Denials Management Software Market Size, Share & Industry Analysis, By Deployment (Cloud-Based, On premise, and Hybrid), By Type (Standalone and RCM Integrated), By Workflow Stage (Pre-bill, Post-bill, and Recovery/variance), By Application (Denial Prevention, Denial Management, Claims Editing, Denial Prioritization, Underpayment Analytics, and Others), By End User (Hospitals & ASCs, Physician's Offices, and Others), and Regional Forecast, 2026-2034

Denials Management Software Market Size and Future Outlook

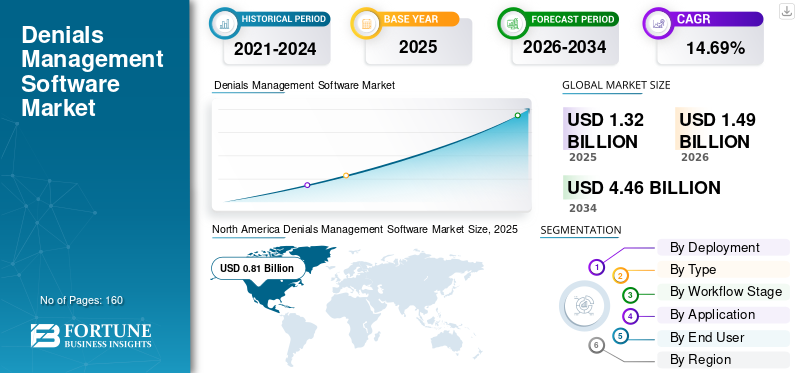

The global denials management software market size was valued at USD 1.32 billion in 2025. The market is projected to grow from USD 1.49 billion in 2026 to USD 4.46 billion by 2034, exhibiting a CAGR of 14.69% during the forecast period. North America dominated the global denials management software market with a market share of 61.36% in 2025.

The denials management software market is expected to experience significant growth in the coming years, driven by increasing pressure from vendors due to lost revenue and rising administrative burden. The increasing reliance on fragmented workflows in denial management results in operational inefficiencies and drives demand for denial management software tools. These tools standardize workflows, prioritize the right denials, and automate routine tasks such as documentation gathering and appeal drafting. Emphasizing the market's growth potential, leading organizations are investing in new product launches to reduce turnaround times and operate more efficiently, thereby supporting the growth of the global denial management software market.

- For instance, in June 2022, Iodine Software launched an appeals management workspace that supports denial management alongside GenAI enhancements. The upgrade revolutionized pre-claim denials management by automating appeal letter generation, centralizing denial tracking, and providing intuitive, customizable nurse-physician collaboration tools.

Leading players in the denials management software industry, such as SCALE Healthcare, Experian Information Solutions, Inc., Infinx Healthcare, and Waystar, are investing heavily in new product launches and strategic collaborations to strengthen their market positions.

Download Free sample to learn more about this report.

Global Denials Management Software Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.32 billion

- 2026 Market Size: USD 1.49 billion

- 2034 Forecast Market Size: USD 4.46 billion

- CAGR: 14.69% from 2026–2034

- North America dominated the denials management software market with a 61.36% share in 2025.

- The cloud-based segment dominated the market by deployment type in 2025.

- The hospitals and ASCs segment dominated the market by end user in 2025.

North America

The region dominated the market with a value of USD 0.81 billion in 2025

Europe

The market is projected to reach USD 0.28 billion in 2026 and grow at a CAGR of 12.30% over the coming years.

Asia Pacific

The region is estimated to reach USD 0.22 billion in 2026, securing its position as the third-largest regional market.

U.S.

The market is estimated to reach USD 0.84 billion in 2026.

Japan

The market is estimated to reach USD 0.05 billion in 2026.

Read More

DENIALS MANAGEMENT SOFTWARE MARKET TRENDS

Shift Toward AI-driven Denial Prevention Is a Prominent Trend Observed

Shift toward AI-driven denial prevention is a significant global denials management software market trend observed. Rising patient volumes have led to an increase in denial claims, prompting healthcare providers to seek greater operational efficiency. These developments are making significant strides to overcome challenges associated with manual work queues and fragmented tools. Platforms are increasingly using AI technologies to predict denials before submission, auto-route work to the right staff, and generate payer-specific appeal content to reduce turnaround time and improve visibility. This trend is also pushing vendors to embed denial intelligence directly into broader revenue cycle workflows, making adoption easier.

Furthermore, key companies are integrating Artificial Intelligence into their solutions and launching new products to support the global denials management software market growth.

- For instance, in June 2025, Finvi launched its new Denial Intelligence Engine within the Artiva HCx platform for insurance claim follow-up. The engine leveraged artificial intelligence (AI) and machine learning (ML) to help healthcare providers and their partners focus follow-up efforts on denied claims.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

High Claim Denials and Limited Visibility to Drive Market Growth

High claim denials and limited visibility are elevating demand for denial management software and pushing providers to invest in these solutions. Large volumes of denial claims make manual follow-up time-consuming and lead to unpredictable revenue cycles. Limited end-to-end visibility also makes it challenging to spot repeated denial patterns or upstream issues such as missing documentation and coding gaps. To overcome these challenges, healthcare providers are increasingly adopting predictive analytics-based denial platform solutions that centralize denial insights, prioritize high-value denials, and optimize workflows.

Due to these advantages, healthcare providers are increasingly adopting these solutions through strategic partnerships with leading market players, thereby fueling overall market growth.

- For instance, in March 2023, Schneck Medical Center collaborated with Experian Health to test two new denial management solutions that used artificial intelligence (AI) to reduce the likelihood of denials and prioritize rework to maximize reimbursement. The AI Advantage-Predictive Denials solutions used AI to predict claims with a high likelihood of denial so they could be corrected before submission to the payer.

MARKET RESTRAINTS

Fragmented Payer Regulations Across Regions to Impede Denials Management Software Market

Fragmented payer regulations across regions act as a market restraint, as they make denials management workflows hard to standardize and automate at scale. When medical policies, coding edits, and documentation requirements differ by payer and geography, providers must maintain multiple rule sets, which increases configuration effort and ongoing maintenance costs. These factors cause data errors and inconsistent claim quality, resulting in high denial rates. As a result, some organizations slow down or limit deployments to specific regions or payer lines until rules stabilize, thereby delaying implementation and restraining market growth.

- For instance, in November 2025, MDaudit’s 2025 Benchmark Report highlighted a sharp rise in certain denial behaviors, showing how denial drivers can differ by payer program, forcing providers to manage different rule sets.

MARKET OPPORTUNITIES

Technological Advancement to Offer Key Market Growth Opportunity

Prior authorization remains a major barrier to market entry, as many providers rely on phone calls, faxes, and multiple payer portals, leading to missing documents, delays in approval, and preventable denials later in the billing cycle. Technological advancements driven by automation offer significant growth opportunities and help overcome these challenges. When staff repeatedly chase payer-specific requirements, administrative costs rise, and patients wait longer for treatment. This creates a clear growth opportunity for denial management software vendors to automate prior authorization. Such innovation enables faster approvals and reduces rework later in the claims cycle. As AI-powered workflows improve, solutions can automatically detect when authorization is required, assemble payer-ready packets, track status, and trigger the right next step without human handoffs. That shift moves organizations from reactive appeals to proactive prevention, improving clean-claim performance and speeding cash collection.

- For instance, in January 2026, R1 launched R1 Prior Authorization, powered by its Phare OS, to automate and streamline prior authorization at scale, reflecting a focus on automation and growth over time.

MARKET CHALLENGES

Integration Complexity with EHRs and Billing Systems Poses a Critical Challenge to Market Growth

Integration complexity with EHRs and billing systems is a significant challenge for the market. Denial claims must pull clean clinical, coding, and eligibility data from multiple systems, and any mismatch creates errors and rework. When data fields are mismatched or workflows don’t align properly, claims may be submitted with incorrect codes or broken authorization references, increasing denials. These integrations also require substantial time, IT effort, and testing across payer and internal rules. This results in projects running longer and costing more than planned. These challenges slow adoption and make it harder for providers to demonstrate ROI quickly, thereby hampering overall market growth.

- For instance, in April 2023, the U.S. Department of Veterans Affairs halted future deployments of its EHR system to focus on resolving issues at existing sites. The development highlighted how large-scale system integration and stabilization problems disrupt operations, delay expected benefits, and slow the adoption of related solutions in the market.

Segmentation Analysis

By Deployment

Cloud-Based Segment Led due to its Benefits

Based on deployment, the market is segmented into cloud-based, on premise, and hybrid.

In 2025, the cloud-based segment dominated the market, driven by providers' need for faster deployment and continuous updates. Cloud platforms make it easier to centralize work queues, standardize workflows, and provide real-time visibility into denial claim status. These features reduce delays and help teams act faster. Cloud delivery also supports quicker scaling during volume spikes, making it easier to launch new analytics and AI features that improve prevention and recovery. Underscoring these advantages, key players are participating in strategic collaborations and acquisitions to expand the offerings of these cloud-based solutions.

- For instance, in January 2026, EnableComp acquired Health Resources Optimization, Inc. (H/ROI), a premier clinical denials and revenue recovery firm.

The hybrid segment is projected to grow at a 9.63% CAGR during the study period.

To know how our report can help streamline your business, Speak to Analyst

By Type

One Stop Solution Offered by RCM Integrated Solutions Reinforced the Segment’s Dominance

Based on type, the market is segmented into standalone and RCM-integrated.

The RCM-integrated solutions accounted for the largest denials management software market share in 2025. The dominance is attributed to the fact that many key companies offer integrated denial management solutions rather than standalone solutions. A one-stop solution for claim edits, remittances, and denial follow-up enables easier root-cause analysis, reducing rework and write-offs. This results in faster turnaround and clearer ROI, especially for large healthcare systems seeking to minimize the number of point solutions. These advantages prompt key companies to integrate the denial management solutions with RCM, thereby fueling segmental growth.

- For instance, in March 2025, RevSpring collaborated with Availity to integrate its revenue cycle management solution, addressing denial management, claims processing, and vendor interactions. The development enabled customers to gain access to a full-service solution to drive more efficient patient payments and processing.

The standalone segment is projected to grow at a CAGR of 6.25% during the study period.

By Workflow Stage

Post-Bill Segment Led the Market due to Key Companies’ Focus on New Product Launches

Based on workflow stage, the market is segmented into pre-bill, post-bill, and recovery/variance.

In 2025, the post-bill segment dominated the global market, accounting for the largest share. The segment dominance is attributed to the fact that denials are typically discovered only after a claim has been processed, shifting provider focus toward recovering revenue already at risk. Providers faced strict timelines and needed to comply with specific documentation requirements and payer-specific steps. Failure to comply with these steps could turn a recoverable claim into a write-off, underscoring the importance of the post-bill management workflows. As a result, key companies are focusing on new product launches to monetize the potential of the segment.

- For instance, in April 2025, Red Sky Health unveiled Daniel, an AI-powered solution design to help healthcare providers identify the root causes of claims errors, fix them in real time, and resubmit claims effeciently. The innovative solution enabled providers to recover lost revenue with higher efficiency by using ML and generative AI algorithms to analyze historical claims data, identify and correct errors, and streamline the resubmission process.

The pre-bill segment is projected to grow at an 18.17% CAGR during the study period.

By Application

Core Workflow of Denial Management to Lead to Segmental Growth

As per application, the market is divided into denial prevention, denial management, claims editing, denial prioritization, underpayment analytics, and others.

In 2025, the denial management segment dominated the global market, as it represents a core workflow for managing high-risk revenue. The segment determines how much revenue is recovered versus written off. Teams require an appropriate system to track denial reasons, route work, manage payer deadlines, and ensure appeals are submitted correctly and on time. Without these foundations, advanced features such as prevention and underpayment analytics do not deliver value. As a result, buyers prioritize denial management capabilities as the primary investment area within the market. Emphasizing these advantages, key companies are directing their resources toward innovative product launches to meet growing global demand for denials management software.

- For instance, in May 2025, MD Clarity launched a major expansion of its denial management module. The offering empowered healthcare providers to identify, appeal, and analyze denials more effectively, facilitating improved optimal reimbursement.

The denial prioritization segment is projected to grow at a CAGR of 16.70% during the study period.

By End User

High Claim Volumes in Hospitals & ASCs Led Segmental Growth

Based on end user, the market is segmented into hospitals & ASCs, physicians' offices, and others.

The hospitals and ASCs segment dominated the market in 2025. The segment generates high claim volumes and handles complex care delivery workflows, where denials have a larger impact on overall performance. These organizations also handle more payer contracts and complex authorization requirements, which require greater clinical documentation. High claim volumes combined with complex documentation increase denial risk and drive the need for structured workflows. Due to these factors, hospitals and ASCs are the primary end users of denial management software and account for the largest share of revenue. Highlighting the segment's dominance, companies are actively engaging in strategic activities, such as acquisitions and mergers, to meet growing demand.

- For instance, in December 2023, R1 RCM Inc., a leading provider of technology-driven solutions to healthcare providers, acquired Acclara, a revenue cycle management The partnership intended to automate revenue management processes and diversify offerings to build long-term value for healthcare providers, patients, and shareholders.

The physician's offices segment is projected to grow at a CAGR of 16.29% during the study period.

Denials Management Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Denials Management Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.72 billion and maintained its leading position in 2025 at USD 0.81 billion. The market is driven by rising denial rates and rapidly changing payer rules from regulatory bodies. Additionally, the shift toward more complex reimbursement models and increased coding scrutiny increased demand for denial management solutions in the region, supporting market growth.

U.S. Denials Management Software Market

Given North America’s substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.84 billion in 2026, accounting for roughly 56.48% of the global denials management software market.

Europe

Europe is projected to grow at 12.30% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.28 billion by 2026. The greater digitization of hospital finance workflows and the region's stricter compliance expectations are expected to drive growth.

U.K. Denials Management Software Market

IThe U.K.’s denials management software market in 2026 is estimated at around USD 0.04 billion, representing roughly 2.86% of the global market.

Germany Denials Management Software Market

In Germany, the denials management software market is projected to reach approximately USD 0.07 billion in 2026, equivalent to around 4.78% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.22 billion in 2026 and secure the position of the third-largest region in the market. The growth is attributed to rising administrative burden and pressure to improve financial efficiency.

Japan Denials Management Software Market

In Japan, the global denial management software market in 2026 is estimated at around USD 0.05 billion, accounting for approximately 3.56% of the global market.

China Denials Management Software Market

China’s market is projected to be among the largest worldwide, with 2026 revenues estimated at around USD 0.07 billion, roughly 4.93% of global sales.

India Denials Management Software Market

In India, the denials management software market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 1.20% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to experience moderate growth in the global denial management software market during the forecast period. The Latin American market is set to reach a valuation of USD 0.04 billion in 2026. The region is experiencing market growth, driven by increased investment and government initiatives. In the Middle East & Africa, the GCC is expected to account for 1.34% of the global market and reach a valuation of USD 0.02 billion.

South Africa Denials Management Software Market

The market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.41% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Propel Market Progress

The global denials management software market is highly consolidated, with companies such as SCALE Healthcare, Experian Information Solutions, Inc., Infinx Healthcare, and Waystar holding significant market share. Strategic partnerships, technological advancements, and increased investments in new product launches are driving market share gains among these companies.

- For instance, in September 2025, Waystar announced advances in AI leadership with the launch of its next-generation denial prevention and reimbursement recovery solution, Waystar AltitudeAI. These advancements reinforced the company’s leading market positions and are aimed at driving market growth.

Other notable players in the global market include FinThrive, Availity, LLC, R1, and Optum, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY DENIALS MANAGEMENT SOFTWARE MARKET COMPANIES PROFILED

- SCALE Healthcare (U.S.)

- Experian Information Solutions, Inc. (U.S.)

- Infinx Healthcare (U.S.)

- Waystar (U.S.)

- (U.S.)

- Availity, LLC. (U.S.)

- R1 (U.S.)

- Optum, Inc. (U.S.)

- Sift Healthcare (U.S.)

- MDaudit (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: NYX Health, a healthcare revenue cycle solutions provider specializing in advanced denial recovery and compliance-driven workflows, launched its AI-powered Denial Appeal Letter Automation solution, NYX Health AI. The development enabled hospitals and health systems to automatically generate accurate, payer-specific denial appeal letters at scale, thereby accelerating appeal timelines.

- July 2025: VisiQuate, a leader, acquired Etyon, a healthcare technology company recognized for its deep RCM machine learning, domain-specific algorithms, and advanced data tokenization capabilities to supercharge insight automation and denials management for healthcare providers.

- June 2025: FinThrive, Inc., launched FinThrive Denials and Underpayments Analyzer, a next-generation analytics solution to assist health systems with payer denials and underpayments.

- November 2024: Claimable, launched its AI-powered appeals platform designed to help children with PANS/PANDAS overcome insurance companies' denials and access critical intravenous immunoglobulin (IVIG) treatment.

- June 2024: Solventum launched an artificial intelligence (AI)-driven payment integrity and revenue cycle solution, Solventum Revenue Integrity System. The solution was developed in collaboration with Sift Healthcare and is designed to help health systems reduce potential denials and ensure timely, accurate payer reimbursement.

- September 2023: Finvi enhanced its Artiva HCx solution with a new denial management suite designed to streamline the denial process for revenue cycle management (RCM) departments in the healthcare industry.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.69% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Deployment, Type, Workflow Stage, Application, End User, and Region |

|

By Deployment |

· Cloud-Based · On premise · Hybrid |

|

By Type |

· Standalone · RCM Integrated |

|

By Workflow Stage |

· Pre-bill · Post-bill · Recovery/variance |

|

By Application |

· Denial Prevention · Denial Management · Claims Editing · Denial Prioritization · Underpayment Analytics · Others |

|

By End User |

· Hospitals & ASCs · Physician's Offices · Others |

|

By Region |

· North America (By Deployment, Type, Workflow Stage, Application, End User, and Country) o U.S. o Canada · Europe (By Deployment, Type, Workflow Stage, Application, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Deployment, Type, Workflow Stage, Application, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Deployment, Type, Workflow Stage, Application, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Deployment, Type, Workflow Stage, Application, End User, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.32 billion in 2025 and is projected to reach USD 4.46 billion by 2034.

In 2025, the market value stood at USD 0.81 billion.

The market is expected to grow at a CAGR of 14.69% over the forecast period (2026-2034).

By deployment, the cloud-based segment led the market.

High claims denial and limited visibility are the key factors driving the market growth.

SCALE Healthcare, Experian Information Solutions, Inc., Infinx Healthcare, and Waystar are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us