Data Center Server Market Size, Share & Industry Analysis, By Server Type (General Purpose Servers, High-Performance Servers, Rack-Mounted Servers, Tower Servers, and Edge Servers), By Enterprise Type (Large Enterprises and Small & Medium Enterprises (SMEs)), By Application (IT & Telecommunications, BFSI, Government, Healthcare, Retail, Media & Entertainment, Energy, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

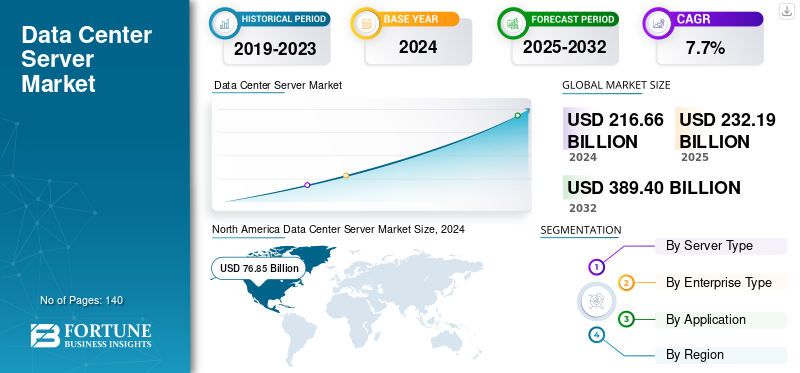

The global data center server market size was valued at USD 232.19 billion in 2025. The market is projected to grow from USD 249.18 billion in 2026 to USD 444.06 billion by 2034, exhibiting a CAGR of 7.49% during the forecast period. North America dominated the global market with a market share of 35.40% in 2025.

The global market refers to the revenue generated from server hardware used to process, store, and manage data within data centers. These servers are deployed across various industries, including IT and telecommunications, BFSI, government, healthcare, retail, media and entertainment, energy, and other commercial sectors. The market encompasses a range of server types, including general-purpose servers, high-density servers, rack-mounted servers, tower servers, and edge servers, and their subtypes, such as web or application servers, storage servers, database servers, HPC servers, AI servers, blade servers, and modular servers.

The key companies operating in the global market include Dell Technologies Inc., Hewlett Packard Enterprise Company, Lenovo Group Limited, Cisco Systems Inc., Huawei Technologies Co., Ltd., Inspur Co., Ltd., Super Micro Computer Inc., Quanta Computer Inc., Fujitsu Limited, and IBM Corporation.

Download Free sample to learn more about this report.

Data Center Server Market Key Takeaways

- 2025 Market Size: USD 232.19 billion

- 2026 Market Size: USD 249.18 billion

- 2034 Forecast Market Size: USD 444.06 billion

- CAGR: 7.49% from 2026-2034

- North America dominated the data center server market with a 35.40% share in 2025.

- General-purpose servers accounted for the largest share of 30.66% in 2026.

- Large enterprises held the largest share of 80.09% in 2026.

North America

North America accounted for USD 81.83 billion in 2025 and is projected to reach USD 87.25 billion in 2026.

Asia Pacific

Asia Pacific reached USD 77.39 billion in 2025 and is expected to grow to USD 84.27 billion in 2026.

Europe

Europe stood at USD 46.76 billion in 2025 and is projected to reach USD 49.42 billion in 2026.

U.S.

The market is estimated to reach USD 72.27 billion in 2026, accounting for approximately 29.8% of global revenue.

Japan

The market is estimated at USD 10.88 billion in 2026, representing approximately 4.5% of global revenue.

Read More

DATA CENTER SERVER MARKET TRENDS

Migration toward Accelerated and High-Density Architectures Fuels Market Expansion

A key market trend is the shift from traditional CPU-based servers to accelerated, high-density architectures designed for AI and advanced analytics.

- IDC reports that revenue for servers with embedded GPUs grew by 192.6% year over year in the fourth quarter of 2024, and these systems accounted for more than half of total server revenue for the year.

- Non-x86 servers, which include many accelerator-focused designs, also grew by more than 260% in the same period. These patterns show that accelerators are becoming a core element of mainstream server design and purchasing decisions.

The rapid expansion of AI workloads is also increasing power density in racks and shaping new facility requirements.

- According to the reports published by the International Atomic Energy Agency, data center electricity use was approximately 460 terawatt-hours in 2022 and is expected to exceed 1,000 terawatt-hours by 2026, comparable to Japan's current total power consumption.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Cloud and AI Infrastructure Drives the Market

Strong growth in cloud computing and AI workloads is a significant factor driving the data center server market growth.

Cloud providers and large enterprises are expanding their server capacity to support SaaS platforms, business applications, and the development of AI models.

- IDC noted that global server revenue reached approximately USD 77.3 billion in the fourth quarter of 2024, marking a 91% increase over the same period in 2023.

This suggests a sustained increase in server investments, rather than a routine replacement cycle.

AI-oriented architectures are further accelerating this growth.

- Revenue from servers equipped with GPUs rose by 192.6% year over year in the same quarter, and these systems accounted for more than half of total server revenue in 2024.

This trend indicates that AI is shifting demand toward higher-value, accelerator-rich server configurations. As a result, companies offering efficient GPU or accelerator-based systems are capturing a larger share of new market opportunities.

MARKET RESTRAINTS

Cost Pressures and Power Constraints to Hamper Market Development

The increasing cost and technical complexity of deploying high-performance servers are becoming significant restraints on the market.

AI-focused servers using GPUs are significantly more expensive than standard general-purpose systems and require substantial investments in cooling, power infrastructure, and advanced networking.

- Dell’Oro reported that these accelerated servers were the primary driver behind the 51% rise in global data center capital spending to USD 455 billion in 2024, highlighting how AI workloads are increasing overall deployment costs.

For many organizations, these higher costs can slow project timelines or reduce the scale of planned installations.

MARKET OPPORTUNITIES

Underpenetrated Markets and Efficiency-focused Innovation Create Significant Opportunity for the Market

A significant opportunity exists in the market for regions where digital activity is expanding faster than existing infrastructure can support.

- India is a leading example, as studies show the country produces about 20% of global data; however, holds only 1 to 3% of global data center capacities as of 2025.

- Additional industry estimates suggest that India’s capacity could nearly triple to around 3 gigawatts by 2030, driven by the growing adoption of AI, cloud services, and data localization policies. This imbalance between data generation and available capacity highlights strong potential for increased server deployments in emerging markets.

There is also a significant opportunity for companies that can enhance energy efficiency while supporting higher performance demands.

These conditions create strong market potential for advanced server designs, innovative cooling systems, and more efficient power architectures.

SEGMENTATION ANALYSIS

By Server Type

General-Purpose Servers (GPS) to Dominate Due to Versatility and Cost Efficiency

Based on server type, the market is divided into general-purpose servers, high-performance servers, rack-mounted servers, tower servers, and edge servers.

General-purpose servers comprise the largest segment globally with a share of 30.66% in 2026, as they handle a broad range of essential enterprise tasks, including database operations, virtualization, and collaboration applications. High-performance servers are expected to record the fastest growth of 9.0% due to rising demand for AI processing, large-scale analytics, and complex computational workloads.

To know how our report can help streamline your business, Speak to Analyst

By Enterprise Type

Large Enterprises to Lead Due to Complex Systems

Based on enterprise type, the market is segmented into large enterprises and SMEs.

Large enterprises account for the largest share globally with a share of 80.09% in 2026, as they operate complex and mission-critical systems that require substantial compute, storage, and networking capacity.

SMEs are expected to grow at the highest CAGR of 9.5% as they accelerate their adoption of cloud services, automation tools, and digital solutions, starting from a smaller base.

By Application

IT & Telecommunications Segment Dominates due to its Ability to Manage Data Traffic

Based on application, the market is segmented into IT & telecommunications, BFSI, government, healthcare, retail, media & entertainment, energy, and others.

The IT and telecommunications segment holds the largest share of 37.83% in 2026. It records the highest CAGR of 10.3% globally as data center operators, cloud providers, and digital service companies require large-scale server infrastructure to manage data traffic, communication services, and compute-intensive workloads.

BFSI is the second-largest segment as financial institutions rely on secure and resilient server systems to handle payments, regulatory processes, fraud detection, and real-time financial services.

DATA CENTER SERVER MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Data Center Server Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 81.83 Billion, accounting for 35.40% of the worldwide market, and is projected to grow to USD 87.25 Billion in 2026. This is due to its large concentration of hyperscale cloud providers, which continually expand their computing infrastructure to support extensive digital operations. These companies create strong demand for advanced server systems to manage cloud services, AI workloads, and high volumes of data processing. Robust enterprise technology spending across various sectors, including finance, healthcare, and IT, further strengthens regional server requirements.

- This position is supported by research indicating that the U.S. alone accounts for more than 54% of global hyperscale data center capacity, underscoring the region’s high server density.

U.S Data Center Server Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 72.27 billion in 2026, accounting for roughly 29.8% of global data center server sales.

Europe

The Europe market generated USD 46.76 billion in 2025, representing 20.14% of the global market landscape, and is expected to reach USD 49.42 billion in 2026. Europe holds a significant share of the global market due to its large and technologically advanced enterprise base, which continues to invest in cloud infrastructure, digital transformation, and data-driven applications.

U.K Data Center Server Market

The U.K. market in 2026 is estimated to be around USD 9.21 billion, representing approximately 3.8% of global data center server revenues.

Germany Data Center Server Market

Germany’s data center server market size is projected to reach approximately USD 11.07 billion in 2026, equivalent to around 4.5% of global data center server sales.

Asia Pacific

Asia Pacific contributed 33.33% to the global market in 2025, with a valuation of USD 77.39 billion, and is projected to reach USD 84.27 billion in 2026, and secure the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 16.85 billion and USD 25.29 billion, respectively, in 2026. Regional and international cloud providers continue to build new data centers in major markets, such as China, India, Japan, and Southeast Asia, to meet the rising computing needs. Government initiatives promoting data localization and broader digital economy development also encourage increased domestic investment in server infrastructure.

- Recent studies indicate that the ten largest data center markets in Asia collectively account for approximately 27% of global colocation capacity, reflecting the region’s expanding infrastructure base.

Japan Data Center Server Market

In Japan, the market in 2026 is estimated to be around USD 10.88 billion, accounting for approximately 4.5% of global data center server revenues.

China Data Center Server Market

China’s market is projected to be one of the largest worldwide, with revenues estimated at approximately USD 25.29 billion in 2026, accounting for roughly 10.1% of global data center server sales.

India Data Center Server Market

The Indian market in 2026 is estimated to be around USD 16.85 billion, accounting for approximately 6.4% of global data center server revenues.

South America, Latin America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in South America is set to reach a valuation of USD 10.09 billion in 2025. The Middle East & Africa market was valued at USD 16.13 billion in 2025, capturing 6.95% of global revenue, and is estimated to reach USD 17.44 billion in 2026. The growth is driven by improvements in regional and international connectivity, including new submarine cable routes and upgraded terrestrial networks, which are enabling more efficient and higher-density deployments.

The market in Latin America reached USD 10.09 billion in 2025, representing 4.30% of total market revenue, and is projected to reach USD 10.81 billion in 2026.

GCC Data Center Server Market

The GCC market is projected to reach approximately USD 6.29 million by 2025, accounting for roughly 2.7% of global data center server revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Solutions to Strengthen Their Market Position

Players in the data center server industry launch new solutions to enhance their market positioning by leveraging technological advancements such as machine learning, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their offerings. Such strategic launches enable the technology companies to maintain and expand their market share in a rapidly evolving landscape.

LIST OF KEY DATA CENTER SERVER COMPANIES PROFILED

- Dell Technologies Inc. (U.S.)

- Hewlett Packard Enterprise Company (U.S.)

- Lenovo Group Limited (China)

- Cisco Systems, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Inspur Co., Ltd. (China)

- Super Micro Computer, Inc. (U.S.)

- Quanta Computer, Inc. (Taiwan)

- Fujitsu Limited (Japan)

- IBM Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025- Dell introduced next-gen PowerEdge servers optimized for AI-driven data centers, enhancing performance, scalability, and efficiency for both traditional and AI workloads.

- May 2025- Dell unveiled new AI solutions at its annual conference, designed to help businesses scale their AI projects and drive faster AI adoption across enterprises.

- November 2025- HPE launched the Cray GX5000 supercomputing platform, designed to support the increasing demand for AI and high-performance computing (HPC) workloads.

- June 2025- HPE introduced AI-driven networking and hybrid cloud infrastructure solutions at HPE Discover Barcelona, further accelerating the adoption of AI and cloud across industries.

- February 2025- Lenovo introduced the ThinkSystem V4 Servers, powered by Intel Xeon 6 processors, which provide improved performance for AI and high-performance applications.

- May 2025- Cisco’s updated lineup focused on providing solutions to support the growing demands for AI workloads and hybrid cloud infrastructures in modern data centers.

- January 2025- Huawei unveiled its “Top 10 Trends for Data Center Facilities 2025,” highlighting the importance of AI, sustainability, and flexibility in data center designs.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.49% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Server Type, Enterprise Type, Application, and Region |

|

By Server Type |

|

|

By Enterprise Type |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 232.19 billion in 2025 and is projected to reach USD 444.06 billion by 2034.

In 2025, the market value stood at USD 81.83 billion.

The market is expected to exhibit a CAGR of 7.49% during the forecast period (2026-2034).

By application, the IT & telecommunications segment leads the market.

Inclination toward traditional CPU-based servers is the key factor driving the market.

Dell Technologies Inc., Hewlett Packard Enterprise Company, Lenovo Group Limited, and Cisco Systems, Inc. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us