Digital Transformation Consulting Services Market Size, Share & Industry Analysis, By Type (Strategy & Advisory Services, Technology Implementation Services, Data & Analytics Consulting, Process & Operations Transformation, Customer Experience (CX) Transformation, Cybersecurity & Risk Transformation, and Others), By Deployment Type (Cloud-Based, On-Premise, and Hybrid Deployment), By End Use Industry (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-commerce, IT & Telecom, Energy & Utilities, Government & Public Sector, Media, and Other), and Regional Forecast, 2026-2034

Digital Transformation Consulting Services Market Size and Future Outlook

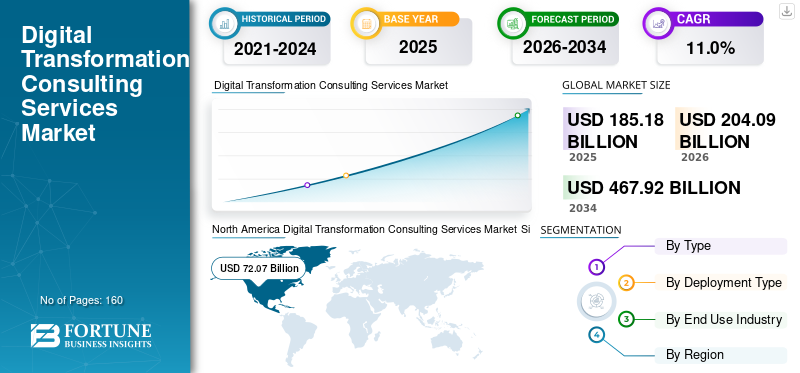

The global digital transformation consulting services market size was valued at USD 185.18 billion in 2025. The market is projected to grow from USD 204.09 billion in 2026 to USD 467.92 billion by 2034, exhibiting a CAGR of 11.0% during the forecast period. North America dominated the digital transformation consulting services market with a market share of 38.92% in 2025.

Artificial Intelligence and Gen AI models are being heavily integrated into the core functions of enterprises and organizations. Migration of legacy IT systems towards cloud-based ecosystems, growing data privacy regulations, and rising cybersecurity threats, all of which are driving the demand for digital transformation consulting services.

Adoption of Industry 4.0, smart manufacturing initiatives and digitization of the supply chains are a few of the key factors propelling the market share. Companies and enterprises are prioritizing customer experience through personalization and advanced analytics, along with critical transformation mandates on sustainability and ESG reporting. All such factors are driving the market demand for customer experience transformation services across the globe.

- For instance, in June 2024, Accenture acquired Parsionate, a Germany-based data consultancy firm, to strengthen its data transformation and SAP data migration capabilities across Europe, enhancing its digital transformation consulting portfolio in data strategy and enterprise modernization.

Key players in the market, such as Accenture, Deloitte, Capgemini, and IBM Consulting, are adopting several strategies, such as cloud-based digital consulting, integrated AI-based technology transformation, new innovative solutions, and strategic partnerships with domestic players. Several such factors have impacted the key players’ market share across geographies.

Tariffs imposed on consumer electronics, industrial machinery, and increased raw materials and hardware costs to boost the market growth during the forecast period. Increased demand for AI forecasting, supply chain analytics, and ERP modernization to drive the consulting services related to digital transformation.

Download Free sample to learn more about this report.

DIGITAL TRANSFORMATION CONSULTING SERVICES MARKET TRENDS

ESG-Driven Digital Transformation is Gaining Momentum in Market

Stringent regulatory and compliance policies, growing awareness about governance, are major factors driving the demand for the services. Sustainability has become a critical parameter embedded in enterprise-wide digital systems. Growing regulatory mandates are digitizing carbon tracing, emissions reporting, etc., which are further projected to drive the market growth. As sustainability becomes closely linked to brand reputation and operational efficiency, digital transformation programs are increasingly designed with ESG performance embedded from the outset, making sustainability-driven consulting a long-term growth avenue rather than a short-term compliance service.

- For example, in March 2024, Capgemini announced a partnership with Microsoft to integrate ESG into carbon accounting, and sustainability metrics.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Enterprise-Wide Data Modernization Mandates to Drive Market Growth

Digital transformation services are primarily growing due to rising investment in data architectures, advanced analytics ecosystems, and data platforms. Digital transformation consultants play a critical role in designing data strategies, ensuring data quality, implementing governance frameworks, and integrating enterprise systems. Additionally, the growing importance of Master Data Management (MDM), real-time dashboards, and predictive analytics is propelling the demand for consulting services at large scale. Regulatory requirements around data privacy and security further increase the complexity of modernization efforts. As a result, data modernization is no longer an IT upgrade but a strategic enterprise transformation initiative, creating sustained and high-value consulting opportunities.

- For instance, in February 2024, Deloitte expanded its alliance with Snowflake to help enterprises modernize legacy data infrastructures by implementing cloud-based data platforms and advanced analytics solutions.

MARKET RESTRAINTS

Data Privacy and Privacy Concerns to Limit the Market Growth

Highly regulated industries such as data centers, BFSI, healthcare, etc., produce huge amounts of critical data. As enterprises transfer data from legacy infrastructures to cloud-based platforms, the risk of cyber threats and unauthorized access increases. Highly sensitive and operational data to further limit the digital transformational consulting services market growth. Cross-border data transfers and transfer restrictions limit the digital transformation initiatives and programs.

MARKET OPPORTUNITIES

Vertical-Specific Digital Platforms Are Creating High-Value Growth Opportunities in Consulting

A digital platform developed to a specific industry presents a strong growth opportunity as enterprises increasingly demand transformation solutions over generic frameworks. Sectors such as banking, manufacturing, healthcare, and energy require customized digital ecosystems that integrate regulatory compliance, sector-specific analysis, and operational workflows. Consulting firms are developing pre-configured industry accelerators, digital twins, smart factory platforms, and vertical cloud solutions to shorten deployment cycles and enhance ROI. These specialized platforms not only improve differentiation but also create revenue through managed services and ongoing optimization.

MARKET CHALLENGES

Integration Complexity in Legacy System is Slowing Down the Services’ Adoption

Integration complexity with legacy systems remains one of the most significant challenges in digital transformation consulting engagements. Many enterprises rely on highly customized, decades-old ERP systems, mainframes, and on-premise infrastructure that were not designed to integrate with modern cloud-native, AI-driven, or API-based platforms. Migrating or integrating these systems often requires extensive reconfiguration, data cleansing, and middleware development, increasing project timelines and costs. Additionally, undocumented system dependencies and fragmented data architectures can create unforeseen technical risks during implementation. These complexities can lead to delays, budget overruns, and operational disruptions, ultimately impacting client’s confidence and consulting firms’ profit margins.

Segmentation Analysis

By Type

Technology Implementation Services Lead Due to Requirement by Enterprises for Large-Scale Execution Projects

Based on the type, the market is divided into strategy & advisory services, technology implementation services, data & analytics consulting, process & operations transformation, Customer Experience (CX) Transformation, cybersecurity & risk transformation, and others.

Technology implementation services account for the largest revenue share as enterprises require end-to-end execution support for cloud migration, ERP modernization, CRM deployment, AI system integration, and infrastructure transformation. These projects are typically large-scale, have multi-year engagements involving system integration, re-architecture, and deployment across business units. Since implementation is execution-heavy and resource-intensive, it generates higher billing volumes compared to advisory-only services.

Data & analytics consulting is the fastest-growing segment due to rapid enterprise AI adoption and the need for real-time, data-driven decision-making. Organizations are modernizing legacy data infrastructures, implementing data lakehouses, and integrating AI/ML models into core operations. Regulatory reporting, predictive analytics, and customer personalization initiatives are accelerating demand for data governance and analytics advisory services.

- For instance, in February 2024, Capgemini expanded its collaboration with SAP to accelerate large-scale S/4HANA cloud implementations, enabling enterprises to modernize legacy ERP systems, streamline business processes, and enhance cloud-based digital core transformation as part of broader technology implementation services.

By Deployment Type

Cloud-Based Consulting Dominates as Enterprises Accelerate the Implementation of Cloud-First Transformation Strategies

Based on deployment type, the market is segmented into cloud-based, on-premise, and hybrid deployment.

Cloud-based consulting dominates and leads in revenue share and growth due to widespread enterprise cloud migration and multi-cloud adoption strategies. Organizations are shifting from on-premise infrastructure to scalable, cost-efficient cloud ecosystems to enhance agility, innovation, and operational efficiency.

Cloud consulting includes migration planning, architecture redesign, cost optimization, security implementation, and SaaS integration. With increasing AI workloads and digital-native applications requiring cloud-native environments, this segment continues to dominate and expand at the fastest rate globally.

By End Use Industry

To know how our report can help streamline your business, Speak to Analyst

BFSI Sector Commands the Largest Share Driven by Regulatory Complexity and Continuous Digital Innovation

Based on end use industry, the market is segmented into BFSI, healthcare & life sciences, manufacturing, retail & e-commerce, IT & telecom, energy & utilities, government & public sector, media & entertainment, transportation & logistics, and others.

The BFSI sector holds the largest revenue share due to continuous digital innovation in banking, fintech, payments, and insurance. Financial institutions invest heavily in cybersecurity, fraud detection, AI-driven risk analytics, digital banking platforms, and regulatory compliance systems. Stringent regulatory requirements and intense competition from fintech startups further drive large-scale digital transformation programs. Given the sector’s high IT spending capacity and regulatory complexity, BFSI remains the leading contributor in consulting revenues.

Healthcare & life sciences is the fastest-growing vertical driven by telehealth expansion, digital health records modernization, AI-powered diagnostics, and clinical data analytics. The sector is undergoing rapid digitalization to improve patient outcomes, optimize hospital operations, and comply with evolving healthcare regulations.

Digital Transformation Consulting Services Market Regional Outlook

By geography, the market is studied across Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Digital Transformation Consulting Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the global digital transformation consulting services market share due to its highly mature enterprise IT ecosystem and strong presence of global consulting giants including Accenture, Deloitte, IBM, and others. The region benefits from early adoption of cloud computing, AI, and advanced analytics across industries, including BFSI, healthcare, and technology. High regulatory compliance requirements and cybersecurity investments further fuel consulting demand. Additionally, strong venture capital activities and digital-native business models drive continuous enterprise modernization.

U.S. Digital Transformation Consulting Services Market

The U.S. market is the largest globally, driven by high enterprise IT spending and rapid adoption of AI, cloud computing, and advanced analytics. Strong demand from BFSI, healthcare, retail, and technology sectors continue to fuel large-scale modernization programs. Regulatory compliance requirements and increasing cybersecurity threats further support consulting engagements. Additionally, the presence of leading global consulting firms and a mature ecosystem for innovation sustains the country’s dominance in terms of revenue.

Europe

Europe’s market growth is driven by Industry 4.0 adoption, particularly in Germany, Italy, and France, where manufacturing digitization remains a priority. Regulatory frameworks such as GDPR and ESG reporting mandates increase demand for compliance-focused digital consulting. The region is also experiencing a strong energy transition and sustainability-driven transformation initiatives. Public sector digitalization across EU nations further supports consulting engagements. Additionally, EU digital funding programs are accelerating enterprise modernization, especially in Eastern Europe.

U.K. Digital Transformation Consulting Services Market

The U.K. market, in 2026 will reach USD 10.14 billion, representing roughly 5.0% of global revenues.

Germany Digital Transformation Consulting Services Market

Germany’s market will reach USD 11.40 billion in 2026, equivalent to around 5.6% of the global sales.

Asia Pacific

Asia Pacific is the fastest-growing region due to rapid digital adoption across emerging economies such as India and ASEAN countries. Large-scale enterprise cloud migration, 5G deployment, and AI integration are accelerating transformation initiatives. Governments across China, India, and Southeast Asia are promoting digital economy programs and smart city development. Manufacturing-heavy economies are investing in automation and Industry 4.0 technologies. The region’s expanding SME base and growing fintech ecosystem further contribute to strong consulting demand.

India Digital Transformation Consulting Services Market

The Indian market, in 2026, will be valued at USD 8.25 billion, accounting for roughly 4.0% of the global market.

China Digital Transformation Consulting Services Market

China’s market is projected to remain dominant in the Asia Pacific in 2026 with revenue reaching USD 18.42 billion, representing roughly 9.0% of global sales.

ASEAN Digital Transformation Consulting Services Market

The ASEAN market in 2026 will reach a value of USD 6.88 billion, accounting for roughly 3.4% of revenue.

South America

South America’s market growth is supported by fintech expansion, particularly in Brazil and Mexico, where digital banking adoption is accelerating. Enterprises are increasingly migrating to cloud-based systems to improve operational efficiency and reduce costs. Manufacturing, retail, and telecom sectors are gradually adopting automation and digital platforms surging the demand for digital transformation consulting services. Economic volatility encourages organizations to pursue cost-optimization and automation consulting. Although growth is moderate compared to Asia Pacific, digital modernization initiatives are steadily expanding across the region.

Brazil Digital Transformation Consulting Services Market

The Brazil market will reach USD 5.85 billion in 2026, representing roughly 2.9% of the global market.

Middle East and Africa

The Middle East & Africa region is driven primarily by government-led digital transformation initiatives, particularly in GCC countries under programs such as Vision 2030. Smart city projects, energy diversification strategies, and public sector modernization are key growth enablers. Increasing cloud adoption and digital banking expansion also contribute to consulting demand. In Africa, fintech innovation and mobile banking ecosystems are supporting digital transformation initiatives. While the market base is smaller, strategic infrastructure projects are creating long-term opportunities.

GCC Digital Transformation Consulting Services Market

The GCC market will reach USD 4.66 billion in 2026, representing roughly 2.3% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

AI-Led Innovation and Strategic Partnerships Amongst Key Players Are Driving Competitive Differentiation

Key players in the digital transformation consulting services market are increasingly focusing on AI-led transformation strategies, integrating generative AI, automation, and advanced analytics into core service offerings. Many consultancy firms are pursuing aggressive mergers and acquisitions to strengthen capabilities in cloud, cybersecurity, data engineering, and industry-specific digital solutions. Strategic partnerships with hyperscalers such as AWS, Microsoft Azure, and Google Cloud are central to expanding cloud migration and multi-cloud consulting portfolios. Firms are also developing industry-specific accelerators and proprietary platforms to differentiate their offerings and shorten deployment cycles.

- For instance, in October 2023, IBM launched IBM Consulting Advantage, an AI-powered delivery platform designed to enhance digital transformation consulting engagements by integrating generative AI, automation tools, and industry-specific assets, enabling faster implementation cycles, improved productivity, and data-driven decision-making for enterprise clients.

LIST OF KEY DIGITAL TRANSFORMATION CONSULTING SERVICES MARKET COMPANIES PROFILED

- Accenture (Ireland)

- Deloitte (U.K.)

- IBM Consulting (U.S.)

- Capgemini (France)

- Tata Consultancy Services (India)

- Infosys (India)

- Cognizant (S.)

- PwC (U.K.)

- Ernst & Young (K.)

- Mckinsey & Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: EY announced the expansion of its Sustainability Digital Services platform, integrating ESG analytics, carbon tracking tools, and AI-powered reporting dashboards into enterprise transformation programs.

- July 2025: PwC launched a Digital Resilience & Cyber Transformation offering, focused on zero-trust architecture implementation and regulatory compliance modernization for global enterprises.

- February 2025: Deloitte announced the expansion of its Global Technology & Transformation practice, investing in AI-driven automation and cloud modernization capabilities to support enterprise-wide digital reinvention initiatives.

- January 2025: Accenture expanded its AI Refinery™ platform with industry-specific generative AI agents, enabling enterprises to accelerate large-scale AI deployment across finance, supply chain, and customer operations as part of end-to-end digital transformation programs.

- April 2024: Capgemini expanded its strategic partnership with Google Cloud, focusing on accelerating AI-driven cloud transformation and industry-specific digital modernization programs.

REPORT COVERAGE

The global digital transformation consulting services market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Deployment Type, End Use Industry, and Region |

| By Type |

|

| By Deployment Type |

|

| By End Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 185.18 billion in 2025 and is projected to reach USD 467.92 billion by 2034.

In 2025, the market value stood at USD 72.07 billion.

The market is expected to exhibit a CAGR of 11.0% during the forecast period.

By end use industry, BFSI sector dominates the market.

Enterprise-wide data modernization mandates to drive the market growth.

Accenture, TCS, Capgemini, and Deloitte are few of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us