Counterspace Security Market Size, Share, Industry Analysis, & Russia Ukraine War Analysis, By Type (Active Counterspace Systems and Passive Counterspace Systems), By System (Kinetic Physical Systems, Non-Kinetic Physical Systems, Electronic Warfare (EW) Systems, Cybersecurity & Network Protection, and Space Situational Awareness (SSA) Systems) By Platform (Ground-Based Installations, Space-Based Satellites, Airborne Platforms, and Naval Platforms), By End User (Government & Military and Commercial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

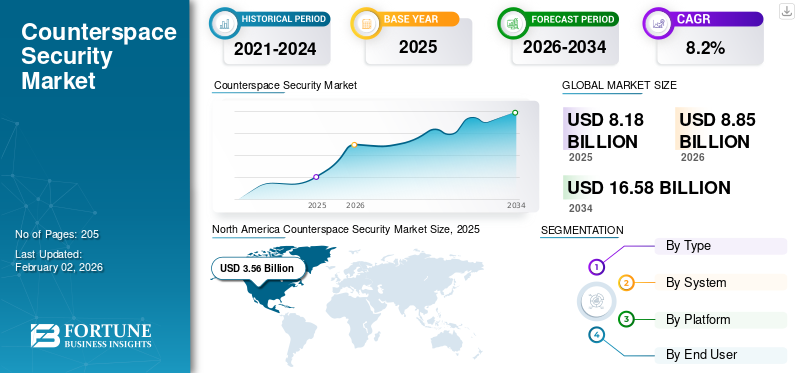

The global counterspace security market size was valued at USD 8.18 billion in 2025. The market is projected to grow from USD 8.85 billion in 2026 to USD 16.58 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period. North America dominated the counterspace security market with a industry share of 3.62% in 2025.

Counterspace security refers to the spectrum of technologies, systems, and measures designed to safeguard space-based assets such as satellites, ground stations, and communication networks from intentional interference, damage, or destruction. It encompasses both defensive and offensive capabilities, including Space Situational Awareness (SSA), electronic warfare, cyber protection, and directed energy or anti-satellite systems. The objective of counterspace security is to ensure the resilience, continuity, and strategic advantage of national and commercial space infrastructure in increasingly contested orbital environments.

Major players in the market include Lockheed Martin, Northrop Grumman, Raytheon Technologies, L3Harris Technologies, and BAE Systems, all of which are leading developers of satellite protection, surveillance, and electronic warfare systems. Thales Group and Airbus Defense & Space are prominent in Europe, focusing on SSA networks and secure satellite communication systems. General Dynamics Mission Systems is actively involved in this sector by developing advanced solutions for counterspace operations and systems space situational awareness.

Download Free sample to learn more about this report.

COUNTERSPACE SECURITY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 8.18 billion

- 2026 Market Size: USD 8.85 billion

- 2034 Forecast Market Size: USD 16.58 billion

- CAGR: 8.2% from 2026–2034

- North America dominated the counterspace security market with a industry share of 3.62% in 2025.

- Electronic warfare segment acquires the largest share in the market due to rising need for electromagnetic dominance.

- The pavement width segment covered in this report includes less than 2.5 Meters, 2.5 – 5 Meters & more than 5 Meters.

North America

North America dominates the market and is valued at USD 3.56 billion in 2025.

Europe

Europe market is growing steadily, driven by multinational defense cooperation and increased funding for space protection programs.

Asia Pacific

Asia Pacific represents the fastest-growing regional market, propelled by rapid militarization of space programs.

U.S.

The U.S. leads global counterspace initiatives through large-scale investments in satellite protection.

Japan

Japan is strengthening its counterspace security capabilities through investments in space situational awareness, satellite resilience programs, and strategic collaborations aimed at protecting critical space infrastructure from emerging threats.

Read More

Impact of Russia–Ukraine War

The Russia–Ukraine war has had a profound impact on the market, accelerating global investment in space-based defense, surveillance, and resilience technologies. The conflict demonstrated the strategic value of satellite networks for real-time intelligence, navigation, and communication with the help of commercial constellations such as Starlink for battlefield connectivity. This has driven nations to strengthen their counterspace and electronic warfare (EW) capabilities to safeguard orbital assets from jamming, spoofing, and cyber intrusion. Such use of anti-satellite (ASAT) technologies has increased the concerns over the vulnerability of space infrastructure, prompting NATO, and allied countries to enhance SSA and electromagnetic spectrum dominance programs.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Militarization of Space Driving Strategic Reliance on Space-Based Infrastructure Fuels Market Growth

A key driver that propels the market is the rapid militarization and strategic dependence on space-based infrastructure. Modern defense, communication, navigation, and intelligence systems increasingly rely on satellites operating across multiple orbits, making them critical yet highly vulnerable assets. The market demand is driven by escalating threats to space-based assets, the growing reliance on satellite technology for communication, navigation, and surveillance, and increasing investments by governments in advanced counterspace capabilities.

The rise in anti-satellite testing, electronic jamming incidents, and cyber intrusions has highlighted the urgent need for robust protection mechanisms. Governments are therefore prioritizing investments in SSA, cyber-resilient command networks, and non-kinetic defense systems to ensure operational continuity in contested environments. As geopolitical competition intensifies, there is an increasing demand for SSA and cutting-edge counterspace capabilities. In addition, the counterspace capabilities are being integrated into national defense strategies, driving sustained funding and technological innovation across the global market.

- For instance, in October 2025, U.S. Army revealed at AUSA conference that U.S. Army will formally prioritize counterspace capabilities in its fiscal 2027 budget requests, underscoring their rising importance for future operations.

MARKET RESTRAINTS

High Development and Installation Costs to Limit Market Expansion

The development and deployment of counterspace systems involve substantial, financial and technological challenges that act as a major restraint on counterspace security market growth. These systems require advanced integration of sensors, propulsion, guidance, electronic warfare, and cybersecurity architectures, each demanding significant R&D investment and specialized expertise. The cost of designing, testing, and launching kinetic and non-kinetic platforms often is costly which limits participation primarily to major defense powers and a few high-capability private entities. Furthermore, the supporting infrastructure, including ground-based command centers, data fusion networks, and SSA systems, adds further layers of cost and operational complexity, which hampers the expansion of the market during the forecast period.

MARKET OPPORTUNITIES

Expanding Role of Commercial Space and Private-Sector Collaboration in Space Defense Provides Significant Market Opportunities

A major opportunity for the market lies in the expanding role of commercial space and private-sector collaboration in space defense. With the rapid proliferation of small satellites, mega-constellations, and private launch providers, governments are increasingly partnering with commercial entities to enhance surveillance, cybersecurity, and situational awareness capabilities in orbit. This shift opens new avenues for private firms specializing in satellite monitoring, electronic warfare software, and cyber defense to supply mission-critical technologies traditionally confined to military programs. The growing emphasis on Public Private Partnerships (PPPs) and dual-use technology development enables faster innovation cycles and cost-sharing benefits presenting opportunities for the market.

COUNTERSPACE SECURITY MARKET TRENDS

Integration of Artificial Intelligence and Machine Learning in Counterspace Operations is a Significant Trend

A defining trend shaping the market is the growing integration of Artificial Intelligence (AI) and Machine Learning (ML) across detection, response, and decision-support systems. Modern counterspace operations require real-time data analysis from diverse sources satellites, radars, and communication networks making automation essential for threat identification and response. AI and ML algorithms are increasingly being used to predict hostile maneuvers, detect signal interference, and optimize resource allocation across multiple domains. These technologies enable faster, more accurate situational awareness and reduce reliance on manual command chains, thereby improving operational readiness.

MARKET CHALLENGES

Ambiguity in International Space Laws and Governance Frameworks to Present Challenges for Market

One of the most pressing challenges in the market is the lack of clear and enforceable international regulations governing space warfare and defense activities. Existing frameworks, such as the Outer Space Treaty of 1967, were designed for peaceful exploration and do not adequately address modern counterspace threats such as cyber interference, satellite jamming, or kinetic ASAT testing. This legal ambiguity creates uncertainty for both governments and private companies operating in the defense space domain, complicating technology development, cooperation, and deployment decisions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Escalating Demand for Protection and Deterrence of Critical Space Assets Drive Active Counterspace Segment Growth

On the basis of type, the market is bifurcated into active counterspace systems and passive counterspace systems.

Active counterspace systems segment is the largest and fastest-growing segment of the market, driven by the escalating demand to protect and deter threats against critical space assets. Nations are increasingly investing in direct-ascent and co-orbital technologies capable of neutralizing adversarial satellites, reflecting a strategic shift from passive defense to active deterrence. The growing militarization of space illustrated by the formation of dedicated space commands and defense agencies has accelerated R&D efforts in kinetic interceptors, directed-energy weapons, and maneuverable satellites.

- For instance, in June 2025, the U.K. Ministry of Defense announced over USD 5.24 billion in funding for autonomous systems and nearly USD 1.31 billion for directed energy weapons, including the DragonFire laser, under the 2025 Strategic Defense Review.

By End User

Surge in Satellite-Based Surveillance and Communication Networks Boosts Demand for Advanced EW Technologies

Based on end user, the market is segmented into kinetic physical systems, non-kinetic physical systems, Electronic Warfare (EW) systems, cybersecurity & network protection, and Space Situational Awareness (SSA) systems.

Electronic warfare segment acquires the largest share in the market due to rising need for electromagnetic dominance and secure satellite communications in an increasingly contested orbital environment. These systems play a pivotal role in detecting, jamming, and spoofing hostile signals to protect national assets and disrupt adversarial operations. The surge in satellite-based surveillance and communication networks has further amplified the demand for advanced EW technologies capable of ensuring information superiority.

- For instance, in September 2025, Collins Aerospace, a business of RTX, received a NATO contract to provide its Electronic Warfare Planning and Battle Management (EWPBM) software, designed to plan, direct, coordinate, synchronize, and assess electromagnetic warfare operations.

The cybersecurity & network protection segment is the fastest-growing segment of the market driven by the sharp increase in cyberattacks targeting satellite networks, command centers, and data relay systems. As both commercial and defense operators rely on digital connectivity for satellite control and mission data transmission, securing these networks has become a strategic imperative. Growing interconnectivity between space, cloud, and terrestrial communication systems has expanded the cyber threat surface, compelling agencies to adopt integrated, end-to-end protection architectures.

- For instance, in December 2023, TLogos, part of the TXT Group secured a USD 8.67 million multi-year contract with the European Space Agency (ESA) to provide cybersecurity services for ESA’s Human Exploration Programme from 2025 to 2029. This contract supports critical programs including the International Space Station Security Programme and Gateway Programme Security Support.

By Platform

Increasing Modernization of Ground-Based Radar, Laser Tracking, and Jamming Infrastructure Support Ground Based Installations Segment Growth

Based on platform, the market is segmented into ground-based installations, space-based satellites, airborne platforms, and naval platforms.

The ground-based installations segment accounts for the majority of the counterspace security market share due to their critical role in command, control, communication, and monitoring of orbital operations. These systems form the backbone of global space defense architecture, enabling real-time situational awareness, threat detection, and signal interception. Nations continue to expand and modernize their ground-based radar, laser tracking, and jamming infrastructure to safeguard satellites and communication networks from interference or hostile activity.

- For instance, in October 2025, Thales announced an upcoming contract to develop and deploy AURORE, a ground-based low orbit space surveillance radar system, as part of the ARES program. The AURORE system will be the largest surveillance radar in Europe, capable of continuous monitoring and tracking multiple space objects, including satellites and debris, in real-time.

The space-based satellites segment is the fastest-growing in the market, propelled by the surge in on-orbit defense, surveillance, and situational awareness missions. As orbital threats evolve, nations are deploying maneuverable satellites equipped with electronic countermeasure payloads, high-resolution sensors, and autonomous threat detection algorithms. The proliferation of small satellite constellations and dual-use defense platforms is enabling faster, more flexible responses to potential space conflicts, which is expected to drive segment growth.

To know how our report can help streamline your business, Speak to Analyst

By End User

Increased Government Investments in Advanced Counterspace Capabilities Including Surveillance, EW, and Missile Interception Drive Government & Military Segment Growth

Based on end user, the market is segmented into government & military and commercial.

The government & military segment holds the largest share of the market, driven by the escalating need for national defense preparedness, strategic deterrence, and protection of critical space infrastructure. Governments worldwide are prioritizing investments in advanced counterspace capabilities ranging from satellite surveillance and electronic warfare to missile-based interception systems to safeguard communication, navigation, and reconnaissance assets.

The commercial segment is the fastest-growing in the market, fueled by the rapid expansion of private satellite constellations, space-based communication networks, and commercial data services. As private enterprises play a larger role in orbital operations, they face increasing exposure to cyber threats, jamming, and debris risks driving the adoption of advanced counterspace protection technologies.

Counterspace Security Market Regional Outlook

Based on region, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Counterspace Security Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America dominates the market and is valued at USD 3.56 billion in 2025, supported by its strong defense infrastructure, high R&D expenditure, and early adoption of advanced space defense technologies. The U.S. leads global counterspace initiatives through large-scale investments in satellite protection, electronic warfare, and space-based surveillance programs. The presence of major defense contractors such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, and Boeing strengthens the North America market. Countries such as the U.S. are investing satellite situational awareness and space based electronic warfare systems as a national security priority.

- For instance, in November 2025, the U.S. Space Force announced the deployment of two new ground-based jamming systems, Meadowlands and the Remote Modular Terminal (RMT), designed to disrupt Chinese and Russian spy satellite surveillance, augmenting the existing Counter Communications System operational from 2020.

Europe

Europe market is growing steadily, driven by multinational defense cooperation and increased funding for space protection programs. The European Union and its member states are developing joint space surveillance and anti-jamming frameworks under the EU Space Defense Strategy to counter emerging threats. The Russia counterspace security market is characterized by significant investment and strategic focus on technologies aimed at protecting space assets and enhancing space-based military capabilities. Countries such as the U.K., France, and Germany are investing heavily in electronic warfare, laser-based tracking, space based monitoring, and SSA systems.

- For instance, in October 2025, the U.K. Ministry of Defense and U.K. Space Agency announced a government-backed initiative to develop advanced sensor technology aimed at detecting and countering laser attacks on British military and civilian satellites. This project, funded with around USD 656,197.5, will enable satellites to identify laser signals.

Asia Pacific

Asia Pacific represents the fastest-growing regional market, propelled by rapid militarization of space programs, increasing defense budgets, and technological advancements. Major countries in the region such as China, India, and Japan are expanding indigenous capabilities in ASAT weapons, cyber defense, and electronic warfare to enhance space sovereignty. China counterspace security market is growing due to the focus of the country on dual-use satellites. Moreover, India’s space defense collaborations with allied nations and development of space satellites to improve defense capabilities is expected to propel the Asia Pacific counterspace security market.

- For instance, in July 2025, India announced the fast-tracking of the deployment of 52 dedicated defense satellites under the Space Based Surveillance Phase-3 (SBS-3) programme, scheduled for completion by 2029, to enhance real-time military intelligence and protect its orbital assets.

Latin America

The market in Latin America is in its early stages but is expanding due to growing partnerships with global defense agencies and private aerospace firms. Countries such as Brazil and Mexico are investing in satellite monitoring, communication encryption, and radar modernization programs to enhance situational awareness and national security.

Middle East & Africa

The Middle East & Africa region is witnessing rising interest in space security, driven by national security priorities, satellite investment programs, and emerging space agencies. Nations such as the UAE and Saudi Arabia are increasing funding toward SSA, cyber defense, and signal protection systems to safeguard their expanding communication and reconnaissance satellite fleets.

COMPETITIVE LANDSCAPE

Key Industry Players

AI-Driven Counterspace Capabilities, Cyber Defense Integration, and Strategic Space Partnerships Strengthen Competitive Positioning in Market

The market is moderately consolidated, comprising a select group of global defense contractors, aerospace OEMs, and specialized technology integrators that dominate both system development and operational support activities. Competition is primarily defined by technological innovation, orbital situational awareness capabilities, electronic warfare expertise, cybersecurity integration, and government defense affiliations.

Leading market participants include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation (RTX), and L3Harris Technologies, all of which maintain extensive portfolios in satellite protection, electronic countermeasures, and cyber-resilient communication systems. These firms leverage long-standing defense contracts and multilateral government collaborations to ensure sustained demand for counterspace infrastructure and mission-support services.

LIST OF KEY COUNTERSPACE SECURITY COMPANIES PROFILED

- BAE Systems plc (U.K.)

- Lockheed Martin Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- RTX Corporation (U.S.)

- Airbus Defense & Space (Germany)

- Leonardo S.p.A. (Italy)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Shoghi Communications (U.S.)

- ELT Group (U.S.)

- CYSEC SA (Switzerland)

- Globals Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: BAE Systems awarded a USD 1.2 billion contract by U.S. Space Systems Command to design and build 10 satellites for the “Resilient Missile Warning & Tracking MEO Epoch 2” programme, including ground-system delivery.

- June 2025: L3Harris developed the Meadowlands system, an advanced, mobile ground-based Counter Communications System (CCS) and delivered to the U.S. Space Force’s Electromagnetic Warfare unit, aimed at disrupting adversary satellite communications.

- May 2025: Raytheon Technologies Corporation received a contract worth USD 580 million production contract from the U.S. Navy for the Next Generation Jammer Mid‑Band (NGJ‑MB) system.

- September 2024: Northrop Grumman was selected to continue developing the Glide Phase Interceptor (GPI), a missile defense asset aimed at neutralizing hypersonic weapons during their glide phase, in a U.S.-Japan co-production initiative led by the U.S. Missile Defense Agency.

- January 2024: The Air Force Research Laboratory and Raytheon, an RTX business, successfully completed a three-week field test of the CHIMERA high-power microwave (HPM) weapon at White Sands Missile Range, demonstrating its capability to acquire, track, and defeat multiple airborne targets.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, System, Platform, and Region |

|

By Type |

· Active Counterspace Systems · Passive Counterspace Systems |

|

By System |

· Kinetic Physical Systems · Non-Kinetic Physical Systems · Electronic Warfare (EW) Systems · Cybersecurity & Network Protection · Space Situational Awareness (SSA) Systems |

|

By Platform |

· Ground-Based Installations · Space-Based Satellites · Airborne Platforms · Naval Platforms |

|

By End User |

· Government & Military · Commercial |

|

By Region |

· North America (By Type, By System, By Platform, and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Type, By System, By Platform, and Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Type, By System, By Platform, and Country) o China (By End User) o Japan (By End User) o India (By End User) o South Korea (By End User) o Rest of Asia Pacific (By End User) · Latin America (By Type, By System, By Platform, and Country) o Brazil (By End User) o Mexico (By End User) o Rest of Latin America( By Platform) · Middle East & Africa (By Type, By System, By Platform, and Country) o UAE (By End User) o Saudi Arabia (By End User) o South Africa (By End User) o Rest of Middle East & Africa (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.18 billion in 2025 and is projected to reach USD 16.58 billion by 2034.

In 2025, the market value stood at USD 3.56 billion.

The market is growing at a CAGR of 8.2% during the counterspace security market forecast period.

The active counterspace system segment led the market by type.

The key factors driving the market are growth of market are rapid militarization of space driving strategic reliance on space-based infrastructure.

BAE Systems plc (U.K.), Lockheed Martin Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), and RTX Corporation (U.S.) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us