Crop Insurance Market Size, Share & Industry Analysis, By Coverage Type (Multi-Peril Crop Insurance (MPCI), Crop Hail Insurance, and Others), By Distribution Channel (Private Insurance Providers, Public/Government Insurance Providers, Broker Agents, Bancassurance, and Online Platforms), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

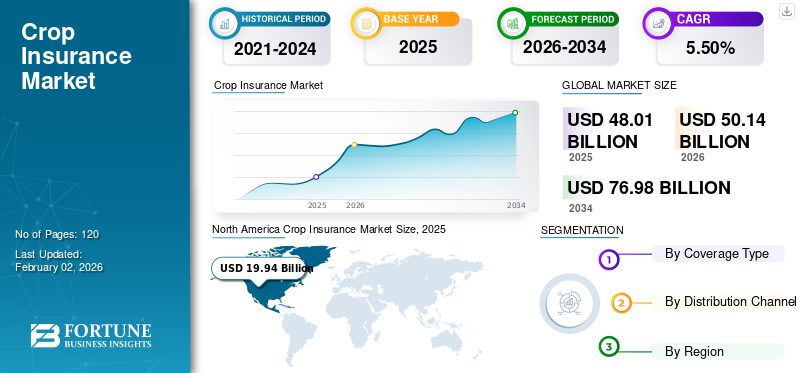

The global crop insurance market size was valued at USD 48.01 billion in 2025 and is projected to grow from USD 50.14 billion in 2026 to USD 76.98 billion by 2034, exhibiting a CAGR of 5.50% during the forecast period. North America dominated the global market with a share of 41.60% in 2025.

The global crop-insurance sector plays an important role in not only stabilizing farm income but also mitigating the financial impact of crop losses that are caused by natural disasters, pests, and diseases. Governments and private insurers have collaborated in order to promote crop insurance, particularly in regions that are vulnerable to climate change and adverse weather conditions. The market is broadly classified based on coverage into Multi-Peril Crop Insurance (MPCI) and Crop Hail Insurance, with MPCI being the most widely adopted owing to its comprehensive coverage. Leading players such as Munich Re, Zurich Insurance Group, and American International Group (AIG) have established their strong presence globally, which is further supported by partnerships with local agencies as well as government-backed programs.

The future for the agriculture insurance market is positive, supported by the increasing frequency of extreme weather events and growing awareness among farm operators, especially in developing economies including India. Technological advancements such as remote sensing, satellite imagery, and AI-powered risk assessment are further expected to enhance underwriting precision and claims management. In addition, the expanding partnerships of the public-private sectors, along with the introduction of index-based insurance products that are tailored for smallholder farmers, are expected to deepen market penetration and improve resilience in agriculture.

Download Free sample to learn more about this report.

CROP INSURANCE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 48.01 Billion

- 2026 Market Size: USD 50.14 Billion

- 2034 Forecast Market Size: USD 76.98 Billion

- CAGR: 5.50% from 2026–2034

- North America dominated the crop insurance market with a 41.60% share in 2025.

- The Multi-Peril Crop Insurance (MPCI) segment is projected to account for 77.78% of the market in 2026.

- The public/government insurance providers segment is projected to hold 49.52% of the market in 2026.

North America

North America reached USD 19.94 billion in 2025, accounting for 41.60% of global market revenue.

Asia Pacific

Asia Pacific was valued at USD 13.60 billion in 2025, representing 28.30% of the global market.

Europe

Europe generated USD 7.40 billion in 2025, contributing 15.40% of global revenue.

U.S.

The market is projected to reach USD 16.83 billion by 2026.

Japan

The market is projected to reach USD 3.34 billion by 2026.

Read More

MARKET DYNAMICS

Crop Insurance Market Trends

Technological Integration in Risk Assessment to Emerge as a Major Trend

Technology advances such as satellite imagery, AI, drone monitoring, and big data analytics are transforming the agriculture insurance market by allowing for more accurate risk modeling, real-time crop monitoring, and faster claims processing. As a result, insurers are also leveraging these innovations on a large scale in order to enhance underwriting precision and reduce operational inefficiencies, which is helping to reshape how policies are designed and delivered. This technological shift has not only streamlined operations but has also expanded access to underserved agricultural regions.

Download Free sample to learn more about this report.

Market Drivers

Climate Volatility and Extreme Weather Events to Drive Market Growth

The rising number of severe climate-related events such as droughts, floods, and unseasonal rainfall is compelling farmers to look out for financial protection through the means of insurance. This increased vulnerability to unpredictable weather patterns has created increased demand for comprehensive coverage, including Multi-Peril Crop Insurance (MPCI), which insures the crops against many different natural calamities. As climate risk intensifies across both developed and emerging regions, insurers and governments are ramping up their efforts to promote agriculture insurance as a key risk mitigation tool.

Market Restraints

Low Farmer Awareness and Affordability Challenges to Restrain Market Expansion

In spite of all the advantages that agricultural insurance offers, the market faces limitations due to less awareness as well as financial constraints, particularly amongst small-scale farmers in developing countries. Also, many farmers are not aware of insurance coverage options or find premium costs prohibitive without any subsidies. Other issues, such as a lack of trust in insurers and delayed claims settlements, are also disincentivizing small farmer participation. This continues to slow widespread adoption and ultimately makes it difficult for insurers to access some of the most vulnerable but most needed markets.

Market Opportunities

Public-Private Collaborations and Index-Based Products to Offer Growth Opportunities

The emergence of index-based insurance products that make use of predefined parameters such as rainfall levels or temperature to trigger payouts offers a scalable solution for improving access in regions that have poor infrastructure as well as limited historical yield data. Index based insurances, when combined with increasing support from governments and international development agencies, public private partnerships are promoting wider distribution and customization of insurance offerings. These collaborations are expected to unlock many lucrative growth prospects for the Asia Pacific and Africa regions, where agriculture is the backbone of rural livelihoods.

SEGMENTATION ANALYSIS

By Coverage Type

Multi-Peril Crop Insurance (MPCI) Dominates Owing to Comprehensive Risk Coverage and Government Support

Based on coverage type, the market is segmented into Multi-Peril Crop Insurance (MPCI), crop hail insurance, and others.

Multi Peril Crop Insurance (MPCI) segment is projected to dominate the market with a share of of 77.78% in 2026 and the highest CAGR over the forecast period. MPCI, owing to its comprehensive coverage, protects farmers from various risks, such as drought, flood, disease, pests, and other natural calamities. MPCI is widely adopted in the U.S., China, and India, where government-backed programs and premium subsidies have made it accessible as well as affordable for large farming communities. The increasing frequency of climate-related events and rising emphasis on food security boost the demand for Multi Peril Crop Insurance MPCI, making it the most preferred insurance product globally.

Crop hail insurance has comparatively a smaller market share in the agriculture insurance space. It is more commonly found in places where hailstorms are a consistent and significant threat, mainly in parts of Europe, North America, and Australia. While it offers targeted protection, its narrow scope in comparison to MPCI limits its adoption in broader risk management tools and strategies.

The others segment includes products such as revenue protection and weather index insurance, which are still niche but growing among products in upcoming markets, primarily due to low administrative costs and ease of implementation. However, these products currently make up a small portion of the market due to a lack of awareness and regulatory support.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Public/Government Insurance Providers Lead with Government Support for Subsidized Agriculture Insurance Schemes

By distribution channel, the market is segmented into private insurance providers, public/government insurance providers, broker agents, bancassurance, and online platforms.

Public/government insurance providers segment is projected to dominate the market with a share of 49.52% in 2026. This is primarily due to considerable government support for subsidized agriculture insurance schemes in large markets such as the U.S., India, and China. Public programs in these regions have a lower premium costs and more accessibility for rural and agriculture areas.

Online platforms are projected to grow the fastest, registering the highest CAGR over the forecast period. This growth is mainly driven by increasing digital utilization, mobile platforms, government-led digital agriculture strategy initiatives, and the ability to compare, purchase, and customize policies online, especially for the younger and tech-savvy generation of farmers.

Private insurance providers have a substantial market share, especially in developed markets with less reliance on public programs, even if they are associated as an affordability component in publicly sponsored programs or reinsurance. Broker Agents can provide individual sales services to educate clients, however shareholders face high servicing costs and hold a small market share.

Bancassurance is a less developed area of protection product distribution, but supports product access through rural bank networks for bundled products toward client engagement as financial literacy develops in rural and urban environments.

CROP INSURANCE MARKET REGIONAL OUTLOOK

Based on regional ground, the market is studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Crop Insurance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 19.94 billion in 2025 and USD 20.68 billion in 2026. North America holds the largest share of the global agriculture insurance market since the U.S. already has a well-established and government-supported crop-insurance industry. Increased awareness among farmers, a well-defined regulatory environment, and high take-up rates of Multi-Peril Crop Insurance (MPCI) are some factors that benefit the region's growth. Importantly, public-private partnerships, particularly through the U.S. Federal Crop Insurance Program, facilitate a degree of coverage that would be difficult for an entirely private insurance sector to achieve alone. Canada also has a solid provincial-level insurance system, while Mexico's market is slowly growing through consolidated government programs and policies for agriculture. The U.S. market is projected to reach USD 16.83 billion by 2026. The market in North America reached USD 19.94 billion in 2025, representing 41.60% of total market revenue, and is projected to reach USD 20.68 billion in 2026.

The U.S. is the global leader in agriculture insurance in terms of market size and policy volume. The Federal Crop Insurance Corporation (FCIC), managed by the USDA’s Risk Management Agency RMA, provides a well-structured framework with premium subsidies and broad participation. Private insurers deliver policies, while the government assumes a substantial part of the risk. As a result, the rapid adoption of digitalization, ongoing government policy support, and reputable actuarial models have all helped to establish the U.S. as a global leader in agriculture insurance practices.

South America

South America is a geographically diverse region, and significant agricultural insurance use is found in Brazil and Argentina. Brazil has one of the most sophisticated programs in the region through its government-sponsored rural insurance scheme, encouraging private sector involvement. However, many smaller countries still face challenges, such as high insurance premiums and limited product accessibility. The increasing significance of agribusiness exports and exposure to extreme weather events will drive plausible future demand in the region. The South America market generated USD 4.7 billion in 2025, representing 9.80% of the global market landscape, and is expected to reach USD 4.96 billion in 2026.

Europe

Europe has a moderately maturing agriculture insurance market, with France, Spain, and Italy being the key countries. Coverage through government support varies considerably across countries, which impacts penetration rates. Hail insurance is a popular product throughout parts of Central and Eastern Europe. Still, climate variability is driving many governments and insurers to investigate and develop broader arrangements that can offer more comprehensive MPCI-type coverage. EU funding programs for agricultural risk management are also driving collaboration and cross-border innovations in insurance schemes. The UK market is projected to reach USD 3.21 billion by 2026, and the Germany market is projected to reach USD 1.4 billion by 2026. Europe contributed approximately USD 7.4 billion to the global market in 2025, accounting for 15.40% share, and is expected to reach USD 7.73 billion in 2026.

Middle East & Africa

The agriculture insurance market in the Middle East & Africa remains relatively unexplored. Still, it is beginning to attract more attention because of the increased risks caused by climate change and food insecurity. Obstacles to continued development include a lack of awareness, low penetration, and challenges facing infrastructure. Nonetheless, pilot projects utilizing index-based insurance paired with collaboration with international development organizations have begun to show promise in parts of sub-Saharan Africa and in North African markets where agriculture is a large contributor to the economy. Middle East & Africa maintained a strong presence in the global market, reaching USD 2.35 billion in 2025, accounting for 4.90% share, and is expected to reach USD 2.47 billion in 2026.

Asia Pacific

Asia Pacific is estimated to depict the highest CAGR over the forecast period. India and China have rapidly expanding agricultural economies, and their governments are actively encouraging agriculture insurance by promoting subsidies, digital platforms, and obligatory schemes. India's Pradhan Mantri Fasal Bima Yojana (PMFBY) and the increasing multi-peril cover in China, led by the government, are already expanding the insured area. The most critical aspect contributing to crop insurance market growth in this region is the increased climate vulnerability farmers face and the need to stabilize total income for these farmers. The Japan market is projected to reach USD 3.34 billion by 2026, the China market is projected to reach USD 4.8 billion by 2026, and the India market is projected to reach USD 2.58 billion by 2026. In 2025, the Asia Pacific market stood at USD 13.6 billion, representing 28.30% of global demand, and is projected to grow to USD 14.31 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Public-Private Partnerships, Risk Diversification, and Tech-Driven Solutions

Major players in the international agriculture insurance sector have a strong emphasis on high public-private partnerships, particularly in the areas of government subsidies and regulatory support. These organizations often combine reinsurance, partnerships with government agencies, and broker, bank, and/or tech platform distribution networks. A noticeable trend among major players is using modern technology such as remote sensing, satellites, AI, and risk modeling to improve underwriting accuracy and expedite claims development. Also, their varied geographies and contour types allow them to offset risk exposure and address a wide spectrum of farming levels, ranging from smallholder emerging market producers to large directors of agribusiness producers in established economies.

Long List of Companies Studied (including but not limited to)

- Munich Re (Germany)

- Swiss Re (Switzerland)

- China United Property Insurance Company (China)

- PICC Property and Casualty Company Limited (China)

- QBE Insurance Group Limited (Australia)

- Tokio Marine Holdings Inc. (Japan)

- Sompo Holdings, Inc. (Japan)

- Zurich Insurance Group (Switzerland)

- American International Group, Inc. (U.S.)

- Chubb Limited (Switzerland)

- AXA XL (France)

- Fairfax Financial Holdings Limited (Canada)

- Allianz SE (Germany)

- The Travelers Companies, Inc. (U.S.)

- Great American Insurance Group (U.S.)

- ICICI Lombard General Insurance Company Ltd. (India)

- Tata AIG General Insurance Company Limited (India)

- Agriculture Insurance Company of India Ltd. (India)

- Mapfre S.A. (Spain)

- The Hartford Financial Services Group, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Palomar Holdings announced the acquisition of Advanced AgProtection (AAP), a Texas-based crop-focused MGA, to expand its specialty insurance offerings and deepen its agri-risk portfolio.

- February 2025: USDA’s Risk Management Agency expands Controlled Environment pilot crop-insurance program to 48 counties across 17 states for 2026, raising coverage limits from 75% to 85%

- February 2025: Government of Canada and Saskatchewan reaffirm funding for the 2025 agriculture insurance program via SCIC, underwriting USD 7 billion in claims, premium reserves, and cost sharing to ensure program stability.

- January 2025: Global Parametrics partners with Frontier Markets to launch parametric drought insurance in Rajasthan and Uttar Pradesh, enabling quick payouts for 5,000 women smallholder farmers.

- May 2022: Philippines introduces first public‑private agriculture insurance scheme backed by Asian Development Bank to boost resilience among smallholder farmers.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading insurance companies, coverage types, and distribution channels of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.50% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Coverage Type

By Distribution Channel

By Region

|

|

Companies Profiled in the Report |

Munich Re (Germany), Swiss Re (Switzerland), China United Property Insurance Company (China), PICC Property and Casualty Company Limited (China), QBE Insurance Group Limited (Australia), Tokio Marine Holdings Inc. (Japan), Sompo Holdings, Inc. (Japan), Zurich Insurance Group (Switzerland), American International Group, Inc. (U.S.), Chubb Limited (Switzerland) |

Frequently Asked Questions

The market is projected to reach USD 76.98 billion by 2034.

In 2025, the market was valued at USD 48.01 billion.

The market is projected to grow at a CAGR of 5.50% during the forecast period.

The Multi-Peril Crop Insurance (MPCI) segment is expected to lead the market.

Climate volatility and extreme weather events are the key factors driving market growth.

Munich Re, Swiss Re, China United Property Insurance Company, American International Group, Inc., Agriculture Insurance Company of India Ltd., and Mapfre S.A. are some of the top players in the market.

North America dominated the global market with a share of 41.60% in 2025.

By distribution channel, the online platform is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us