Curing Agents Market Size, Share & Industry Analysis, By Type (Epoxy, Polyurethane, Silicone Rubber, and Others), By End Use (Paints & Coatings, Adhesive & Sealants, Composites, Building & Construction, and Others), and Regional Forecast, 2026-2034

Curing Agents Market Size and Future Outlook

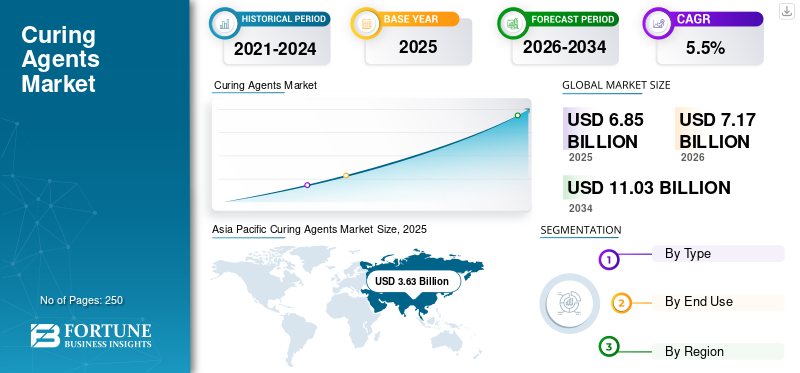

The global curing agents market size was valued at USD 6.85 billion in 2025. The market is projected to grow from USD 7.17 billion in 2026 to USD 11.03 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period. Asia Pacific dominated the curing agents market with a market share of 52.99% in 2025.

Curing agents are reactive chemicals added to resins to trigger crosslinking and convert liquid formulations into durable, high-strength thermoset materials. They are essential for achieving targeted properties such as hardness, adhesion, chemical resistance, heat stability, and corrosion protection, making them widely used in protective coatings. In addition, it is used in a wide range of industries, including construction, adhesives and sealants, composites, and electrical & electronics. Growing demand for curing agents in the global market is primarily driven by steady consumption of industrial maintenance coatings, expanding use of epoxy flooring, and increasing penetration of composites in energy.

The market is led by global chemical groups and specialty formulators that maintain strong positions through integrated production of key intermediates and broad portfolios of curing agents, including amines, amides, anhydrides, phenalkamines, and blends. Established major players such as Aditya Birla Chemicals, BASF, Huntsman Corporation, Olin Corporation, and Evonik Industries maintain market presence through integrated access to key feedstocks and intermediates.

Download Free sample to learn more about this report.

Curing Agents Market Key Takeaways

- 2025 Market Size: USD 6.85 Billion

- 2026 Market Size: USD 7.17 Billion

- 2034 Forecast Market Size: USD 11.03 Billion

- CAGR: 5.5% from 2026–2034

- Asia Pacific dominated the curing agents market with a 52.99% share in 2025.

- The epoxy segment accounted for the largest market share in 2025.

- The paints & coatings segment held the leading end-use market share in 2025.

Asia Pacific

Asia Pacific dominated the global market with a value of USD 3.63 billion in 2025 and is projected to reach USD 3.84 billion in 2026.

North America

North America reached USD 1.04 billion in 2025 and is expected to grow to USD 1.09 billion in 2026.

Europe

Europe was valued at USD 1.47 billion in 2025 and is projected to expand at a CAGR of 5.0% during the forecast period.

U.S.

The market is estimated at USD 0.97 billion in 2026, accounting for approximately 14% of global revenues.

Japan

Demand is supported by strong consumption of curing agents across coatings, construction, and industrial manufacturing applications.

Read More

CURING AGENTS MARKET TRENDS

Rising Shift Toward Low Emission and Safer Cure Chemistries to Strengthen Product Adoption

Industries are increasingly prioritizing curing agents that support lower emissions, improved workplace safety, and regulatory compliance while maintaining coating and composite performance. This trend is most evident in protective coatings, industrial flooring, and construction chemicals, where demand is rising for low odor systems, reduced free amine exposure, and formulations. Customers are also seeking curing packages that deliver predictable cure profiles, longer pot life control, and improved surface finish to reduce rework and failure rates in field applications. As sustainability targets expand across coatings and adhesives value chains, suppliers are strengthening their portfolios by combining performance with improved environmental and handling profiles, reinforcing long-term adoption.

- Companies such as BASF, Evonik Industries, and Huntsman Corporation continue to expand their performance-focused curing agent portfolios to align with evolving compliance requirements and the demand for high-performance products.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Protective Coatings and Infrastructure Rehabilitation to Drive Market Growth

The market is primarily driven by sustained demand for epoxy and polyurethane systems used in industrial maintenance, corrosion protection, and infrastructure rehabilitation. Curing agents are critical in enabling chemical resistance, adhesion strength, and long-term durability in applications such as pipelines, bridges, marine assets, industrial flooring, and tank linings. Rising refurbishment activity across aging infrastructure, increasing emphasis on asset life extension, and higher spend on industrial maintenance are supporting consistent consumption. In addition, growth in commercial and industrial construction is expanding the use of epoxy flooring and repair materials where cure reliability and mechanical strength are essential. Hence, steady consumption across maintenance and construction will drive the global curing agents market growth during the forecast period.

MARKET RESTRAINTS

Feedstock Volatility and Handling Constraints May Limit Market Expansion

Despite strong functional importance, the market faces constraints linked to raw material price volatility and chemistry-specific handling challenges. Many curing agents are tied to upstream cost swings in petrochemical chains, which can compress margins and disrupt contract pricing, particularly in price-sensitive coatings and construction formulations. In addition, certain amine-based systems face stricter transport, storage, and worker exposure requirements due to odor, sensitization risk, and hazard labeling, which place greater compliance burdens on applicators and smaller formulators. In mature markets, some buyers may shift toward alternative resin systems or lower-cost cure packages when performance requirements are less critical, limiting premiumization potential. These factors collectively moderate overall market expansion despite steady demand fundamentals.

MARKET OPPORTUNITIES

Growth in Wind Composites and Electrification Materials to Create Lucrative Opportunities

Wind energy composites and electrification-linked materials present strong growth opportunities as demand rises for high-performance thermosets with long service life and reliability. Curing agents tailored for composites are increasingly required to achieve toughness, fatigue resistance, and controlled reactivity for large structural components, supporting growth in wind blades and related composite parts. At the same time, increasing use of encapsulation and insulation systems in electrical and electronic components is expanding demand for curing agents that deliver thermal stability, dielectric strength, and consistent long-term performance. Suppliers with strong application engineering, consistent quality control, and tailored cure-profile design capabilities are well-positioned to capture higher-margin growth in these segments.

Segmentation Analysis

By Type

Epoxy Dominated Market Due to Strong Performance and Broad Industrial Use

Based on the type, the market is segmented into epoxy, polyurethane, silicone rubber, and others.

The epoxy segment accounted for the largest global market share in 2025, supported by its strong fit with high-performance formulations where adhesion, chemical resistance, and corrosion protection are critical. Epoxy-based systems remain widely preferred in protective coatings, industrial maintenance, and in construction flooring and repair applications where cure reliability and long service life are prioritized. Its broad formulation versatility across varied end-use conditions continues to reinforce its leadership in large-volume applications.

The polyurethane segment is expected to grow at a CAGR of 6.3% from 2026 to 2034, driven by expanding use in fast-curing coatings, adhesives, sealants, and elastomeric applications. Increasing demand from commercial construction, industrial flooring, and electrical and electronic protection materials is supporting higher consumption of polyurethane-compatible curing systems, especially where flexibility, abrasion resistance, and productivity-led cure profiles are required.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Paints & Coatings Dominated Due to High Consumption in Protective and Industrial Maintenance Applications

Based on the end use, the market is segmented into paints & coatings, adhesives & sealants, composites, building & construction, and others.

The paints & coatings segment accounted for the largest global curing agents market share in 2025, supported by sustained consumption of epoxy and polyurethane coating systems. The segment’s growth is driven by high utilization of coatings across industrial maintenance, infrastructure protection, marine environments, and corrosion-control programs. Curing agents remain essential to achieve film integrity, adhesion strength, and chemical resistance in high-performance protective coatings. The recurring nature of maintenance repainting cycles and the growing preference for longer-life coating systems will maintain the segment’s leadership.

The composites segment is expected to grow at the fastest pace, with a 6.3% CAGR over the forecast period. The growth is anticipated to be driven by the increasing use of thermoset systems in wind blades, structural components, and lightweight industrial parts. Curing agents are critical in controlling reactivity, toughness, and fatigue performance, which are essential for large composite structures exposed to cyclic loading and harsh outdoor conditions. The rising installation of wind capacity, along with the broader adoption of composites in transportation and industrial manufacturing, is driving the market.

The others segment is supported by specialty uses such as electrical and electronic potting, encapsulation, insulation, and niche industrial applications where long-term reliability is critical. Demand is further reinforced by industrial modernization and higher use of engineered materials in equipment manufacturing, where consistent cure behavior and performance retention under heat and chemical exposure are required. As a result, the segment is projected to grow steadily at a 4.9% CAGR over the assessment period.

Curing Agents Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Curing Agents Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 3.63 billion, and is projected to grow to USD 3.84 billion in 2026. The region’s leadership is supported by strong downstream demand from large-scale manufacturing economies led by China and India. Asia Pacific benefits from a deep base of epoxy and polyurethane consumption across protective coatings, construction chemicals, electronics, and expanding composites demand. Strong industrial activity, continued infrastructure build-out, and rising use of high-performance materials in transportation and energy applications further sustain demand for curing agents.

China Curing Agents Market

Based on Asia Pacific’s substantial contribution and China’s large-scale downstream consumption, the China market is expected to reach USD 2.08 billion in 2026, accounting for approximately 29% of global revenues. Demand is supported by heavy use of curing agents in industrial coatings, construction flooring and repair, electronics protection materials, and composites linked to energy and manufacturing.

India Curing Agents Market

The India market is expected to reach USD 0.36 billion in 2026, representing roughly 5% of global revenues. Demand is driven by growing consumption of protective coatings, construction chemicals, adhesives, and industrial maintenance solutions, supported by infrastructure expansion and rising manufacturing output.

North America

North America remains a significant regional market, reaching USD 1.04 billion in 2025 and expected to rise to USD 1.09 billion in 2026. Regional demand is supported by steady industrial maintenance spending, corrosion protection programs, and consistent use of epoxy and polyurethane systems in flooring, repair, and engineered adhesives. The region also benefits from strong specification-led coatings demand and higher adoption of performance-grade curing systems in regulated end uses.

U.S. Curing Agents Market

The U.S. market is estimated at USD 0.97 billion in 2026, accounting for approximately ~14% of global revenues.

Europe

The market in Europe reached a valuation of USD 1.47 billion in 2025 and is projected to grow at 5% over the coming years. The region represents a mature, regulation-driven market where high standards for durability, safety, and compliance in protective coatings, construction systems, and industrial manufacturing shape demand. Growth is supported by infrastructure refurbishment, industrial asset protection, and steady demand from high-value formulation segments.

Germany Curing Agents Market

The Germany market is expected to reach USD 0.32 billion in 2026, equivalent to around 4% of global revenues. Demand is supported by strong industrial coatings demand, engineered adhesives usage, and advanced manufacturing applications.

U.K. Curing Agents Market

The U.K. market is expected to reach USD 0.18 billion in 2026, accounting for approximately 3% of global revenues. Growth is supported by infrastructure maintenance activity, industrial coatings consumption, and consistent demand from construction chemicals and repair applications.

Latin America

Latin America reached a market valuation of USD 0.32 billion in 2025. Industrial maintenance requirements, construction activity, and the gradual expansion of protective coatings and flooring applications support regional demand. Availability of downstream formulation capacity and project-based demand cycles influence consumption patterns across the region.

Brazil Curing Agents Market

The Brazil market is expected to reach USD 0.15 billion in 2026, accounting for roughly 2% of global revenues. Protective coatings for industrial assets, construction flooring, and repair systems drive demand. The expanding use of adhesives and sealants in building and construction applications further supports regional growth.

Middle East & Africa

The Middle East & Africa’s estimated market valuation was worth USD 0.38 billion in 2025. The region represents a smaller but steadily developing market, supported by demand for protective coatings in harsh environments, ongoing construction activity, and industrial asset protection requirements. Growth is reinforced by energy and infrastructure projects that require durable coating systems and long-life repair materials, where curing agents are essential for performance reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

Oleochemical Integration and Formulation Capability Defines Competitive Strength

Competitive dynamics in the curing agents market are being reshaped by a clear set of strategic moves centered on expanding manufacturing presence, tightening customer alignment, and upgrading portfolios toward higher-value chemistries. Large suppliers are prioritizing regional footprint building to reduce lead times and improve supply reliability for coatings, construction chemicals, and polymer formulators. Capacity investments, such as Evonik’s specialty amines expansion in Nanjing, China, where demand for polyurethane and epoxy systems is growing. At the same time, companies are using acquisitions to accelerate market access and broaden advanced materials capabilities, illustrated by Aditya Birla Group’s purchase of Cargill’s specialty chemical facility. Collectively, these strategies are likely to raise entry barriers, increase share gains for globally scaled players, and push the market toward more specialized, performance-driven curing systems rather than commodity supply.

LIST OF KEY CURING AGENT COMPANIES PROFILED

- Aditya Birla Chemicals (India)

- BASF (Germany)

- China AAB Industry Technology Group (China)

- Ellecha Global Private Limited (India)

- Evonik Industries (Germany)

- Huntsman Corporation (U.S.)

- Jiangsu Sanmu Group (China)

- Jinan Ever-growing Rubber Additive Co., Ltd. (China)

- Miller-Stephenson Chemical Company, Inc. (U.S.)

- Olin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Aditya Birla Group successfully acquired Cargill Incorporated’s 17-acre specialty chemical manufacturing facility in Dalton, Georgia. With this acquisition, Aditya Birla has expanded its U.S. Advanced Materials business.

- March 2025: BASF and Sika introduced Baxxodur EC 151, a new amine building block for curing epoxy resins targeted at flooring and industrial coating The solution is positioned for low-emission formulations, reduced thinner need, and reliable curing performance at lower application temperatures, reinforcing the market shift toward performance plus regulatory readiness.

- November 2024: Evonik expanded its capacity for specialty amines at its facility located in Nanjing, China, to meet the increasing demand in the polyurethane and epoxy curing agent markets. The expansion has strengthened Evonik's position in China.

- September 2024: Evonik expanded its epoxy curing agent portfolio in the Americas with Ancamide 2853 and Ancamide 2865, highlighting nonylphenol-free chemistry and partial bio-based raw material content. The launch targets flexible and fast-return-to-service civil engineering and flooring applications where durability, movement tolerance, and safer labeling are increasingly required.

REPORT COVERAGE

The global curing agents market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.5% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, End Use, and Region |

| By Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 6.85 billion in 2025 and is projected to reach USD 11.03 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 3.63 billion.

Recording a CAGR of 5.5%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The paints & coatings end use segment led in 2025.

Expanding protective coatings and infrastructure rehabilitation are expected to drive market growth.

Aditya Birla Chemicals, BASF, Huntsman Corporation, Olin Corporation, and Evonik Industries are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Rising shift toward low-emission and safer cure chemistries to strengthen product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us