Industrial Services Market Size, Share & Industry Analysis, By Services (Consulting & Engineering, Maintenance, Repair & Inspection, Installation, and Operational Improvement), By Provider Type (Original Equipment Manufacturers (OEM), Third Party Services, and In-House Teams), By Industry (Automotive & Mobility, IT & Networking, Manufacturing & Mining, Construction & Infrastructure, Energy & Power, and Others (Chemicals, etc.)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

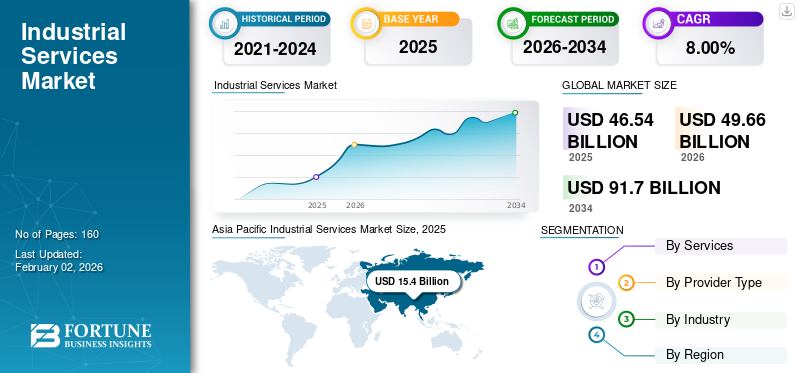

The global industrial services market size was valued at USD 46.54 billion in 2025 and is projected to grow from USD 49.66 billion in 2026 to USD 91.70 billion by 2034, exhibiting a CAGR of 8.00% during the forecast period. Asia Pacific dominated the global market with a share of 33.10% in 2025.

Industrial services solutions have swiftly transformed manufacturing, where sustainability and operational efficiency are the prime criteria for new-age technology. The market was primarily driven by the increasing demand for predictive maintenance and the usage of Artificial Intelligence (AI) and Machine Learning (ML) in manufacturing and production to increase Overall Equipment Efficiency (OEE). Furthermore, the growing trend of utilizing digital twin technology in Research and Development (R&D) and resource optimization showcases a major leap in the service industry.

Global industrial services companies such as ABB, Honeywell, and Siemens are keeping up with the changing trends by offering more flexible industrial solutions that extend the capabilities of the existing system. Furthermore, increased collaboration between companies and technology service providers increases the adoption of IoT, VR, and AI, which reduces environmental impact through advanced automation product portfolios.

Download Free sample to learn more about this report.

Industrial Services Market Key Takeaways

- 2025 Market Size: USD 46.54 billion

- 2026 Market Size: USD 49.66 billion

- 2034 Forecast Market Size: USD 91.70 billion

- CAGR: 8.00% from 2026–2034

- Asia Pacific dominated the industrial services market with a 33.10% share in 2025.

- The maintenance services segment held a 32.46% market share in 2026.

- The manufacturing & mining segment accounted for a 26.08% market share in 2026.

Asia Pacific

Asia Pacific generated USD 15.40 billion in 2025 and accounted for 33.10% of global market revenue.

Europe

Europe reached USD 12.11 billion in 2025, representing 26.00% of the global industrial services market.

North America

North America recorded USD 10.95 billion in 2025 and captured a 23.50% market share.

U.S.

The market is projected to reach USD 8.61 billion by 2026, supported by a strong manufacturing base and digital transformation initiatives.

Japan

The industrial services market is projected to reach USD 3.69 billion by 2026.

Read More

IMPACT OF TARIFFS

Adjustment in Supply Chain and Pricing Strategies Revaluation

Increased tariffs by the leading global and emerging economies raise costs for manufacturers and distributors. Companies may translate into higher import and purchase prices and are likely to squeeze margins in the short term. The tariffs in the market are less attractive, pushing existing companies to explore new markets for sourcing due to higher costs. The increasing cost further necessitates a re-evaluation of pricing strategies for both manufacturers and distributors.

- For instance, China imposed retaliatory tariffs on several goods, including industrial components and systems, after the U.S. increased tariffs to 104% in April 2025. The prime metals are expected to increase the additional cost for manufacturers by 25% to 30%.

MARKET DYNAMICS

Industrial Services Market Trends

Ascendancy of VR and Technological Advancements Shape Modern Trends

Modern manufacturing and the service industry have expanded mainstream product capabilities by offering remote collaboration for inspection and maintenance. The adoption of modern Industry 4.0 technologies in advanced manufacturing to optimize operation and maintenance has propelled innovation and increased user adoption. Businesses are focusing on the importance of VR in eliminating material wastage in production processes with optimal design. Augmented and virtual reality technologies are increasingly being adopted in manufacturing to enhance sustainability and process efficiency, driving the trend and the market size positively.

- For instance, in March 2025, Siemens and Audi revolutionized manufacturing processes with software-defined AI and automation solutions to scale production processes. The partnership is accelerating innovation in automotive by integrating virtual and hardware controls.

Download Free sample to learn more about this report.

Market Drivers

Focus on Automation and Digital Technology Drives Industrial Efficiency Demand

Original Equipment Manufacturers (OEM) and the in-house operations team are focusing on integrating automation and digital technologies for the analysis and deployment of greener solutions. Businesses are actively leveraging the benefits of predictive analysis and statistical methods for Overall Equipment Efficiency (OEE). Further, many OEMs are focusing on providing better services for the onshore worker with production-linked, which helps eliminate issues and improve productivity and industrial efficiency. These strategies drive the industrial services market size progressively during the forecast period.

- For instance, in recent years, ThyssenKrupp, an elevator manufacturer, announced that its technicians would be using Microsoft HoloLens technology to improve service operations. HoloLens enables service technicians to visualize and identify elevator problems. They also have remote access to technical and remote information.

Market Challenges

Shortage of Skilled Workforce and Limited Cash Flow Hinders Market Development

The market is growing positively. However, a shortage of skilled workforce to integrate modern automation equipment into traditional systems limits product adoption. Automation systems are technologically advanced systems that need a skilled workforce to eliminate the gap in technology adoption. Further, businesses observed limited cash flow owing to fewer investments in research and development and stringent international standards (ISO, IEC, OSHA). Local environmental and safety regulations complicate service delivery, especially for multinational providers, which pose complex challenges for the market.

Market Opportunities

Harvesting Opportunities Through Predictive Maintenance and Digital Twin Technology

Engineering and manufacturing companies are focusing on optimizing process lines by increasing focus on integrating a modern service portfolio to minimize downtime, optimize operational performance, and improve efficiency, further fueling the adoption of predictive maintenance. Industries prioritize upgradation, revolutionizing industrial services, and enabling real time data monitoring. Additionally, digital twin technology is the new age technology gaining attention from critical production and industrial services. This technology is crucial to predictive maintenance and operational efficiency, especially in inspection and monitoring. Thus, focus on the integration of modern service offerings, harvesting opportunities for the industrial services market growth.

- For instance, in June 2024, Regal Rexnord, a global leader in engineering and manufacturing components, launched a perceptive, intelligent, and reliable maintenance solution for condition monitoring and predictive maintenance in industrial engineering. The system is designed to build and evolve multiple legacy Regal Rexnord condition monitoring systems into a single unified architecture built with the world’s latest technologies.

SEGMENTATION ANALYSIS

By Services

Maintenance Segment Dominates Due to Its Widespread Utilization

Based on services, the market is divided into consulting & engineering, maintenance, repair & inspection, installation, and operational improvement.

The maintenance services segment is anticipated to hold a dominant market share of 32.46% in 2026, due to highest usage and share in the core automotive and manufacturing industries. Businesses are focusing on expanding maintenance service offerings and redefining operational efficiencies. Maintenance-as-a-Service (MaaS) is a new-age measure accepted by many small and medium-scale manufacturers to shift maintenance costs from traditional capital expenses to operational ones.

Repair and inspection service offerings grow with the increasing manufacturing and industrial sectors. The segment shows progressive growth owing to the rising demand for specialized emergency and scheduled repairs for specialized engineering and machinery. Other segments, including operational improvement, engineering consulting, and installation, significantly drive the service portfolio of companies across various industries.

By Provider Type

Growing In-house Teams and Focus on Upskilling Drive Segment Growth

Provider type segment has broadly been categorized into Original Equipment Manufacturers (OEM), third party services, and in-house teams.

In-house teams are the dominant segment owing to the adoption of advanced technologies such as IoT and preventive maintenance. These strategies help businesses upskill their existing in-house teams. Further, businesses are focusing on enhancing their business with more specialized maintenance, repair, and overhaul capabilities.

OEMs in prominent and developed markets are focusing on expanding their Annual Maintenance Service (AMS) offerings which are designed for consistent client relations, generating recurring revenue.

Third-party services segment is anticipated to hold a dominant market share of 39.47% in 2026. Markets are widespread, offering competitive service offerings that increase complexities for OEMs to operate at low margins.

By Industry

To know how our report can help streamline your business, Speak to Analyst

Expanding Focus on Process Optimization in Manufacturing and Mining Nurture Businesses

Industry segment is classified into automotive and mobility, IT and networking, manufacturing and mining, construction and infrastructure, energy and power, and others (IT and networking, etc.).

The manufacturing and mining segment dominates the industry segment is anticipated to hold a dominant market share of 26.08 in 2026, as manufacturing firms upgrade their existing facilities with modern machinery that is complex to operate and requires prior and skilled maintenance.

The construction and infrastructure segment is progressively growing as many developed and emerging markets are focusing on investing in financing projects. Also, the need for skilled and experienced engineering facilities for automotive and infrastructure complex projects is nurturing the industrial services sector. At the same time, other segments such as energy & power, IT & networking, and others are significantly pushing the segment growth.

INDUSTRIAL SERVICES MARKET REGIONAL OUTLOOK

Based on geography, the market is categorized into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

Asia Pacific

Asia Pacific Industrial Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 15.4 billion, contributing 33.10% to global market revenue, and is projected to grow to USD 16.56 billion in 2026, as the large and growing presence of manufacturing facilities primarily drives the market. Industrial facilities in this region are focusing on either upgrading the existing facility or automating the processes with AI and ML in maintenance and repair to drive optimization, minimize the risk of bottlenecks, and optimize the operation workflow. Countries in Asia Pacific, such as China, India, Japan, South Korea, and others, are significantly a part of emerging economies, focusing on attracting Foreign Direct Investments (FDI) for industrial expansion.

China is the largest market in the Asia Pacific region, and its prominent industrial base contributes major revenue to global manufacturing. The country is investing heavily in the Engineering Procurement Commissioning (EPC) projects to outsource a team of skilled workforce to handle complex mega engineering and industrial projects. The Japan market is projected to reach USD 3.69 billion by 2026, the China market is projected to reach USD 6.13 billion by 2026, and the India market is projected to reach USD 2.15 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

North America's market growth is driven by its progressive-led policies and groomed infrastructure. Today, manufacturing constitutes 12-13% of the region, with major manufacturing in the U.S. Demand for industrial services in the region is growing steadily, driven by the advanced service offerings extending applications of AI and VR to optimize the process. Additionally, the U.S. has an established manufacturing base, ongoing digital transformation, and the imperative for operational efficiency. The U.S. market is projected to reach USD 8.61 billion by 2026. The North America region captured 23.50% of the global market in 2025, generating USD 10.95 billion in revenue, and is projected to reach USD 11.67 billion in 2026.

Europe

Europe is the second-largest market, underpinned by the installed and active industrial base. The market is driven by the innovation and incorporation of modern AI and ML techniques and the pervasive adoption of Industry 4.0. The trend for the market is the use of modern and precision engineering in automotive and high-quality manufacturing, and the energy sector is supporting the progressive growth. The UK market is projected to reach USD 2.37 billion by 2026, and the Germany market is projected to reach USD 3.37 billion by 2026. Europe maintained a strong presence in the global market, reaching USD 12.11 billion in 2025, accounting for 26.00% share, and is expected to reach USD 12.93 billion in 2026.

South America

The South American market is shaped by the gradual acceleration of the region's manufacturing and infrastructure, supported by the growing investment in setting up processing facilities. In Brazil and Argentina, demand is particularly driven by the expanding mining and growing need for efficiency and renewable energy infrastructure. The South America market was valued at USD 3.56 billion in 2025, capturing 7.70% of global revenue, and is estimated to reach USD 3.73 billion in 2026.

Middle East and Africa

The MEA market is an emerging market. Traditional automation is in demand in the oil field, and capital investors are shifting their investments into infrastructure and EPC projects. South Africa, on the other hand, is attracting investments for major infrastructure projects, driving regional growth. Middle East & Africa recorded a market size of USD 4.53 billion in 2025, capturing 9.70% of the global market share, and is projected to reach USD 4.76 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leveraging AI Capabilities in Process Improvements Benefits Businesses

Companies in industrial services and OEMs are investing heavily in integrating automated AI tools and ML techniques to generate meaningful insights and improve process automation in industries. Machine learning systems in the modern industry services market promote system reliability and efficiency to refine the production process by minimizing repetitive errors and manual logging to accomplish desired results. Further, an AI system enables industrial companies to drive efficient product research, driving business growth.

- For instance, in April 2023, Siemens and Microsoft are harnessing the collaborative power of generative AI, which helps industrial companies drive innovation and efficiency across the operational lifecycle of products. To enhance collaboration, companies are collaborating with Siemens Teamcenter and Microsoft collaboration teams and language models in Azure.

List of Key Industrial Services Companies Profiled

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- GE Digital (General Electric) (U.S.)

- Schneider Electric SE (France)

- Rockwell Automation Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Hitachi, Ltd. (Japan)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Bosch Rexroth AG (Germany)

- Atlas Copco AB (Sweden)

- Eaton Corporation plc (Ireland)

- Pentair plc (U.S.)

- Ingersoll-Rand plc (U.S.)

- Integrated Power Service (U.S.)

- Bilfinger (Germany)

- Sisco (Saudi Arabia)

- L&T Technology Services

- ATS Advanced Technology Services, Inc.

- Metso (Finland)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Integrated Power Services (IPS), a prominent electrical, mechanical, and power management solution provider, conducted a joint exercise to display products and services with the greatest depth of mining expertise. It provides in-shop and field service with 24/7 emergency rapid response backed by professional engineers and expert availability across 97 locations in America.

- March 2025: ABB, a global technology leader, introduced ABB Ability, an industrial knowledge vault that uses generative AI to transform information sharing and retention. ABB experts, in collaboration with Microsoft, together two industry leaders to enhance productivity and efficiency.

- February 2025: ABB has signed a Memorandum of Understanding (MoU) with Bilfinger, a leading industrial service provider. Both companies will together deliver energy and process industries instrumentation and digital services, including work in energy transition contexts such as Hydrogen and CCUS plants.

- December 2024: Siemens and Tietoevry partnered to accelerate the digital transformation of the power utilities sector in Northern and Central Europe. The company will use Siemens ' GridScale X software in conjunction with its IT software.

- October 2024: Workhorse Group Inc. adopted the Siemens Xcelerator portfolio of industrial software, enabling companies to streamline supply chain and development team activities. The use case also accelerates the transition to zero-emission commercial vehicles.

REPORT COVERAGE

The industrial services report includes the services, provider type, and industry segment, a detailed analysis of the market, and focuses on key aspects such as leading companies, services, and applications. It also offers insights into market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.00% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Services

By Provider Type

By Industry

By Region

|

|

Companies Profiled in the Report |

ABB Ltd. (Switzerland), Siemens AG (Germany), GE Digital (General Electric) (U.S.), Schneider Electric SE (France), Rockwell Automation Inc. (U.S.), Mitsubishi Electric Corporation (Japan), Hitachi, Ltd. (Japan), Emerson Electric Co. (U.S.), Honeywell International Inc. (U.S.), Bosch Rexroth AG (Germany) |

Frequently Asked Questions

The market is projected to reach USD 91.70 billion by 2034.

In 2025, the market was valued at USD 46.54 billion.

The market is projected to grow at a CAGR of 8.00% during the forecast period.

The maintenance is the leading service in the market.

Focus on the working class and emerging economies drives market demand.

The top players in the market are ABB Ltd., Siemens AG, GE Digital (General Electric), Schneider Electric SE, Rockwell Automation Inc., Mitsubishi Electric Corporation, Hitachi, Ltd., Emerson Electric Co., Honeywell International Inc., and Bosch Rexroth AG.

Asia Pacific dominated the global market with a share of 33.10% in 2025.

The manufacturing & mining is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us