Digital Shipyard Market Size, Share & Industry Analysis By Shipyard Type (Commercial, Military), By Technology Platform (Robotic Process Automation, Additive Manufacturing, Artificial Intelligence and Big Data Analytics, and others), By Digitalization Level (Semi Digital Shipyard, Fully Digital Shipyard) and Regional Forecast, 2026-2034

Digital Shipyard Market Size and Industry Overview

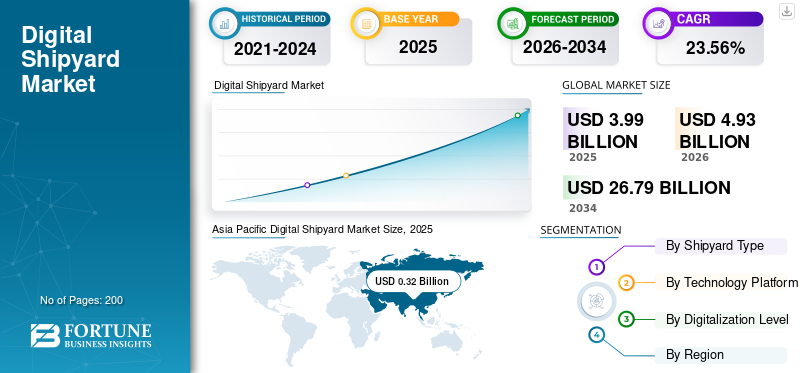

The global digital shipyard market size was valued at USD 3.99 billion in 2025. The market is projected to grow from USD 4.93 billion in 2026 to USD 26.79 billion by 2034, exhibiting a CAGR of 23.56% during the forecast period. Asia Pacific dominated the digital shipyard market with a market share of 33.55% in 2025.

The market growth is supported by sustained naval modernization programs and commercial fleet renewal. Defense authorities increasingly mandate digital continuity, model-based systems engineering, and secure data environments. These requirements elevate Digital shipyard platforms from productivity tools to mission-critical infrastructure within military shipyards.The

The Digital shipyard market reflects a structural transformation in global shipbuilding and maintenance operations. Digital shipyards integrate advanced software platforms, automation technologies, and data-driven workflows across vessel design, construction, and lifecycle management. Adoption is accelerating as shipyards respond to cost pressure, rising vessel complexity, and skilled labor constraints.

Commercial shipyards account for the largest share of installations by volume. Their investment focus centers on throughput optimization, schedule reliability, and labor efficiency. Military shipyards contribute a smaller share of deployments but generate higher revenue per project due to system complexity, cybersecurity requirements, and multi-decade lifecycle support obligations.

Technology adoption is strongest across artificial intelligence and big data analytics, additive manufacturing, and robotic process automation. Artificial intelligence improves production planning accuracy, quality assurance, and resource utilization. Additive manufacturing reduces lead times for spare parts and tooling while lowering inventory risk. Robotic process automation streamlines documentation, engineering change management, and regulatory compliance.

Regional adoption patterns vary by industrial maturity. North America and Europe lead in fully integrated Digital shipyard implementations. Asia-Pacific drives scale-based growth through smart shipyard investments in high-volume construction hubs. Emerging regions prioritize semi-digital shipyard models that deliver faster returns with lower capital exposure.

The adoption of Industry 4.0 capabilities in designing, manufacturing, and maintaining marine vessels is known as the digital shipyard. The shipyards use capabilities such as Internet of Things (IoT) and Cyber-Physical Systems (CPS) to upgrade the shipyards for a technologically advanced world. Systems such as 3D modelling, 3D scanning, 3D printing, digital twins, and others are utilized in the digitalization of a shipyard. Rising demand for modernization in shipbuilding is expected to propel the growth of this market.

Download Free sample to learn more about this report.

Digital Shipyard Market Key Takeaways

- 2025 Market Size: USD 3.99 billion

- 2026 Market Size: USD 4.93 billion

- 2034 Forecast Market Size: USD 26.79 billion

- CAGR: 23.56% from 2026–2034

- Asia Pacific dominated the digital shipyard market with a 33.55% share in 2025.

- The commercial segment is projected to hold the largest market share in 2025 and remain the fastest-growing segment during the forecast period.

- The Artificial Intelligence and Big Data Analytics segment is expected to account for a 28.22% market share in 2025.

Asia Pacific

With a market size of USD 323.3 million in 2020, Asia Pacific is expected to have the largest market share and grow at a faster compound annual growth rate during the projected period.

North America

The North American market is expected to grow due to increased research and development initiatives by key companies, such as Altair Engineering Inc. and others, to digitize shipyards.

Europe

Europe is expected to expand steadily as shipbuilders increase investments in automated robotics and advanced industrial technologies.

U.S.

The market is supported by federal procurement standards and defense-sector digitalization programs, encouraging the adoption of advanced digital shipyard solutions.

Japan

Market growth is driven by workforce demographic challenges, stringent quality assurance requirements, and the adoption of digital platforms, robotics, and artificial intelligence to improve operational reliability.

Read More

Digital Shipyard Market Trends

Increasing Demand for Additive Manufacturing is a Prominent Trend

Additive manufacturing, also known as 3D printing, can print a 3D digital model in very little time. Recent technological advances in 3D printers have enabled printing larger components as well. The material of 3D printing is not limited to plastic anymore. Advanced printer systems can also create parts from metal using a technique of high-velocity particle fusion. The adoption of additive manufacturing in shipyards can reduce system repair time, as one can print and replace the damaged part.

Download Free sample to learn more about this report.

Market Drivers & Trends

Increased Industrial Internet of Things (IIoT) Use in Shipbuilding to Boost Growth

By merging the IoT's communication capabilities with machine learning and big data, the digital shipyard leverages the IIoT to improve its decision-making skills and manufacturing processes. The market is expected to rise due to the increasing usage of IIoT in the shipbuilding industry to boost output, minimize downtime, and improve operational efficiency.

In December 2019, Navantia, a European shipyard, chose Siemens Digital Industries Software as its technological partner to digitalize its shipbuilding process.

Rising Implementation of Robot Technology in the Shipbuilding Industry to Fuel Market Growth

Shipbuilding companies worldwide are focusing on automating manufacturing operations such as cutting, welding, painting, assembly, and others to speed up the process and save costs. Several key players, such as Hyundai Heavy Industries, Samsung Heavy Industries, and Daewoo Shipbuilding & Marine Engineering, have implemented welding robots to reduce the production cost of the ship.

- For instance, Samsung Heavy Industries Co. Ltd.’s Geoje Shipyard developed several robot systems, such as cleaning pipe robots, wall-climbing robots, spider automatic welding robots, vacuum blasting robots, and inspection robots. Since installing these robots, the Geoje Shipyard has recorded a 68% production automation rate.

The Digital shipyard market reflects a structural transformation in global shipbuilding and maintenance operations. Digital shipyards integrate advanced software platforms, automation technologies, and data-driven workflows across vessel design, construction, and lifecycle management. Adoption is accelerating as shipyards respond to cost pressure, rising vessel complexity, and skilled labor constraints.

The market growth is supported by sustained naval modernization programs and commercial fleet renewal. Defense authorities increasingly mandate digital continuity, model-based systems engineering, and secure data environments. These requirements elevate Digital shipyard platforms from productivity tools to mission-critical infrastructure within military shipyards.

Commercial shipyards account for the largest share of installations by volume. Their investment focus centers on throughput optimization, schedule reliability, and labor efficiency. Military shipyards contribute a smaller share of deployments but generate higher revenue per project due to system complexity, cybersecurity requirements, and multi-decade lifecycle support obligations.

Technology adoption is strongest across artificial intelligence and big data analytics, additive manufacturing, and robotic process automation. Artificial intelligence improves production planning accuracy, quality assurance, and resource utilization. Additive manufacturing reduces lead times for spare parts and tooling while lowering inventory risk. Robotic process automation streamlines documentation, engineering change management, and regulatory compliance.

North America and Europe lead in fully integrated Digital shipyard implementations. Asia-Pacific drives scale-based growth through smart shipyard investments in high-volume construction hubs. Emerging regions prioritize semi-digital shipyard models that deliver faster returns with lower capital exposure.

RESTRAINING FACTORS

High Working Capital for Hardware and Software May Hamper the Growth of the Market

The early stages of automating a manufacturing plant include procurement, accessories, programming, integration, and others. The huge capital expenditure at the beginning stage can be challenging for some businesses. The price of the industrial system, along with integration and maintenance costs, makes automation an expensive investment for small and medium-sized shipbuilders. Many small and medium-scale shipbuilders find it tough to gather huge funds due to the low production volume and sluggish return on investment.

Moreover, the software cost is also high, which is anticipated to restrain the digital shipyard market growth.

Segmentation Analysis

The Digital shipyard market is segmented by shipyard type, technology platform, and level of digitalization. Each segment reflects distinct investment priorities, adoption barriers, and value realization timelines. Understanding these differences is essential for accurately assessing demand patterns and competitive positioning.

By Shipyard Type Analysis

Commercial Segment to Dominate the Market Owing to Increasing Maritime Trade

Based on shipyard type, the market is segmented into commercial and military.

Commercial shipyards represent the largest share of Digital shipyard deployments by volume. These shipyards operate under intense cost, schedule, and margin pressure. Their primary objective is to maximize throughput while maintaining quality and delivery predictability.

The commercial segment is predicted to be the largest segment in 2025 and is expected to be the fastest-growing segment throughout the forecast period. The growth is attributed to the rise in seaborne trade worldwide. As stated by the United Nations Conference on Trade and Development (UNCTAD), around 80% of the global trade by volume is carried out by sea, which increases ship procurement, thus increasing the demand for digitalizing shipyards to speed up the manufacturing process.

Digital shipyard adoption in commercial facilities focuses on production planning, modular construction, and supply-chain coordination. Integrated design and manufacturing data reduces rework caused by late-stage design changes. Real-time visibility into production status improves schedule adherence across parallel block construction.

Large commercial shipyards prioritize scalable platforms that can be deployed across multiple yards or production lines. Labor productivity is a central use case. Digital work instructions, automated quality checks, and data-driven resource allocation reduce dependency on scarce skilled labor.

The military segment is expected to grow significantly during the forecast period due to rising government investment in developing and implementing digital twins in defense technologies. Military shipyards differ fundamentally in their Digital shipyard requirements. Program durations are longer, vessels are more complex, and compliance requirements are significantly higher. Digital shipyard investments are, therefore, more capital-intensive but generate higher contract values.

Defense shipyards emphasize configuration control, traceability, and lifecycle data continuity. Digital twins are central to these environments, supporting design validation, maintenance planning, and upgrade management over decades. Secure collaboration between shipyards, defense agencies, and suppliers is mandatory.

Unlike commercial yards, military shipyards are less sensitive to short-term return on investment. Adoption decisions are driven by strategic readiness, regulatory mandates, and long-term sustainment efficiency. Fully digital shipyard architectures are more common, particularly in government-owned or prime-contractor-operated facilities.

By Technology Platform Analysis

To know how our report can help streamline your business, Speak to Analyst

Robotic Process Automation Category to Dominate the Market Due To Increased Demand for Automation.

The market is divided into robotic process automation, additive manufacturing, artificial intelligence and big data analytics, digital twin, blockchain, industrial Internet of Things (IIOT), and other categories based on technology platforms.

Robotic process automation addresses administrative and engineering inefficiencies within shipyards. Common applications include document management, engineering change processing, compliance reporting, and data synchronization between legacy systems.

RPA is often an entry point for digital shipyard transformation due to its relatively low implementation cost and rapid payback. It enables shipyards to standardize workflows without extensive system replacement. However, RPA delivers incremental efficiency gains rather than structural transformation.

Due to the increased need for automation of many ship manufacturing processes, including welding, cutting, painting, and others, the robotic process automation segment is expected to dominate the market in 2020.

- For example, in 2018, a Ulsan-based shipyard claimed that it would automate the welding process, saving USD 9.4 million per year. The automation cut welding time in half and lowered the number of skilled workers by two-thirds.

- The Artificial Intelligence and Big Data Analytics segment is expected to hold a 28.22% share in 2025.

Due to the rising usage of artificial intelligence in robotic technology to automate the production process without human interference, the artificial intelligence segment is predicted to grow at a faster CAGR over the forecast period.

Additive manufacturing is gaining traction as qualification standards mature for maritime and defense applications. Shipyards deploy additive manufacturing for tooling, jigs, fixtures, and selected spare parts. This reduces lead times and minimizes reliance on external suppliers.

Integration with Digital shipyard platforms is critical. Design data, material specifications, and certification records must remain synchronized to ensure compliance and repeatability. As confidence grows, additive manufacturing expands from support functions to operational components.

While adoption remains selective, additive manufacturing is strategically important for maintenance, repair, and overhaul operations, particularly in remote or time-critical environments.

Artificial intelligence and big data analytics represent the fastest-growing technology segment within the Digital shipyard market. These tools convert large volumes of production, engineering, and operational data into actionable insights.

Key use cases include predictive production scheduling, defect detection, workforce optimization, and supply-chain risk analysis. Artificial intelligence enables shipyards to anticipate bottlenecks and quality issues before they escalate into delays or cost overruns.

Adoption requires high-quality data and organizational readiness. Shipyards with fragmented systems face integration challenges. As data architectures mature, artificial intelligence becomes a core decision-support capability rather than an experimental tool.

By Digitalization Level Analysis

Fully Digital Shipyard Segment to Record High CAGR Led by Increased Adoption of Advanced Technologies

The market is categorized into semi and fully digital shipyards based on their level of digitalization.

Semi-digital shipyards represent the largest share of facilities globally. These shipyards deploy digital tools within specific functions, such as design, planning, or quality management, while retaining manual or legacy processes elsewhere. This approach reflects capital constraints, risk aversion, and workforce readiness considerations. Semi-digital shipyards prioritize quick wins, focusing on areas with immediate productivity or compliance benefits.

While effective in the short term, fragmented digitalization limits data continuity and cross-functional optimization. As competitive pressure increases, many semi-digital shipyards transition toward more integrated models.

In 2020, the semi-digital shipyard segment is expected to be the largest. The dominance can be linked to shipbuilding businesses' growing awareness of the need to update their manufacturing processes. Due to the increased use of IIoT, augmented reality, digital twins, and other sophisticated technologies in marine vessel building, the fully digital shipyard is predicted to be the fastest-growing market over the projection period.

Fully digital shipyards operate integrated, data-centric environments spanning design, production, logistics, and lifecycle management. Digital twins, real-time analytics, and closed-loop feedback systems define this segment. These shipyards achieve higher productivity, improved quality consistency, and superior lifecycle transparency. However, implementation requires significant upfront investment, organizational change management, and cybersecurity capability.

Fully digital shipyards are most prevalent among large defense facilities and leading commercial builders with long-term capital planning horizons. Over the forecast period, this segment is expected to expand steadily as digital platforms mature and implementation risk declines.

Segmentation Outlook

Across all segments, the Digital shipyard market is moving toward deeper integration rather than broader experimentation. Shipyards increasingly favor platforms that support phased adoption while preserving a clear pathway to full digitalization.

The interaction between shipyard type, technology platform, and digital maturity ultimately determines adoption speed and value realization. Vendors and stakeholders that align solutions with these structural realities will capture the most durable growth.

REGIONAL ANALYSIS

Asia Pacific Digital Shipyard Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The global market is segmented by region into North America, Europe, Asia Pacific, the Middle East and Africa, and South America.

North America

The North American market is expected to grow due to increased research and development initiatives by key companies, such as Altair Engineering Inc. and others, to digitize shipyards. North America’s Digital shipyard market is driven by naval fleet modernization programs and complex commercial vessel construction. Shipyards invest in integrated digital platforms, cybersecurity frameworks, and lifecycle data management to meet operational and regulatory requirements. Labor cost pressure and program complexity reinforce the adoption of automation, digital twins, and analytics across large shipbuilding and maintenance facilities.

United States Digital Shipyard Market

The United States Digital Shipyard market is anchored in federal procurement standards and defense digitalization mandates. Naval shipyards deploy model-based systems engineering, secure digital twins, and lifecycle analytics to support fleet readiness. Commercial shipyards prioritize production visibility and schedule control. Vendor selection emphasizes interoperability, cybersecurity accreditation, and long-term sustainment capability.

Asia-Pacific

With a market size of USD 323.3 million in 2020, the Asia Pacific is expected to have the largest market share and grow at a faster compound annual growth rate during the projected period. Major shipbuilders like as Daewoo Shipbuilding, Marine Engineering, and China Shipbuilding Industry Corporation, among others, are responsible for the region's dominance in the digital shipbuilding sector. According to a published report, 90 percent of global cargo ships are produced in South Korea, Japan, and China. As a result, the existence of shipbuilding enterprises in the region aids in the digitalization of shipyards.

Asia-Pacific’s Digital shipyard market is underpinned by large-scale commercial shipbuilding activity and government-backed industrial development. Shipyards invest in automation, analytics, and modular construction to improve productivity and cost control. High production volumes and export competitiveness requirements accelerate digital deployment across major shipbuilding hubs.

Japan

Japan’s Digital shipyard market is driven by workforce demographics, quality assurance standards, and manufacturing reliability requirements. Shipyards apply digital platforms, robotics, and artificial intelligence to maintain production accuracy and process stability. Adoption strategies emphasize controlled implementation aligned with long-term operational efficiency.

China

China’s Digital shipyard market is supported by state-led industrial policy and extensive shipbuilding capacity. Investments focus on automation, analytics, and additive manufacturing to improve efficiency and reduce manual dependency. Digital shipyard adoption enables the delivery of complex commercial and naval vessel programs at scale.

Europe

The market in Europe is expected to develop significantly as European shipbuilders increase their investments in automated robotic technology for industrial operations. Europe’s Digital shipyard market reflects stringent regulatory frameworks, sustainability objectives, and advanced engineering requirements. Shipbuilders invest in interoperable digital platforms, energy-efficient production planning, and lifecycle data management. Public funding initiatives and cross-border collaboration programs support adoption across commercial and naval shipyards managing complex vessel designs.

Germany

Germany’s Digital shipyard market is defined by precision engineering practices and structured manufacturing processes. Shipyards deploy automation, production analytics, and digital quality management to support customized vessel construction. Investment priorities center on tight integration between engineering and manufacturing systems, enabling traceability, consistency, and export competitiveness.

United Kingdom

The United Kingdom Digital shipyard market develops around naval fleet renewal priorities and defense-industrial policy. Government-supported initiatives promote digital continuity, supplier integration, and lifecycle transparency. Commercial shipyards apply digital platforms to improve modular construction efficiency. Secure collaboration and long-term asset management guide technology investment.

Latin America

Latin America’s Digital shipyard market evolves in response to operational efficiency goals, budget constraints, and regional fleet requirements. Shipyards prioritize modular digital upgrades that deliver measurable productivity gains. Adoption strategies focus on targeted use cases rather than comprehensive platform transformation.

Middle East & Africa

The Middle East & Africa Digital shipyard market centers on maintenance, repair, and overhaul demand across commercial and defense fleets. Digital initiatives emphasize asset tracking, analytics-driven maintenance planning, and documentation automation. Investment priorities align with improving fleet availability and service efficiency.

Competitive Landscape

Market Players Are Using Strategies Such as Investment, Collaboration, Partnerships, and Others to Increase Their Market Potential

Companies have been concentrating on the automation of the manufacturing process over the last few years. Several companies are taking initiatives to adopt digitization in shipbuilding. There has been a rise in investments in the modernization of capabilities to increase efficiency and decrease costs. Players such as SAP and Accenture are collaborating to develop a new SAP cloud utility solution that will assist shipbuilding businesses in managing customer experiences and business processes efficiently. Market players are making R&D investments to design advanced robotic technology based on AI, IoT, and Augmented Reality (AR).

The Digital shipyard market features a mix of global industrial software providers, defense-focused technology firms, and specialized maritime solution vendors. Competition centers on platform breadth, maritime domain expertise, cybersecurity capability, and long-term support capacity rather than price alone.

Large multinational vendors provide end-to-end Digital shipyard platforms that integrate product lifecycle management, manufacturing execution, simulation, and analytics. These providers benefit from scale, global service networks, and established relationships with major shipbuilders and defense agencies. Their strategies emphasize platform interoperability, modular deployment, and alignment with defense compliance standards.

Defense-oriented technology firms occupy a strong position within military shipyards. These companies differentiate through secure architectures, accreditation experience, and lifecycle data governance. Long contract durations and sustainment services generate recurring revenue and high switching costs, reinforcing vendor entrenchment.

Niche players address specific functional gaps within Digital shipyard ecosystems. These include additive manufacturing workflow specialists, production analytics providers, robotics integrators, and digital quality management firms. Niche vendors often partner with larger platform providers, embedding specialized capabilities into broader shipyard deployments.

Strategic partnerships are a defining competitive feature. Shipbuilders increasingly prefer co-development models, where vendors tailor Digital shipyard solutions to specific production environments. Consulting and systems integration firms play a critical role, translating operational requirements into deployable digital architectures. Mergers and acquisitions remain targeted rather than expansive. Acquirers focus on analytics, artificial intelligence, cybersecurity, and cloud deployment expertise that strengthens platform differentiation. Competitive advantage increasingly depends on implementation success and measurable operational outcomes, not technology claims alone.

List of Top Digital Shipyard Companies:

- IFS AB (Sweden)

- Pemamek Oy (Finland)

- Dassault Systèmes (France)

- BAE Systems (U.K.)

- Altair Engineering, Inc. (U.S.)

- AVEVA Group Plc. (U.K.)

- Wartsila (Finland)

- KUKA AG (Germany)

- Damen Shipyards Group (Netherlands)

- Prostep AG (Germany)

KEY INDUSTRY DEVELOPMENTS:

- March 2024: Siemens expanded its Digital shipyard portfolio to integrate production planning, digital twin modeling, and lifecycle data management, supporting end-to-end data continuity across complex commercial and naval shipbuilding programs.

- July 2024: Dassault Systèmes entered a strategic collaboration with a European naval shipbuilder to deploy model-based systems engineering and secure digital collaboration, enabling configuration control and lifecycle traceability for next-generation defense vessels.

- November 2024: Hexagon enhanced its maritime analytics offering with artificial intelligence-driven inspection and production intelligence capabilities, targeting quality improvement and workforce optimization within high-complexity shipyard environments.

- February 2025: AVEVA introduced a cloud-enabled Digital shipyard solution designed to improve real-time production visibility, supplier coordination, and multi-site deployment flexibility for large commercial shipbuilders.

- June 2025: Accenture launched a defense-focused Digital shipyard framework combining cybersecurity architecture, analytics integration, and additive manufacturing advisory services to support naval shipyard digital transformation programs.

REPORT COVERAGE

The market research report provides a detailed analysis of the industry. It focuses on key aspects, such as key players, shipyard types, technology platforms, and the digitalization Level of digital shipyards. Moreover, the research report offers insights into digital shipyard market trends, competitive landscape, market competition, product pricing, market status, and highlights key industry developments. In addition to the major factors mentioned above, it encompasses several direct and indirect factors that have contributed to the sizing of the global market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Shipyard Type

By Technology Platform

By Digitalization Level

|

|

By Geography

|

|

Frequently Asked Questions

The global digital shipyard market size is valued at USD 4.93 billion in 2026, projected to reach USD 26.79 billion by 2034 at a CAGR of 23.56% during 2026–2034.

Registering a CAGR of 23.56%, the market will exhibit steady growth in the forecast period (2026-2034).

Growth is driven by Industry 4.0 adoption in shipbuilding, rising demand for automation and digital twins, increased use of IoT and AI for shipyard operations, and growing need for modernization of shipbuilding facilities to improve efficiency and reduce costs.

Asia Pacific dominated the market in 2025 with a 33.55% share, led by shipbuilding giants in China, South Korea, and Japan. High ship production volumes and rapid implementation of smart shipyard technologies fuel the region’s growth.

Major technologies include robotic process automation, additive manufacturing (3D printing), digital twins, artificial intelligence, big data analytics, and IIoT (Industrial Internet of Things), enabling real-time monitoring, predictive maintenance, and faster production cycles.

Semi-digital shipyards use partial automation and selective digital tools, while fully digital shipyards integrate end-to-end digital systems, including AI, AR/VR, digital twins, and robotics for complete lifecycle management of shipbuilding and maintenance.

The commercial shipyard segment dominates due to rising global maritime trade and increased demand for cargo ships, container vessels, and cruise ships. Military shipyards are also growing with investments in naval modernization and smart defense vessels.

Key trends include AI-powered smart shipyards, 3D metal printing for ship components, integration of blockchain for supply chain transparency, adoption of augmented reality for training and inspections, and rising demand for green and sustainable shipbuilding practices.

Prominent players include IFS AB, Dassault Systèmes, AVEVA Group, Wartsila, BAE Systems, Damen Shipyards Group, Pemamek Oy, and Altair Engineering, focusing on cloud-based shipyard platforms, robotics, and IoT-enabled solutions for shipbuilding digitalization.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us