Containerboard Market Size, Share & Industry Analysis, By Material (Virgin and Recycled), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Industrial, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

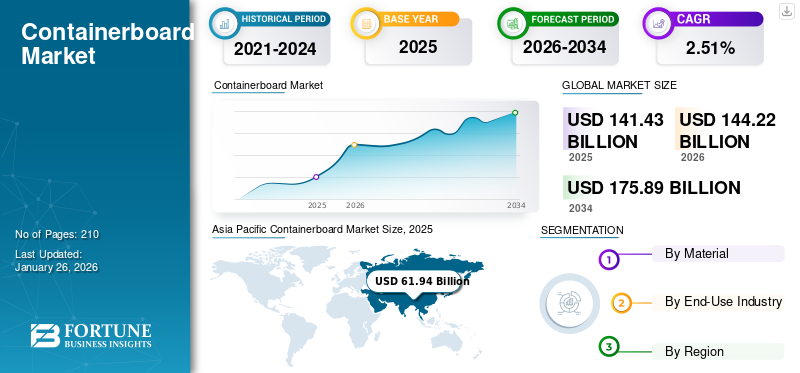

The global containerboard market size was valued at USD 141.43 billion in 2025. It is projected to be worth USD 144.22 billion in 2026 and reach USD 175.89 billion by 2034, exhibiting a CAGR of 2.51% during the forecast period. Asia Pacific dominated the containerboard market with a market share of 43.80% in 2025.

Containerboard is a type of paperboard composed of linerboard and corrugated medium that provides strength and durability to corrugated boxes. It is widely used across various industries, including food & beverage, electronics, e-commerce, pharmaceutical, and retail, due to its lightweight nature, cost-effectiveness, recyclability, and versatility. The containerboard market includes production, distribution, and utilization of containerboard materials, which are primarily used in the manufacturing of corrugated packaging products.

International Paper and Mondi Group are the leading product manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

Containerboard Market KEY TAKEAWAYS

- 2025 Market Size: USD 141.43 billion

- 2026 Market Size: USD 144.22 billion

- 2034 Forecast Market Size: USD 175.89 billion

- CAGR: 2.51% from 2026–2034

- Asia Pacific dominated the containerboard market with a 43.80% share in 2025.

- Recycled segment accounted for the largest market share in 2026.

- Food & beverage end-use segment is projected to hold a 49.72% share in 2026.

Asia Pacific

Asia Pacific reached USD 61.94 billion in 2025, driven by rapid urbanization, e-commerce expansion, and strong containerboard production in China.

North America

North America accounted for USD 26.66 billion in 2025, supported by sustainable packaging initiatives and high demand from the retail and food industries.

Europe

Europe accounted for 20.59% of the global market in 2025, driven by biodegradable packaging innovations and stringent recycling regulations.

U.S.

The market is projected to reach USD 23.53 billion by 2026, fueled by strong containerboard production and growing demand for recyclable packaging.

Japan

The market is projected to reach USD 11.26 billion by 2026, supported by rising demand for sustainable packaging and advanced paper manufacturing.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rise in E-Commerce Trends and Increased Focus on Sustainability to Foster Market Growth

The rapid expansion of e-commerce has significantly boosted the global containerboard market growth. With online shopping stores becoming a primary retail channel, there is a heightened need for sturdy and lightweight packaging solutions for shipping. Containerboards, particularly corrugated boxes, are favored for their ability to protect products during transit and their customizability for branding purposes. Sustainability has become a major driver in the market as consumers and governments push for eco-friendly packaging solutions. Containerboards are primarily made from recycled fibers and renewable resources, aligning with global efforts to reduce plastic waste.

For instance, according to a study published in the Confederation of European Paper Industries, the total paper production in 2022 reached 84.8 million tons. A notable decrease was reported in almost all paper and paperboard grades, with the exception of household and sanitary grades.

Technological Advancements in Containerboard Production to Drive Market Growth

Innovations in containerboard manufacturing, such as the use of lightweight and high-strength materials, have further fueled market growth. Modern production techniques allow for improved durability, reduced material usage, and enhanced recyclability, making these boards more appealing to businesses seeking cost-effective and sustainable solutions. Digital printing technologies have also enabled better customization, which is vital for branding and marketing, further boosting the product’s appeal to industries.

MARKET RESTRAINTS

Volatility in Raw Material Prices to Hamper Market Growth

The market is highly dependent on the availability and cost of raw materials, such as virgin wood pulp and recycled paper. Fluctuations in raw material prices, driven by factors, such as global supply chain disruptions, trade restrictions, and environmental regulations, create significant cost pressures for manufacturers. Additionally, increased demand for sustainable packaging has intensified the competition for high-quality recycled fiber, further driving up costs. This price volatility often reduces profit margins and poses challenges for maintaining stable pricing structures in the market.

MARKET OPPORTUNITIES

Rising Industrialization and Urbanization in Emerging Economies Will Generate Market Growth Opportunities

Rising industrialization and urbanization in emerging economies, particularly in Asia Pacific, Latin America, and Africa, are driving the containerboard demand. These regions are witnessing increased investments in manufacturing and retail sectors, necessitating the use of high-quality packaging materials. Additionally, the growth of organized retail and food & beverage sectors in these markets is creating new avenues for the use of containerboards. Manufacturers can capitalize on this trend by establishing localized production facilities and supply chains to meet region-specific needs.

MARKET CHALLENGES

Intense Competition and Market Fragmentation to Challenge Market Growth

The market is highly competitive and fragmented, with numerous regional and global players. This intense competition puts pressure on profit margins, especially for manufacturers operating in price-sensitive markets. Additionally, as e-commerce continues to grow, packaging requirements are evolving, prompting companies to innovate continuously, which can be resource-intensive.

Download Free sample to learn more about this report.

CONTAINERBOARD MARKET TRENDS

Increasing Demand for Sustainable Packaging Solutions to Emerge as a Key Trend

Manufacturers of cosmetics, personal care, electronics, food & beverages, and others prefer eco-friendly packaging solutions as they help them reduce their packaging waste. Corrugated boxes offer versatile, lightweight, high grammage, and durable characteristics, which make them the preferred choice for making packaging solutions. They are considered a sustainable form of packaging as they are made from recycled materials. The production of corrugated boxes from recycled materials helps manufacturers reduce environmental impact, thereby abiding by the industrial standards and regulations of the governments to protect the environment.

Regulations by governments and associations have led several manufacturers to add sustainable container boards to their portfolios. In May 2020, Cascades introduced a new line of packaging products for e-commerce. In the product line, the company added corrugated boxes as a sustainable packaging solution for companies that sell their products online. The increasing adoption of eco-friendly products, the rapid expansion of the e-commerce industry, and rising technological innovations will also fuel the adoption of container boards. Hence, these factors will cause the market to flourish during the forecast timeframe.

IMPACT OF COVID-19

The COVID-19 Pandemic Caused Slowdown in Manufacturing Activities

The COVID-19 pandemic had a negative impact on a variety of industries across the globe, especially the packaging industry. Corrugated box manufacturers were offering environment-friendly, reusable, and biodegradable packaging made using containerboard. However, concerns about the hygiene and safety of reusable packaging put a temporary halt to the packaging industry's progress toward a circular and sustainable supply chain.

The pandemic also caused a spike in internet ordering, resulting in an increased need for corrugated packaging. Supply networks encountered various challenges as a result of the increasing demand. A demand-supply imbalance influenced global transportation logistics in container flows.

RESEARCH AND DEVELOPMENT

Research and development in lightweight containerboards have gained momentum as manufacturers seek to reduce material usage while maintaining strength and durability. Innovations focus on optimizing fiber composition and layering techniques to create high-performance container boards with reduced weight. This decreases transportation costs and aligns with the sustainability goals of reducing carbon footprints. Companies are exploring advanced papermaking technologies, such as chemical additives and refining processes to enhance the strength-to-weight ratio of containerboards without compromising on their functionality.

SEGMENTATION ANALYSIS

By Material

Recycled Segment Leads Market Due to Rise in Environmental Awareness

Based on material, the market is segmented into virgin and recycled.

The recycled is the dominating segment is expected to account for 73.80% of the market in 2026. Recycled containerboard is considered more sustainable as it reduces the need for virgin fibers, which involves deforestation and higher carbon emissions during production. As global environmental concerns rise, consumers and companies alike are prioritizing recyclable and eco-friendly packaging options. Many regions are setting ambitious recycling targets. For instance, the U.S. Environmental Protection Agency (EPA) has set a goal of increasing recycling rates for paper products, encouraging the use of recycled paper in packaging, including containerboard.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Food & Beverage Segment Dominates Market Owing to Widespread Usage of Containerboards

Based on the end-use industry, the market is segmented into food & beverages, personal care & cosmetics, industrial, and others.

The food & beverage end-use industry takes the lead in the market as containerboard offers robust protection for a variety of food items, from dry goods to perishables, while maintaining the required hygiene standards, expected to contributing 49.72% globally in 2026. Its ability to withstand moisture, physical stress, and rough handling during transportation makes it ideal for food packaging. Moreover, the increasing consumer preference for sustainable, recyclable, and biodegradable packaging materials aligns with containerboard’s eco-friendly attributes, particularly as food brands seek to reduce their environmental footprint. Containerboard is also used to package fresh fruits and vegetables that need to travel long distances. The growing utilization of the packaging of frozen foods, fresh produce, ready-to-eat foods, and canned products thus enhances segmental growth.

CONTAINERBOARD MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Containerboard Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Increased Urbanization to Support Market Growth in Asia Pacific

Asia Pacific

Asia Pacific contributed approximately USD 61.94 billion to the global market in 2025, accounting for 43.80% share, and is expected to reach USD 63.35 billion in 2026. Asia Pacific is expected to exhibit the fastest growth in the global market, with China, Japan, and India being the largest markets. Rapid urbanization and expansion of e-commerce in India and Southeast Asia are contributing to the surge in demand for containerboards. The Japan market is projected to reach USD 11.26 billion by 2026, the China market is projected to reach USD 22.08 billion by 2026, and the India market is projected to reach USD 15.65 billion by 2026.

- The China National Paper Industry Association reported that China alone produced over 70 million tons of containerboard in 2023, making it the largest global producer and consumer of corrugated packaging.

Rising Preference for Sustainable Packaging Solutions Drives Market Growth in North America

North America

In 2025, North America held 18.85% of the global market share, reaching a valuation of USD 26.66 billion, and is projected to grow to USD 27.16 billion in 2026. North American governments are increasingly emphasizing sustainable packaging. In 2022, the U.S. Federal Packaging Recycling Act was proposed to reduce plastic waste and promote recycling, which will benefit the market as corrugated packaging is 100% recyclable. Canada’s Zero Plastic Waste Strategy aligns with the push for more sustainable and eco-friendly packaging, encouraging the adoption of containerboard due to its recyclable and biodegradable properties. The U.S. market is projected to reach USD 23.53 billion by 2026.

- According to the American Forest & Paper Association (AF&PA), containerboard production in the U.S. alone reached 31.5 million tons in 2023, with the industry growing at an annual rate of about 2% over the last five years. The U.S. is the largest producer of containerboard globally, driven by extensive packaging requirements in retail, food, and beverage sectors.

Advancements in Biodegradable Coatings to Enhance Market Growth in Europe

Europe

The market in Europe reached USD 29.12 billion in 2025, representing 20.59% of total market revenue, and is projected to reach USD 29.72 billion in 2026. Europe is the second-largest region and is expected to grow rapidly in the coming years. The regional market is witnessing innovations in biodegradable coatings and sustainable packaging solutions as manufacturers respond to the growing consumer demand for green products. The UK market is projected to reach USD 3.44 billion by 2026, while the Germany market is projected to reach USD 6.65 billion by 2026.

- The European Union’s Circular Economy Action Plan, which emphasizes reducing the environmental impact of packaging, has been a major driver for the market. The EU has set ambitious recycling targets, aiming for a 90% recycling rate for paper and cardboard by 2025. This regulatory push will directly benefit the market as it aligns with the shift toward recyclable packaging materials.

Regulations and Sustainability Efforts Will Encourage Steady Market Growth in Latin America

Latin America

In 2025, Latin America generated USD 12.3 billion, contributing 8.69% to global market revenue, and is projected to grow to USD 12.48 billion in 2026. The market in Latin America is witnessing a shift toward more sustainable practices, with local manufacturers adopting more environmentally friendly production techniques and increasing the use of recycled fibers in containerboard production.

- Brazil’s National Policy on Solid Waste (PNRS), which encourages recycling and the use of recyclable packaging, has helped drive demand for corrugated packaging. The policy promotes a shift from plastic to paper-based materials such as containerboard.

Growing Regulations and Sustainability Efforts are Driving Market Growth in the Middle East

Middle East & Africa

The Middle East & Africa region captured 8.07% of the global market in 2025, generating USD 11.42 billion in revenue, and is projected to reach USD 11.51 billion in 2026. The Middle East & Africa region has a relatively small but growing market, primarily driven by countries, such as Turkey, South Africa, and UAE.

- In UAE, government regulations are focusing on increasing recycling rates and reducing plastic waste. The UAE’s Zero Waste Strategy is pushing industries to adopt more sustainable packaging, including containerboard.

FUTURE OUTLOOK & INVESTMENTS

The containerboard market is seeing strategic mergers and acquisitions as companies aim to strengthen their market position and expand their product offerings. Notable acquisitions, such as Smurfit Kappa’s acquisition of Papeteries de Genval in 2020, reflect companies’ drive toward consolidating their production capabilities and entering new markets. These deals are often aimed at securing a larger share of the sustainable packaging market or tapping into emerging regional markets, such as Asia Pacific and Latin America.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The global market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These players are constantly focusing on expanding their customer base across regions by innovating their existing range of products. The report also highlights the key developments by manufacturers.

Major players in the industry include International Paper, Mondi Group, SCG Packaging Public Company Limited, DS Smith, Lee & Man Paper Manufacturing Ltd., Smurfit Kappa, and others. Numerous other companies operating in the market are focused on delivering advanced packaging solutions.

List of the Key Containerboard Companies Profiled in the Report:

- International Paper (U.S.)

- SCG PACKAGING PUBLIC COMPANY LIMITED (Thailand)

- DS Smith (U.K.)

- Lee & Man Paper Manufacturing Ltd. (China)

- Smurfit Kappa (Ireland)

- Mondi Group (U.K.)

- Oji Fibre Solutions (NZ) Ltd. (Australia)

- WestRock Company (U.S.)

- Rengo Co., Ltd. (Japan)

- Georgia-Pacic LLC (U.S.)

- Hamburger Containerboard (Austria)

- Nine Dragons Paper (Holdings) Limited (Hong Kong)

- Stora Enso (Finland)

KEY INDUSTRY DEVELOPMENTS

- January 2024 – WestRock Company announced plans to build a new corrugated box plant in Pleasant Prairie, Wisconsin, to meet the growing demand from customers in the Great Lakes region. The company intends to close its existing plant in North Chicago when construction of the new facility is completed.

- May 2023 - Smurfit Kappa completed its latest investment project in Poland, resulting in a significant expansion of its Pruszków corrugated plant. The expansion made the plant Smurfit Kappa’s largest in Poland and one of the most high-tech and modern packaging plants in Europe.

- January 2023 – Mondi Plc completed the acquisition of the Duino mill from the Burgo Group near Trieste (Italy) for a total consideration of USD 43.29 million. The mill operated on one paper machine that produces lightweight coated mechanical paper. Mondi planned to convert the paper machine to produce around 420,000 tons of high-quality recycled containerboard annually. This acquisition will help Mondi Group invest in the growth of the packaging business, build an integrated platform, and broaden its geographic reach.

- October 2022 - Middle East Paper Co (MEPCO) announced that it would invest USD 400 million in a paper or containerboard packaging plant in the U.K. The plant, after completion, will have an annual production capacity of 400,000 tons and serve both local and global markets. The plant will also help MEPCO increase its production capacity and expand its consumer base in different and new markets globally.

- September 2022 - Stora Enso announced the acquisition of De Jong Packaging Group, a Netherlands-based containerboard mill, for a price of USD 1.04 billion. De Jong manufactures corrugated trays and boxes mainly for e-commerce, fresh produce, and industrial purposes. This acquisition was expected to help Stora Enso advance its strategic directions, thereby increasing revenue and building market share in the renewable packaging sector in Europe.

- September 2021 - Rengo Co., Ltd. announced that Vina Kraft Paper Co., Ltd., its joint venture in Vietnam, had decided to construct a new production base for containerboards. With the newly constructed mill, Vina Kraft Paper will firmly establish its position as a leader in the Vietnam containerboard market and aim for sustainable growth and development.

REPORT COVERAGE

The report provides a detailed market analysis. The market overview also focuses on key aspects, such as top key players, competitive landscape, product/service types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.51% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 141.43 billion in 2025.

The market is likely to record a CAGR of 2.51% over the forecast period.

The recycled material segment leads the market.

The Asia Pacific market value stood at USD 60.65 billion in 2025.

The key market drivers are the rising demand for e-commerce and increased focus on sustainability.

Some of the top players in the market are International Paper, Mondi Group, SCG Packaging Public Company Limited, DS Smith, Lee & Man Paper Manufacturing Ltd., Smurfit Kappa, and others.

The global market size is expected to reach a valuation of USD 175.89 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us