Reinsurance Market Size, Share & Industry Analysis, By Type (Facultative Reinsurance and Treaty Reinsurance), By Application (Life Reinsurance and Non-Life Reinsurance), and Regional Forecast, 2026-2034

Reinsurance Market Outook 2026

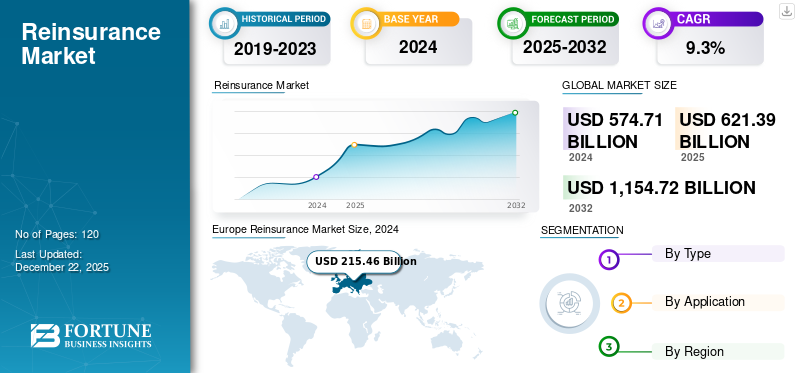

The global reinsurance market size was valued at USD 621.39 billion in 2025 and is projected to grow from USD 673.28 billion in 2026 to USD 1403.7 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period. Europe dominated the reinsurance market with a market share of 37% in 2025.

Reinsurance holds a unique significance within the BFSI sector, as it serves as a critical mechanism for insurers to manage and transfer large-scale risks to ensure financial security while also contributing to market growth. More recently, instead of merely mitigating large risks, it may also be used to transfer risk strategically to ensure that a certain level of risk is still present to stabilize the market. It can be defined as insurers transferring portions of their risk portfolios to specialized reinsurers, which in turn helps mitigate risk across the market.

There are significant players in the market who will continue to play a crucial role, including Munich Re, Swiss Re, Hannover Re, and others, whose strategies and results are of significance to governments, insurers, and other organizations, lending further credence to their viability as continued players in this space. Recently, we faced the evolution brought on by the COVID-19 pandemic, which introduced a scale of unique systemic risks globally, forcing reinsurers to rethink their risk models, performance, and capital adequacy. This led to increased scrutiny of previously held underwriting practices and a reassessment of pricing within the reinsurance industry amid higher levels of uncertainty and financial volatility triggered by the pandemic.

The global reinsurance market occupies a central position within the insurance ecosystem by enabling capital optimization, risk diversification, and underwriting capacity expansion for primary insurers. Market dynamics increasingly reflect catastrophe exposure, interest rate conditions, regulatory requirements, and evolving risk landscapes rather than premium growth alone. Reinsurance market growth remains closely linked to the financial strength of cedents, natural disaster frequency, and the industry's ability to absorb emerging risks across life and non-life portfolios. Pricing discipline and capital adequacy continue shaping profitability and competitive positioning.

Non-life business remains the largest contributor to the reinsurance market size due to rising catastrophe losses, inflationary pressures, and increasing complexity within property, casualty, cyber, and specialty lines. Life reinsurance demand also continues benefiting from demographic shifts, longevity trends, and growing protection requirements across developing economies. Primary insurers increasingly rely on reinsurance structures to manage solvency ratios, earnings volatility, and concentration risks.

Supply-side conditions have undergone a significant transformation. Reinsurers are emphasizing underwriting discipline, portfolio optimization, and exposure management following elevated catastrophe losses and higher claims severity. Alternative capital sources, including Insurance-Linked Securities (ILS), continue influencing market liquidity and pricing behavior. Capacity availability varies considerably across business classes, with specialty risks and catastrophe-exposed segments experiencing tighter conditions.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Reinsurance Market Takeaways

- 2025 Market Size: USD 621.39 Billion

- 2026 Market Size: USD 673.28 Billion

- 2034 Forecast Market Size: USD 1,403.70 Billion

- CAGR: 9.6% from 2026–2034

- Europe dominated the reinsurance market with a 37.00% share in 2025.

- The facultative reinsurance segment is projected to lead the market with a 57.33% share in 2026.

- The non-life reinsurance segment is expected to dominate with a 67.05% share in 2026.

North America

North America accounted for USD 215.35 billion in 2025 and is expected to grow to USD 232.47 billion by 2026.

Europe

Europe led the global market with USD 230.22 billion in 2025 and is projected to reach USD 246.45 billion in 2026.

Asia Pacific

Asia Pacific represented USD 140.95 billion in 2025 and is projected to reach USD 156.22 billion in 2026, supported by rising insurance penetration.

U.S.

The U.S. reinsurance market is projected to reach USD 194.07 billion by 2026.

Japan

The Japanese reinsurance market is projected to reach USD 30.51 billion by 2026.

Read More

Reinsurance Market Dynamics

Reinsurance Market Trends:

Digital Adoption and ESG Focus are Driving Improved Efficiency and Innovation

A key trend is the accelerated uptake of digital transformation and advanced analytics. Reinsurers increasingly utilize technologies such as Artificial Intelligence (AI) and big data to improve risk analysis, enhance pricing models, and automate claims. This focus on automation and data-driven insights aims to improve operational efficiency and underwriting precision.

There is also a rising interest in sustainable and Environmental, Social, and Governance (ESG) benchmarks that shape their risk management and product design. It reflects a general industry transition toward more socially responsible practices, including environmental and social considerations integrated into everyday operations and core business decisions. InsurTech partnerships are also beginning to emerge, facilitating innovation within all business activities.

Risk analytics and technological capabilities are increasingly shaping reinsurance market trends and underwriting strategies. Advanced modeling techniques, artificial intelligence, and predictive analytics are improving portfolio assessment and enabling more granular pricing methodologies. Reinsurers are allocating greater resources toward data-driven decision frameworks to enhance capital efficiency and strengthen risk selection.

Climate adaptation has emerged as a defining industry priority. Elevated catastrophe activity and changing weather patterns are prompting revisions to exposure assumptions and pricing structures. Geographic diversification and portfolio optimization have become increasingly important as firms seek to mitigate concentration risk and improve resilience.

Alternative capital participation continues influencing competitive dynamics. Insurance-Linked Securities and catastrophe bonds have evolved into established components of the broader risk transfer ecosystem. Their growing role supports additional capacity while providing institutional investors with exposure to uncorrelated asset classes.

Portfolio discipline has gained renewed importance following several years of elevated claims activity. Reinsurers increasingly emphasize underwriting profitability rather than market share expansion. Capacity allocation is becoming more selective, particularly in segments characterized by higher uncertainty or inadequate pricing.

Reinsurance Market Growth Drivers:

Growing Insurance Needs and Risk Complexity Continuously Fuel Demand for the Market

Constantly evolving and complex global economies increase the reliance on risk transfer for risk management to maintain financial security. As insurance penetration develops in emerging economies, it drives demand for reinsurance support. Insurers’ reliance on capital management and risk transfer creates an almost continuous process of need. That reliance forces insurers to leverage reinsurers to minimize the impact of potentially catastrophic losses on their balance sheets. This allows them to offer broader coverage for greater risk. The symbiotic nature of that relationship creates an ongoing and growing need for the market across many disciplines.

Escalating risk complexity across global insurance markets continues to strengthen demand for reinsurance capacity and capital support. Primary insurers increasingly rely on reinsurance arrangements to manage earnings volatility, improve solvency ratios, and maintain underwriting flexibility. Exposure growth across property, casualty, cyber, and specialty segments has elevated the strategic importance of external risk transfer mechanisms. Consequently, reinsurance market growth remains closely aligned with the expansion of insured assets and increasing risk accumulation.

Climate-related events represent another major demand catalyst. Rising catastrophe frequency and higher claims severity have increased the need for portfolio diversification and capital protection. Cedents increasingly seek reinsurance support to absorb peak exposures and preserve balance sheet stability during periods of elevated losses.

Regulatory frameworks also influence market expansion. Solvency requirements and capital adequacy standards encourage insurers to optimize risk retention strategies and improve financial resilience through reinsurance partnerships. Structured arrangements frequently enable insurers to enhance capital efficiency while maintaining growth objectives.

Reinsurance Market Restraints:

Cyclicality, Competition, Regulation, and Capital Needs Limit Market Growth and Stability

A primary constraint is the natural cyclicality and volatility in financial performance. Profits are extremely vulnerable to catastrophic losses, contributing to random profitability patterns and periods of market hardening. High levels of competition impact pricing and margins, and high levels of regulation introduce compliance costs and complexity. These forces severely limit the ability to achieve reliable growth or profitability. Additionally, the high capital requirements to underwrite large risks can limit market entry for new participants and restrict the expansion of current participants, leading to more instability in the market.

Claims volatility remains one of the principal challenges affecting the reinsurance market. Natural catastrophes, secondary perils, inflation-driven loss severity, and geopolitical disruptions periodically create substantial earnings pressure. Such events may reduce capital availability and contribute to tighter underwriting conditions, particularly within catastrophe-sensitive business lines.

Pricing cyclicality represents another structural restraint. Reinsurance markets historically experience alternating hard and soft phases that influence profitability and capacity deployment. Intense competition during soft markets can compress margins, while hard market conditions may restrict affordability for cedents seeking additional protection.

Model uncertainty increasingly complicates risk assessment. Climate change, cyber exposures, and emerging liability risks introduce variables that remain difficult to quantify accurately. Traditional actuarial assumptions may not fully capture evolving risk characteristics, increasing underwriting complexity, and reserve uncertainty.

Reinsurance Market Opportunities:

Emerging Market GDP Growth and Rising Penetration Drive Demand for Market

Emerging markets’ growth represents a significant opportunity, mainly driven by the increase in Gross Domestic Product (GDP) and the rising insurance penetration in developing regions. As these economies grow, people find themselves with more disposable income, which leads to a greater demand for life and general insurance products that protect their assets and provide financial security. At the same time, governments and regulatory bodies often put policies in place to promote financial inclusion and mandate insurance coverage in certain sectors, which helps to increase penetration rates further. This expanding insurance landscape creates a larger pool of primary insurers to transfer risk, resulting in a substantial new demand for reinsurance capacity and services in these promising markets.

Emerging economies represent a significant opportunity for the reinsurance market as insurance penetration rates remain comparatively low across many regions. Expanding middle-class populations, increasing asset ownership, and improving financial awareness are supporting primary insurance development, thereby creating additional demand for reinsurance capacity and expertise.

Climate resilience initiatives present another attractive avenue for growth. Governments, insurers, and multilateral organizations are increasingly exploring public-private partnerships to address catastrophe protection gaps. Innovative risk-sharing mechanisms and parametric structures are gaining attention as tools for improving financial resilience in vulnerable regions.

Specialty lines offer favorable prospects for value creation. Cyber insurance, renewable energy projects, marine risks, and complex liability exposures require sophisticated underwriting capabilities and advanced analytical support. Reinsurers possessing niche expertise may achieve stronger margins and differentiated positioning in these segments.

Market Segmentation Analysis

By Type

Facultative Reinsurance's Adaptability for Unique, High-Value Risks Leads to Its Dominant Market Share

The market is segmented by type into facultative reinsurance and treaty reinsurance.

Facultative Reinsurance

The Facultative reinsurance segment led the market, accounting for 57.33% market share in 2026, as it is traditionally known for playing an important role in managing specific, high-value, or unique individual risks on a case-by-case basis. This type of business reflects the reinsuring of distinct insurable policies or transactions, where a separate underwriting judgment is needed for every case. Its greater share can be attributed to its ability to adapt and accurately provide solutions for unique risks that make little sense in a standard treaty context. It is still an essential solution for complex or one-off exposures in a variety of lines of business.

Risk-specific underwriting requirements provide the foundation for facultative reinsurance demand. This segment addresses individual exposures requiring bespoke evaluation, particularly where insured values, technical complexity, or accumulation risks exceed standard treaty parameters. Large infrastructure projects, aviation risks, energy assets, and specialized liability exposures frequently rely on facultative arrangements because underwriting decisions are tailored to each submission.

Capacity flexibility remains one of the segment's key advantages. Cedents often seek facultative support when managing unusual risks or securing additional protection beyond existing treaty limits. This approach enables insurers to maintain underwriting relationships while limiting concentration risk and preserving capital efficiency.

Claims severity trends and inflationary pressures have increased the relevance of facultative structures. Complex commercial risks and high-value assets require detailed risk assessment, encouraging closer collaboration between cedents and reinsurers. Pricing considerations increasingly reflect engineering expertise, exposure modeling, and geographic characteristics.

Treaty Reinsurance

At the same time, treaty reinsurance is growing considerably faster, having delivered the highest CAGR due to its automatic coverage for the classes of business defined in the treaty that the primary insurer cedes over a certain period. It allows insurance companies to hand off enormous amounts of homogeneous risks without the need to negotiate for each policy, leading to faster growth. Its growth characteristics arise from the increasing volume of written insurance business in emerging markets or new business product lines, where treaties provide essential capacity and stability to underwriting results, making treaty reinsurance the fastest-growing component.

Portfolio-wide risk transfer objectives underpin the dominance of treaty reinsurance within the global reinsurance market. Unlike facultative structures, treaty arrangements provide automatic coverage for predefined classes of business, enabling insurers to manage volatility and optimize capital utilization across broad portfolios. Such structures support underwriting consistency and enhance scalability.

Capital management considerations strongly influence treaty demand. Primary insurers increasingly rely on quota share, surplus, and excess-of-loss treaties to stabilize earnings and improve solvency ratios. These mechanisms enable cedents to expand business volumes while maintaining acceptable risk retention levels.

Market conditions and catastrophe activity significantly affect treaty pricing. Elevated claims severity and changing exposure profiles have encouraged reinsurers to emphasize underwriting discipline and tighter terms. Portfolio quality and historical performance increasingly determine access to capacity and pricing outcomes.

By Application

To know how our report can help streamline your business, Speak to Analyst

Nature of Frequent and Severe Claims in Property, Casualty, and General Insurance Drives Dominance of Non-Life Reinsurance

The market is segmented by application into life reinsurance and non-life reinsurance.

Life Reinsurance

By application, the non-life reinsurance segment is projected to dominate the market with a share of 67.05% in 2026, as it covers the risks associated with property, casualty, and other general insurance lines. These broader types of cover allow for a higher frequency (and randomness) of claims that require the reinsurance capacity needed to stabilize any insurer, particularly due to catastrophes or liability exposures across the spectrum of coverage types.

Demographic evolution and rising protection requirements are reshaping the strategic importance of life reinsurance across global insurance markets. Aging populations, longevity improvements, and increasing healthcare expenditures are creating more complex liabilities for primary insurers, prompting greater reliance on external capital support and actuarial expertise. These structural factors continue to influence reinsurance market growth within long-duration business lines.

Balance sheet optimization remains a major consideration for cedents operating in life insurance segments. Mortality, longevity, morbidity, and lapse risks require sophisticated portfolio management approaches that often extend beyond internal retention capabilities. Reinsurance arrangements enable insurers to improve capital efficiency, stabilize earnings, and accelerate product innovation without materially increasing risk concentrations.

Expansion of insurance penetration across emerging economies is creating additional demand for life reinsurance solutions. Rising household incomes and growing awareness regarding financial protection are supporting sales of life, health, and retirement products. Reinsurers possessing advanced underwriting capabilities and experience in product development increasingly serve as strategic partners rather than solely capacity providers.

Non-Life Reinsurance

In contrast to non-life reinsurance, life reinsurance has witnessed the greatest shift in the global market during the study period. Life reinsurance carries the highest CAGR across the application segment because of increased life expectancy, rising disposable income in developing countries, and the overall acceptance of life and health insurance-related products. The rise of pension funds, the evolution of new annuity products, and the need for reinsurers to manage risks related to longevity and mortality have also been key contributors.

Exposure accumulation and catastrophe volatility make non-life reinsurance the largest and most dynamic segment within the global reinsurance market. Property, casualty, cyber, marine, aviation, engineering, and specialty risks collectively generate substantial demand for risk transfer capacity. Claims severity and inflationary pressures have elevated the strategic importance of portfolio diversification and disciplined underwriting practices.

Natural catastrophes continue to exert a strong influence on capacity deployment and pricing behavior. Hurricanes, floods, wildfires, severe convective storms, and secondary perils have increased uncertainty across many regions, encouraging insurers to seek greater protection against earnings volatility. Reinsurers with diversified geographic exposure and strong capital positions are generally better positioned to manage these risks.

Commercial insurance expansion provides another source of growth. Infrastructure investments, renewable energy projects, digital assets, and supply chain complexity are creating new categories of insured exposures requiring specialized expertise. Cyber insurance and climate-related risks have emerged as particularly attractive areas for differentiated underwriting capabilities.

Regional Market Insights

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe Reinsurance Market Analysis:

Europe Reinsurance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The European market generated USD 230.22 billion in 2025, representing 37.00% of the global market landscape, and is expected to reach USD 246.45 billion in 2026. Europe commands the largest market share, aided by a strong presence of global reinsurers, primarily from Switzerland or Germany. The insurance markets are well developed, and the regulations (such as Solvency II) are stringent, demanding sound risk management practices and reserves of capital, which provide an ecosystem for reinsurance demand. A variety of risks, such as natural catastrophes, liability, and large commercial lines underwriting demand, are backed by a strong local network of primary insurers and reinsurers to support their risk management needs. The European insurance industry has some great growth potential in niche products and technology, but it is also dealing with tough competition and the evolving challenges that come with climate risks.

Regulatory sophistication and established insurance ecosystems underpin Europe's position within the reinsurance market. Solvency frameworks encourage efficient capital utilization and support demand for structured risk transfer solutions. Climate-related losses and specialty lines continue shaping underwriting strategies. Global reinsurers headquartered in Europe maintain strong international diversification, contributing to sustained reinsurance market growth and competitive depth.

Germany Reinsurance Market:

Germany is the largest economy in Europe and is critical to the market since it accommodates many leading players and is one of the key underwriting market centers. Germany has a solid industrial base and a comprehensive commercial insurance market.

Germany faces different types of risks, from natural catastrophes to complicated commercial business lines. These factors all help to expand a strong demand for reinsurance. German firms are very well respected in terms of their financial stability, technical expertise, and global reach, and they play a significant role in the market both at home and abroad. These firms frequently are at or near the top of treaty-reinsurance agreements throughout Europe or within a sophisticated global approach. The UK market is projected to reach USD 50.25 billion by 2026, while the German market is projected to reach USD 65.06 billion by 2026.

Germany occupies an influential position within the reinsurance market through its concentration of globally significant reinsurers and advanced actuarial expertise. Industrial risks, specialty lines, and international diversification support underwriting activity. Climate adaptation initiatives and evolving regulatory expectations increasingly influence portfolio strategies. Strong analytical capabilities continue to reinforce Germany's contribution to the reinsurance market share worldwide.

United Kingdom Reinsurance Market:

International underwriting expertise and London's position as a specialty insurance hub continue to support the United Kingdom reinsurance market. Complex commercial risks, marine exposures, and specialty lines contribute significantly to ceded business volumes. Innovation in alternative risk transfer and cyber insurance remains important. Strong broker networks and global connectivity continue to support long-term market development.

North America Reinsurance Market Analysis:

In 2025, North America represented USD 215.35 billion, accounting for 34.70% of the worldwide market, and is projected to grow to USD 232.47 billion in 2026.

North America is one of the largest and most active markets in the world, especially in the U.S. The market in the U.S. is substantially large and active. It also has a large number of opportunities for reinsurance, especially in the property-casualty sector. The potential exposure to significant natural disasters, from hurricanes to earthquakes, generates massive demand for reinsurance. In this environment, primary insurers are seeking options in the market to help insulate themselves from their risk and to increase their capacity, backed up with a solid financial situation.

Capital concentration and mature insurance penetration continue to support North America's leadership within the reinsurance market. Catastrophe exposure, specialty insurance demand, and sophisticated capital management practices sustain strong reliance on reinsurance solutions. Alternative capital participation and advanced risk modeling capabilities further enhance market depth. Pricing discipline and elevated catastrophe losses continue shaping reinsurance market growth across the region.

Market dynamics and pricing trends in North America are considerably influenced by factors of regulation, competition, and frequency and severity of catastrophic loss events. The U.S. market is projected to reach USD 194.07 billion by 2026.

United States Reinsurance Market:

The United States represents the largest contributor to the reinsurance market size due to substantial insured values and high catastrophe exposure. Property and casualty lines account for a significant share of ceded premiums. Hurricane activity, liability inflation, and cyber risk expansion continue influencing underwriting priorities. Strong capital markets and alternative risk transfer mechanisms reinforce the country's strategic importance.

Asia-Pacific Reinsurance Market Analysis:

Asia Pacific contributed 22.70% to the global market in 2025, with a valuation of USD 140.95 billion, and is projected to reach USD 156.22 billion in 2026. Asia Pacific is the fastest-growing market in the world, supported by significant economic growth, increasing disposable incomes, growing middle classes, and rising insurance penetration throughout many developing countries. China and India are both huge, under-exploited markets with significant long-term value for both primary insurers and reinsurers.

Economic expansion and increasing insurance penetration are strengthening the Asia-Pacific's importance within the reinsurance market. Natural catastrophe exposure and rising asset values support demand for risk transfer solutions. China, Japan, India, and Southeast Asia remain important growth centers. Infrastructure development and expanding middle-class populations continue contributing to long-term reinsurance market growth throughout the region.

The growth is influenced by a vast array of risks, especially related to infrastructure development, natural catastrophes in vulnerable environments, and growing life and health insurance markets. Reinsurers, while becoming increasingly focused on the Asia Pacific to provide capacity, expertise, and solutions, face a range of regulatory and market maturity issues. The Japan market is projected to reach USD 30.51 billion by 2026, the China market is projected to reach USD 49.12 billion by 2026, and the India market is projected to reach USD 17.85 billion by 2026.

Japan Reinsurance Market:

Earthquake exposure and a mature insurance sector define Japan's position within the reinsurance market. Catastrophe protection requirements remain a primary source of ceded premium demand. Aging demographics also support life reinsurance activity. Advanced catastrophe modeling capabilities and strong risk awareness continue to reinforce Japan's strategic significance within global reinsurance market trends and capital allocation.

China Reinsurance Market:

Rapid insurance sector expansion and increasing economic complexity are elevating China's role within the reinsurance market. Property, health, and agricultural insurance growth continue driving demand for capacity and technical expertise. Domestic market development and regulatory modernization are reshaping competitive dynamics. Rising insured assets and urbanization continue to strengthen long-term reinsurance market growth prospects.

Middle East & Africa Reinsurance Market Analysis:

The Middle East & Africa market was valued at USD 13.48 billion in 2025, capturing 2.20% of global revenue, and is estimated to reach USD 14.68 billion in 2026. The Middle East & African markets are continuously developing as a result of economic diversification, infrastructure development, and an increasing awareness of the importance of risk management.

Economic diversification and infrastructure development continue to strengthen the Middle East & Africa reinsurance market. Energy risks, construction activity, and catastrophe exposures support demand for reinsurance capacity. Insurance penetration remains comparatively low, creating long-term opportunities. Regulatory modernization and expanding financial sectors continue contributing to sustained reinsurance market growth across both regions.

In the Middle East, countries in the GCC (Gulf Cooperation Council) continue to reinforce their regulation while also investing in insurance penetration within their regions, which provides opportunities for regional and international reinsurers. Meanwhile, as climate change increases the risks of natural disasters, the African market is benefiting from the increasing appetite for agricultural, health, and catastrophe reinsurance. There are also challenges for both regions, especially limited insurance literacy and political instability in some areas.

South America Reinsurance Market Analysis

The South America region captured 3.40% of the global market in 2025, generating USD 21.4 billion in revenue, and is projected to reach USD 23.46 billion in 2026. The South American market has both potential and challenges related to volatility and development. Various types of instability are involved, such as economic, currency, and inconsistent regulatory situations across many countries, which impact reinsurance market growth and the risk appetite for reinsurers.

South America does have some positive aspects, including many emerging economies, increasing insurance penetration in certain countries, and growing awareness of the necessity of transferring risk, particularly evident in property and casualty lines and among large corporate clients. Tapping into long-term growth opportunities will likely depend on this localized knowledge, particularly in areas where treaty reinsurance is essential for building capacity.

Reinsurance Industry Competitive Landscape

KEY INDUSTRY PLAYERS

Players Leverage Diversification and Innovation to Underwrite Complex Risks Across the Market Effectively

The market's competitive landscape features both robust global firms and nimbler regional providers. These providers appear well-positioned to continue providing the full range of risk management options for a variety of risks. Key players in the market include Munich Re, Swiss Re, Hannover Re, SCOR, and Berkshire Hathaway, which all have a considerable global operating presence and a breadth of diversifying insurance and reinsurance portfolios. These leading firms are able to utilize developing risk modeling capabilities with robust capital, geographic reach, and overall risk tolerance. This is for underwriting complex risks in a variety of property and casualty insurance markets, as well as life and specialty risks. Leading providers rely on joint ventures, digital initiatives, and geographic expansion as competitive advantages.

Competitive intensity within the reinsurance market is shaped by capital strength, underwriting discipline, geographic diversification, and analytical capabilities. Unlike primary insurance markets, scale alone does not determine competitive advantage. Portfolio quality, catastrophe exposure management, and access to alternative capital increasingly influence long-term profitability and market positioning. Reinsurers are prioritizing return on equity and capital efficiency over premium expansion, reflecting a more disciplined approach following several years of elevated catastrophe losses and inflation-driven claims severity.

Large global participants continue to account for a significant share of the reinsurance market size. Munich Re, Swiss Re, Hannover Re, SCOR, Berkshire Hathaway Reinsurance Group, Lloyd’s market participants, Everest Group, RenaissanceRe, PartnerRe, and Arch Capital maintain strong competitive positions through diversified portfolios and extensive underwriting expertise. Geographic diversification and broad product offerings enable these firms to manage earnings volatility more effectively and preserve balance sheet resilience across underwriting cycles.

Capital management has become an increasingly important differentiator. Firms possessing strong credit ratings and conservative reserve practices enjoy greater pricing flexibility and stronger relationships with cedents. At the same time, alternative capital sources, including catastrophe bonds and Insurance-Linked Securities (ILS), continue influencing capacity availability and competitive dynamics across catastrophe-exposed segments.

Top Reinsurance Companies Analyzed:

- Munich Re (Germany)

- Swiss Re (Switzerland)

- Berkshire Hathaway Reinsurance Group (U.S.)

- Hannover Re (Germany)

- Lloyd’s (U.K.)

- SCOR (France)

- Reinsurance Group of America – RGA (U.S.)

- Great West Lifeco (Canada)

- Everest Re (Bermuda)

- Arch Capital Group (Bermuda)

- PartnerRe (Bermuda)

- RenaissanceRe (Bermuda)

- Mapfre Re (Spain)

- China Re (China)

- Allianz SE Re (Germany)

- MS&AD Insurance Group (Japan)

- Transatlantic Re (U.S.)

- Chubb Tempest Re (Bermuda)

- GIC Re (India)

- Sompo International (Bermuda)

Latest Reinsurance Industry Developments:

- December 2025: Munich Re launched its Ambition 2030 strategy to support profitable growth and address emerging risks, including artificial intelligence, cyber threats, renewable energy, and space-related exposures. Technologies and capabilities involved included AI-related risk solutions, cyber underwriting capabilities, and specialty risk expertise.

- February 2026: Munich Re reported a record net profit of €6.1 billion for 2025, supported by strong underwriting performance and sustained demand across reinsurance markets. Technologies and capabilities involved included advanced risk modeling and diversified reinsurance operations.

- December 2025: Swiss Re introduced a refreshed corporate strategy and established a USD 4.5 billion net income target for 2026, focusing on portfolio resilience and productivity improvements. Technologies and capabilities involved included AI-enabled productivity initiatives and portfolio optimization capabilities.

- February 2026: Swiss Re reported a record 2025 net income of USD 4.8 billion, driven by strong property and casualty reinsurance performance. Technologies and capabilities involved included catastrophe modeling and enterprise risk management frameworks.

- September 2025: Hannover Re raised its earnings guidance following strong business performance and improved reserve resilience. Technologies and capabilities involved included reserve analytics, underwriting models, and capital management capabilities

REPORT COVERAGE

The report provides a detailed analysis of the current market condition and focuses on key aspects such as leading reinsurance companies, types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Application

By Region

|

|

Companies Profiled in the Report |

Munich Re (Germany), Swiss Re (Switzerland), Berkshire Hathaway Reinsurance Group (U.S.), Hannover Re (Germany), Lloyd’s (U.K.), SCOR (France), Reinsurance Group of America – RGA (U.S.), Great West Lifeco (Canada), Everest Re (Bermuda), Arch Capital Group (Bermuda) |

Frequently Asked Questions

The market is projected to reach USD 1403.7 billion by 2034.

In 2025, the market was valued at USD 621.39 billion.

The market is projected to grow at a CAGR of 9.6% during the forecast period.

The facultative reinsurance segment is expected to lead the market in terms of revenue.

As insurance needs evolve and risks grow more complex, demand for innovative reinsurance solutions continues to accelerate market growth.

Munich Re, Swiss Re, Berkshire Hathaway Reinsurance Group, and Hannover Re are the markets top players.

Europe is expected to hold the highest market share.

By application, life reinsurance is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us