Connected Living Room Market Size, Share & Industry Analysis, By Product Type (Smart TVs & Streaming Devices/STBs, Gaming Consoles, Smart Speakers & Voice Assistants, Home Theater Systems & Soundbars, Computer and Laptops, Connected Security Systems, and Others), By Connectivity Type (Wired Devices and Wireless Devices), By Application (New Installation and Retrofit Installation), By End-user (Individual Households, Luxury Apartments, and Hospitality Sector), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

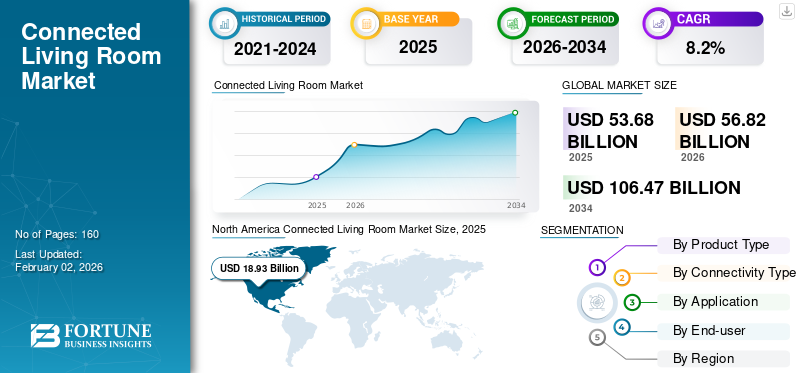

The global connected living room market size was valued at USD 53.68 billion in 2025 and is projected to grow from USD 56.82 billion in 2026 to USD 106.47 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period. North America dominated the dental market with a market share of 35.3% in 2025.

The connected living room is referred to an interconnected ecosystem of entertainment, and smart home devices (e.g., smart TVs, gaming consoles, smart speakers, media streaming devices, and others) that interact to create a fully integrated and immersive digital experience. These devices can work with voice assistants, home automation platforms, and mobile applications, allowing for shared ownership, integration, and personalization of content on multiple devices throughout the home.

With consumers increasingly looking for integrated and intelligent experiences in the home, the market is innovating products with features such as real-time content synchronization, AI-based recommendations, and cross-platform use and interaction. The market desires a seamless and consistent customer experience across entertainment, communication, and smart home automation.

Major players such as ABB, Amazon, Nvidia, Samsung, Google LLC, and Honeywell are increasingly focusing on building comprehensive ecosystems rather than standalone devices. Their strategies involve integrating hardware, software, and AI capabilities to deliver smarter, more responsive living spaces. From voice-controlled assistants to intelligent automation hubs, these companies are driving the shift toward connected environments that anticipate user need.

Download Free sample to learn more about this report.

Connected Living Room Market Key Takeaways

- 2025 Market Size: USD 53.68 billion

- 2026 Market Size: USD 56.82 billion

- 2034 Forecast Market Size: USD 106.47 billion

- CAGR: 8.2% from 2026–2034

- North America dominated the market with a 35.30% share in 2025.

- Smart TV & Streaming Devices/STBs segment is projected to hold a 29.70% share in 2026.

- Wireless Devices segment is projected to hold a 70.03% share in 2026.

North America

The market reached USD 18.93 billion in 2025, driven by high smart home adoption and digital infrastructure.

Asia Pacific

The market reached USD 15.41 billion in 2025, driven by rising internet penetration and smart home adoption.

Europe

The market reached USD 10.16 billion in 2025, driven by strong smart TV adoption and digital ecosystems.

U.S.

The market is projected to reach USD 14.68 billion by 2026.

Japan

The market is projected to reach USD 2.90 billion by 2026.

Read More

IMPACT OF GENERATIVE AI

Implementation of Generative AI Capabilities to Fuel the Market Growth

Generative AI is set to transform the connected living room by making the experience more natural, personalized, and immersive than ever before. Unlike conventional AI, which is goal-oriented and follows pre-disclosed information, generative AI learns user preferences and can adjust according to it in real-time. For instance, a smart TV not only recommends shows but generates a custom highlight reel based on preferences or automatically edits the "spoilers" from a show or movie. For instance,

- In February 2025, Glance partnered with Google Cloud to bring generative AI experiences to smartphone lock screens and ambient TV screens, aiming to create a personalized “internet” for users. Glance plans to include features such as AI-driven commerce and personalized wallpapers using Google's Gemini and Imagen AI models.

Voice assistants will shift from voice commands to participate in natural conversations, voicing opinions on movies, comparing and contrasting relevant content based on the user's preferences, and creating bedtime stories for kids. For instance,

- In February 2025, Amazon unveiled Alexa+, a next-gen digital assistant powered by generative AI, offering more natural conversations, personalized interactions, and the ability to complete tasks such as bookings and shopping.

Smart home systems identify user patterns, resulting in more predictable solutions, especially for lighting and temperature changes, along with site-specific maintenance reminders, generated by AI before service failures. For instance,

- In January 2025, Philips Hue announced a roll out a generative AI-powered lighting assistant in early 2025, enabling users to create custom lighting scenes using text or voice prompts describing moods, events, or styles. This marks Hue’s leap into generative AI, joining rivals such as Govee, as it expands smart home personalization.

IMPACT OF RECIPROCAL TARIFF

Reciprocal Tariff Rates Will Hamper the Market Growth

Reciprocal tariffs can change the market when the potential for global supply chains gets disrupted, and prices increase. Most smart home devices contain imported components, such as chips, displays, and sensors, that usually incur cross-border tariffs. For instance,

- If the U.S. imposes a 30% tariff on Chinese-made smart displays and China retaliates with tariffs on American microprocessors, companies such as Amazon and Google could face a 15-20% rise in production costs for devices including Echo Shows and Nest Hubs.

MARKET DYNAMICS

Connected Living Room Market Trends

Sustainability and Energy Efficiency Has Emerged as a Key Trend in the Market

Sustainability and energy efficiency are central in the connected living room sector. Consumers are rapidly inclining toward smart appliances that are environmentally sustainable and energy-efficient models, featuring low standby power, and intelligent power-saving modes. As major part of these consumers are environmentally conscious young adults who want to save money as power utilities increase rates, and/or want to adopt energy-saving technology. For instance,

- In March 2025, Samsung’s SmartThings Flex Connect expands to PJM, the largest U.S. wholesale electricity market. Users across the Mid-Atlantic and Chicago can automate smart devices to save energy and earn a USD 50 reward.

Manufacturers such as LG, Samsung, and Sony are incorporating eco-friendly materials, including recycled plastics, into smart TVs, speakers, and remotes, reducing packaging waste. Green initiatives in product design focus on low-power adoption, such as solar-powered remotes, recyclable components, and features that reduce energy consumption. For instance,

- In August 2023, LG presented its “Sustainable Life, Joy for All” vision, highlighting eco-friendly home solutions and strong commitments to recycling. The LG Sustainable Village featured smart homes such as the solar-powered Smart Cottage, energy-efficient appliances, and MoodUP™ refrigerators with color-changing doors made from recycled materials. Visitors explored ThinQ UP customizable tech and appliances crafted with recycled plastics, underscoring LG’s upcycling efforts.

Market Drivers

Rising Smart Home Adoption to Drive the Market Growth

Connected living rooms are increasingly becoming crucial to smart home ecosystems, transforming a traditional entertainment space into a smarter setting that enhances convenience, comfort, and efficiency. As consumer expectations for their living rooms changes from the numerous devices in the room "working" together to the devices seamlessly operating in conjunction with other connected home devices, such as lighting, thermostats, security cameras, and voice assistant devices (Alexa, Siri, Google Assistant), the potential to connect can enhance the connected living experience as all devices can be controlled from one interface or with simple voice commands.

Connected smart devices can provide a seamless experience connecting entertainment, lighting, climate, and security. They also enable automation settings such as the lights automatically dimming when a movie starts or the music pauses, when a doorbell camera detects someone approaching the door, creating a more personalized experience. Additionally, recent investments in the smart home market are driving the connected living room market growth. For instance,

- In March 2025, Gopalan Enterprises announced investing USD 58.5 million to develop 3,000 AI-powered smart homes in Bengaluru by 2025, targeting tech-savvy millennials. The homes, priced between USD 0.20 million- USD 0.30 million, will feature AI-controlled appliances and flexible Japanese-inspired furniture. Projects will be located in Whitefield and Rajarajeshwari Nagar.

- In December 2024, SmartRent launched a USD 10 million investment program to enhance its Smart Operations Solutions for the rental housing industry. The investment will drive innovation in AI workflows, preventive maintenance, and centralized property management, improving efficiency, resident experience, and operational insights across rental communities.

Market Restraints

Privacy and Security Threats Restrain Market Growth

Privacy and security threats are substantial barriers to the connected living room market growth. Concerns about data breaches, hacking, and "invasion of privacy" of devices that collect sensitive information, viewing habits, or even audio and video recording, including smart TVs, voice assistants, and connected cameras, hamper the end users.

If these elements are compromised within smart home systems, data linked to a user's connected smart home could become vulnerable, potentially exposing personal data, financial data, or private images to hackers via vulnerable smart devices.

High-profile smart device hacking or surveillance incidents have further hampered public confidence. As a result of the complexity of trust and privacy, consumers are usually confused by privacy policies, consent items and settings, making it difficult to know when sensitive personal information is being collected or shared. For instance,

- In May 2024, a Korean hacker breached wallpad cameras in over 400,000 South Korean homes, accessing private videos and photos from smart home systems and selling intimate footage online. He exploited vulnerabilities in apartment security devices and used overseas servers to hide his tracks.

Market Opportunities

Emerging Markets Around the World Create Lucrative Market Opportunities

Emerging markets offer significant opportunities for the market, driven by growing internet access, rising incomes, and a strong demand for affordable technology.

Consumers are interested in smart home and digital entertainment experiences in different parts of Asia, Africa, Latin America, and Middle Eastern regions. However, they are often unable to afford high-end devices. Consequently, there is demand for lower-cost alternatives, including affordable streaming devices such as Fire Stick, Roku, and inexpensive Android TV sticks to convert a standard television into a smart television with minimal new hardware investment.

The introduction of 5G adds to new offerings, as slow broadband has restricted the delivery of 4K and 8K video streaming content in areas with only limited offerings, thus enhancing entertainment experiences and enabling more complex smart home uses. Companies that can deliver reliable, affordable, and locally relevant solutions are well-positioned to capture market share in these expanding territories. For instance,

- In March 2024, IKEA launched the TRETAKT smart plug online across various EU countries, priced from USD 7.5 to USD 8.5. The plug lets users control regular household devices via voice commands, remote control, or the IKEA app, but requires pairing with the DIRIGERA or TRADFRI gateway for app features. It supports up to 3,680W and has a built-in on/off button. Availability in other markets such as the U.S. and U.K. remains uncertain.

SEGMENTATION ANALYSIS

By Product Type

Smart TV & Streaming Devices/STBs to Lead the Market Due to their Accelerating Adoption

Based on product type, the market is segmented into smart TV & streaming devices/STBs, gaming consoles, smart speakers & voice assistants, home theatre systems & soundbars, computers & laptops, connected security systems, and others.

The Smart TV & streaming devices/STB segment dominated the market accounting for 29.7% market share in 2026, over the forecast period, due to the evolution of smart TVs being the primary entertainment location within households. Consumers now prefer smart TVs as they have built-in internet capabilities, direct access to streaming services such as Netflix, Disney+, and YouTube, with standard integration of voice assistants such as Alexa or Google Assistant. With the falling prices of large, high-resolution smart televisions (4K and 8K), they are now available to a large number of end users, resulting in rapid adoption. Therefore, smart TVs replace older televisions as the hub in the connected living room ecosystems and remain a smart device leader, establishing them as a potential component in the smart home market.

Connected security systems are projected to experience the fastest growth rate over the forecast timeframe as consumers become more safety-minded and value remote access to real-time monitoring. As urban areas continue to grow, and concerns of burglary or intrusion expand along with newfound knowledge of smart security options, there is a growing demand for leading-edge smart home security options. Most modern connected security devices, such as smart cameras, video doorbells, motion detectors, or integrated alarm systems, are either wireless or easy to install and connect to other smart home platforms. For instance,

- In February 2025, Reolink launched new wireless security camera systems designed for easy home use, featuring battery-powered 4K cameras, solar panels, and a Home Hub for managing up to 8 cameras with no subscription fees.

By Connectivity Type

Surging Adoption of Wireless Solutions Fuels the Segment’s Growth of Wireless Devices

Based on connectivity type, the market is segmented into wired devices and wireless devices.

The Wireless devices segment is projected to dominate the market with a share of 70.03% in 2026 and grow at the highest CAGR in the market as they provide unrivaled convenience, flexibility, and modern user experiences. Consumers are steadily falling towards wireless solution options, including smart speakers, streaming sticks, and wireless audio systems that can eliminate cable clutter and simplify installation while supporting their use within a smart home ecosystem. Further improvements in wireless technology, Wi-Fi 6, Bluetooth Low Energy, and ultra-wideband (UBW), drive performance, reliability, and energy efficiency, encouraging its widespread adoption and upgrades over performance improvements.

While wireless devices are the standard in the connected living room marketplace, wired devices still matter, particularly where speed and stability matter in gaming consoles, set-top boxes, and home theatre devices. These devices offer lower latency and more stable performance, meaning they are often preferred when bandwidth-intensive usage is required.

By Application

Accelerating Retrofit Installations Propel the Segment Growth

Based on application, the market is bifurcated into new installation and retrofit installation.

The retrofit installation segment will account for 70.74% market share in 2026. This is due to the immense building stock of existing buildings in both residential and commercial sectors, and their growing adoption of smart technologies. Property owners going through the population migration shift are updating rather than building new infrastructure. Furthermore, government incentives for smart energy retrofits and sustainability certifications are pushing legacy properties toward such upgrades, reinforcing the dominance of retrofit in market. For instance,

- In February 2025, Lambeth Council completed energy-saving upgrades for nearly 700 social homes as part of a USD 7.2 million retrofit project in partnership with Metropolitan Thames Valley Housing and the U.K. Government's Social Housing Decarbonisation Fund.

New installations are expected to grow at the highest CAGR, as there is an increased opportunity for greenfield construction projects to be designed from scratch with smart infrastructure. Emerging economies, rapid urbanization, and rising consumer demand for tech-enabled, energy-efficient living spaces create a inclination for investors, architects, and developers to integrate AI-driven and IoT-based systems in architecture and construction at the beginning of greenfield projects.

By End-user

To know how our report can help streamline your business, Speak to Analyst

Mass Market Adoption by Households Propels the Segment Growth

Based on end-user, the market is segmented into individual households, luxury apartments, and hospitality sector.

Household markets are forecasted to hold the largest connected living room market share over the forecast period, as a cross-section of middle-income consumers has adopted smart entertainment and automation technology. Affordable smart TVs, streaming devices, voice assistants, and modular home connectivity systems have conveniently added smart living room solutions within households. Additionally, the growth of personalization for entertainment and convenience, and energy efficiency at home is strengthening the market as households continue to renovate their first smart home with accessible smart technology.

Furthermore, luxury apartments are projected to grow at the highest CAGR owing to the increasing incorporation of high-end, fully integrated smart living room ecosystems during construction. Developers of premium residential projects prioritize smart infrastructure to attract affluent buyers seeking tech-enabled lifestyles. For instance,

- In November 2024, Imtiaz Developments has partnered with global tech leader Legrand to equip 18 luxury waterfront projects in Dubai with smart home automation and access control systems. Residents can control lighting, climate, security, and entertainment through smart devices, enhancing modern, tech-driven living.

CONNECTED LIVING ROOM MARKET REGIONAL OUTLOOK

Based on the region, the market is segmented into North America, South America, Europe, Asia Pacific and Middle East & Africa.

North America

North America Connected Living Room Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 18.93 billion, representing 35.30% of global demand, and is expected to reach USD 19.88 billion in 2026. North America holds the majority of the connected living room market share. This is due to technology readiness and pent-up demand from consumer for digital experiences. High-speed internet is ubiquitous in North America, constituting a suitable infrastructure base for reliable streaming, gaming, and smart home integration. More than infrastructure, North American consumers have a strong need for smart technology and the increasing disposable income to invest in high-priced devices such as smart TVs, next-generation sound systems, and voice-controlled hubs. For instance,

- According to industry reports, in 2023, around 63.43 million residences in the U.S. were utilizing smart home devices. This represents nearly 45% of all households in the U.S.

The culture in the U.S. strongly inclines toward modern devices; enabling the associated market to prosper as Americans quickly adopt smart devices that convert their living room into entertainment consumption, gaming, and control of their homes in one experience based on personalization and convenience. The U.S. market is projected to reach USD 14.68 billion by 2026.

Download Free sample to learn more about this report.

South America

South America is projected to grow at a slow and steady CAGR in the market as economic conditions and income levels vary widely across the region. Although there is an increasing interest in smart TVs, streaming devices, and home automation, the economic volatility in many South American countries including Argentina and Brazil face significant local currency depreciation, keeping many consumers cautious with their discretionary spending.

Europe

The Europe region captured 18.90% of the global market in 2025, generating USD 10.16 billion in revenue, and is expected to reach USD 10.71 billion in 2026. Europe is expected to grow with a slow and steady CAGR, as it already has significant presence of smart TVs, streaming devices, and home automation. The UK market is projected to reach USD 2.94 billion by 2026, while the Germany market is projected to reach USD 1.86 billion by 2026.

With high penetration rates leaving comparatively less room for high growth, the market in Europe is developing and mature, as consumers want to retain their investments in established digital ecosystems and have a dependable infrastructure for quality broadband connectivity in most of European countries. For instance,

- According to ABB, the U.K.’s smart home penetration will rise from 20.5% (6.6 million households) in 2024 to 50.2% (approximately 16.5 million households) by 2027.

A steady demand will remain, as families continue acquiring new devices for their beneficial features, energy efficiency, and ability to integrate with existing smart home products seamlessly.

Middle East & Africa

The Middle East & Africa are seeing constant growth in the market due to increased digital awareness, urbanization, and investment to build smart infrastructure. The Middle East & Africa market accounted for USD 5.89 billion in 2025, representing 11.00% of the global industry, and is expected to reach USD 6.3 billion in 2026.

Countries across the region are increasing the availability of broadband networks and are introducing 5G networks, which have created a growing base for connected devices. A young population with digital awareness is enhancing interest in smart TVs, voice assistants, and streaming platforms, especially in urban areas. Recent innovations in the region regarding smart home experiences also support this trend. For instance

- In October 2024, e& UAE revealed the region’s first AI-powered Smart Home experience at GITEX GLOBAL 2024 in Dubai. The system uses AI to learn users’ moods, routines, and health, automatically adjusting lighting, ambiance, and aromatherapy to create a personalized living environment. Featuring over 80 smart devices across interactive zones, the showcase highlights how AI transforms homes into intuitive, adaptive spaces that enhance comfort, safety, and daily life.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 15.41 billion in 2025, accounting for 28.70% share, and is expected to reach USD 16.47 billion in 2026. The Asia Pacific market is expected to grow with the highest CAGR, primarily due to rising disposable income, population growth, faster urbanization, and the rapidly growing internet penetration in countries such as China, India, and Southeast Asia. The Japan market is projected to reach USD 2.9 billion by 2026, the China market is projected to reach USD 6.7 billion by 2026, and the India market is projected to reach USD 2.34 billion by 2026. For instance,

- According to World Population Review, in 2024, China had the highest number of internet users, boasting 1.1 billion, which accounts for 77.3% of its population. India follows closely with 881.3 million internet users, representing 62.6% of its population.

Additionally, due to new local tech manufacturers developing innovative connected devices that are more affordable and intended for cost-conscious consumers, and the impact of numerous government initiatives to support their smart city and digital transformation projects, there is a growing interest and demand for smart living rooms. For instance,

- In February 2025, China’s AI startup DeepSeek plans to expand its technology into household appliances, partnering with major manufacturers such as Haier, Hisense, and TCL. The AI models enhance smart devices with improved voice command accuracy and functionality, such as improved obstacle avoidance in robot vacuums.

Latin America

In 2025, Latin America represented USD 3.28 billion, accounting for 6.10% of the worldwide market, and is projected to grow to USD 3.47 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players are Focusing on Ecosystem Integration, Strategic Partnerships, and Innovative Offerings to Gain a Competitive Edge

Key players in the market are continuously driving innovation by enhancing device interoperability, user experience, and smart home automation capabilities. With the increasing demand for unified entertainment systems and seamless control interfaces, companies are heavily investing in voice-assistant integration, AI-powered recommendations, and multi-device synchronization. ABB, Amazon, Nvidia, Samsung, Google LLC, and Honeywell, among others, are few key players in the market.

Long List of Companies Studied (including but not limited to)

- ABB (Switzerland)

- Amazon.com, Inc. (U.S.)

- Apple Inc. (U.S.)

- Google LLC (U.S.)

- Honeywell International Inc. (U.S.)

- LG Electronics (South Korea)

- Microsoft (U.S.)

- Nvidia Corporation (U.S.)

- Panasonic Corporation (Japan)

- Robert Bosch GmbH (Germany)

- Samsung (South Korea)

- Signify Holdings (Netherlands)

- Sony Corporation (Japan)

…and more

KEY INDUSTRY DEVELOPMENTS

- January 2025: Signify has unveiled new AI-powered innovations for Philips Hue, including a generative AI assistant that creates personalized lighting scenes, and enhanced home security features such as smoke alarm sound detection and improved voice and app controls.

- December 2024: Glance and Airtel Digital TV have launched Glance TV, transforming idle TV screens into AI-powered smart surfaces that display live, personalized content. The platform delivers real-time updates across news, sports, entertainment, and weather when TVs are not in active use. It is currently available in English on Airtel Xstream devices. It has rolled out on over 1 million devices in India, with plans to expand to 4 million by June 2025 before entering global markets.

- September 2024: Samsung has launched its 2024 premium Smart TV lineup in India, featuring Neo QLED 8K, Neo QLED 4K, and OLED models with advanced AI features for personalized viewing. Aimed at premium buyers, these TVs offer AI-driven picture and sound enhancements, security via Samsung Knox, and smart home integration.

- September 2024: ABB India has launched ABB-free@home, a wireless smart home automation system offering seamless integration with platforms such as Apple HomeKit, Google Home, Amazon Alexa, and Samsung SmartThings. It connects with devices from brands such as Philips Hue, Miele, and Sonos, allowing centralized control of lighting, HVAC, appliances, and more.

- August 2024: Samsung launched The Premiere 9 and The Premiere 7 ultra-short throw projectors, featuring advanced laser technology for stunning 4K resolution up to 130 inches. Both models offer high brightness (3,450 and 2,500 ISO lumens), HDR10+ support, AI enhancements, and built-in Dolby Atmos speaker.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investors in the connected living market can anticipate attractive growth potential as consumer demand rises for seamless, smart home experiences. With the increasing adoption of smart TVs, voice-controlled devices, home automation hubs, and streaming platforms, the market offers lucrative opportunities for companies developing integrated ecosystems that enhance convenience and personalization.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on key aspects such as leading companies, product/service types, and leading product applications. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.2% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type

By Connectivity Type

By Application

By End-user

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach USD 106.47 billion by 2034.

In 2025, the market was valued at USD 53.68 billion.

The market is projected to grow at a CAGR of 8.2% during the forecast period.

The individual households are expected to hold the highest share.

Rising smart home adoption to drive the market growth.

ABB, Amazon, Nvidia, Samsung, Google LLC, and Honeywell are the top players in the market.

North America is expected to hold the highest market share.

By product type, connected security systems are expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us