populations.

- For instance, in September 2025, Volvo Trucks reported one million connected trucks on the road, highlighting how connected services enable over-the-air updates that reduce unnecessary workshop visits.

The integrated aftermarket systems segment is expected to grow at a CAGR of 8.2% over the forecast period.

By Application

Core Vehicle Diagnostics Dominates as It is a Daily Operational Baseline

On the basis of application, the market is segmented into core vehicle diagnostics, predictive maintenance & health monitoring, fleet performance & compliance management, and others.

Core vehicle diagnostics dominate as every fleet needs immediate fault visibility for engine, emissions, braking, and electrical issues. It is the entry point for digital maintenance programs and the most frequently used function across fleets, especially in mixed-asset environments. Once core alerts are trusted, fleets expand into predictive maintenance and workflow automation, but core diagnostics remains the highest-volume use case.

- For instance, in April 2025, Geotab published updates that improve how users understand faults, including a more structured view of vehicle fault codes to strengthen diagnostics workflows.

The predictive maintenance & health monitoring segment is expected to grow at a CAGR of 11.2% over the forecast period.

By End User

Freight & Logistics Fleet Operators Lead as They Run Dense Routes

On the basis of end user, the market is segmented into freight & logistics fleet operators, public & passenger transport operators, industrial & specialized fleet operators, OEMs & authorized service networks, and others.

Freight & logistics fleet operators dominate as every hour of downtime disrupts deliveries and reduces asset utilization. They run dense routes, operate large fleets, and rely on predictive insights to plan maintenance around dispatch schedules. Remote diagnostics strengthens maintenance control, reduces roadside incidents, and improves coordination across drivers, dispatchers, and repair networks, making it a high-ROI capability for logistics.

- For instance, in February 2025, Mack Trucks introduced enhanced OTA capabilities to maximize vehicle performance while reducing administrative workload, supporting fleets that prioritize uptime and operational continuity.

The OEMs & authorized service networks segment is expected to grow at a CAGR of 8.8% over the forecast period.

COMMERCIAL VEHICLE REMOTE DIAGNOSTICS MARKET REGIONAL OUTLOOK

By geography, the global market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Commercial Vehicle Remote Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 4.04 billion, and also maintained the leading share in 2024, with USD 3.73 billion. North America dominates due to high telematics penetration, mature fleet digitization, and a strong ROI focus on uptime. Large for-hire carriers and private fleets widely deploy connected platforms that combine maintenance alerts, remote programming, and service network coordination. OEM ecosystems and strong aftermarket telematics adoption further accelerate subscriptions, while fleets prioritize measurable savings from reduced downtime and faster repair cycles. In the U.S., growth is more ROI-driven, with faster SaaS bundling and large-fleet standardization.

- For instance, in March 2025, Volvo Trucks North America expanded Volvo Connect remote programming to streamline OTA updates across new and legacy trucks to maximize fleet uptime.

U.S. Commercial Vehicle Remote Diagnostics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.10 billion, representing roughly 26.2% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 3.76 billion in 2026 and secure the position of the second-largest region in the market. Market growth is led by fleet expansion, rising e-commerce logistics density, and faster digitization in major markets. Mixed maturity encourages both embedded connectivity in newer vehicles and retrofit solutions for older fleets. As uptime pressure increases, platforms that combine diagnostics with dispatch, maintenance planning, and driver workflows scale rapidly across large, cost-sensitive operator bases.

China Commercial Vehicle Remote Diagnostics Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 1.65 billion, representing roughly 13.9% of the global market.

India Commercial Vehicle Remote Diagnostics Market

The India market in 2025 was valued at USD 0.43 billion, accounting for roughly 3.6% of global revenues.

Europe

Europe is projected to record a growth rate of 7.2% in the coming years and reach a valuation of USD 3.42 billion by 2026. Europe will grow through compliance-driven digitization, especially in tachograph, emissions, and software governance requirements. Fleets increasingly adopt connected services that automate data retrieval, maintenance records, and service scheduling, while OEMs expand secure update and diagnostics toolchains aligned with cyber and software rules. The market is more regulation-led than price-led.

Germany Commercial Vehicle Remote Diagnostics Market

The Germany market in 2025 was valued at USD 0.89 billion, accounting for roughly 7.5% of global revenues.

U.K. Commercial Vehicle Remote Diagnostics Market

The U.K. market in 2025 was valued at USD 0.62 billion, accounting for roughly 5.2% of global revenues.

Rest of the World

The Rest of the World market growth is supported by retrofit-friendly connectivity, gradual telematics penetration, and increasing focus on reducing unplanned downtime in mining, construction, and cross-border freight. Adoption is uneven due to infrastructure gaps and cost sensitivity, but plug-and-play solutions and service-based offerings help operators digitize maintenance without heavy upfront investment.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-First Ecosystems Reshape Remote Diagnostics Competition

Competition in the global commercial vehicle remote diagnostics market is shaped by how well players convert vehicle data into actionable maintenance outcomes. OEMs (truck and bus makers) focus on embedded connectivity, remote programming, and dealer integration. Tier-1 suppliers and telematics platforms compete by offering broader multi-brand coverage, faster analytics, and workflow tools that convert health alerts into work orders and service events.

A key differentiator is data depth. Companies that decode more fault code libraries, correlate them with operating conditions, and surface clear recommendations are viewed as having stronger diagnostic capabilities. Another differentiator is integration; customers prefer platforms that connect remote fault detection with scheduling, parts availability, warranty claims, and technician communication, as this directly helps reduce maintenance costs and improves fleet uptime.

Cloud architecture is becoming the default as it supports rapid feature releases, cross-fleet benchmarking, and scalable AI models. That is why many vendors position cloud analytics as the backbone of fleet management solutions and the broader vehicle remote diagnostics market. Players are also expanding cybersecurity and software update compliance, since connected vehicles create new audit requirements, and customers expect trusted data governance across the remote diagnostics market report lifecycle.

To win share, leading companies pursue OEM-to-platform partnerships, acquisitions of workflow or analytics capabilities, open APIs for third-party apps, and bundled subscriptions that link remote diagnostics with safety, compliance, and operational dashboards. This strategy directly drives the global toward platform consolidation, where a smaller set of ecosystems can hold the global commercial vehicle remote diagnostics industry through long-term contracts and embedded services.

- For instance, in March 2025, Trimble and Daimler Truck North America integrated Trimble Road Call with Freightliner Service Tracker to streamline repairs and reduce downtime using connected maintenance workflows.

LIST OF KEY COMMERCIAL VEHICLE REMOTE DIAGNOSTICS COMPANIES PROFILED

- Bosch (Germany)

- Continental (Germany)

- ZF Friedrichshafen (Germany)

- Volvo Group (Sweden)

- Scania (Sweden)

- PACCAR (U.S.)

- Cummins (U.S.)

- Allison Transmission (U.S.)

- Geotab (Canada)

- Samsara (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Daimler Truck introduced Short Test as a next-generation diagnostic solution, replacing its previous Remote Diagnostics system. The updated platform provides faster vehicle status checks, mobile-enabled accessibility, and improved integration with workshop workflows, supporting more efficient service handling and strengthening digital maintenance capabilities across its commercial vehicle network.

- October 2025: ZF launched a SUMS Service Suite aligned with UN/ECE R156 needs, combining tools and services to support secure software update management. It links ZF diagnostics capabilities with scalable software governance.

- August 2025: Continental introduced VDO Link, a plug-and-play solution that connects digital tachographs to cloud services for remote data retrieval. It reduces the need for permanently installed telematics units and speeds up connectivity deployments.

- June 2025: Bosch launched FleetME, a digital fleet maintenance platform designed to centralize vehicle data, diagnostics alerts, and service scheduling into a single interface. The solution integrates predictive analytics with workshop coordination tools, enabling fleets to proactively manage upkeep, minimize downtime, and streamline maintenance decision-making across multi-brand vehicle operations.

- April 2025: Cummins announced the global release of its updated PrevenTech platform at Bauma 2025. The platform emphasizes remote monitoring and predictive analytics to improve engine uptime and performance outcomes.

- March 2025: Volvo Trucks North America announced enhancements to Volvo Connect and remote programming, streamlining OTA updates across new and legacy trucks. The move strengthens uptime services tied to connected diagnostics.

- March 2025: Trimble and Daimler Truck North America announced an integration between Trimble TMT Fleet Maintenance (Road Call) and Freightliner Service Tracker. It targets faster repairs by connecting breakdown events with maintenance workflows.

- February 2025: Mack Trucks announced enhancements to its over-the-air capabilities, including automated software deployment features aimed at reducing admin workload and improving vehicle performance for fleets. This supports connected maintenance and diagnostics workflows.

REPORT COVERAGE

The global commercial vehicle remote diagnostics market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.9% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Component, Deployment Type, Connectivity Type, Application, End User, and Region |

| By Vehicle Type |

|

| By Component |

|

| By Deployment Type |

|

| By Connectivity Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.85 billion in 2025 and is projected to reach USD 25.46 billion by 2034.

In 2025, the market value in North America stood at USD 4.04 billion.

The market is expected to exhibit a CAGR of 8.9% during the forecast period of 2026-2034.

The light commercial vehicles segment led the market by vehicle type.

Uptime pressure and cost inflation drive market expansion.

Bosch, Volvo, Geotab, and ZF are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us