Digital Battlefield Market Size, Share, Industry Analysis and Russia-Ukraine War Impact Analysis, By Component (Hardware, Software, and Services), By Technology (5G, IoT, AI, Blockchain, Cloud Computing, Big Data, AR and VR, and Others), By Installation (New Installations and Upgrade), By End Use (Land, Naval, Air, and Space) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

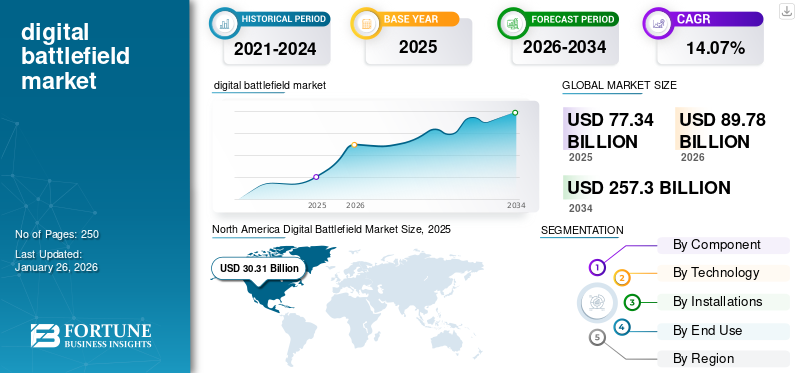

The global digital battlefield market size was valued at USD 77.34 billion in 2025. The market is projected to grow from USD 89.78 billion in 2026 to USD 257.30 billion by 2034, exhibiting a CAGR of 14.07% during the forecast period.

The market encompasses the integration of advanced digital technologies into military operations to enhance situational awareness, decision-making, and combat effectiveness. It includes hardware such as sensors, communication devices, and specialized equipment, software for data analytics and command & control, and services such as integration, maintenance, and training. Key technologies driving the market include Artificial Intelligence (AI), internet of things (IoT), 5G, cloud computing, big data analytics, augmented reality (AR), and virtual reality (VR). The market growth is fueled by the increasing need for real-time information, improved communication, enhanced cybersecurity, and greater automation.

The COVID-19 pandemic had a mixed impact on the market. While supply chain disruptions initially slowed down hardware production and project deployments, the pandemic also accelerated the demand for remote monitoring, autonomous systems, and telemedicine in military applications. As a result, investments in digital transformation and advanced technologies increased, partially offsetting the initial challenges.

Key players in the market include major defense contractors such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, General Dynamics, and BAE Systems. Tech companies such as Microsoft, IBM, Intel, and Amazon are also significant participants, providing cloud computing, AI, and cybersecurity solutions. Smaller innovative companies and startups are contributing with specialized hardware, software, and services, driving technological advancements. The market is characterized by intense competition, strategic partnerships, and continuous innovation to develop and deploy advanced digital battlefield solutions.

Download Free sample to learn more about this report.

Digital Battlefield Market Key Takeaways

- 2025 Market Size: USD 77.34 billion

- 2026 Market Size: USD 89.78 billion

- 2034 Forecast Market Size: USD 257.30 billion

- CAGR: 14.07% from 2026–2034

- North America dominated the digital battlefield market with a 39.19% share in 2025.

- The land segment is projected to hold a 12.14% market share in 2026.

- The hardware segment is projected to account for an 11.17% market share in 2026.

North America

North America held a 39.19% share in 2025, valued at USD 30.31 billion.

Asia Pacific

Asia Pacific accounted for 27.23% share in 2025, valued at USD 21.06 billion.

Europe

Europe held a 21.57% share in 2025, valued at USD 16.68 billion.

U.S.

The market projected to reach USD 31.14 billion by 2026.

Japan

The market projected to reach USD 5.14 billion by 2026.

Read More

RUSSIA-UKRAINE WAR IMPACT

Accelerated Digitalization and Rising Significance of Cybersecurity Has Boosted Market Growth

The Russia-Ukraine war has profoundly impacted the market, significantly accelerating the adoption of advanced digital technologies and placing an unprecedented emphasis on cybersecurity. The conflict has demonstrated the critical importance of real-time intelligence, secure communication networks, and advanced weaponry in modern warfare. Nations are now rapidly investing in digital infrastructure, including advanced sensors, AI-driven analytics, and cloud computing platforms, to enhance situational awareness and decision-making capabilities. The conflict has also highlighted the vulnerability of digital systems to cyberattacks, leading to a surge in the demand for robust cybersecurity solutions to protect critical military assets and infrastructure.

The war has exposed the limitations of traditional warfare tactics and has also emphasized growing importance of information dominance. This realization has prompted countries to prioritize investments in unmanned systems, satellite-based communication, and advanced command and control systems. Additionally, the conflict has emphasized the need for enhanced interoperability between different branches of the military and allied forces, driving the adoption of standardized digital platforms. The Russia-Ukraine war has served as a catalyst for digital transformation in the defense sector, reshaping procurement strategies and driving innovation across the market.

DIGITAL BATTLEFIELD MARKET TRENDS

Rise of Autonomous Systems and AI Integration

A prominent trend in the market is the increasing integration of Artificial Intelligence (AI) and the proliferation of autonomous systems. AI is being embedded into a wide range of military applications, spanning from surveillance and reconnaissance to target identification and autonomous weapons platforms. Machine learning algorithms are being utilized to analyze vast amounts of data, enabling predictive analytics and improved decision-making. This trend is driving innovation in areas such as unmanned aerial vehicles (UAVs), autonomous ground vehicles (AGVs), and robotic systems capable of operating in complex and contested environments.

The development of AI-powered solutions is also leading to the automation of various military tasks, reducing the workload on human operators and enhancing operational efficiency. Additionally, the integration of AI is facilitating the development of intelligent cyber defense systems, capable of detecting and responding to cyberattacks in real-time.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Geopolitical Tensions and Modernization Efforts to Propel Market Growth

Escalating geopolitical tensions and the increasing frequency of armed conflicts worldwide are major drivers of the digital battlefield market. Nations are investing heavily in modernizing their military capabilities to address emerging threats and secure a competitive edge. This modernization process involves the adoption of advanced digital technologies to enhance situational awareness, improve command and control, and increase combat effectiveness.

The desire to reduce casualties and minimize human involvement in dangerous missions is also driving the demand for unmanned systems and autonomous technologies. Furthermore, the need to counter asymmetric warfare tactics and hybrid threats is prompting the development of advanced cybersecurity and intelligence gathering solutions.

MARKET RESTRAINTS

High Costs and Integration Complexity to Hamper the Market Growth

The high costs associated with the development, deployment, and maintenance of digital battlefield solutions can restrain the growth of the market. The advanced technologies involved often require significant upfront investments and ongoing operational expenses. The complexity of integrating new digital technologies with existing legacy systems is another significant restraint. Many military organizations still rely on outdated infrastructure, making it difficult to implement advanced solutions. Ensuring compatibility and seamless integration is essential but often requires extensive customization and upgrades.

MARKET CHALLENGES

Ensuring Interoperability and Data Security to Create Challenges for Market Expansion

Ensuring interoperability between different systems and platforms remains a major challenge for market expansion. The lack of standardization and the proliferation of proprietary technologies can hinder the seamless exchange of information and limit the effectiveness of joint operations. Another significant challenge is ensuring data security and protecting sensitive information from unauthorized access. The risk of cyberattacks and data breaches is a major concern, requiring the implementation of robust security measures and the development of advanced encryption techniques.

MARKET OPPORTUNITIES

Surging Need for Cybersecurity Solutions and Data Analytics Platforms to Offer New Opportunities for Growth

A significant opportunity in the market lies in the development and deployment of robust cybersecurity solutions to protect critical military assets and infrastructure. The increasing reliance on digital networks and interconnected systems makes military operations more vulnerable to cyberattacks.

There is also a growing need for advanced data analytics platforms to process and analyze the vast amounts of data generated by sensors, satellites, and other sources. These platforms can provide valuable insights for intelligence gathering, threat assessment, and operational planning. The development of cloud-based solutions and secure data storage infrastructure is also presenting lucrative opportunities for companies in the market.

SEGMENTATION ANALYSIS

By End Use

Land Segment to Expand with Rising Implementation of Ground-Based Digital Battlefield Technologies for Military Operations

By end use, the market is classified into land, naval, air, and space.

The space segment is projected to be the fastest-growing segment in the market. This growth is driven by a rising dependence on satellite-based technologies for reconnaissance, surveillance, and communication in military operations. Space assets offer essential capabilities for real-time intelligence collection, global positioning, and the enhancement of command and control functions across various operational theaters. The advanced digital battlefield solutions demand within the space segment is poised to surge significantly as defense agencies emphasize the importance of space-based assets, including space-based sensors and satellite constellations, to bolster their strategic capabilities.

By Component

Hardware Segment Led the Market Due to Rising Demand for Sophisticated Physical Components

By component, the market is classified into hardware, software, and services.

The hardware segment is expected to lead the market with a share of 11.17% in 2026. primarily due to the rising demand for sophisticated physical components, including sensors, communication devices, and unmanned systems. The continuous progress in these technologies, along with significant defense investments aimed at enhancing and expanding hardware capabilities, resulted in remarkable segment growth, establishing it as the leading segment in the market.

The services segment is the fastest growing segment. This growth is propelled by the increasing necessity for ongoing support, maintenance, and upgrades of intricate digital battlefield systems. As military and defense organizations embrace advanced technologies, they necessitate specialized services such as cybersecurity, training, systems integration, and data analytics to guarantee optimal performance and adaptability. The swift advancement of technology and the imperative for continuous operational readiness further stimulate the demand for comprehensive service solutions.

To know how our report can help streamline your business, Speak to Analyst

By Installation

New Installations Segment Leads the Market Due to Integration of Sophisticated Digital Technologies by Defense Forces

Based on installation, the market is bifurcated into new installations and upgrade.

The New Installations segment is projected to dominate the market with a share of 14.28% in 2026. The new installations segment dominates the market attributed to continuous modernization initiatives and the integration of sophisticated digital technologies by defense forces across the globe. Governments and military entities are channeling investments into the enhancement of their infrastructure through the implementation of cutting edge digital battlefield systems, aimed at improving operational capabilities and ensuring technological dominance. This encompasses the deployment of new installations featuring integrated IoT devices, AI-powered command and control centers, secure communication networks, and unmanned systems, indicative of a strong demand for advanced military installations worldwide.

The upgrade segment is the fastest-growing category as defense forces increasingly emphasize the improvement of existing infrastructure with state-of-the-art technologies. In light of rapid technological progress and shifting threat environments, military organizations are concentrating on upgrading their digital battlefield systems to sustain competitiveness and operational efficiency.

By Technology

IoT Segment Dominates Due to Increasing Adoption of Interconnected Devices and Sensors

Based on technology, the market is subdivided into 5G, IoT, AI, blockchain, cloud computing, big data, AR and VR, and others.

The IoT segment is expected to hold the largest digital battlefield market share of 6.24% in 2026. attributed to the increasing adoption of interconnected devices and sensors that improve situational awareness and operational efficiency. The combination of IoT with other cutting-edge technologies, including AI and robotics, facilitates more coordinated and effective military operations. This extensive deployment of IoT solutions in military contexts has greatly contributed to the dominance of the segment.

The AI segment is the fastest-growing segment owing to its crucial role in improving autonomous decision-making, predictive analytics, and operational efficiencies. AI algorithms empower military systems to process large volumes of data in real time, recognize patterns, and autonomously adjust to changing battlefield conditions. Defense agencies are increasingly focusing on AI-driven technologies for intelligence gathering, threat detection, and mission planning, leading to a significant rise in the demand for AI solutions in the digital battlefield, which is expected to propel substantial growth in this segment.

DIGITAL BATTLEFIELD MARKET REGIONAL OUTLOOK

Based on region, the market is segmented into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Digital Battlefield Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 30.31 billion in 2025 and is projected to reach USD 34.96 billion in 2026. The North America market has captured the largest market share, propelled by significant investments in artificial intelligence, cybersecurity, and unmanned systems, which enhance defense capabilities. With a strong defense industrial base and considerable government funding, this region is at the forefront of developing innovative technologies aimed at improving military readiness and operational efficiency. The U.S. market is projected to reach USD 31.14 billion by 2026.

The U.S. is making rapid progress, supported by substantial investments in military research and development, as well as partnerships between defense contractors and technology companies. The nation's strategic initiatives focus on AI-driven decision-making, resilience in cybersecurity, and the incorporation of unmanned systems for various military uses. The U.S. military's commitment to maintaining technological superiority is fostering ongoing advancements in digital warfare capabilities, placing it at the leading edge of the global market.

Europe

Europe accounted for USD 16.68 billion in 2025, representing 21.57% of the global market share, and is projected to reach USD 19.38 billion in 2026. driven by strong defense expenditures and the adoption of advanced technologies in military operations. Initiatives by the European Union aimed at defense collaboration and technological innovation are promoting partnerships among member states, which in turn enhances advancements in digital battlefield capabilities and secures strategic autonomy in defense matters. The U.K. market is projected to reach USD 4.97 billion by 2026, while the Germany market is projected to reach USD 4.39 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 21.06 billion in 2025, capturing 27.23% of global revenue, and is estimated to reach USD 24.76 billion in 2026. attributed to the swift modernization of military forces, which is increasing the demand for sophisticated digital warfare solutions. The geopolitical landscape and rising defense budgets in this area are stimulating innovation in unmanned systems, cyber warfare, and satellite technologies, thereby influencing the future of military operations in Asia Pacific. The Japan market is projected to reach USD 5.14 billion by 2026, the China market is projected to reach USD 9.96 billion by 2026, and the India market is projected to reach USD 6.69 billion by 2026.

Rest of the World

The market in the rest of the world is expected to experience the moderate compound annual growth rate (CAGR). The region's strategic positioning and geopolitical factors are propelling the demand for cybersecurity solutions, unmanned systems, and surveillance technologies to tackle emerging threats and ensure stability.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Innovation by Key Players to Reshape the Digital Battlefield Landscape

Among the prominent participants in the market are Lockheed Martin Corporation and Northrop Grumman Corporation, along with several others.

Lockheed Martin Corporation is a company specializing in aerospace, defense, and security. It is recognized as a contractor for its cutting-edge technology platforms and solutions that span air, land, sea, space, and cyber domains. Lockheed Martin boasts a varied portfolio that features fighter jets such as the F-35 Lightning II, missile systems, satellite systems, and sophisticated cybersecurity capabilities. The company's advancements in autonomous systems, artificial intelligence, and advanced manufacturing play a crucial role in defining the future of defense capabilities.

Northrop Grumman Corporation, noted for its proficiency in autonomous systems and cybersecurity, delivers essential capabilities for contemporary warfare settings. Their innovation significantly helps improve operational efficiency and situational awareness in combat scenarios.

LIST OF KEY COMPANIES PROFILED

- Airbus S.A.S (France)

- AeroVironment, Inc. (U.S.)

- BAE Systems, Inc. (U.S.)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corporation (U.S.)

- L3Harris Technologies Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Nothrop Grumman Corporation (U.S.)

- RTX Corporation (U.S.)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- July 2025 - The Chief Digital and Artificial Intelligence Office (CDAO) (U.S.) announced the awarding of contracts to prominent U.S. frontier AI companies, aimed at expediting the Department of Defense (DoD)'s adoption of advanced AI capabilities to tackle significant national security challenges.

- April 2025 - NATO declared that it granted a contract to Palantir for the implementation of its Maven Smart System, which is designed for artificial intelligence-enhanced battlefield operations. The NATO Communications and Information Agency (NCIA) intends to utilize a variant of the AI system — Maven Smart System NATO — to assist the strategic command of the Allied Command Operations within the transatlantic military organization.

- January 2025 - Leonardo DRS, Inc., announced that it received a contract to supply the U.S. Army with advanced Mortar Fire Control Systems (MFCS). This firm fixed-price IDIQ contract is valued at over USD 99 million.

- October 2024 - QinetiQ secured a three-year contract to offer Defence Digital engineering and program expertise aimed at facilitating the development of the next generation of tactical military communications. This contract is associated with the Land Environment Tactical Communications and Information Systems (LETacCIS) Programme, which will empower the British Army to make more informed and timely decisions while operating on the front line.

- July 2024 - V2X, Inc., announced the receipt of a USD 48.5 million Indefinite Delivery Indefinite Quantity (IDIQ) contract from the U.S. Army, managed under the PEO Soldier portfolio, for the cutting-edge Gateway Mission Router (GMR). The GMR establishes a fully integrated operational environment on the battlefield for soldiers by effortlessly merging information and reliable communications across various domains.

REPORT COVERAGE

The research report offers a comprehensive market analysis, identifying key players, product categories, and primary applications. It also details market trends and significant industry developments. Moreover, the report highlights various factors that have fueled the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.07% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Component

|

|

By Technology

|

|

|

By Installation

|

|

|

By End Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 77.34 billion in 2025 and is estimated to reach USD 257.30 billion by 2034.

The market will grow steadily at a CAGR of 14.07% during the projection period (2026-2034).

By component, the hardware segment is the leading segment in this market.

Airbus S.A.S (France), AeroVironment, Inc. (U.S.), BAE Systems, Inc. (U.S.), Elbit Systems Ltd. (Israel), General Dynamics Corporation (U.S.), L3Harris Technologies Inc. (U.S.), Lockheed Martin Corporation (U.S.) are some of the leading OEMs in the market.

North America holds the largest share in the global market.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us