Crystalline Polyethylene Terephthalate Market Size, Share & Industry Analysis, By Product (Trays & Containers, Cups & Lids, Films & Sheets, and Others), By End-Use Industry (Food & Beverage, Pharmaceutical, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

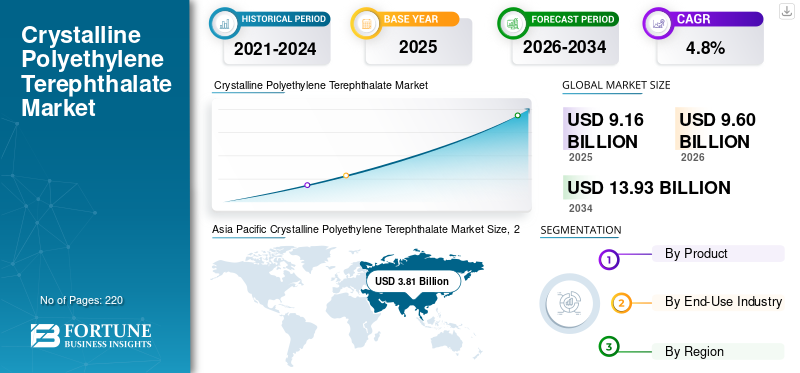

The global crystalline polyethylene terephthalate market size was valued at USD 9.16 billion in 2025. The market is projected to grow from USD 9.60 billion in 2026 to USD 13.93 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the global crystalline polyethylene terephthalate market with a share of 41.59% in 2025.

Crystalline Polyethylene Terephthalate (CPET) is a semi-crystalline thermoplastic polymer known for its high thermal stability, rigidity, and dimensional consistency, making it suitable for applications that require resistance to elevated temperatures and structural reliability. Its commercial production relies on the polymerization of purified terephthalic acid and monoethylene glycol, followed by controlled crystallization to develop heat-resistant molecular structure. CPET is widely used in ovenable and microwaveable food packaging, where it maintains shape under high temperatures and supports safe food contact performance. Its strength, chemical resistance, and barrier properties also enable use in trays, containers, lids, and specialty packaging formats. These products are manufactured through the processes of injection molding or thermoforming. These processes precisely control crystallinity levels, which improves heat resistance but requires higher processing temperatures, greater energy consumption, and stricter process control compared to PET materials.

Furthermore, the market encompasses several key players, including Amcor plc, Pactiv Evergreen Inc., NOVAPET S.A., SABIC, and Eastman Chemical Company, which are at the forefront. A broad product portfolio, expansion of production capacities, and a strong geographical presence have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

CRYSTALLINE POLYETHYLENE TEREPHTHALATE MARKET Key Takeaways

- 2025 Market Size: USD 9.16 billion

- 2026 Market Size: USD 9.60 billion

- 2034 Forecast Market Size: USD 13.93 billion

- CAGR: 4.8% from 2026–2034

- Asia Pacific dominated the global crystalline polyethylene terephthalate market with a share of 41.59% in 2025.

- The films & sheets segment holds a steady share of the CPET market and is set to grow at a CAGR of 4.6% over the forecast period.

- The food and beverage segment dominates the market and is projected to grow at a CAGR of 4.7% during the forecast period.

Asia Pacific

The Asia Pacific region held a dominant share of the market in 2025, valued at USD 3.81 billion, and continued to maintain a strong position in 2026, with USD 4.02 billion.

North America

North America is projected to grow at a rate of 4.2% during the forecast period and reach a valuation of USD 2.08 billion by 2026.

Europe

The market in Europe is estimated to reach USD 2.39 billion in 2025 and is expected to grow significantly during the forecast period.

U.S.

The U.S. is expected to record a valuation of USD 1.67 billion in 2026, driven by its large food processing industry and the widespread use of CPET trays and containers.

Japan

Japan is one of the major economies supporting Asia Pacific market growth through the expansion of food processing and packaging industries.

Read More

CRYSTALLINE POLYETHYLENE TEREPHTHALATE MARKET TRENDS

Shift toward Lightweight and Design-Optimized CPET Packaging

The CPET market is seeing a shift toward lightweight and design-optimized packaging solutions as manufacturers aim to reduce material usage while maintaining heat resistance and strength. Packaging producers are refining tray geometry, wall thickness, and rib designs to achieve the required thermal performance with lower resin consumption. Advances in mold design and thermoforming precision support consistent quality and improved aesthetics. This trend helps food processors reduce packaging weight, transportation costs, and overall material intensity. The growing focus on lightweight yet functional CPET formats reflects a clear move toward efficiency-driven product design rather than increased material use.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Heat-Resistant and Convenient Food Packaging Solutions to Propel Industry Expansion

Crystalline polyethylene terephthalate is increasingly used in food packaging as it provides high thermal stability, rigidity, and shape retention under elevated temperatures. In ready-meal and frozen food packaging, CPET trays and containers enable products to transition directly from the freezer to the oven or microwave without warping, ensuring safe and reliable performance. Its controlled crystallinity supports consistent wall thickness, strength, and dimensional accuracy, which are essential for automated filling, sealing, and reheating processes. CPET also offers good barrier properties and compliance with food-contact standards, supporting use in bakery products, airline catering, and convenience foods. The demand for ready-to-eat meals, frozen foods, and foodservice packaging is rising driven by urbanization and changing consumer lifestyles. This is pushing the use of CPET as a functional packaging material that enhances durability, safety, and processing efficiency, which is expected to drive the crystalline polyethylene terephthalate market growth.

- According to the U.S. Department of Agriculture (USDA, 2024), the retail sales of frozen foods in the U.S. exceeded USD 70 billion in 2023. This reflects strong and sustained consumer demand for ready-to-eat and convenience food products that rely heavily on heat-resistant packaging solutions such as CPET.

MARKET RESTRAINTS

Volatile Raw Material Prices and High Energy Costs May Restrict Market Growth

The CPET market faces a major restraint due to its dependence on petrochemical raw materials such as purified terephthalic acid and monoethylene glycol. The price volatility in crude oil and natural gas directly affects feedstock costs, creating uncertainty in production and pricing. In addition, CPET manufacturing is energy-intensive, as it requires higher processing temperatures and controlled crystallization compared to conventional PET. The rising electricity and fuel costs further increase overall production expenses. Environmental regulations related to emissions, energy efficiency, and plastic waste management also add to compliance costs. Together, these factors increase the cost pressure on manufacturers and limit adoption in price-sensitive applications, thereby restricting the overall market growth.

MARKET OPPORTUNITIES

Growing Use of CPET in Pharmaceutical and Institutional Packaging to Open Doors to New Avenues

CPET presents new opportunities in pharmaceutical and institutional packaging applications that require strength, heat resistance, and dimensional stability. CPET can withstand elevated temperatures and handling without deformation, making it suitable for medical trays, diagnostic packaging, and hospital food service applications. Its rigidity supports safe storage, transport, and controlled heating. As pharmaceutical manufacturing and healthcare facilities continue to expand, the demand is rising for reliable packaging materials that meet quality and hygiene standards. As packaging needs become increasingly application-specific, the growing use of crystalline polyethylene terephthalate beyond food packaging is expected to create new opportunities for market growth.

MARKET CHALLENGES

Limited Processing Flexibility and High Technical Requirements for CPET Production

The CPET market faces a significant challenge due to the technical complexity of achieving consistent crystallinity and thermal performance during production. Many manufacturers rely on conventional PET processing lines that are not designed for the precise control of crystallization, which limits output quality. This constraint affects uniformity in thickness, rigidity, and heat resistance, which are critical for ovenable and microwaveable packaging applications. As food and pharmaceutical packaging users demand tighter quality tolerances and reliable high-temperature performance, producers must invest in specialized equipment and process expertise.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product

Trays & Containers Segment Led the Market Driven by High Adoption in Microwaveable and Ovenable Food & Beverage Packaging

Based on product, the market is classified into trays & containers, cups & lids, films & sheets, and others.

The trays & containers segment held the dominant crystalline polyethylene terephthalate market share in 2025, supported by its widespread use in ovenable and microwaveable food and beverage packaging. CPET trays and containers offer high thermal stability, rigidity, and dimensional integrity, making them suitable for ready-to-eat meals, frozen foods, and airline catering applications. Their ability to withstand high temperatures without deformation, combined with good barrier performance and recyclability, supports consistent demand from food processors and packaging manufacturers. With the growing consumption of convenience foods and ready meals, this segment is expected to remain the leading product category during the forecast period.

The films & sheets segment holds a steady share of the CPET market and is set to grow at a CAGR of 4.6% over the forecast period. This is supported by applications in thermoforming, specialty packaging, and industrial uses requiring heat stability and rigidity. CPET films and sheets provide higher thermal resistance than conventional PET, enabling performance in high-temperature forming and packaging environments. They are widely used as base materials for the downstream manufacturing process of trays, lids, and rigid components. The ongoing demand from packaging converters and specialty processors supports stable consumption across food and industrial packaging applications.

By End-Use Industry

Food & Beverage Segment Leads the Market Propelled by Extensive Product Usage for Packaging Ready-to-Eat Foods

Based on end-use industry, the market is segmented into food & beverage, pharmaceutical, and others.

To know how our report can help streamline your business, Speak to Analyst

The food and beverage segment dominates the market, driven by the extensive use of CPET in packaging for ovenable, microwaveable, and ready-to-eat foods. CPET trays, containers, and lids are widely used for frozen meals, bakery products, ready meals, and airline catering due to their ability to withstand high temperatures while maintaining shape and structural integrity. The material also supports food safety, portion control, and compatibility with automated filling and sealing lines. The rising consumption of convenience foods, increasing demand for ready meals, and growth in food service packaging continue to drive the adoption of CPET. As a result, the food and beverage segment is expected to remain the largest consumer and is projected to grow at a CAGR of 4.7% during the forecast period.

The pharmaceutical segment holds a steady share of the CPET market, supported by the demand for packaging solutions that require dimensional stability, chemical resistance, and controlled thermal performance. The segment is poised to expand at a CAGR of 5.2% over the analysis period. CPET is used in trays, blister components, and specialized packaging where strength and reliability are critical during storage, transportation, and sterilization processes. The growing pharmaceutical production and emphasis on safe, durable packaging continue to support consistent demand from this segment, which accounted for a 13.35% share in 2025.

Crystalline Polyethylene Terephthalate Market Regional Outlook

By geography, the market has been studied across North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Crystalline Polyethylene Terephthalate Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region held a dominant share of the market in 2025, valued at USD 3.81 billion, and continued to maintain a strong position in 2026, with USD 4.02 billion, and is expected to continue expanding over the forecast period. This is supported by the expansion of food processing and packaging industries across major economies, such as China, India, and Japan. Rapid urbanization, rising disposable incomes, and changing consumer lifestyles have increased the demand for ready meals, frozen foods, and convenience packaging, where CPET is widely used for ovenable and microwaveable applications. In addition, the presence of large-scale packaging manufacturers and the growing adoption of advanced thermoforming technologies further strengthen regional consumption. Together, these factors reinforce the leading share of Asia Pacific in the global CPET demand.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to witness steady growth in the market in the coming years. During the forecast period, the region is projected to grow at a rate of 4.2% and reach a valuation of USD 2.08 billion by 2026. The market demand in North America is mainly driven by strong consumption of ready meals, frozen foods, and convenience food products that require ovenable and microwaveable packaging. The U.S. leads the regional demand due to its large food processing industry and the widespread use of CPET trays and containers in retail and foodservice packaging. Canada maintains a stable demand, supported by its processed food sector and the increasing use of recyclable materials. Supported by these factors, the U.S. is expected to record a valuation of USD 1.67 billion, while Canada is projected to reach USD 0.42 billion in 2026.

Europe

The market in Europe is estimated to reach USD 2.39 billion in 2025 and is expected to grow significantly during the forecast period. In Europe, the U.K. and Germany represent a key market, supported by a strong demand from the ready-meal, frozen food, and foodservice packaging industries. The country’s growing consumption of convenience foods and well-developed retail food sector drives the use of CPET trays and containers for ovenable and microwaveable applications. Additionally, Europe’s broader bakery, airline catering, and processed food industries contribute to a consistent demand for heat-resistant packaging materials. With an increasing focus on food safety, quality packaging, and recyclability, the demand for crystalline polyethylene terephthalate remains stable across the region. In 2026, the U.K. and Germany markets are estimated to reach USD 0.44 billion and USD 0.55 billion, respectively.

Latin America

In 2026, the Latin America market is expected to record a valuation of USD 0.52 billion in the CPET market. The regional growth is supported by the expanding packaged food and food processing industries, where CPET is used for ovenable and microwaveable food packaging. Countries such as Brazil and Mexico remain key contributors, driven by the rising demand for ready meals and frozen food products. The increasing urbanization and gradual development of modern food retail channels further support the demand for CPET across the region.

Middle East and Africa

The Middle East and Africa market is expected to grow at a CAGR of 4.6% during the forecast period. Growth in the GCC is supported by the rising demand for packaged and convenience foods, as well as the increasing adoption of ovenable and microwaveable food packaging in urban areas. The expansion of food service, airline catering, and hospitality sectors further contributes to crystalline polyethylene terephthalate consumption across the region. In South Africa, the product demand is driven by the growing processed food industry and a gradual shift toward modern, heat-resistant packaging formats. Supported by these factors, the GCC market touched a valuation of USD 0.24 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Deploy Expansion Initiatives and Acquisitions to Enhance their Market Share

Large companies utilize their R&D capabilities, scale, and sustainability efforts to stay ahead of competitors, whereas regional players focus on proximity to local infrastructure projects and cost savings. Some of the prominent industry participants include Amcor plc, Pactiv Evergreen Inc., NOVAPET S.A., SABIC, and Eastman Chemical Company. These players are deploying strategies such as partnerships, takeovers, and expansion initiatives to gain market share.

LIST OF KEY CRYSTALLINE POLYETHYLENE TEREPHTHALATE COMPANIES PROFILED

- NOVAPET, S.A. (Spain)

- SABIC (Saudi Arabia)

- Mitsubishi Chemical Group (Japan)

- Amcor plc (Switzerland)

- Reliance Industries Limited (India)

- Eastman Chemical Company (U.S.)

- Indorama Ventures Public Company Limited (Thailand)

- Celanese Corporation (U.S.)

- Pactiv Evergreen Inc. (U.S.)

- NAN YA Plastics Industrial Co., Ltd. (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Indorama Ventures completed its takeover of CarbonLite Holdings’ PET recycling facility in Texas. The acquired site, known as Indorama Ventures Sustainable Recycling (IVSR), produces food-grade recycled PET (rPET) pellets, expanding the company’s PET recycling capacity.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.8% from 2026-2034 |

|

Unit |

Value (USD Billion), Volume (Kilotons) |

|

Segmentation |

By Product, End-Use Industry, and Region |

|

By Product |

· Trays & Containers · Cups & Lids · Films & Sheets · Others |

|

By End-Use Industry |

· Food & Beverage · Pharmaceutical · Others |

|

By Geography |

· North America (By Product, End-Use Industry, and Country) o U.S. o Canada · Europe (By Product, End-Use Industry, and Country) o Germany o U.K. o France o Italy o Spain o Rest of Europe · Asia Pacific (By Product, End-Use Industry, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Latin America (By Product, End-Use Industry, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product, End-Use Industry, and Country) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.16 billion in 2025 and is projected to reach USD 13.93 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 3.81 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period of 2026-2034.

The trays & containers segment led the market by product in 2025.

The key factors driving the market are the growing demand for heat-resistant packaging and the rising consumption of ready-to-eat and frozen foods.

Amcor plc, Pactiv Evergreen Inc., NOVAPET, S.A., SABIC, and Eastman Chemical Company are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

The rising demand for heat-resistant, rigid, and reliable packaging materials in ready-to-eat meals, frozen foods, and foodservice applications is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us