Cooking Wine Market Size, Share & Industry Analysis, By Type (Rice Cooking Wine, Grape-based Cooking Wine, Fortified Wine and Others), By Nature (Conventional and Organic), By End Use (Food Processing, Food Service and Retail), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

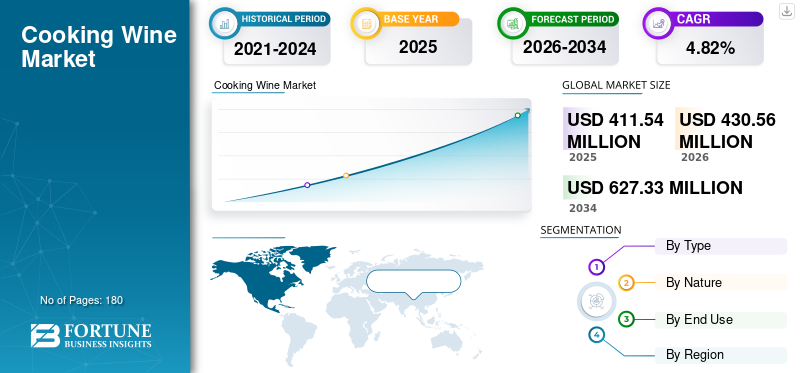

Cooking Wine Market Size and Future Outlook

The global cooking wine market size was valued at USD 411.54 million in 2025. The market is projected to grow from USD 430.56 million in 2026 to USD 627.33 million by 2034, exhibiting a CAGR of 4.82% during the forecast period. Europe dominated the global cooking wine market with a market share of 35.93% in 2025.

Cooking wine is a specialized liquid ingredient formulated to improve the aroma and flavor of several dishes across global cuisines. Unlike table wine, culinary wine is specifically produced for cooking applications, providing consistent flavor intensity and balanced acidity through controlled salt content and alcohol levels. Its flavor varies from caramelized to fruity, mainly depending on the type of wine. Rice wine, fortified wine (sherry wine), red wine, and white wine are a few popular types of cooking wine. For culinary purposes, this wine is used in sauces, marinades, gravies, and for tenderizing meat. Moreover, it is used for preparing stews, soups, and poaching fruit. Similar to other wines, this cooking wine has a longer shelf life and is preserved with additional salt content. Based on consumption, Europe and North America are leading markets globally.

The rising awareness of dessert wine, along with the increasing number of home cooks, are key factors that boost the market for cooking wines. Few prominent players are AAK AB, Goya Foods, Roland Foods, and others.

Download Free sample to learn more about this report.

Cooking Wine Market KEY TAKEAWAYS

- 2025 Market Size: USD 411.54 million

- 2026 Market Size: USD 430.56 million

- 2034 Forecast Market Size: USD 627.33 million

- CAGR: 4.82% from 2026–2034

- Europe dominated the cooking wine market with a 35.93% share in 2025.

- Grape-based cooking wine was the leading type segment in 2025.

- The conventional segment accounted for the largest market share in 2025.

Europe

Europe led the global market in 2025, supported by growing demand for gourmet home cooking and international cuisines.

Asia Pacific

North America held the second-largest market position and is projected to grow at a CAGR of 4.02% during the forecast period.

Asia Pacific

Asia Pacific ranked third in 2025, driven by fusion cooking trends and expanding e-commerce channels.

U.S.

U.S. The market is supported by rising home cooking trends, meal-kit services, and a strong presence of wine producers.

Japan

Japan Growing interest in premium culinary ingredients and international cuisine is expected to support market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growth in Packaged Food Industry Fuels Demand for Culinary Wine

The processed food industry is one of the largest drivers, contributing to increased demand for cooking wine. These wines are widely utilized in industrial formulations such as stir-fry sauces, marinades, gravies, dumpling fillings and frozen dishes. The majority of food manufacturers depend on culinary wine not solely for flavor enhancement, but also for its other advantages, such as flavor stability, aroma development, and tenderization, especially during high-heat processing. Moreover, as the consumption of quick meals rises worldwide, particularly in North America, the Asia Pacific, and Europe, food processors are incorporating wines into product portfolio. Additionally, the rising inclination toward fusion and international cuisines further supports the usage of wine. By keeping this in view, the producers aim to introduce new, flavorful cooking wines that can be used in a variety of cuisines.

MARKET RESTRAINTS:

Raw Material Cost Fluctuations and Limited Household Adoption Impede Market Growth

One of the major obstacles in the industry is fluctuations in raw material prices. Globally, culinary wines depend on agricultural inputs such as rice, grapes, and grains. Unpredictable harvest conditions, supply chain disruption, and climate change can substantially impact the pricing and availability of these components. For instance, rice export bans and grape crop shortages can fuel manufacturing costs, minimize margins, and restrict producers' ability to scale their production. Moreover, import-dependent countries face extra difficulties when logistics delays and exchange rate variations affect procurement. As a result, these factors make it difficult for wine producers to maintain consistent product development and stable price structures.

Limited household adoption is another obstacle in the market. Most of the individuals are unaware of the importance of wine in enhancing aroma/flavor, and are accustomed to using stock or spice blends instead of culinary wine. Thus, the above factor further impedes the global cooking wine market share.

MARKET OPPORTUNITIES:

Technological Advancements in the Wine Market Open Growth Opportunities

The adoption of innovative technologies in the wine industry opens various growth prospects. To enhance sensory qualities, producers can utilize non-thermal technologies, such as high hydrostatic pressure, pulsed electric fields, and ultraviolet radiation. Crossflow microfiltration is another technique gaining significant popularity, used to clarify wine without modifying its ingredients.

Moreover, genetic engineering and biotechnology are being employed by companies, which aid in controlling pH and minimizing alcohol content. Additionally, wine producers are exploring alternative technologies to reduce/replace the requirement for sulfur dioxide content. Additionally, smart fermentation tanks are also used in wine preparation industry, assuring quality and consistency.

COOKING WINE MARKET TRENDS:

Rising Inclination Toward Alcohol-Free Wine is Ongoing Trend

The market is experiencing a surge and remarkable trend of alcohol-free wine. In today’s era, majority of consumers, especially those with religious/cultural restrictions, are looking for premium-quality wines that are alcohol-free. Producers are launching culinary wines that offer a similar flavor without using alcohol, which is often achieved by removing ethanol/denaturing during production. These end products allow the HoReCa sector, particularly in restrictive markets, to use alcohol-free wine without violating regulations. Moreover, this trend is expanding in Western countries, where teetotalers and health-centric consumers are seeking substitutes that provide depth and acidity of wine without utilizing alcohol.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Grape-based Cooking Wine Led the Market Owing to Its Neutral Flavor Profile

On the basis of type, the market is divided into rice cooking wine, grape-based cooking wine, fortified cooking wine, and others. The grape-based cooking wine dominated the global market in 2025. This wine is one of the most popular culinary wines, ideal for a range of dishes across Mediterranean, Latin American, and Western cuisines. Moreover, its natural acidity makes it appropriate for marinades and tenderizing meats. Additionally, its improved accessibility and global availability further strengthening its utilization. In addition, it can be used for gourmet cooking and is effective for deglazing.

The rice cooking wine segment is predicted to grow at a high CAGR of 6.82% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Nature

Predictable Category Dominated Market Due to Its Cost-Effectiveness

Based on nature, the industry is distributed into conventional and organic. The conventional segment leads the market in 2025.

When compared to organic wines, traditional wines are more widely available across the retail channel, fulfilling the mass-market demand. Moreover, it is economical for both consumers and foodservice, who purchase bulk quantities. Additionally, conventional wine is easily available in numerous formulations, such as fortified, herb-infused, and red or white, further appealing to the global population. Additionally, it has a longer shelf life and better stability as similar to organic wines. Thus, such instances support the growth of global market.

The organic segment is probable to grow at a high CAGR of 6.89% over the forecast period.

By End Use

Food Processing Leads the Industry Due to High Usage of Wine Via Bulk Purchasing

On the basis of end use, the market is divided into food processing, food service, and retail. The food processing segment dominated the market in 2025. Globally, food processing firms purchase culinary wines in larger volumes than households/restaurants, as they are utilized as a functional component in mass-produced ready meals, marinades, and seasonings. Moreover, the food processing sector has a reliable demand compared to the foodservice sector, which varies with dining preferences and tourism cycles. Primarily, culinary wine is used in a range of packaged food categories, including ramen, broth, pasta sauces and frozen entrees. Thus, the above-mentioned factors propel the segment’s growth.

The foodservice segment is predicted to grow at a CAGR of 4.39% over the study timeframe.

Cooking Wine Market Regional Outlook

Based on regions, the industry is divided into South America, Europe, North America, Asia Pacific, and Middle East & Africa.

Europe Cooking Wine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

Europe cooking wine market dominated and held the largest share in 2025. This growth is backed by rising influence of international cuisines and a surging preference for convenient gourmet cooking. Currently, most consumers are increasingly looking for restaurant-style flavors at home, fueling the use of wine in daily meal preparation, especially for sauces and stews. Moreover, the increasing adoption of Asian, Mediterranean, and Western dishes supports the utilization of grape-based, rice-based and fortified culinary wines. Moreover, the growing processed food industry, specifically the ready meals and frozen dishes sector, boosts the acceptance of wine as a flavor enhancer. In addition, the wide availability of low-sodium and organic wines, as well as premiumization trends, are other crucial factors that are strengthening the region’s momentum.

Asia Pacific and North America

Other regions, including the Asia Pacific and North America, are expected to experience significant surge in the future. During the forecast period, North America is anticipated to record a growth rate of 4.02%, and is the second-highest region globally. The growing inclination toward home cooking, combined with the presence of well-known wine producers, enhances the North America cooking wine market. Among all the American countries, the U.S. leads in the region, followed by Mexico and Canada. The rapidly growing meal-kit services and foodservice outlets are encouraging the nation’s thrust. After North America, the Asia Pacific cooking wine market placed third in the industry in 2025. The rising trend of fusion cooking, combined with a robust e-commerce network, bolsters the region’s growth.

South America and the Middle East & Africa

South America and the Middle East & Africa are projected to witness modest growth in the near term. The launch of new products and increasing awareness of culinary wine drive market expansion.

COMPETITIVE LANDSCAPE

Major Industry Player

Key Players in Market Are Directing on New Launches to Advance Their Market Position

Key players in the market include AAK AB, Roland Foods, and Goya Foods. All players operating in the global market are aiming to launch products that cater to the rising consumer needs. Through such launches, the firms can improve their brand image in the market.

List of Key Cooking Wine Companies Profiled:

- AAK AB (Sweden)

- Batory Foods, Inc. (U.S.)

- Roland Foods (U.S.)

- Vin Sullivan Foods (U.K.)

- Stratas Foods (U.S.)

- Pagoda brand (China)

- Mizkan America, Inc. (U.S.)

- Goya Foods (U.S.)

- Kuaijishan Shaoxing Wine Co. (China)

- Takara Shuzo Co. (Japan)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: The Wine Group LLC, a California-based wine producer that also sells wine suitable for cooking, acquired various wine brands and manufacturing facilities from Constellation Brands, a U.S.-based alcohol producer.

- October 2024: AAK AB, a Swedish manufacturer of cooking wine and vegetable oil, announced the sale of its foodservice facility based in New Jersey to Stratas Foods, an American supplier of dressings.

- July 2024: Knorr, a brand of Unilever plc, a British consumer packaged goods firm, introduced white and red wine-flavored stock pots, which can be used to enhance the flavor of dishes.

REPORT COVERAGES

The global cooking wine market report includes quantitative and qualitative insights into the market. It also offers a detailed market analysis of sizing and growth rate for all possible market segments. Various key insights presented in the market research report are an overview of related markets, competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory scenario in critical countries, and global market trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) |

|

Growth Rate |

CAGR of 4.82% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Nature

|

|

|

By End Use

|

|

|

By Geography North America (By Type, Nature, End Use, and Country)

Europe (By Type, Nature, End Use, and Country)

Asia Pacific (By Type, Nature, End Use, and Country)

South America (By Type, Nature, End Use, and Country)

Middle East & Africa (By Type, Nature, End Use, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 411.54 million in 2025.

The market is expected to grow at a CAGR of 4.82% during the global market forecast period (2026-2034).

By nature, the conventional segment led the market.

Growth in the packaged food industry fuels demand for culinary wine.

AAK AB, Roland Foods, and Goya Foods are among the top players in the market.

Europe held the highest share of the market.

Technological Advancements in the Wine Market Open Growth Opportunities.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us