Dewatering Equipment Market Size, Share & Industry Analysis, By Equipment Type (Sludge Dewatering Equipment and Other Dewatering Equipment) By Technology Type (Pumps & WellPoint, Centrifuges, Filter Presses, Dewatering Screens, Belt Presses, and Others) By End User (Industrial Wastewater Treatment, Municipal, Mining & Mineral Processing, Oil & Gas, Construction, and Others) and Regional Forecast, 2026-2034

Dewatering Equipment Market Size and Future Outlook

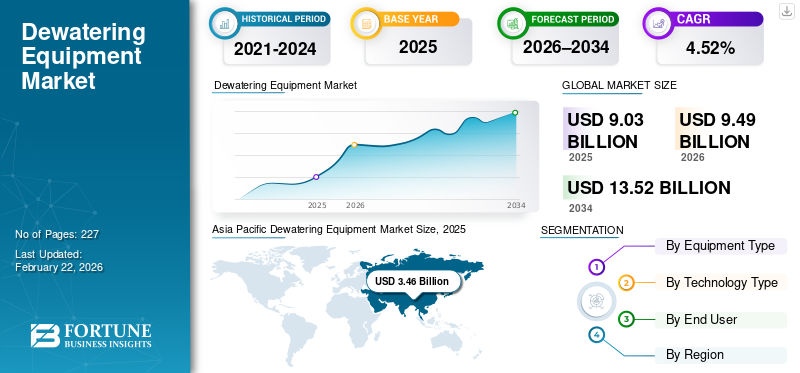

The global dewatering equipment market size was valued at USD 9.03 billion in 2025. The market is projected to grow from USD 9.49 billion in 2026 to USD 13.52 billion by 2034, with a CAGR of 4.52% over the forecast period. Asia Pacific dominated the dewatering equipment market with a market share of 38.32% in 2025.

Dewatering equipment is a mechanical system used to separate water from solids, slurries, or sludge, reducing moisture content for easier handling, disposal, or reuse. These systems are widely applied in municipal and industrial wastewater treatment, mining, construction, oil & gas, and infrastructure projects. Common dewatering equipment includes centrifuges, filter presses, belt presses, pumps, wellpoints, and dewatering screens. The primary objective is to minimize volume, lower transportation and disposal costs, and improve process efficiency. Dewatering equipment also supports regulatory compliance and environmental protection by enabling effective solids management and water recovery.

The global dewatering equipment market is gaining momentum, driven by the rapid expansion of municipal wastewater treatment infrastructure, urbanization, and stricter environmental regulations. Increasing industrial wastewater generation from sectors such as chemicals, power, food processing, and mining is boosting demand for efficient dewatering solutions. Growth in mining and mineral processing activities, especially in emerging economies, is creating sustained demand for slurry and tailings dewatering equipment. Large-scale infrastructure and construction projects are increasing the use of pumps, wellpoints, and site dewatering systems. In addition, the growing focus on cost reduction, water reuse, and sludge volume minimization is accelerating the adoption of advanced, automated dewatering technologies.

Leading players operating in the market, such as Veolia Environnement, Alfa Laval, ANDRITZ AG, SUEZ Water Technologies & Solutions, adn Xylem Inc, are focusing on technology innovation, broad equipment portfolios, global service networks, deep end-market expertise, and strong customer support structures, enabling them to capture demand across municipal wastewater, industrial processes, mining, and infrastructure sectors.

Download Free sample to learn more about this report.

Dewatering Equipment Market Trends

Shift Toward Resource Recovery and Sludge Valorization Are Driving Market Growth

A key trend shaping the dewatering equipment market is the growing shift from basic sludge disposal toward resource recovery and sludge valorization. Utilities and industries are increasingly viewing sludge as a resource rather than waste, driving demand for high-performance dewatering systems that enable downstream processes such as biogas production, nutrient recovery, and thermal treatment. Improved dewatering efficiency directly enhances the economics of anaerobic digestion and energy recovery by increasing solids concentration and reducing transport volumes. In several regions, especially Europe and parts of the Asia Pacific, wastewater treatment plants are being redesigned as resource recovery facilities, emphasizing energy neutrality and circular economy principles. This transition is accelerating the adoption of advanced centrifuges, filter presses, and screw presses that deliver higher cake dryness and consistent performance. As sustainability targets tighten and landfill disposal declines, sludge valorization is becoming a structural demand driver for advanced dewatering technologies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Wastewater Generation and Regulatory Pressure to Push the Market Growth

A key driver of the global dewatering equipment market is the rapid increase in wastewater and sludge volumes generated by urbanization and industrial activity, combined with tightening environmental regulations. Globally, more than 300 billion cubic meters of wastewater are generated each year, and an increasing proportion must undergo advanced treatment before discharge or reuse. Governments are enforcing stricter standards on sludge handling, landfill disposal, and water reuse, pushing municipalities and industries to invest in efficient dewatering technologies to reduce sludge volume and operating costs. Large-scale wastewater infrastructure programs in the Asia Pacific, the Middle East, and parts of Europe continue to add new treatment capacity, directly increasing demand for centrifuges, filter presses, and belt presses. Compliance-driven upgrades in mature markets further sustain replacement demand, making regulation-backed wastewater treatment expansion a structurally strong dewatering equipment market growth driver.

Market Restraints

High Capital and Operating Costs Limit Market Expansion

High upfront investment and ongoing operating costs remain a key restraint for the dewatering equipment market. Advanced systems such as high-capacity centrifuges and automated filter presses typically carry initial costs 20–30% higher than those of conventional or low-tech alternatives, discouraging adoption among smaller municipalities and industrial operators. Energy consumption, polymer usage, and maintenance requirements add to the total cost of ownership, with operating expenses accounting for a significant share of lifecycle costs. For budget-constrained users, especially in emerging markets, these cost factors often delay purchase decisions or push buyers toward refurbished equipment and rental solutions. As a result, despite clear efficiency and compliance benefits, cost sensitivity continues to restrain the faster penetration of advanced dewatering solutions.

Market Opportunities

Smart, Energy-Efficient, and Automated Dewatering Solutions to Create New Growth Avenues

A major opportunity in the dewatering equipment market lies in the growing adoption of smart, automated, and energy-efficient technologies. Digital monitoring, IoT-enabled sensors, and predictive maintenance capabilities are increasingly being integrated into dewatering systems, improving uptime and reducing operating costs. Adoption of smart water and wastewater technologies has accelerated, with a significant share of new treatment facilities incorporating automation and data-driven controls. Energy-efficient drives, improved polymer dosing systems, and modular designs are also gaining traction as operators focus on sustainability and lifecycle cost reduction. Rapid wastewater infrastructure expansion in the Asia Pacific and the Middle East, combined with modernization needs in Europe and North America, creates strong opportunities for suppliers offering technologically advanced, low-energy, and digitally enabled dewatering solutions.

Market Challenges

Infrastructure Gaps and Uneven Market Development to Limit Market Growth

A major challenge for the dewatering equipment market is the uneven development of wastewater and industrial infrastructure across regions. In many developing economies, a significant share of wastewater is still discharged untreated due to limited treatment capacity, creating a deployment gap of roughly one-third for modern dewatering systems. Funding constraints, project delays, and weak institutional capacity slow the rollout of new treatment plants and upgrades. Additionally, differences in sludge disposal regulations and enforcement levels across countries create uncertainty for equipment suppliers and end users. Supply chain disruptions and long equipment lead times have further complicated project execution in recent years. These factors collectively limit the pace of adoption of advanced dewatering technologies in high-need but capital-constrained markets.

Segmentation Analysis

By Equipment Type

High Importance of Wastewater Sludge Handling to Lead the Sludge Dewatering Equipment Segment Growth

Based on equipment type, the market is segmented into sludge dewatering equipment and other dewatering equipment.

Sludge dewatering equipment accounts for approximately 62.35% of the market share. The segment is expected to grow at a significant rate due to the rising volume of wastewater generated by rapid urbanization, industrialization, and population growth, which increase pressure on municipal and industrial wastewater treatment infrastructure to manage larger sludge streams effectively. Regulatory frameworks globally have become more stringent regarding wastewater discharge and biosolids handling, pushing utilities and industries to invest in reliable dewatering solutions to comply with environmental standards and reduce disposal costs. Additionally, advancements in technology, such as energy‑efficient systems, automation, and digital monitoring, are encouraging adoption, as they lower operational costs and improve performance while aligning with sustainability goals such as resource recovery and reduced carbon footprints.

Other dewatering equipment is expected to grow at a CAGR of 4.07% during the forecast period.

By Technology Type

Compact Configurations and Ability to Deliver Consistent Solids‑Liquid Separation Fuel the Segment Growth

Based on technology type, the market is segmented into pumps & wellpoint, centrifuges, filter, presses, dewatering screens, belt presses, and others.

Centrifuges account for 33.39% of the market share, due to their high separation efficiency and suitability for large‑scale industrial and wastewater applications. Their compact configurations and ability to deliver consistent solids‑liquid separation make them preferred in municipal wastewater treatment plants and in heavy industries such as mining and chemicals. Strong demand is underpinned by stringent environmental regulations, the need for high-throughput dewatering solutions, and ongoing technological upgrades that boost performance and reduce operating costs. As a result, centrifuges typically hold a significant share among dewatering technologies.

The dewatering screens segment is expected to grow at a CAGR of 5.60% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User Analysis

Stringent Environmental Regulations to Propel the Segment Growth

Based on end user, the market is segmented into industrial wastewater treatment, municipal, mining & mineral processing, oil & gas, construction, and others.

The municipal segment represents the largest dewatering equipment market share. It accounted for approximately 33.83% in 2025, driven by stringent environmental regulations and the need for efficient effluent handling from chemical, food & beverage, pharmaceutical, and other processing industries. Adoption is supported by significant investment in water recycling and sludge-volume-reduction technologies that reduce disposal costs and improve circular water use. Industrial players increasingly prefer advanced dewatering solutions with automation and real-time monitoring, bolstering demand for high-performance centrifuges and presses. This segment also benefits from growth in manufacturing activity in the Asia Pacific and emerging markets. The municipal segment was also the fastest-growing, with a 5.44% CAGR during the forecast period.

The industrial wastewater treatment segment is the second-largest segment, with a 25.04% share in 2025.

Dewatering Equipment Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Dewatering Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest region in 2025, valued at USD 3.46 billion, accounting for approximately 38.28% of global dewatering equipment revenues. Asia Pacific is the dominant region globally, fueled by rapid industrialization, urbanization, and extensive infrastructure development throughout China, India, Southeast Asia, and other developing economies. Expansion of municipal wastewater treatment plants, growth in mining and mineral processing, and large construction projects create a strong, diversified demand for dewatering solutions. Government initiatives to improve sanitation and environmental management further accelerate the adoption of both traditional and portable dewatering technologies across urban and rural settings.

China Dewatering Equipment Market

China remains the dominant contributor in Asia Pacific, valued at USD 1.55 billion in 2025. It is expected to be valued at USD 1.64 billion in 2026, fueled by rapid urbanization, large-scale infrastructure projects, and aggressive expansion of municipal wastewater treatment capacity. The government's focus on pollution control and industrial water reuse is accelerating the adoption of high-capacity dewatering equipment.

India Dewatering Equipment Market

India was valued at USD 0.64 billion in 2025 and is set to reach USD 0.68 billion in 2026, supported by urban infrastructure expansion, river cleaning programs, and rising investments in sewage and industrial effluent treatment. Growth is further reinforced by construction activity and increasing regulatory emphasis on sludge management and water conservation.

Japan Dewatering Equipment Market

Japan was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.47 billion in 2026. The modernization of aging wastewater infrastructure and strict environmental compliance standards shape Japan’s demand for dewatering equipment. Advanced, compact, and energy-efficient technologies are preferred due to space constraints and high operational efficiency requirements.

North America

North America was valued at USD 2.48 billion in 2025, accounting for approximately 27.43% of the global dewatering equipment market. North America holds a significant position in the market, supported by stringent environmental and wastewater regulations that drive investment in advanced treatment and dewatering technologies. Strong municipal and industrial applications, particularly in the U.S. and Canada, fuel demand for systems that improve sludge handling and water recovery. The construction and mining sectors also contribute substantially, requiring reliable seasonal and project-based dewatering solutions. Technological innovation, including automated and IoT-enabled equipment, further strengthens market activity across the region.

U.S. Dewatering Equipment Market

The U.S. dewatering equipment market was estimated at USD 2.14 billion in 2025 and is anticipated to reach USD 2.24 billion in 2026, driven by stringent environmental regulations and sustained investment in municipal wastewater upgrades and industrial water management. Strong construction, shale oil & gas activity, and mining also support steady demand for advanced and mobile dewatering systems.

Europe

Europe accounted for USD 2.18 billion in 2025, representing approximately 23.89% of global revenues. The region maintains robust demand for dewatering equipment, driven by sustainability and circular economy initiatives that emphasize water reuse, energy-efficient processes, and reduced environmental impact. Advanced wastewater treatment facilities in Germany, France, and the U.K. integrate highly efficient dewatering technologies to meet strict EU standards. Growth is bolstered by the ongoing modernization of aging infrastructure and the adoption of automated systems that enhance operational efficiency. Public investment in water quality and resource recovery continues to push market expansion.

Germany Dewatering Equipment Market

Germany was estimated at USD 0.55 billion in 2025 and is set to reach USD 0.57 billion in 2026. Germany benefits from strong industrial wastewater treatment needs and from leadership in sustainable, energy-efficient water technologies. Circular economy practices and advanced sludge processing initiatives drive consistent demand for high-performance dewatering solutions.

U.K. Dewatering Equipment Market

The U.K. market was valued at USD 0.32 billion in 2025 and is expected to reach USD 0.34 billion in 2026, driven by regulatory pressure on water utilities to improve sludge handling and meet environmental discharge targets. Ongoing upgrades of wastewater treatment facilities and infrastructure resilience projects support steady equipment adoption.

Latin America

Latin America accounted for USD 0.38 billion in 2025, or approximately 4.22% of global revenues. The region’s growth is driven by infrastructure modernization and mining activities as key drivers of development. Countries such as Brazil, Mexico, and Argentina are increasing investments in wastewater management and industrial water treatment, boosting demand for dewatering equipment. The construction sector also contributes, especially through public-private partnerships that integrate effective water removal solutions into larger projects. While smaller in scale than in North America and the Asia Pacific, steady regional growth reflects rising environmental awareness and policy support.

Middle East & Africa

The Middle East & Africa were valued at USD 0.56 billion in 2025. The region, though a smaller share of the global market, is expanding due to water scarcity, oil & gas operations, and rapid urban development, especially in Gulf Cooperation Council (GCC) countries. Demand for dewatering technologies is tied to industrial wastewater handling, desalination plant support infrastructure, and construction dewatering needs in growing cities. In sub-Saharan Africa, basic dewatering and mobile systems are increasingly adopted to address grassroots sanitation and water management needs, supported by international funding and NGO initiatives.

GCC Dewatering Equipment Market

The GCC market was estimated at USD 0.25 billion in 2025 and is set to reach USD 0.27 billion in 2026. The GCC region witnesses demand primarily from construction, oil & gas operations, and industrial wastewater treatment linked to desalination and urban expansion. Water scarcity and large infrastructure projects continue to underpin the adoption of robust, mobile dewatering systems. Saudi Arabia is addressing extreme water scarcity by making water security a national priority. With agriculture accounting for most water use and climate change increasing drought risks, the Kingdom has launched the National Water Strategy 2030 in line with Vision 2030 and SDG 6. The strategy places strong emphasis on water governance, efficiency, and sustainability to support long-term development.

Competitive Landscape

KEY INDUSTRY PLAYERS

The Extensive Water Technologies Portfolio is a Booming Market Share for the Companies.

Veolia, Alfa Laval, ANDRITZ AG, SUEZ Water Technologies & Solutions, and Xylem Inc. are key players in this market. Veolia Environment S.A. is widely regarded as a leading company in the global dewatering equipment and water treatment market, due to its extensive water technologies portfolio, global reach, and integrated environmental services. The company combines advanced dewatering and wastewater treatment solutions with broader water management services, serving municipal and industrial customers in more than 130 countries through Veolia Water Technologies & Solutions.

List of Key Dewatering Equipment Companies Profiled:

- Veolia (France)

- Alfa Laval AB (Sweden)

- ANDRITZ AG (Austria)

- SUEZ Water Technologies & Solutions (France)

- Huber SE (Germany)

- Evoqua Water Technologies LLC (U.S.)

- Komline-Sanderson Engineering Corporation (U.S.)

- Flottweg SE (Germany)

- Xylem Inc. (U.S.)

- GEA Group AG (Germany)

- Aqseptence Group, Inc. (Germany)

- Phoenix Process Equipment Co. (U.S.)

- FLSmidth & Co. A/S (Denmark)

- Hitachi Zosen Corporation (Japan)

- Kurita Water Industries Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Metso secured a major order from Barrick Mining’s Reko Diq Mining Company to supply advanced flotation and dewatering equipment for the Reko Diq copper-gold project in Pakistan. Valued at about USD 82 million, the contracts cover Metso Plus beneficiation solutions, with orders booked across the third and fourth quarters of 2025. The delivery includes a complete, modern flotation flowsheet combining TankCell® technology for rougher and scavenger stages with Concorde Cell™ units for ultrafine particle cleaning, designed to enhance recovery and process efficiency.

- May 2025: Pelagia, a pelagic fish product solutions company headquartered in Bergen, Norway, acquired aquaculture equipment supplier Fjord Solutions. Through this acquisition, Pelagia expands its Blue Ocean Technology portfolio, strengthening its capabilities in sludge dewatering, water treatment, and storage solutions. The deal enables Pelagia to provide a more comprehensive sludge management offering while integrating Fjord Solutions’ workforce, technologies, and intellectual property.

- December 2023: Andritz secured an order from Rondo Ganahl AG to upgrade dewatering and dispersing systems at its paper mill in Frastanz, Austria, with start-up planned by the end of 2024. The project involves replacing the entire dewatering line to boost system capacity to 230 bdt/day and improve process efficiency. A key element is a space-optimized Twin Wire Press designed for high pulp dryness and effective water separation, along with engineering support, installation supervision, commissioning, and operator training.

- February 2023: Atlas Copco introduced a new range of electric, self-priming surface dewatering pumps designed for diverse applications. Available in canopy and open-set versions, the E-Pump range is engineered to handle high flows and large solids efficiently. By offering electric, diesel-free operation with digital connectivity, the E PAS and PAC models help lower operating costs, eliminate CO₂ emissions from pumping, and enable use in emission-restricted environments.

- October 2021: Wayss & Freytag Ingenieurbau and Ed. Züblin formed a joint venture to build a 7.4 km drainage tunnel for the former Ibbenbüren coal mine in Germany. Awarded by RAG Aktiengesellschaft, the project will use two tunnel boring machines to excavate parallel tunnel sections from separate access points. The scope also includes the construction of a TBM launch section and a deep central shaft to enable long-term mine water drainage.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.52% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology Type · Pumps & Wellpoints · Centrifuges · Filter Presses · Dewatering Screens · Belt Presses · Others |

|

By End User · Industrial Wastewater Treatment · Municipal · Mining & Mineral Processing · Oil & Gas · Construction · Others |

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.03 billion in 2025 and is projected to reach USD 13.52 billion by 2034.

The market is likely to grow at a CAGR of 4.52% over the forecast period (2026-2034).

By technology type, the centrifuges segment is leading the market.

The Asia Pacific market size stood at USD 3.46 billion in 2025.

Rising wastewater generation and regulatory pressure are the key factors driving the market.

Some of the leading players in the market include Veolia, Alfa Laval, ANDRITZ AG, SUEZ Water Technologies & Solutions, and Xylem Inc., among others.

The global market size is expected to reach USD 13.52 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 227

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us