Digital Health Systems Market Size, Share & Industry Analysis, By Type (EMR/HER, e-Prescribing System, and Others), By End-User (Healthcare Providers, Healthcare Payers, and Others), and Regional Forecast, 2026-2034

DIGITAL HEALTH SYSTEMS MARKET SIZE AND FUTURE OUTLOOK

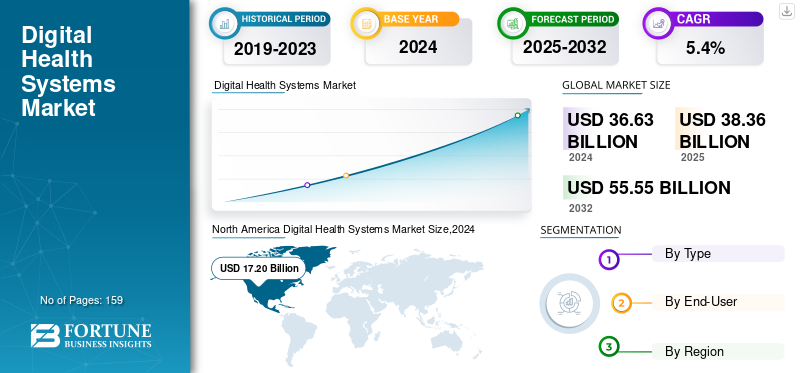

The global digital health systems market size was valued at USD 38.36 billion in 2025. The market is projected to grow from USD 40.24 billion in 2026 to USD 55.05 billion in 2034, exhibiting a CAGR of 3.99% during the forecast period. North America dominated the global digital health systems market with a market share of 47.24% in 2025.

A digital health system uses digital technologies to improve healthcare delivery by making it more accessible, affordable, and sustainable. It includes a broad range of technologies and applications that aim to improve healthcare outcomes by promoting wellness, managing illnesses, and providing personalized care. The market is undergoing transformative growth, driven by the rising adoption of telehealth, mobile health (mHealth), and Electronic Health Records (EHRs). Additionally, the market is reflecting robust momentum supported by AI integration, remote patient monitoring, and digital therapeutics. This is further propelled by the need for cost-efficient healthcare models, aging populations, and increasing investments in digital healthcare infrastructure globally.

Prominent market players such as Oracle, Epic Systems Corporation, Veradigm LLC, and others are actively engaged in offering innovative solutions integrated with advanced technologies to maintain their market positions.

Download Free sample to learn more about this report.

Digital Health Systems Market Takeaways

- 2025 Market Size: USD 38.36 billion

- 2026 Market Size: USD 40.24 billion

- 2034 Forecast Market Size: USD 55.05 billion

- CAGR: 3.99% from 2026–2034

- North America dominated the digital health systems market with a 47.24% share in 2025.

- The EMR/EHR segment held the largest market share in 2026 due to widespread adoption across healthcare facilities.

- The healthcare providers segment accounted for the dominant share in 2026, supported by growing EHR implementation and digital healthcare investments.

North America

North America led the market with a valuation of USD 18.12 billion in 2025.

Europe

Europe dominated the market with a valuation of USD 8.79 billion in 2025 and is expected to reach USD 9.22 billion in 2026.

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 6.73 billion in 2025 and is expected to reach USD 7.01 billion in 2026.

U.S.

Strong adoption of digital health systems among healthcare providers and strategic partnerships continue to support market expansion.

Japan

Increasing healthcare digitalization and investments in advanced health IT solutions are supporting market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Digital Healthcare to Propel Market Growth

In recent years, with increasing penetration of telecommunication and internet, healthcare is shifting toward digitalization. This is one of the major factors driving the digital health systems market growth. With increased smartphone penetration and regulatory support, virtual consultations have become a staple in healthcare delivery across urban and rural regions. Devices such as smartwatches and biosensors provide real-time data on cardiovascular health, glucose levels, and sleep patterns, improving preventive care strategies. In addition, software-driven therapeutic solutions are now approved and prescribed for conditions such as Type 2 diabetes, depression, and insomnia, reshaping treatment landscapes. All these factors have resulted in increasing usage of digital health systems, in turn propelling the market growth.

Healthcare systems are increasingly using these digital tools owing to their several benefits. These devices allow healthcare providers to remotely monitor patients, and offer virtual consultations leading to better patient outcomes.

- For instance, as per the data provided by the American Medical Association in 2022, the percentage of physicians using remote monitoring devices increased from 12% in 2016 to 30% in 2022.

MARKET RESTRAINTS

Technology Access Inequality Limits Market Growth

Even though the adoption of digital health systems is rapidly growing, there are certain factors that limit growth. Inequality in access to technology is one of the key factors hampering the market growth. A significant population in low-income or remote areas still lacks access to smartphones, internet connectivity, or digital health literacy.

- For instance, according to the Broadband Commission for Sustainable Development 2023 data, 93.0% of the population is estimated to use internet in high-income countries. Comparatively, 62.0% of the population have internet access in low-and-middle-income countries and 27.0% in low-income nations.

Additionally, as digital health platforms scale-up, they become prime targets for cyberattacks. Securing personal health data and complying with regulations such as HIPAA and GDPR are top concerns.

MARKET OPPORTUNITIES

Technological Advancements to Offer a Strong Growth Opportunity

In recent years, the market has witnessed a strong shift toward the development and integration of advanced technologies. Integration of artificial intelligence is revolutionizing diagnostic imaging, clinical decision support, and patient risk profiling, resulting in improved efficiency and reduced operational burdens. Thus, market players are focusing on integration of AI in their product offerings. These systems can analyze large amounts of data to identify patterns, predict outcomes, and personalize care, ultimately leading to more efficient and effective healthcare delivery.

For instance, eClinicalWorks is one of the operating players in the market that offer AI driven EHR systems.

Furthermore, blockchain is also gaining adoption to maintain immutable, interoperable, and privacy-compliant digital health records, especially in cross-border data exchange contexts.

MARKET CHALLENGES

Regulatory Variability and Challenges Associated With System Integration and Interoperability

The regulatory framework for digital health solutions is stringent due to the concerns associated with data privacy and cybersecurity. In addition, these systems face inconsistent regulatory standards across different countries, complicating international product launches and compliance. This creates a significant challenge for market players to capture untapped regions.

Additionally, due to the inconsistent penetration of internet across the globe, the exchange of data is another concern. Disparate health IT ecosystems make integration difficult, limiting seamless care coordination between providers and healthcare settings.

DIGITAL HEALTH SYSTEMS MARKET TRENDS

Rising Number of Investments by Emerging Players is a Significant Market Trend

With the rising demand and adoption of digital health systems among the healthcare providers as well as patients, the number of health-tech start-ups offering innovative solutions is also increasing. Additionally, increasing investments by companies for the development and introduction of advanced products for various applications is also boosting market growth. The number of companies offering digital platforms for cognitive behavioral therapy (CBT), online counseling, and meditation support is also increasing and are being rapidly adopted, especially post-COVID-19 pandemic.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

SEGMENTATION ANALYSIS

By Type

Increasing Implementation of EHR Systems Led to Dominance of EMR/HER Segment

Based on type, the market is divided into EMR/HER, e-prescribing system, and others.

In 2026, the EMR/EHR segment dominated the global market with highest share driven by increasing implementation of these systems by various healthcare facilities including, hospitals, clinics, and others. Additionally, technological advancements by companies in their product offerings also resulted in growing demand for these systems across end-users.

- For instance, in March 2023, Coryell Health introduced OracleCerner EHR to accelerate efficiencies.

The e-prescribing system segment is expected to witness the fastest growth during the forecast period fueled by the increasing number of e-prescriptions.

- For instance, according to an article published by the Office of the National Coordinator for Health IT in July 2024, in 2020, 92% of the total prescribers were e-prescribers.

By End-user

Growing Need to Manage Administrative Workload Structurally Drives Growth of Healthcare Providers

On the basis of end-user, the market is segmented into healthcare providers, healthcare payers, and others.

The healthcare providers segment held the dominant share of the market in 2026. The demand for these systems is driven by factors such as government incentives, shift toward value-based care, and improved efficiency and data sharing. This demand is impacting the entire industry, leading to increased investment in EHR solutions and a rising need for skilled professionals in health informatics. Additionally, EHR systems are evolving, where clinical decision support, advanced analytics, and patient portals can be integrated, enhancing their value among healthcare professionals.

The healthcare payers and others segments are anticipated to witness a notable growth in the coming years. This is primarily due to the increasing adoption of digital health systems by end users in the past few years.

DIGITAL HEALTH SYSTEMS MARKET REGIONAL OUTLOOK

By region, this market is divided into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America maintained a strong presence in the global market, reaching USD 18.12 Billion in 2025, accounting for 47.24% share, and is expected to reach USD 19.12 Billion in 2026 and is anticipated to continue its dominance in the global market. Mature healthcare ecosystem, government mandates for EHR adoption, and presence of key vendors and rapid cloud adoption are some of the factors promoting the market growth in the region.

North America Digital Health Systems Market Size,2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.S.

The U.S. held the dominating market share of the North American region in 2026. The growing adoption of digital health systems among healthcare providers along with the presence of well-established digital healthcare infrastructure are some of the key factors boosting the country’s dominance. Additionally, partnerships amongst key players further propel market growth.

- For instance, in May 2024, Axis Health System partnered with NextGen Healthcare for the implementation of NextGen Enterprise EHR (Electronic Health Record) system.

Europe

In 2025, Europe generated USD 8.79 Billion, contributing 22.92% to global market revenue, and is projected to grow to USD 9.22 Billion in 2026. The growth is driven by strong digital health strategies across European countries and increasing adoption of these systems.

- For example, according to an article published in the Pharmaceutical Journal in February 2023, the number of prescription items issued electronically reached 996 million in 2021/2022, accounting for 95% of all prescriptions.

Asia Pacific

The Asia Pacific market accounted for USD 6.73 Billion in 2025, representing 17.56% of the global industry, and is expected to reach USD 7.01 Billion in 2026. Increasing digital health initiatives undertaken by governments to boost the penetration of this technology coupled with rapidly expanding healthcare infrastructure in Asian countries are some of the factors supplementing the market growth.

- For instance, in September 2021, Ayushman Bharat Digital Mission was launched by the Government of India for the development of integrated digital health infrastructure in the country.

Latin America

Latin America contributed 6.18% to the global market in 2025, with a valuation of USD 2.37 Billion, and is projected to reach USD 2.45 Billion in 2026. These regions are considered to be the emerging markets for the digital health systems with the increasing access to telecommunications and developing healthcare infrastructure for digitalization.

Middle East & Africa

In 2025, Middle East & Africa represented USD 2.34 Billion, accounting for 6.11% of the worldwide market, and is projected to grow to USD 2.44 Billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Technological Advancements in Product Offerings by Prominent Players to Propel Market Progress

The competitive landscape for digital health systems market features both well-established as well as emerging players. Some of the prominent players include Oracle, Epic Systems Corporation, Veradigm LLC, and Practice Fusion, Inc. among others. They are focusing on introducing technologically advanced products and collaborating with healthcare providers to strengthen market presence.

Other notable players in the market include UI8, LLC., NXGN Management, LLC, CareCloud, Inc., and others. These companies are also focusing on various strategic initiatives to boost their digital health systems market share during the forecast period.

LIST OF KEY DIGITAL HEALTH SYSTEMS COMPANIES PROFILED

- Oracle (U.S.)

- UI8 LLC. (U.S.)

- Veradigm LLC (U.S.)

- NXGN Management, LLC. (U.S.)

- Practice Fusion, Inc. (U.S.)

- CareCloud, Inc. (U.S.)

- Tiga Healthcare Technologies (U.S.)

- Epic Systems Corporation (U.S.)s

KEY INDUSTRY DEVELOPMENTS

- February 2025: VSee Health, Inc. signed a USD 340K contract with a key EAP provider for the development of an AI-enabled EHR system.

- January 2025: IntelligentDX launched revolutionary AI-based deep learning software that optimizes Electronic Medical Records (EMR) and Electronic Health Records (EHR) systems.

- October 2024: Oracle announced its plans to introduce a new artificial intelligence-backed electronic health record in 2025. This new system will allow physicians to use voice for navigation and search.

- September 2024: Oracle introduced new electronic health record innovations to enhance information access, prioritize safety and offer other benefits as well.

- April 2024: Health First collaborated with Verona for the implementation of Epic EHR system to optimize workflow and to unify patient information.

REPORT COVERAGE

The global digital health systems market research report comprises of key aspects such as an overview of cutting-edge technologies, regulatory environment in major countries, and the challenges faced in adopting and implementing tech-based solutions. The report also provides notable industry developments, including mergers, partnerships, and acquisitions. Furthermore, it comprises of detailed regional analysis of various segments and market dynamics.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.99% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By End-User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market size was USD 40.24 billion in 2026 and is projected to reach USD 55.05 billion by 2034.

In 2025, North America’s market value stood at USD 18.12 billion.

Registering a CAGR of 3.99%, the market will exhibit rapid growth over the forecast period.

Based on type, the EMR/EHR segment leads the market.

Rising adoption of remote care as well as homecare and shift toward digital healthcare are some of the key factors driving the market.

Oracle, Veradigm LLC, and Practice Fusion, Inc., are some of the prominent players in the market.

North America dominated the global digital health systems market with a market share of 47.24% in 2025.

The increasing demand for advanced care options coupled with better patient outcomes are some of the factors expected to drive the adoption of the products.

- 2021-2034

- 2025

- 2021-2024

- 159

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us