Connected Car Data Monetization Service Market Size, Share & Industry Analysis, By Type (Direct Monetization and Indirect Monetization), By Data Type (Vehicle Diagnostics & Health Data, Driving Behavior & Usage Data, Location & Mobility Data, and Others), By Application (Insurance & Risk Assessment, Fleet Management & Operations, Predictive Maintenance & Aftermarket Services, and Smart Cities & Traffic Management), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

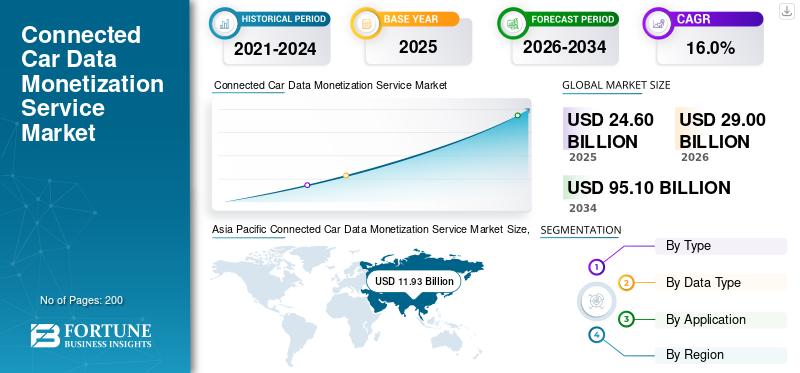

The global connected car data monetization service market size was valued at USD 24.60 billion in 2025. The market is projected to grow from USD 29.00 billion in 2026 to USD 95.10 billion by 2034, exhibiting a CAGR of 16.0% during the forecast period. Asia Pacific dominated the global market with a market share of 48.49% in 2025.

he connected car data monetization service market refers to the market encompassing platforms, solutions, and services that enable automotive ecosystem participants to leverage data generated by connected vehicles for commercial purposes. This market encompasses the collection, aggregation, processing, analytics, and commercialization of vehicle-generated data, including telematics, diagnostics, location, usage patterns, and driver behavior. Monetization is achieved through both direct revenue models, such as data-as-a-service, Subscription, and partnerships, and indirect models, where real-time data is used to enhance customer experience, improve vehicle lifecycle management, enable predictive maintenance, support usage-based insurance, and optimize mobility and fleet operations. The market is driven by the rising penetration of connected and autonomous vehicles, advancements in cloud-based computing and analytics, and increasing demand for data-driven mobility services. Meanwhile, data privacy, cybersecurity, and regulatory compliance remain critical structural considerations.

From a competitive landscape and key player perspective, the market is characterized by the presence of automotive industry OEMs such as Otonomo, CARUSO Dataplace, HERE Technologies, and Motorq, telematics service providers, technology firms, and data platform specialists, each positioned at different points of the data value chain. OEMs typically hold a strategic advantage due to direct access to in-vehicle data and are increasingly developing proprietary data platforms or forming partnerships to monetize this asset. Technology and platform providers focus on scalable analytics, AI-driven insights, and secure data exchange frameworks to enable monetization across multiple use cases. Meanwhile, telecom and mobility service providers play a supporting role by ensuring connectivity, data transmission, and ecosystem integration. Overall, market competition is shaped by data ownership, analytics capabilities, ecosystem partnerships, and the ability to deliver compliant, value-added services to end-users, including insurers, fleet operators, municipalities, and digital service providers.

Download Free sample to learn more about this report.

CONNECTED CAR DATA MONETIZATION SERVICE MARKET TRENDS

Shift Toward Subscription-Based and Recurring Revenue Data Monetization Models is a Key Market Trend

The shift toward subscription-based and recurring revenue data monetization models is a key trend shaping the market. Automotive OEMs and service providers are increasingly moving away from one-time data transactions toward continuous, service-oriented revenue streams such as connected car services, advanced analytics subscriptions, and data-driven mobility solutions. This model allows stakeholders to generate predictable and long-term revenue while strengthening customer engagement throughout the vehicle lifecycle. Additionally, subscription-based monetization supports continuous software updates, personalized services, and scalable deployment across vehicle fleets. As a result, the growing preference for recurring revenue models is redefining monetization strategies and accelerating the evolution of connected car data services.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Increase in Global Penetration of Connected and Software-Defined Vehicles Drives Market Growth

The rapid increase in the global penetration of connected and software-defined vehicles is a key factor driving the market's growth. Modern vehicles are increasingly equipped with advanced sensors, embedded connectivity, and software-centric architectures that continuously generate large volumes of real-time data. As the number of such vehicles on the road increases, the availability of high-value data related to driving behavior, vehicle health, location, and usage patterns expands significantly. This growing data pool creates substantial opportunities for automotive OEMs and service providers to develop monetization models centered on digital services, analytics-driven insights, and recurring revenue streams. Consequently, key participants are increasingly investing in data platforms, software capabilities, and ecosystem partnerships to capitalize on this expanding connected vehicle base, thereby accelerating the connected car data monetization service market growth.

MARKET RESTRAINTS

Stringent Data Privacy and Vehicle Data Protection Regulations are Restricting Market Growth

Stringent data privacy and vehicle data protection regulations across various regions are significantly restraining the market's growth. Governments and regulatory bodies have implemented strict frameworks governing the collection, storage, processing, and sharing of vehicle and personal data, requiring explicit user consent and robust data security measures. Compliance with these regulations increases operational complexity and raises investment requirements for automotive OEMs and service providers, particularly for cross-border data sharing and large-scale commercialization. In addition, evolving regulatory standards create uncertainty for market participants, limiting their ability to monetize connected car data freely. As a result, these regulatory constraints slow the pace of service adoption and limit the full monetization potential of connected vehicle data, thereby restricting market growth.

MARKET OPPORTUNITIES

Expansion of Fleet Management and Logistics Digitalization Initiatives is Creating Growth Opportunities

The expansion of fleet management and logistics digitalization initiatives is creating significant growth opportunities in the market. Fleet operators and logistics companies are increasingly adopting connected vehicle technologies to gain real-time visibility into vehicle location, performance, fuel consumption, and driver behavior. This growing reliance on data-driven fleet operations is increasing demand for advanced analytics, predictive maintenance, and optimization services derived from connected car data. As logistics networks continue to digitalize, automotive OEMs and data service providers have increased opportunities to monetize vehicle data through subscription-based platforms, data analytics services, and value-added solutions tailored to enhancing fleet efficiency and reducing costs. Consequently, the rising focus on digital transformation within fleet and logistics operations is accelerating the adoption of connected car data monetization services.

MARKET CHALLENGES

High Cybersecurity Risks Associated with Connected Vehicle Ecosystems Challenging Market Adoption

High cybersecurity risks associated with connected vehicle ecosystems represent a significant challenge for the market. Connected vehicles rely on continuous data exchange across onboard systems, cloud platforms, and third-party applications, thereby increasing their exposure to cyber threats, including data breaches, unauthorized access, and system manipulation. These risks compel OEMs and service providers to invest heavily in advanced security architectures, encryption technologies, and continuous monitoring systems, thereby raising operational costs. Additionally, cybersecurity incidents can erode consumer trust and limit their willingness to share vehicle data, directly impacting the monetization potential. As a result, managing cybersecurity risks remains a critical challenge that can hinder market adoption and limit the large-scale commercialization of connected car data services.

Segmentation Analysis

By Type

Increasing Use of Connected Vehicle Data Boosted Indirect Monetization Segment Growth

Based on type, the market is segmented into direct monetization and indirect monetization.

The indirect monetization segment is expected to account for the dominant share of the market. The strong position of this segment is primarily driven by the increasing use of connected vehicle data to enhance internal operations, customer experience, and long-term value creation rather than immediate data sales. Automotive OEMs and mobility service providers are leveraging vehicle-generated data to enable predictive maintenance, improve vehicle performance, optimize product development, and support subscription-based digital services. Unlike direct monetization, indirect models face relatively lower regulatory and consumer resistance, as data is primarily used to deliver value-added services instead of being sold to third parties. Furthermore, the growing focus of OEMs on software-defined vehicles and lifecycle-based revenue models continues to strengthen the adoption of indirect monetization strategies, supporting sustained segmental growth.

The direct monetization segment is driven by the increasing demand for real-time vehicle data from third-party stakeholders such as insurers, fleet operators, mobility service providers, and smart city authorities.

By Data Type

Growing Demand for Usage-Based and Behavior-Driven Insights to Propel Driving Behavior & Usage Data Segment Growth

Based on data type, the market is segmented into vehicle diagnostics & health data, driving behavior & usage data, location & mobility data, and others.

The driving behavior & usage data segment is anticipated to hold the largest connected car data monetization service market share. The dominance of this segment is primarily attributed to its wide applicability across multiple high-value use cases such as usage-based insurance, fleet management, driver safety monitoring, and personalized mobility services. Data related to acceleration patterns, braking behavior, mileage, driving frequency, and vehicle usage intensity enables OEMs, insurers, and mobility service providers to develop tailored offerings and risk-based pricing models. Compared to other data types, driving behavior and usage data deliver immediate commercial value and support recurring revenue models through continuous data streams. Additionally, the increasing adoption of connected fleets and pay-as-you-drive solutions is further strengthening demand for this data type, reinforcing its leading position within the market.

The vehicle diagnostics & health data segment is anticipated to expand at the fastest rate, depicting a CAGR of 17.0% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising Adoption of Usage-Based Insurance Models to Drive Insurance & Risk Assessment Segment Growth

Based on application, the market is segmented into insurance & risk assessment, fleet management & operations, predictive maintenance & aftermarket services, and smart cities & traffic management.

The insurance & risk assessment segment is expected to dominate the market. The strong growth of this segment is primarily driven by the increasing adoption of usage-based insurance (UBI) and pay-how-you-drive models, which rely heavily on real-time driving behavior and vehicle usage data. Insurers are leveraging connected car data to enhance risk profiling, improve pricing accuracy, reduce fraud, and offer personalized policies, thereby improving profitability and customer retention. Additionally, collaboration between automotive OEMs, telematics providers, and insurance companies has accelerated the integration of connected vehicle data into insurance platforms. These factors collectively strengthen the dominance of the insurance and risk assessment segment and continue to drive its expansion within the market.

The Predictive Maintenance & Aftermarket Services segment is anticipated to expand at the fastest rate, depicting a CAGR of 17.2% over the forecast period.

Connected Car Data Monetization Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Connected Car Data Monetization Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is expected to witness the fastest growth in the market, driven by rising vehicle production, increasing connected car penetration, and rapid urbanization. Countries such as China, Japan, and South Korea are actively investing in smart transportation and vehicle connectivity solutions. The expanding middle-class population and growing demand for digitally enabled vehicles are further accelerating data generation. Additionally, the increasing adoption of fleet management and mobility-as-a-service platforms is creating new monetization opportunities, positioning Asia Pacific as a high-growth regional market.

China Connected Car Data Monetization Service Market

Large-scale connected vehicle deployment, strong government support for smart transportation, rapid digitalization of mobility services, and growing OEM investments in data-driven platforms are accelerating market growth in China.

North America

North America holds a significant market share, driven by the early adoption of connected vehicle technologies and the strong presence of automotive OEMs, automotive companies, and telematics providers. High penetration of advanced driver assistance systems, software-defined vehicles, and usage-based insurance models has accelerated demand for vehicle data monetization services. Additionally, mature digital infrastructure and high consumer acceptance of subscription-based services are supporting market growth. Strategic collaborations between OEMs, insurers, and mobility service providers further strengthen the region’s position, while continuous investments in data analytics and cybersecurity enhance large-scale commercialization.

U.S. Connected Car Data Monetization Service Market

The high adoption of connected vehicles, a strong presence of OEMs and insurers, and the rapid uptake of usage-based insurance and subscription-based digital services are driving market growth in the U.S.

Europe

Europe represents a key market for connected car data monetization, supported by strong automotive manufacturing capabilities and rapid integration of connected and electric vehicles. OEMs in the region are increasingly focusing on indirect data monetization strategies to enhance vehicle lifecycle management and digital services. Although stringent data protection regulations influence data usage practices, they have also encouraged the development of secure and compliant monetization frameworks. Growing adoption of smart mobility, fleet electrification, and connected logistics solutions continues to drive demand for advanced vehicle data analytics across the region.

U.K. Connected Car Data Monetization Service Market

Rising adoption of connected and electric vehicles, expanding telematics-based insurance models, and an increasing focus on smart mobility and regulatory-compliant data monetization support market growth in the U.K.

Rest of the World

The Rest of the World market, comprising Latin America, the Middle East & Africa, is experiencing steady growth in connected car data monetization services. The improvement of automotive connectivity infrastructure and the gradual adoption of telematics solutions are supporting market expansion. Fleet management and logistics applications are emerging as key use cases, particularly in commercial transportation and urban mobility. While the region currently lags in connected vehicle penetration compared to developed markets, increasing investments in smart city initiatives and digital mobility solutions are expected to create long-term growth opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Platform Expansion by Key Players to Propel Market Progress

The connected car data monetization service market demonstrates a moderately consolidated competitive landscape, with a mix of specialized data platform providers, telematics companies, and mobility technology firms playing a critical role in market development. Key players, including Otonomo, CARUSO Dataplace, HERE Technologies, and Motorq, focus on creating secure, standardized data marketplaces that enable OEMs and service providers to commercialize vehicle data efficiently. Telematics leaders, including Octo Telematics, Geotab, CalAmp, Ituran, and Gurtam, strengthen their market presence through large-scale data analytics capabilities, fleet-focused solutions, and long-standing partnerships across the insurance, logistics, and mobility sectors.

Other notable participants such as Smartcar, Inc., VINchain, Cox Automotive, and Bright Box, emphasize API-driven data access, blockchain-enabled data integrity, and digital vehicle lifecycle solutions to enhance monetization opportunities. Collectively, these companies are expected to prioritize ecosystem expansion, interoperability, and the development of value-added services to strengthen their competitive positioning and capture a larger share of the global market during the forecast period.

LIST OF KEY CONNECTED CAR DATA MONETIZATION SERVICE COMPANIES PROFILED:

- Otonomo (Israel)

- CARUSO Dataplace (Germany)

- Smartcar, Inc. (U.S.)

- VINchain (U.S.)

- Octo Telematics (Italy)

- Geotab (Canada)

- CalAmp (U.S.)

- Ituran (Israel)

- Gurtam (Lithuania)

- Cox Automotive (U.S.)

- HERE Technologies (Netherlands)

- Bright Box (Switzerland)

- Motorq (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, Smartcar announced that Mercedes-Benz is now available on Smartcar! Connect Mercedes-Benz electric vehicles to access vehicle data and enable smart charging capabilities. Mercedes-Benz BEV and PHEV vehicles can now connect through Smartcar. Enhanced connect flow with VIN verification for Mercedes vehicles.

- In September 2025, Smartcar launched an updated Smartcar Platform with enhanced webhooks and API improvements, enabling developers and businesses building connected mobility applications to access higher-frequency, reliable vehicle data.

- In December 2024, Mitsubishi Motors entered into a commercial agreement with Otonomo to enhance in-vehicle connectivity and deliver smart services, including parking, concierge offerings, and preventive maintenance, by leveraging Otonomo’s automotive data platform. This demonstrates the strategic adoption of connected car data solutions in production vehicles.

- In January 2024, Octo Telematics developed a smartphone-based crash detection system that utilizes telematics data to identify accidents and enhance emergency response services, demonstrating the company’s ongoing innovation in telematics and safety applications.

- In September 2023, CARUSO partnered with Toyota to develop next-generation fleet management solutions, enabling real-time, consented connected car data from Toyota vehicles. This partnership aims to enhance fleet efficiency and inform data-driven decision-making.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.0% from 2025-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Data Type, By Application, and By Region |

|

By Type |

· Direct Monetization · Indirect Monetization |

|

By Data Type |

· Vehicle Diagnostics & Health Data · Driving Behavior & Usage Data · Location & Mobility Data · Others |

|

By Application |

· Insurance & Risk Assessment · Fleet Management & Operations · Predictive Maintenance & Aftermarket Services · Smart Cities & Traffic Management |

|

By Region |

· North America (By Type, By Data Type, By Application, and By Country) o U.S. (By Type) o Canada (By Type) o Mexico (By Type) · Europe (By Type, By Data Type, By Application, and By Country) o Germany (By Type) o U.K. (By Type) o France (By Type) o Rest of Europe (By Type) · Asia Pacific (By Type, By Data Type, By Application, and By Country) o China (By Type) o Japan (By Type) o India (By Type) o Rest of Asia Pacific (By Type) · Rest of the World (By Type, By Data Type, By Application, and By Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 24.60 billion in 2025 and is projected to reach USD 95.10 billion by 2034.

In 2025, the market value stood at USD 11.93 billion.

The market is expected to exhibit a CAGR of 16.0% during the forecast period of 2026-2034

The driving behavior & usage data segment is expected to lead the market by data type.

The rapid increase in global penetration of connected and software-defined vehicles drives the market growth.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us