Solar Components Recycling Market Size, Share & Industry Analysis, By Component Type (Panels, Inverters, Electrical BOS, Structural BOS, and Others), By Material (Glass, Aluminum, Copper, Silicon, and Others), By End User (Utility-Scale, Commercial & Industrial, and Residential), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

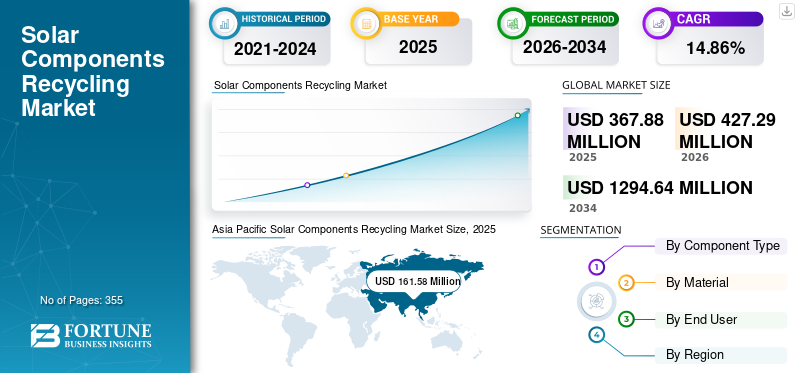

The global solar components recycling market size was valued at USD 367.88 million in 2025. It is projected to grow from USD 427.29 million in 2026 to USD 1,294.64 million by 2034, exhibiting a CAGR of 14.86% during the forecast period. Asia Pacific dominated the global solar components recycling market with a market share of 43.92% in 2025.

Solar component recycling refers to the systematic process of collecting, dismantling, and processing end-of-life or repowered Solar Photovoltaic (PV) system components to recover valuable materials and ensure environmentally responsible disposal. It covers a broad range of equipment, including solar panels, inverters, and electrical balance-of-system components such as cables and switchgear, as well as structural elements, such as mounting systems and trackers. The objective of solar component recycling is to maximize material recovery, including glass, aluminum, copper, silicon, and other metals, while minimizing landfill disposal and environmental impact. This activity plays a crucial role in supporting circular economy principles within the solar industry by reducing raw material dependency, enhancing resource efficiency, and facilitating regulatory compliance as large volumes of installed solar capacity reach the end of their operational life.

First Solar, Inc. is a leading player in the market due to its fully integrated, in-house recycling program. The company operates advanced recycling facilities capable of recovering a high percentage of glass and semiconductor materials from end-of-life modules. Its closed-loop recycling model enables recovered materials to be reused in new manufacturing processes, reducing reliance on virgin raw materials. First Solar’s early investment in recycling infrastructure has set industry benchmarks for sustainability, regulatory compliance, and the adoption of a circular economy within the global solar sector.

Download Free sample to learn more about this report.

Solar Components Recycling Market Key Takeaways

- 2025 Market Size: USD 367.88 million

- 2026 Market Size: USD 427.29 million

- 2034 Forecast Market Size: USD 1,294.64 million

- CAGR: 14.86% from 2026–2034

- Asia Pacific dominated the market with a 43.92% share in 2025.

- Panels segment is expected to dominate with a 40.32% share in 2025.

- Utility-scale segment is projected to lead with a 64.24% share.

North America

Projected to reach USD 78.17 million in 2026, driven by advanced recycling technologies and supportive regulations.

Asia Pacific

Valued at USD 161.58 million in 2025, driven by large solar installations and expanding recycling infrastructure.

Europe

Expected to reach USD 116.41 million in 2026, supported by strong recycling regulations and mature PV recycling systems.

U.S.

The U.S. market is projected to reach USD 68.76 million by 2026.

Japan

The Japan market is projected to reach USD 29.80 million by 2026.

Read More

SOLAR COMPONENTS RECYCLING MARKET TRENDS

Emergence of Advanced Recycling Technologies and Volume-Driven Scale to Lead Market Growth

A significant trend shaping the market is the rapid evolution and adoption of advanced recycling technologies in the solar power industry, driven by the increasing volume of end-of-life solar infrastructure. As global solar installations expand, the industry is transitioning from predominantly basic mechanical processes, such as shredding and simple material separation, to more advanced ones. This shift is toward more sophisticated thermal, chemical, and hybrid approaches that achieve higher material recovery rates and better preserve the quality of recovered silicon, metals, and glass. These advanced techniques are increasingly deployed to address the complex, multi-layer components and mixed materials found in modern PV modules and BOS elements, thereby improving economics by boosting the yield of high-value materials, such as silicon and copper. Meanwhile, growing-scale facility investments, including new plants with multi-GW annual processing capacity, are enabling recyclers to process ever-larger waste streams cost-effectively. Together, technological innovation and volume-driven economies of scale are shifting solar recycling from niche waste handling toward industrial-grade material recovery, aligning recycling capacity with expected surges in decommissioned solar infrastructure.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Increase in End-of-Life Solar Waste Volumes to Drive Market Growth

A primary driver for the solar components recycling market growth is the sharp rise in end-of-life solar equipment volumes worldwide. Solar PV systems typically operate for 25–30 years, and a large portion of installations commissioned during the early and mid-2010s are now entering repowering or retirement phases. As global installed solar capacity has crossed the multi-terawatt level, even small retirement rates translate into millions of tons of waste annually. This waste stream extends beyond panels to include inverters, cables, transformers, mounting structures, and trackers, many of which have shorter operational shelf life than modules. In utility-scale projects, repowering often occurs well before technical end-of-life to improve efficiency and returns, accelerating component replacement. The predictable and growing flow of retired solar components is creating a stable feedstock for recycling facilities, driving investment in collection, processing, and material recovery infrastructure, and transforming recycling from a compliance activity into a scalable industrial market.

Strengthening Environmental Regulations and Circular Economy Mandates to Propel Market Growth

The expansion of environmental regulations and circular economy policies is another major driver accelerating the market. Governments are increasingly recognizing solar waste as a future environmental challenge and are introducing regulations that require structured end-of-life management. Extended producer responsibility frameworks assign accountability to manufacturers and asset owners for the collection and recycling of solar equipment. In mature markets, mandatory recycling targets and reporting obligations are prompting solar stakeholders to adopt formal recycling channels rather than landfill disposal. Emerging markets are also introducing solar-specific waste rules as installed capacity grows rapidly, ensuring early development of compliant recycling ecosystems. These regulatory measures reduce uncertainty, create enforceable demand for recycling services, and support long-term planning for recyclers. As compliance requirements tighten and enforcement improves, recycling adoption is shifting from voluntary initiatives to a regulated necessity, directly supporting sustained market growth and investment.

MARKET RESTRAINTS

High Cost and Limited Economic Incentives for Recycling Infrastructure to Restrain Market Growth

A significant restraint on the market is the high cost of recycling infrastructure and uncertain economic incentives for operators. Recycling advanced materials, such as silicon, silver, and copper, at scale requires substantial capital investment in mechanical, thermal, and chemical processing technologies, as well as logistics networks for collection and transportation. In many regions, the value of recovered materials does not yet fully offset these costs, especially when commodity prices are low or volatile. For example, solar glass, which accounts for the majority of module mass, has a relatively low market value, making its recycling economically less attractive unless subsidies, regulatory mandates, or premium pricing for recycled content are in place. Without sufficient cost recovery mechanisms or strong Extended Producer Responsibility (EPR) frameworks, many recyclers struggle with narrow margins. This financial pressure can slow facility expansion, limit the adoption of advanced recovery technologies, and create market concentration in regions with stronger policy support, restraining broader global growth of the solar components recycling ecosystem.

MARKET OPPORTUNITIES

Strategic Partnerships and Circular Supply Chains to Offer Lucrative Opportunities for Market Growth

A major market opportunity exists in strategic partnerships among solar manufacturers, recyclers, and energy asset owners that facilitate the creation of circular supply chains and closed-loop material ecosystems. As the volume of solar components reaching end-of-life rises, manufacturers and project developers are increasingly entering recycling agreements to recover valuable materials and reintegrate them into new manufacturing lines. These collaborations improve the economics of recycling by securing steady feedstock flows, while also supporting solar companies in meeting their expanding Environmental, Social, and Governance (ESG) commitments and regulatory requirements related to extended producer responsibility. By aligning recycling operations with production and installation businesses, stakeholders can improve cost certainty for raw materials, reduce their dependency on virgin inputs, and reinforce their sustainable branding. The opportunity expands further when recyclers pair these partnerships with logistics networks and data-driven tracking systems to streamline collection and compliance reporting. In this way, circular supply chain models are emerging as a scalable commercial blueprint that enhances profitability while advancing decarbonization and resource efficiency goals across the solar industry.

MARKET CHALLENGES

Fragmented Collection Networks and Inconsistent Regulatory Frameworks to Hinder Market Growth

A major challenge facing the market is the fragmentation of collection systems and the patchwork of regulatory frameworks across jurisdictions. End-of-life solar systems are often dispersed across residential rooftops, commercial sites, and remote utility installations, which complicates the efficient aggregation and transportation of recyclable components. In many emerging markets, there is no formal infrastructure for retrieving decommissioned PV equipment, which leads to informal disposal or storage, delaying recycling activity. Furthermore, regulatory mandates for recycling vary significantly: some regions enforce strict take-back and reporting requirements, while others lack specific laws for solar components recycling altogether. This inconsistency increases the complexity of compliance for multinational recycling firms and creates uneven demand for structured recycling services. Standardizing certification, tracking, and extended producer responsibility programs across regions remains a challenge. Without coordinated frameworks and robust collection networks, the industry risks inefficiencies, higher logistics costs, and lost material recovery opportunities, hindering the scalability and sustainability of the solar components recycling market.

IMPACT OF TARIFF ON THE MARKET

Tariffs have a noticeable impact on the solar components recycling market by influencing both input costs and material recovery economics. Import duties on recycling equipment, spare parts, and processing chemicals can raise capital and operating costs for recycling facilities, particularly in emerging markets that rely on imported technology. At the same time, tariffs on primary raw materials such as aluminum, copper, and silicon can improve the relative competitiveness of recycled materials, indirectly supporting recycling demand. Trade barriers on solar modules may also accelerate domestic manufacturing and, over time, increase localized end-of-life volumes that require recycling. However, inconsistent tariff regimes across regions can distort cross-border movement of recyclable solar waste, increasing logistics complexity and compliance costs. Overall, tariffs create mixed effects, acting as both a cost pressure and a potential demand catalyst depending on regional trade and industrial policies.

SEGMENTATION ANALYSIS

By Component Type

Large Amount of Waste Generated by Panel to Lead its Market Share

By component type, the market is segmented into panels, inverters, electrical BOS, structural BOS, and others.

The panels segment commands the largest revenue share of 40.32% in 2025 in the market, as these panels constitute the largest volume of End‑Of‑Life (EoL) solar waste, being the core of any solar installation and having the highest cumulative installed base globally. Most recycling activity currently focuses on recovering materials such as glass, silicon, aluminum, and silver from panels due to the economic value of these constituents. Crystalline silicon panels make up the vast majority of installed capacity (often reported at 80‑90%+) and generate the largest waste stream as installations age. They command the largest share of recycling demand and infrastructure investment in the market. This strong dominance persists even as new recovery technologies (mechanical, thermal, chemical, and laser processes) evolve to improve material yield and reduce costs.

Inverters is the second leading segment with a CAGR of 15.16% in the market, as critical power electronics components that often fail or are replaced before the end of a panel’s lifespan, inverters contain valuable metals and electronics that warrant specialized recycling. The inverter recycling sector is emerging with a projected Compound Annual Growth Rate (CAGR) higher than the broader PV recycling market, as more stringent e‑waste regulations (especially in the EU under directives, such as WEEE) require structured disposal and recovery of electrical components. Europe currently leads this segment, with a significant share of inverter recycling activity, followed by North America. While exact percentage share figures vary by region and report, inverters typically represent a smaller proportion of the overall market compared to panels, but are gaining attention due to the higher electronic content per unit weight.

By Material

Easy Separation of Glass from the Waste Boosted the Glass Segment Growth

Based on material, the market is divided into glass, aluminum, copper, silicon, and others.

Glass segment dominates the market, accounting for 41.47% of the market share. Glass represents the largest share by volume in solar panel recycling, primarily due to its significant contribution to the overall weight of a typical photovoltaic module, which is typically around 70–75%. As panels reach the end of their life, glass is one of the easiest materials to separate and recycle through established glass recycling processes. This high material volume translates to significant activity in recycling facilities that crush, clean, and repurpose glass for use in new panels or other industrial applications. While its unit value per kilogram is lower than that of some metals, its sheer quantity gives glass a dominant position in the material recovery mix.

Silicon is the fastest growing segment in the market, expected to grow at a CAGR of 16.12% during the forecast period. Silicon, the core semiconductor material in most PV cells, constitutes a smaller share by weight but can represent one of the most valuable recycled materials when processed to high purity. Despite challenges in separating silicon cells from other panel layers, advancements in recycling techniques are improving recovery rates. As the volume of decommissioned silicon‑based panels grows with the expansion of the solar fleet, silicon’s share in material recovery is expected to rise, driven by demand from both photovoltaic manufacturing and electronics industries that value high‑grade silicon feedstock.

By End User

To know how our report can help streamline your business, Speak to Analyst

Significant Deployment in Large Scale Solar Projects to Lead Utility-Scale Segment Growth

As per end user, the global Solar Components Recycling market is broadly segmented into utility-scale, commercial & industrial, and residential.

Utility-scale accounts for the largest market share, at 64.24%, driven largely by large solar farms that generate the most significant volumes of end‑of‑life panels and related materials. These massive installations, often comprising tens of thousands to millions of panels, generate predictable and concentrated waste streams when they are decommissioned or upgraded. This concentration allows recyclers to achieve economies of scale in collection, transportation, and processing, making utility‑scale recycling efforts more cost‑effective and operationally efficient than smaller, dispersed systems. As a result, this segment frequently accounts for the largest portion of recycling demand and revenue, reflecting both the sheer volume of material and the structured logistics that large projects enable. According to recent market forecast, utility‑scale installations represent the dominant end‑use share in the solar panel recycling sector.

The commercial & industrial segment is set to grow at a CAGR of 15.71% during the forecast period and is the fastest growing segment among the end user. This category includes solar installations on office complexes, warehouses, manufacturing facilities, institutions, and other non‑residential properties. While the volume of panels from any single C&I project is typically less than utility farms, the cumulative volume is notable due to the broad adoption of solar in business and industrial applications. Many corporations and industrial facilities pursue recycling to align with sustainability goals, comply with environmental regulations, and manage lifecycle costs responsibly. This compliance‑driven adoption, coupled with moderate system sizes that still yield meaningful quantities of recyclable materials, sustains this segment’s solid market share.

SOLAR COMPONENTS RECYCLING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Solar Components Recycling Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the most dominating region in the market, valued at USD 161.58 million in 2025. The region is rapidly expanding and is expected to be one of the fastest‑growing markets, driven by massive installed capacity in China, Japan, and India. China’s vast solar fleet, exceeding hundreds of gigawatts, and increasing mandates for end‑of‑life management are generating substantial volumes of recyclable materials, while Japan and India are enhancing their recycling infrastructure to manage rising decommissioning streams. This combination of large installed bases and policy momentum positions the Asia Pacific for accelerated growth in the coming years. Leading countries, such as China, Japan, and India, are set to reach valuations of USD 85.33 million, USD 29.80 million, and USD 24.04 million, respectively.

North America

North America also holds a considerable position in the market, set to be valued at USD 78.17 million in 2026, primarily driven by the U.S. North America maintains a significant market position, driven by increasing end‑of‑life solar installations and growing regulatory support for circular economy practices. The regional market is also supported by investments in advanced recycling technologies and expanding processing infrastructure, particularly in the U.S. and Canada. The U.S. Department of Energy’s funding initiatives and state‑level mandates (such as California’s e‑waste regulations) are encouraging formal recycling programs for decommissioned modules and electrical components, setting the stage for continued growth through the decade. The U.S. is expected to hold a market value of USD 68.76 million in 2026.

Europe

Europe represents a significant and quality‐focused share, with a market value of USD 116.41 million in 2026, owing to robust policy frameworks and early adoption of photovoltaic technology. The European Union’s WEEE Directive and national extended producer responsibility laws require high collection and recovery rates for PV modules, making Europe the most mature recycling ecosystem worldwide. Countries such as Germany, France, Italy, and the U.K. are at the forefront, with Germany alone reporting strong year‑over‑year increases in recycled panel volumes and extensive certified recycling facilities. This regulatory environment ensures high material recovery rates and underpins Europe’s dominant share of recycling activity. Leading countries such as the U.K., Germany, and France are expected to have market values of USD 5.16 million, USD 38.02 million, and USD 11.13 million, respectively, by 2026.

Latin America

Latin America accounts for a modest solar components recycling market share of the global market, largely driven by Brazil, Mexico, and Chile, where expanding solar deployments and supportive renewable energy policies are increasing the volume of panels reaching the end of life. While specialized recycling infrastructure is still in its early stages, collaborations with global recyclers and national electronic waste regulations are helping to establish foundational processing capacity. Continued investment and scaling efforts, particularly in Brazil’s sizeable market, are expected to raise the region’s share over the next decade.

Middle East & Africa

The Middle East & Africa currently represent a modest share of the market, and are emerging as future growth regions. Countries such as the UAE, Saudi Arabia, and South Africa are increasingly investing in solar infrastructure as part of their broader energy diversification strategies, which will soon generate larger end‑of‑life waste streams that demand recycling solutions. While formal recycling ecosystems are less mature in the region than in Europe or North America, emerging pilot projects, public‑private partnerships, and integrated waste management policies reflect a growing regional commitment to sustainable solar lifecycle management. The region is expected to hold a market value of USD 26.38 million by 2026, with the GCC countries alone accounting for approximately USD 12.05 million in the same year.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players’ Increasing Investment in Material Innovation to Lead the Market Share

First Solar, Inc. plays a pioneering role in the solar components recycling market, leveraging its position as a leading thin-film PV manufacturer. The company has implemented a closed-loop recycling program in which it recovers nearly 90% of semiconductor and glass materials from its end-of-life modules, feeding them back into new production. First Solar continually invests in advanced recycling technologies and infrastructure, ensuring sustainable management of decommissioned panels while minimizing environmental impact. Their efforts reduce landfill waste and provide economic value through material recovery, setting a benchmark for industry-wide best practices. By integrating recycling into its business model, First Solar reinforces its commitment to the circular economy and long-term sustainability in solar energy.

List of the Key Solar Components Recycling Companies Profiled:

- First Solar, Inc. (U.S.)

- Reclaim PV Recycling (Australia)

- Enva (U.K.)

- Reiling GmbH & Co. KG (Germany)

- We Recycle Solar (U.S.)

- Canadian Solar Inc. (Canada)

- Silcontel Ltd. (Israel)

- SOLARCYCLE, Inc. (U.S.)

- Echo Environmental, LLC (U.S.)

- Rinovasol Global ServicesV. (Netherlands)

- The Retrofit Companies, Inc. (U.S.)

- PVRE Cycle / Resource Recycling (Belgium)

- Meyer Burger Technology AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, Envaris GmbH developed a hybrid recycling technique that combines thermal and mechanical methods to improve the recovery efficiency of silicon wafers and other valuable materials from end-of-life modules. This technical advancement aims to raise material yields and reduce processing costs.

- In March 2025, SolarCycle partnered with Veolia to establish a global solar panel recycling network that scales end-of-life processing across North America and Europe, enabling standardized logistics and increasing material recovery capacity in key markets. This collaboration reflects industry efforts to address the growing volume of decommissioned modules worldwide.

- In January 2025, PV Cycle announced a Europe-wide partnership with manufacturers to develop standardized logistics and Extended Producer Responsibility (EPR) frameworks for retired solar panels. The initiative aims to support compliance with increasingly stringent regulations and improve collection infrastructure across EU markets.

- In December 2024, Reclaim PV Recycling launched a second recycling facility in Brisbane, Australia, expanding capacity to process both monocrystalline and polycrystalline panels. This expansion supports regional growth in Asia Pacific recycling infrastructure and addresses rising solar waste streams from older installations.

- In June 2023, Orsted committed to fully recycle end-of-life solar modules from its U.S. portfolio by partnering with SolarCycle, marking one of the earliest strategic pledges by a major energy developer to integrate recycling throughout the asset lifecycle. This move set an early precedent for corporate circularity in the industry.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends & technologies and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.86% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component Type · Panels · Inverters · Electrical BOS · Structural BOS · Others |

|

By Material · Glass · Aluminium · Copper · Silicon · Others |

|

|

By End User · Utility-Scale · Commercial & Industrial · Residential |

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 367.88 million in 2025.

The market is likely to record a CAGR of 14.86% over the forecast period (2026-2034).

By end user, the utility-scale segment leads the market.

The Asia Pacific market size was valued at USD 161.58 million in 2025.

Rapid Increase in end-of-life solar waste volumes is the key factor driving the market.

Some of the top players in the market are First Solar, Veolia Environment, Reclaim PV Recycling, Enva, and others.

The global market size is expected to reach a valuation of USD 1,294.64 million by 2034.

- 2021-2034

- 2025

- 2021-2024

- 355

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us