Core Materials Market Size, Share Industry Analysis, By Type (Foam, Honeycomb, and Balsa), By Application (Marine, Automotive, Aerospace, Energy, Construction, and Industrial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

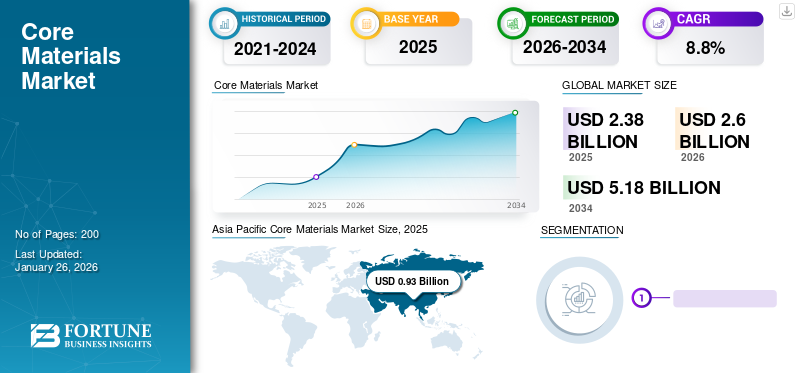

The global core materials market size was valued at USD 2.38 billion in 2025 and is projected to grow from USD 2.6 billion in 2026 to USD 5.18 billion by 2034, exhibiting a CAGR of 8.8% during the forecast period. Asia Pacific dominated the core materials market with a market share of 39.00% in 2025. Moreover, the core materials market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 990.6 million by 2032, driven by boost in the aerospace industry, as the product is highly utilized in flight vehicles, Unscrewed Air Vehicles (UAVs), and airships due to its unique specifications, such as high strength, great flexibility, minimal maintenance, radar transparency, and low thermal conductivity.

Core or structural materials are lightweight and utilize high-strength materials to produce high-strength-to-weight ratio structures in end-use applications. These materials are usually made of engineering items, including foam, wood, or paper, and are used as the primary component in sandwich panel construction. These sandwich panels are key structural materials for boats, ships, aircraft, wind turbines, and others. Therefore, the core material is highly utilized in various applications, including marine, automotive, energy, construction, and industrial, in foam, honeycomb, and balsa, as this material offers excellent sound insulation, enhanced conductivity, and optimal fire resistance.

These materials are widely utilized in engineering structures of different designs as they offer massive energy absorption, stiffness, and impact resistance. The core materials market growth is associated with its comprehensive utilization in various industries such as marine, aerospace, and others. Designers in these industries typically focus on the structural properties required in end-use applications. For instance, honeycomb core material is usually utilized in marine and aerospace applications as the product offers a good strength-to-weight ratio and provides optimum spacing between the two skins of the sandwich structure.

COVID-19 broke out in 2019 and hit nearly every country in the world. The production of core materials was halted or decreased due to fluctuations in the supply chain. This resulted in limited production and low demand for the product. Additionally, the manufacturers and suppliers of the product had to face low demand for the product as the end-use industries were operating at the lowest production capacities. Countries such as the U.S., India, and China had to impose restrictions on the movement of men and transportation, which led to the profound loss of this industry.

Download Free sample to learn more about this report.

Core Materials Market Key Takeaways

- 2025 Market Size: USD 2.38 billion

- 2026 Market Size: USD 2.60 billion

- 2034 Forecast Market Size: USD 5.18 billion

- CAGR: 8.80% from 2026–2034

- Asia Pacific dominated the market with a 39.00% share in 2025.

- Foam segment is projected to hold the largest market share with 53.85% in 2026.

- Automotive segment is projected to account for 58.08% of the global market share in 2026.

North America

The market reached USD 0.66 billion in 2025, driven by strong demand from the aerospace industry.

Asia Pacific

The market reached USD 0.93 billion in 2025, accounting for 39.00% of global revenue.

Europe

The market reached USD 0.56 billion in 2025, supported by rising automotive demand and high consumer spending.

U.S.

The market is projected to reach USD 990.6 million by 2032.

Japan

The market is projected to reach USD 0.20 billion by 2026.

Read More

Core Materials Market Trends

Rising Demand for PET and PVC-based Memory Foams Core Material to Surge Demand

The demand for memory-based foam materials increased in the end-use industries over the past few years. This memory foam is commonly used in car seats, spray foam, and others. Thus, the rising demand for memory foam has become popular, creating a massive opportunity for the existing and new producers of these foam products to establish their presence in the global market. Furthermore, foam materials are gaining momentum in industrial applications owing to their excellent characteristics. Additionally, the increasing population in countries, such as Germany and Japan, has created a demand for memory foam-based seats and panels as they relieve physical stress when used in car and automotive seating.

Download Free sample to learn more about this report.

Core Materials Market Growth Factors

Growth in the Aerospace Industry is Propelling Demand for Core Materials

The growth of the market is associated with the boost in the aerospace industry, as the product is highly utilized in flight vehicles, Unscrewed Air Vehicles (UAVs), and airships due to its unique specifications, such as high strength, great flexibility, minimal maintenance, radar transparency, and low thermal conductivity. The most commonly used materials are open and closed-structured foams such as polystyrene, polyurethane, polyvinyl chloride, honeycombs, and balsa wood. Additionally, these materials are utilized in structural manufacturing methods such as infusion, wet lamination, prepreg, RTM, press bonding, and vacuum bagging, making the material more adaptable for the aerospace industry. For instance, flight control surfaces, landing gear doors, interior components, floor beams, and floorboards are made using these manufacturing methods. Furthermore, different materials are utilized to give the desired sandwich structure with additional features, including FST insulation or resistance in the aerospace industry.

Despite the materials’ excellent flexibility, weight reduction is a significant factor in the aerospace industry. These lightweight materials may increase profitability with a massive increase in fuel efficiency. Therefore, the structural components made of materials are being highly consumed in the aerospace industry to reduce weight. Additionally, these materials offer design flexibility, ensuring modification in the case of maintenance. Thus, using materials in the aerospace component will spur market growth in the forecast period.

Growing Marine Industry to Propel the Demand for Core Materials

Over the past few years, international trade has increased between the nations. Industries such as steel and aluminium have a strong presence in India owing to the presence of key manufacturers such as Tata Steel. All the products from these industries are exported through large ships, which drives the marine industry growth. Honeycomb is the material used in ships ranging from small to large owing to its structural properties. The utilization of the honeycomb structure made from steel, iron, and aluminium makes the ships lighter and stronger. Additionally, core materials such as foam and balsa wood are the light materials that are used in the manufacturing of seats, chairs, and floors on the ship. Thus, increasing international trade and the expanding marine industry are propelling the demand for core materials.

RESTRAINING FACTORS

Rising Concerns for Sustainable Production of Core Materials to Restrict Market Growth

Demand for these materials is high in the end-use industries, but environmental concerns and the increased demand for sustainable production may hamper market growth. Industries such as marine, aerospace, automotive, energy, construction, and industrial use the sandwich structure, where this material is employed in manufacturing the panels' floors, bulkheads, and hatches. These materials are usually made of PET, PVC, and wood. Many countries, such as the U.K., have imposed rules and regulations on producing these polymers and cutting the wood. Moreover, polymers such as PET and PVC are non-biodegradable and highly regulated in various countries. Therefore, these factors affect the demand for materials and act as a restraint on the market.

Core Materials Market

By Type Analysis

Foam Segment is Expected to Drive the Market Owing to Usage in Automotive Industry

The market is segmented into foam, honeycomb, and balsa on the basis of type. The demand for the foam segment is high due to their massive usage in the automotive and aerospace industries, as foam materials offer remarkable properties at a low weight. The foam materials can be combined with the composite material sheets in the form of a structural sandwich, making it more suitable for the end-use applications as foams have great dimensional density and require minimal maintenance. The sun control film segment is projected to dominate the market with a share of 53.85% in 2026.

Moreover, using honeycomb materials in end-use applications has boosted the demand for the materials market. Honeycombs are made of overexpanded NOMEX aramid and extruded polypropylene, which is most appropriate for boats, ships, traditional aircraft, cars, trucks, and other vehicles as the materials offer reduced weight and greater thermal & chemical resistance than traditional structures.

Meanwhile, the balsa segment is utilized in marine and aerospace applications. Thus, the demand for materials is increasing moderately.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Aerospace Segment to Exhibit Significant Growth Rate Due to Rising Disposable Income

Based on application, the market is segmented into marine, automotive, aerospace, energy, construction, and industrial. The growth of core material is associated with rapid increase in the aerospace industry. For instance, NOMEX honeycomb material contributes to a dominant market share in the aerospace floor panels market as the product enables rigid and durable floor structures. Additionally, increasing demand for memory foam or viscoelastic foam is expected to boost this material demand in the aerospace industry, as the viscoelastic foam offers extensive flexibility at an elevated period in the aircraft' journey. The automotive segment is expected to account for 58.08% of the market in 2026.

Moreover, the marine segment is expected to witness significant growth as the demand for ships, boats, maritime transportation, and the naval industry is high. Materials, such as balsa wood, are highly utilized in these applications' structural design.

These materials are widely utilized in the marine industry in designing the nacelle, hulls, and deck. Thus, using the material in marine applications is expected to boost the segment in the forecast time frame. On the other hand, the core consumption of the materials is high in the construction and industrial segments as the materials are used for insulation.

REGIONAL INSIGHTS

Asia Pacific

Asia Pacific Core Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 0.93 billion to the global market in 2025, accounting for 39.00% share, and is expected to reach USD 1.02 billion in 2026. Asia Pacific held the largest core materials market share and is anticipated to dominate the market during the forecast period. The market growth is associated with high industrial activities in the region, which boosts different sectors. Additionally, countries in the region, such as India and China, have the highest populations. As one of the largest consumers of automotive applications, the demand continues even though there was a downward trend in the industry during the COVID-19 pandemic. This material is one of the key raw materials for producing automotive components. Thus, the market is expected to grow at a high CAGR during the forecast time frame. The Japan market is projected to reach USD 0.2 billion by 2026, the China market is projected to reach USD 0.55 billion by 2026, and the India market is projected to reach USD 0.15 billion by 2026.

North America

In 2025, North America held 28.00% of the global market share, reaching a valuation of USD 0.66 billion, and is projected to grow to USD 0.73 billion in 2026. The demand for core materials in North America is associated with the rapid growth of the aerospace industry. The number of aerospace institutions and key players is high in the region. On the other hand, aerospace R&D activities have increased over the past year in several countries in the region, including the U.S. The U.S. market is projected to reach USD 0.58 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Europe

The market in Europe reached USD 0.56 billion in 2025, representing 24.00% of total market revenue, and is projected to reach USD 0.61 billion in 2026. The market growth in Europe is significant due to the rapid increase in the region's automotive industry. High per capita income and consumer preference for cars and trucks boost major market growth. Additionally, the presence of a few material manufacturers in the region is expected to boost the consumption of materials there. The UK market is projected to reach USD 0.11 billion by 2026, while the Germany market is projected to reach USD 0.27 billion by 2026.

Latin America

In 2025, Latin America generated USD 0.11 billion, contributing 5.00% to global market revenue, and is projected to grow to USD 0.12 billion in 2026. The growth of the market in Latin America is due to increased industrialization. Core materials primarily work as structural materials for various end-use industries due to their stiffness and lightweight. For instance, the demand for core materials in the marine industry is rapidly increasing, propelling the region's demand for core materials.

Middle East & Africa

Meanwhile, the Middle East & Africa is expected to have significant market growth driven by increased industrial investments. The Middle East & Africa region captured 5.00% of the global market in 2025, generating USD 0.11 billion in revenue, and is projected to reach USD 0.12 billion in 2026.

List of Key Companies in Core Materials Market

Key Players to Strengthen their Position by Offering Products to the Automotive and Aerospace Industries

The foremost producers, including Evonik Industries AG, Armacell International S.A., Plascore Incorporated, Euro-Composites S.A., Diab Group, 3A Composites, Gurit Holding AG, Hexcel Corporation, The Gill Corporation, and Changzhou Tiansheng New Materials Co. Ltd., are company trademarks for the core materials business.

On the other hand, Evonik Industries has a strong presence in Europe and manufactures natural materials. The company has a presence in Germany. The company is one of the biggest manufacturers of materials in the region. Similarly, the other key players have established a strong regional presence, robust distribution channels, and varied product offerings.

LIST OF KEY COMPANIES PROFILED:

- Evonik Industries AG (Germany)

- Armacell International S.A. (Luxembourg)

- Plascore Incorporated (U.S.)

- Euro-Composites S.A. (Luxembourg)

- Diab Group (Sweden)

- 3A Composites (Switzerland)

- Gurit Holding AG (Switzerland)

- Hexcel Corporation (U.S.)

- The Gill Corporation (U.S.)

- Changzhou Tiansheng New Materials Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- February 2021 - Armacell International S.A. launched its new flexible PET foams in the global market. The purpose of the new product launch is to maximize revenue.

- February 2021 - Euro-Composites S.A. launched the poly shape core material. This poly-shaped core material can be used in boats, helicopters, aircraft, and other applications. The core material launch aims to establish its presence in the different end-use industries.

- February 2021 - Diab Group acquired SABIC’s foam production line. The company decided to present the newly acquired foam products under the Divinycell portfolio. The purpose of the acquisition is to expand its product portfolio to maximize revenue.

- November 2019 - Evonik Industries announced the expansion of its production capacity for lightweight construction materials. The company expanded its ROHACELL closed foam cell production in North America. The purpose of the product expansion is to maximize revenue.

REPORT COVERAGE

The research report provides a detailed market analysis and focuses on crucial aspects such as types, applications, and leading companies. It provides quantitative data regarding value, research methodology for market size estimation, and insights into market trends. It highlights vital industry developments and the competitive landscape. In addition to the abovementioned factors, the report encompasses various factors contributing to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.8% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.38 billion in 2025 and is projected to reach USD 5.18 billion by 2034.

Registering a significant CAGR of 8.8%, the market will exhibit considerable growth over the forecast period (2026-2034).

Foam is expected to be the leading segment in this market during the forecast period.

Growth in the aerospace industry is driving the market.

China held the highest share of the market in 2023.

Evonik Industries AG, Armacell International S.A., Plascore Incorporated, Euro-Composites S.A., and Diab Group are the leading players in the global market.

The rising demand for lightweight materials in the end-use industry is driving the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us