Dealership Digital Transformation Services Market Size, Share & Industry Analysis, By Service Type (Dealer Management Systems & ERP Services, CRM & Lead Management Services, Digital Retailing & E-Commerce Services, Service & Aftersales Digitalization Services, & Others), By Dealership Function (Sales & F&I Digital Transformation, Service & Workshop Digital Transformation, & Others), By Deployment Model (Cloud-Based (SaaS / Subscription) and On-Premise / Hybrid), By Dealership Type (Passenger Cars Dealerships, Commercial Vehicle Dealerships, & Others) and Regional Forecast, 2026-2034

Dealership Digital Transformation Services Market Size and Future Outlook

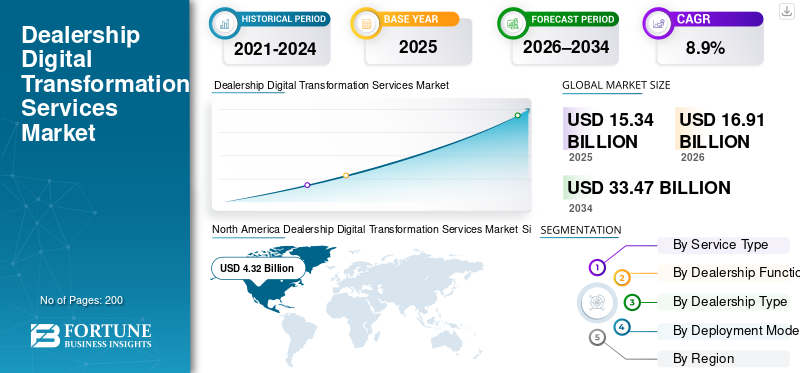

The global dealership digital transformation services market size was valued at USD 15.34 billion in 2025. The market is projected to grow from USD 16.91 billion in 2026 to USD 33.47 billion by 2034, exhibiting a CAGR of 8.9% during the forecast period. North America dominated the dealership digital transformation services market with a market share of 28.16% in 2025.

The dealership digital transformation services market encompasses digital technologies and consulting solutions that modernize dealership sales, service, marketing, and operations through integrated platforms, automation, data analytics, and connected customer engagement tools, aiming to improve efficiency and enhance customer experience.

The market growth is driven by rising customer demand for omnichannel retail experiences, increasing dealership operational complexity, growing adoption of connected vehicles, pressure to improve aftersales profitability, regulatory compliance needs, and the shift toward data-driven, automated dealership operations globally. Major players, including Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech, and other players in the automotive industry, focus on advanced diagnostics, workshop automation, connected service platforms, digital integration with dealer systems, and safety-centric solutions to enhance data service efficiency and digital dealership ecosystems.

Download Free sample to learn more about this report.

DEALERSHIP DIGITAL TRANSFORMATION SERVICES MARKET TRENDS

Accelerated Omnichannel Retail Adoption Enhances Engagement and Revenue

Digital transformation in dealerships is increasingly driven by the trend toward omnichannel retailing, where online and in-store journeys are fully integrated. Customers today begin vehicle discovery and comparison on digital platforms and expect seamless transitions into physical interactions. Dealers are adopting digital retail tools, virtual showrooms, CRM-linked lead nurturing, and automated financing workflows to shorten sales cycles and improve conversion rates. This trend also encompasses real-time inventory visibility and personalized engagement across touchpoints. As buyers’ expectations for convenience and transparency rise, dealers must invest in adaptable digital toolsets to retain competitiveness and loyalty, making omnichannel customized experiences central to growth in the dealership digital transformation market. In August 2025, automotive AI CRM platforms demonstrated that faster lead response and personalized engagement significantly improved customer interactions across channels.

MARKET DYNAMICS

MARKET DRIVERS

Customer-Centric Digital Tools Drive Operational Efficiency and Satisfaction

Digital tools that streamline service scheduling, automate workflows, and leverage data analytics are key drivers of dealership transformation. By digitizing core operations such as service desk workflows, ticketing, and customer follow-ups, dealerships can reduce manual errors, improve turnaround times, and enhance customer satisfaction. The integration of CRM, DMS, and parts inventory management systems enables seamless data flow, informing decision-making and facilitating proactive engagement. These integrated digital services also support personalized offerings and predictive maintenance, helping dealerships retain existing customers and generate repeat business. Moreover, as customer expectations evolve, digital automation and analytics become critical levers for superior operational performance and competitive differentiation, fostering long-term growth in dealer engagements. In May 2025, digital transformation blueprints highlighted a 68% increase in customer preference for digital service scheduling, underscoring demand for customer-centric tools.

MARKET RESTRAINTS

Legacy System Complexity Remains a Constraint on Transformation Progress

Despite investments in digital initiatives, many dealerships face resistance due to the complexity of legacy systems. Integrating new cloud-native platforms with existing DMS, CRM, and backend tools often requires significant time, expertise, and capital, which can slow transformation progress. Legacy technology stacks often lack modern APIs, hindering real-time data synchronization and cross-departmental workflows. The absence of standardized data models also complicates analytics and reporting, reducing the ability to leverage next-generation AI or predictive tools. In addition, smaller dealerships may lack in-house IT capabilities to manage hybrid environments, which can prolong implementation timelines and dilute the expected ROI. As a result, modernization efforts can be delayed, restraining the pace at which full digital benefits are realized. This impacts the dealership digital transformation services market growth.

MARKET OPPORTUNITIES

Connected Vehicle Data and AI Insight Expansion Open New Revenue Streams

The proliferation of connected vehicles, telematics, and AI driven analytics offers a substantial opportunity for digital transformation in dealerships. By harnessing real-time usage data and predictive insights, dealerships can tailor service offerings, forecast maintenance needs, and deliver personalized communication. These capabilities enhance customer lifetime value and create new service bundles linked to usage trends, driving additional revenue beyond one-time transactions. Furthermore, as electrification and autonomy introduce new data streams, dealer systems must evolve to capture and operationalize this information, unlocking revenue opportunities tied to software-enabled services. Robust data platforms also enable market segmentation, targeted marketing, and dynamic pricing, expanding the role of digital tools in revenue optimization across the ownership lifecycle. In October 2025, digital tools highlighted the importance of virtual showrooms and integrated ecosystems for future dealership competitiveness.

MARKET CHALLENGES

Workforce Skill Gaps Challenge Implementation of Digital Solutions

A significant challenge in dealership digital transformation services is the shortage of digital skills among staff and leadership. While technology adoption accelerates, many dealerships struggle to train employees on new systems, interpret analytics outputs, or maintain digital platforms without external support. Resistance to change, insufficient training budgets, and the lack of structured upskilling pathways can hinder transformation projects or result in suboptimal tool utilization. As digital solutions become more sophisticated, incorporating AI, machine learning, cloud based platforms, and deep analytics, dealerships must invest in talent development and change management programs to fully realize the value of their technology investments. Without addressing these workforce gaps, uptake and ROI on digital platforms remain below potential, limiting operational gains.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service Type

Dealer Management Systems (DMS) & ERP Services Segment Dominates Due to Integrated, Cloud-based Dealership Operations

Based on service type, the market is segmented into Dealer Management Systems (DMS) & ERP services, CRM & lead management services, digital retailing & e-commerce services, service & aftersales digitalization services, and data analytics, AI & cloud integration services.

Dealer Management Systems (DMS) & ERP services segment dominates with the largest dealership digital transformation services market share. They serve as the foundational platform that integrates sales, service, inventory, finance, and customer data under a single digital infrastructure. Dealers globally prioritize DMS modernization to eliminate manual silos, improve data accuracy, and support downstream digital modules. This deep integration supports efficient transactions and data-driven decision-making across departments, making it the largest spend category within transformation initiatives. Cloud-native DMS platforms are particularly prevalent as they reduce IT overhead and increase real-time visibility across multi-location dealerships.

The data analytics, AI & cloud integration services segment is projected to grow at a CAGR of 11.2% over the forecast period.

- In July 2025, Keyloop expanded its cloud-native automotive retail platform to integrate CRM, sales, and aftermarket services across more than 20,000 dealerships globally, highlighting the shift toward comprehensive digital platforms.

By Dealership Function

After-Sales Revenue Focus, Workflow Automation, and Predictive Insights Drives Service & Workshop Digital Transformation Segment Growth

Based on function, the market is classified into sales & F&I digital transformation, service & workshop digital transformation, parts & inventory digitalization, and customer engagement & marketing digitalization.

Service & workshop digital transformation is the dominating segment, as after-sales operations generate high recurring revenue and directly influence customer retention. Dealers invest heavily in digital service scheduling, digital vehicle health inspection tools, workflow automation, and parts coordination systems to streamline service throughput, increase labor utilization, and improve service experience. Data-driven service metrics also feed predictive maintenance and parts forecasting platforms, further enhancing operational efficiency. These capabilities help dealers maximize fixed streamline operations profitability, often the largest margin area in dealership P&L.

The customer engagement & marketing digitalization segment is projected to grow at a CAGR of 11.4% over the forecast period.

- In August 2025, advanced digital service blueprints outlined how dealerships are integrating digital tools to reshape service workflows and meet increasingly demanding customer standards, reflecting a focus on investment in digitalization of after-sales services.

By Deployment Model

Lower Ownership Costs, Scalability, Rapid Updates, and Remote Accessibility Drives Cloud-Based (SaaS/Subscription) Segment Growth

Based on the deployment model, the market is categorized into cloud-based (SaaS / subscription) and on-premise / hybrid.

Cloud-Based (SaaS/Subscription) segment dominates the market and is the fastest-growing. They eliminate upfront infrastructure complexity, enable rapid deployment of updates, and support remote access across dealership networks. With multi-tenant cloud systems, dealers benefit from lower total cost of ownership, built-in security patches, and scalable performance that aligns with fluctuating transaction volumes and multi-location operations. This deployment preference accelerates the adoption of advanced modules, including CRM, analytics, and omnichannel retail experiences.

The cloud-based segment is projected to grow at a CAGR of 10.4% over the forecast period. In contrast, the on-premise/hybrid segment continues to grow more slowly, as some large dealer groups maintain legacy systems or require localized data compliance, often supporting bespoke integrations rather than full SaaS adoption. Digital transformation efforts often begin with cloud migration to tap into scalability and reduce IT overhead.

By Dealership Type

To know how our report can help streamline your business, Speak to Analyst

High Transaction Volumes, Complex Inventories, and Intensive Customer Engagement Drives Passenger Car Dealerships Segment Growth

Based on dealership type, the market is segmented into passenger cars dealerships, commercial vehicle dealerships, and pre-owned dealer groups.

Passenger car dealerships dominate due to the sheer volume and scale of consumer retail activity worldwide. These dealers typically have higher transaction frequencies, larger showroom footprints, and more diverse service needs, which drives higher absolute spend on digital systems such as integrated DMS, CRM, digital retailing, and analytics platforms. Their complex inventories, varied financing options, and high customer interaction rates accelerate digital adoption compared to the commercial vehicle and pre-owned segments.

The pre-owned dealer groups segment is projected to grow at a CAGR of 11.1% over the forecast period, as organized used-car retail expands and technology adoption rises to address pricing transparency and online purchasing demand. While there is widespread recognition of digital implementation in dealerships, precise operational milestones vary by region and dealer scale.

DEALERSHIP DIGITAL TRANSFORMATION SERVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Dealership Digital Transformation Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America represents a dominant, mature yet steadily expanding market, driven by high dealership IT penetration, strong SaaS adoption, and continuous upgrades of legacy DMS platforms. Dealers are increasingly investing in cloud-based DMS, CRM automation, digital retailing, and service workflow optimization to enhance efficiency and the customer experience. Regulatory compliance, cybersecurity requirements, and AI-driven analytics further support the growth in spending. Mexico is expected to contribute faster incremental growth as dealership digitization accelerates from a lower base, while the U.S. remains the largest revenue contributor due to its scale and higher per-dealer IT spending.

U.S. Dealership Digital Transformation Services Market

The U.S. market is driven by widespread cloud DMS migration, advanced CRM usage, and strong adoption of digital retailing tools. Large dealer groups invest heavily in analytics, cybersecurity, and omnichannel platforms to optimize sales and after-sales performance, sustaining steady market growth. It was valued at USD 4.87 billion in 2025.

Asia Pacific

Asia Pacific is the fastest-growing regional market due to its massive dealership footprint, rising vehicle ownership, and rapid digitization across emerging economies. Dealers increasingly adopt cloud-based DMS, CRM, and digital retailing platforms to manage high transaction volumes efficiently. Growth is strongest in China and India, supported by scale and organized dealer networks, while Japan exhibits steady expansion driven by analytics and the digitization of used cars. Lower legacy IT constraints enable faster SaaS adoption across the region.

China Dealership Digital Transformation Services Market

China dominates with share of 46.7% in 2025, due to its large dealership network and high transaction volumes. Growth is driven by digital retailing, CRM integration, and the rapid expansion of organized pre-owned dealer platforms.

Japan Dealership Digital Transformation Services Market

Japan’s market is growing steadily through the digitalization of services, the adoption of analytics, and the implementation of sophisticated CRM systems, with a strong focus on customer retention and the management of the used-vehicle lifecycle.

India Dealership Digital Transformation Services Market

India is the fastest-growing with CAGR of 15% during the forecast period, supported by over 30,000 dealership outlets and accelerating adoption of cloud DMS, CRM, and service workflow tools to manage scale and improve efficiency.

Europe

A large dealership base, stringent regulatory compliance requirements, and a strong focus on operational standardization underpin Europe’s growth. Dealers prioritize service and digitalization of workshops, parts inventory optimization, and the integration of ERP platforms to improve margins. Cloud adoption is rising steadily, although hybrid deployments remain relevant due to data localization norms. Growth is more evenly distributed across Western and broader European markets, with analytics, customer engagement platforms, and the digitization of used cars emerging as key drivers.

U.K. Dealership Digital Transformation Services Market

U.K. dealerships are focusing on digital retailing, CRM automation, and customer engagement platforms to address the competitive retail dynamics, with strong online lead generation and service booking adoption supporting consistent market growth, valued at USD 0.44 billion.

Germany Dealership Digital Transformation Services Market

Germany’s market with CAGR of 7.2% during the forecast period, is driven by structured dealer networks that emphasize ERP integration, digitalization of services, and compliance-ready systems. Analytics and AI adoption are increasing to support operational efficiency and margin control.

Rest of the World

The rest of the world exhibits moderate yet accelerating growth as dealership networks become more organized and digitalization adoption increases. Cloud-based platforms enable dealers to bypass the limitations of legacy infrastructure, supporting the rapid deployment of CRM, service booking, and inventory systems. Growth is led by Latin America and the Middle East, where improving digital infrastructure and rising customer expectations drive investments in dealership digital tools, particularly in service operations and customer engagement.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-Defined Platforms, Cloud Migration, and Strategic Partnerships Shape Dealership Digital Transformation Competitiveness

The global dealership digital transformation services market trends are characterized by rapid adoption of cloud-native platforms, modular software architectures, and integrated data ecosystems that connect sales, service, and customer engagement functions. Leading players, including CDK Global, Cox Automotive, Reynolds and Reynolds, Tekion, Keyloop, SAP, Salesforce, and Microsoft, compete through scalable DMS platforms, advanced CRM capabilities, omnichannel retailing tools, and AI-driven analytics. Companies strengthen competitiveness by accelerating SaaS migration, embedding cybersecurity and compliance features, and enabling seamless integration with OEM, financial, and third-party systems. Strategic partnerships with cloud providers, payment platforms, and AI technology companies are increasingly crucial for expanding functionality and geographic reach. Vendors also differentiate through continuous OTA software updates, user-centric interfaces, and data intelligence solutions that enhance dealer efficiency and customer experience. In April 2025, Tekion expanded its cloud-native automotive retail platform through deeper integrations with financial services and analytics tools, reinforcing its competitive positioning in large dealership groups and multi-brand dealer networks.

LIST OF KEY DEALERSHIP DIGITAL TRANSFORMATION SERVICES COMPANIES PROFILED

- CDK Global (U.S.)

- Cox Automotive (U.S.)

- The Reynolds and Reynolds Company (U.S.)

- Tekion (U.S.)

- Keyloop (U.K.)

- AI (U.K.)

- Dealertrack (Cox Automotive) (U.S.)

- Capgemini Engineering (France)

- Bosch Automotive Service Solutions (Germany)

- SAP (Germany)

- Oracle (U.S.)

- Salesforce (U.S.)

- Microsoft (U.S.)

- Xtime (Cox Automotive) (U.S.)

- Auto/Mate (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Pinewood.AI announced a seven-day go-live offer for its CARS suite of AI products, designed to be compatible with any DMS, targeting faster deployment for dealer groups seeking rapid operational digitization and quicker time-to-value from analytics, automation, and AI-enabled workflows.

- October 2025: Keyloop launched its Fusion Automotive Retail Platform at a dealer event in Montreal, positioning the platform to optimize the dealership journey from enquiry through ownership and retention, with a cloud-based modular approach and a consolidated data core designed to support AI-assisted decision-making.

- October 2025: Cox Automotive announced its omnichannel digital retailing platform, enabling complete vehicle purchases across multiple digital channels. This platform integrates e-commerce capabilities on retailer sites with in-store workflows and marketplace purchasing to support fully connected transactions.

- September 2025: Tekion announced that Hartwell Automotive Group had selected Tekion’s AI-powered Automotive Retail Cloud for a phased rollout across 11 U.K. locations, aiming to modernize end-to-end dealership operations (retail, service, parts, accounting, and analytics) through a unified, cloud-native platform.

- July 2025: Tekion reported that Automotive Partner Cloud (APC) 2.0 had experienced rapid adoption growth, with dealer app installations and the professional user base scaling significantly. This expansion was accompanied by the introduction of an Integration Hub that centralizes, authorizes, and manages third-party integrations, aiming to address dealership tech fragmentation and data silo issues.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.9% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, By Dealership Function, By Dealership Type, By Deployment Model, and By Region |

|

By Service Type |

· Dealer Management Systems (DMS) & ERP Services · CRM & Lead Management Services · Digital Retailing & E-Commerce Services · Service & Aftersales Digitalization Services · Data Analytics, AI & Cloud Integration Services |

|

By Dealership Function |

· Sales & F&I Digital Transformation · Service & Workshop Digital Transformation · Parts & Inventory Digitalization · Customer Engagement & Marketing Digitalization |

|

By Deployment Model |

· Cloud-Based (SaaS / Subscription) · On-Premise / Hybrid |

|

By Dealership Type |

· Passenger Cars Dealerships · Commercial Vehicle Dealerships · Pre-owned Dealer Groups |

|

By Geography |

· North America (By Service Type, By Dealership Function, By Dealership Type, By Deployment Model and By Country) o U.S. (By Dealership Type) o Canada (By Dealership Type) o Mexico (By Dealership Type) · Europe (By Service Type, By Dealership Function, By Dealership Type, By Deployment Model and By Country) o Germany (By Dealership Type) o U.K. (By Dealership Type) o France (By Dealership Type) o Rest of Europe (By Dealership Type) · Asia Pacific (By Service Type, By Dealership Function, By Dealership Type, By Deployment Model, and By Country) o China (By Dealership Type) o Japan (By Dealership Type) o India (By Dealership Type) o South Korea (By Dealership Type) o Rest of Asia Pacific (By Dealership Type) · Rest of the World (By Service Type, By Dealership Function, By Dealership Type, and By Deployment Model) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 15.34 Billion in 2025 and is projected to reach USD 33.47 Billion by 2034.

In 2025, the North America market value stood at USD 4.32 billion.

The market is expected to grow at a CAGR of 8.9% during the forecast period from 2026 to 2034.

By deployment model, the cloud-based (SaaS/subscription) segment led the market.

Customer-centric digital tools drive operational efficiency and satisfaction.

Key market players in the market include Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech.

North America accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us