Distributed AI Infrastructure Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Deployment (Cloud, On-premises, Hybrid, and Edge), By Workload (Training, Inference, and Data Processing and Orchestration), By End-user (BFSI, Healthcare, Manufacturing, Automotive, Retail, Telecom, Government & Defense, and Others), and Regional Forecast, 2026 – 2034

DISTRIBUTED AI INFRASTRUCTURE MARKET SIZE AND FUTURE OUTLOOK

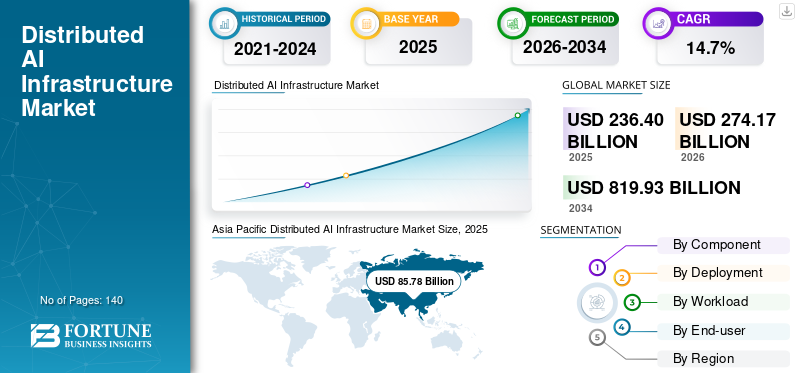

The global distributed AI infrastructure market size was valued at USD 236.40 billion in 2025. The market is projected to grow from USD 274.17 billion in 2026 to USD 819.93 billion by 2034, exhibiting a CAGR of 14.7% during the forecast period. Asia Pacific dominated the distributed ai infrastructure market with a market share of 27.82% in 2025.

The distributed AI infrastructure market refers to systems that enable agentic AI to operate across interconnected environments, forming broader AI ecosystems that span cloud, on- premises, and edge locations. These systems often function as part of a distributed AI hub, allowing seamless coordination of models, data, and computing resources. It includes hardware such as servers and GPUs, software for managing data and AI models, and services for deployment and support. These solutions help organizations process large volumes of data efficiently, support autonomous decision making, and enable real time insights. They are widely used across industries such as BFSI, healthcare, manufacturing, automotive, retail, telecom, government and defense, and others to improve efficiency, scalability, and automation.

NVIDIA Corporation, Microsoft Corporation, Amazon Web Services, Inc., Google LLC, Advanced Micro Devices, Inc., Intel Corporation, Dell Technologies Inc., Hewlett Packard Enterprise Company, Cisco Systems, Inc., and Lenovo Group Limited are the top players in the market.

Download Free sample to learn more about this report.

Distributed AI Infrastructure Market Key Takeaways

- 2025 Market Size: USD 236.40 billion

- 2026 Market Size: USD 274.17 billion

- 2034 Forecast Market Size: USD 819.93 billion

- CAGR: 14.7% from 2026–2034

- Asia Pacific dominated the market with a 27.82% share in 2025.

- Hardware accounted for the largest share (61.3%) by component in 2025.

- Cloud held the largest share (46.7%) by deployment in 2025.

North America

Held the second-largest market share, supported by hyperscalers, advanced data centers, and high AI adoption across industries.

Asia Pacific

The market reached USD 85.78 billion in 2025, driven by rapid AI infrastructure expansion and strong government support.

Europe

Held a significant market share, driven by enterprise AI adoption, data sovereignty initiatives, and industrial digital transformation.

U.S.

The market was valued at USD 71.72 billion in 2025.

Japan

The market was valued at USD 11.05 billion in 2025.

Read More

DISTRIBUTED AI INFRASTRUCTURE MARKET TRENDS

Shift Toward Edge and Distributed AI Driving Real-Time Processing Capabilities to be a Significant Market Trend

Enterprises are increasingly deploying AI infrastructure platforms closer to the point of data generation to enable faster processing and real-time decision-making across operations. This approach, often supported by AI cloud infrastructure and distributed AI networking, helps reduce latency, lower data transfer costs, and improve the efficiency of applications that cannot rely solely on centralized environments. It also supports better resource utilization and enhances performance in scenarios requiring immediate insights and continuous data processing. Adoption is gaining momentum across industries such as manufacturing, telecom, healthcare, retail, and automotive, driven by the need for automation, monitoring, predictive maintenance, and improved customer engagement through advanced AI infrastructure solutions.

- Gartner estimates that 75% of enterprise-generated data will be created and processed outside traditional centralized data centers or cloud environments by 2025, highlighting the growing shift toward distributed and edge-based AI infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Real-Time Processing and Low-Latency AI Applications to Drive Market Growth

Organizations are significantly increasing investments in AI training infrastructure and high-performance AI infrastructure to support advanced analytics, automation, and large-scale model development across industries. The growing complexity of AI workloads requires robust computing capabilities, including GPUs, accelerators, and scalable data processing systems, to ensure efficiency and reliability. Enterprises are expanding AI cloud infrastructure alongside on-premises and hybrid environments to manage rising data volumes and improve computational performance. This expansion is accelerating adoption across sectors such as BFSI, healthcare, manufacturing, and telecom, as organizations integrate AI into core business operations supported by comprehensive AI infrastructure services. In turn, driving the distributed AI infrastructure market growth.

- According to NVIDIA, data center revenue reached USD 115.2 billion in FY2025, reflecting strong demand for AI-driven computing infrastructure.

MARKET RESTRAINTS

High Infrastructure Costs and Energy Consumption Associated with AI Deployments to Challenge Market Growth

Organizations face significant upfront investments in building and scaling distributed AI environments, including high-performance AI infrastructure, advanced networking, and storage systems. The deployment of GPUs, accelerators, and AI training infrastructure requires substantial capital expenditure, making large-scale adoption difficult for small and medium enterprises. In addition, AI workloads demand high energy consumption, increasing operational costs, and raising concerns related to sustainability and power availability. These challenges intensify as enterprises expand AI cloud infrastructure and on-premises capabilities to support growing workloads, complex data flows, and distributed AI networking requirements.

- According to the International Energy Agency (IEA), data centers account for approximately 1% to 1.5% of global electricity consumption, highlighting the rising energy demands of computing infrastructure.

MARKET OPPORTUNITIES

Expansion of Edge Computing Infrastructure Creating Opportunities for DPU Adoption

The increasing penetration of artificial intelligence across emerging economies is creating new growth avenues for providers of AI infrastructure services and scalable AI infrastructure solutions. Rapid digital transformation, rising enterprise IT spending, and improving connectivity are enabling organizations to adopt AI-driven systems at scale. In addition, industries such as manufacturing, healthcare, retail, and logistics are expanding their use of AI for automation, analytics, and operational optimization. This broadening adoption base is encouraging vendors to develop flexible AI infrastructure platforms that integrate cloud, edge, and on-premises capabilities, thereby strengthening long-term market potential.

- According to IDC, global spending on AI is expected to exceed USD 500 billion by 2027, reflecting strong growth potential across industries and regions.

SEGMENTATION ANALYSIS

By Component

Hardware Segment Leads Owing to High Capital Investment in AI Infrastructure

Based on component, the market is divided into hardware, software, and services.

Hardware segment leads the market with a market share of 61.3% in 2025 due to the high capital intensity of AI infrastructure, driven by strong demand for GPUs, AI accelerators, servers, and networking equipment required for training and inference workloads. These components form the core foundation of distributed AI systems, resulting in significantly higher upfront spending, further supported by large-scale investments from hyperscalers and enterprises in data centers and high-performance computing infrastructure.

Services segment is expected to grow at the highest CAGR of 16.5% over the forecast period due to the increasing complexity of deploying and managing distributed AI environments across cloud, on-premises, and edge systems. Organizations are relying on consulting, integration, and managed services to address skill gaps and ensure efficient deployment, optimization, and scaling of AI infrastructure, especially as adoption expands across industries.

By Deployment

Cloud Segment Leads Due to Scalable and Flexible Infrastructure

Based on deployment, the market is divided into cloud, on-premises, hybrid, and edge.

Cloud segment held the largest share of 46.7% in 2025 due to its ability to provide scalable, flexible, and cost-efficient infrastructure for AI workloads, allowing organizations to deploy and manage models without heavy upfront investments in physical infrastructure. The strong presence of hyperscalers such as AWS, Microsoft Azure, and Google Cloud, along with their continuous investments in AI capabilities, further drives widespread cloud adoption across enterprises.

Edge segment is projected to grow at the highest CAGR of 17.0% over the forecast period due to the increasing demand for real-time data processing and low-latency applications across industries. As use cases such as autonomous systems, industrial automation, and smart devices expand, organizations are adopting edge deployments to process data closer to the source and improve performance.

By Workload

Training Segment Leads Due to High Compute Requirements

Based on workload, the market is segmented into training, inference, and data processing and orchestration.

Training segment held the maximum share of 40.6% in 2025 due to the high compute intensity required to build, fine-tune, and scale advanced AI models. These workloads require large volumes of data, powerful GPUs, accelerators, storage, and networking resources, resulting in higher infrastructure spending compared to other workload types.

Inference segment is expected to record the highest CAGR of 15.9% over the forecast period as enterprises increasingly deploy AI models into real-world applications after training is completed. Growing use of AI in automation, customer service, fraud detection, predictive maintenance, and edge applications is increasing the need for fast, continuous, and scalable inference infrastructure.

To know how our report can help streamline your business, Speak to Analyst

By End-User

Telecom Segment Leads Owing to High Network Data Volumes

By end-user, the market is segmented into BFSI, healthcare, manufacturing, automotive, retail, telecom, government & defense, and others.

In 2025, telecom segment held the largest share of 21.0% due to its strong reliance on distributed infrastructure, high data traffic, and growing use of AI for network optimization, predictive maintenance, customer analytics, and 5G-enabled services. Telecom operators also require large-scale cloud, edge, and data center investments to manage real-time network performance and support AI-driven connectivity services.

Automotive segment is expected to grow at the maximum CAGR of 17.8% over the forecast period due to the rising adoption of AI in autonomous driving, ADAS, connected vehicles, and smart manufacturing. The growing need for real-time processing, simulation, vehicle data analytics, and edge-based intelligence is increasing demand for distributed AI infrastructure across the automotive value chain.

Distributed AI Infrastructure Market Regional Outlook

By geography, the market is categorized into North America, South America, Asia Pacific, Europe, and the Middle East & Africa.

Asia Pacific

Asia Pacific Distributed AI Infrastructure Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market, with its value reaching USD 85.78 billion in 2025. The market is driven by the rapid expansion of AI infrastructure across major economies such as China, India, Japan, and South Korea. Strong government support, increasing cloud adoption, and rising investments in 5G and industrial automation are accelerating growth. The region’s large enterprise base and high demand across telecom, manufacturing, and automotive further strengthen its leading position.

Japan Distributed AI Infrastructure Market

The Japanese market was valued at around USD 11.05 billion in 2025, accounting for roughly 4.7% of global revenues.

China Distributed AI Infrastructure Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 37.32 billion, representing roughly 15.8% of global sales.

To know how our report can help streamline your business, Speak to Analyst

India Distributed AI Infrastructure Market

The Indian market was valued at around USD 12.19 billion in 2025, accounting for roughly 5.2% of global revenues.

North America

North America holds the second-largest share owing to the presence of major technology companies, hyperscalers, and advanced data center infrastructure. High adoption of AI across industries such as BFSI, healthcare, and telecom continues to drive demand. Continuous investments in innovation and high-performance computing further support market growth.

U.S. Distributed AI Infrastructure Market

The U.S. market was approximated at around USD 71.72 billion in 2025, accounting for roughly 30.3% of sales.

Europe

Europe holds a significant share due to increasing AI adoption across regulated industries such as BFSI, healthcare, and manufacturing. Strong focus on data protection, data sovereignty, and secure infrastructure is encouraging enterprise adoption. Industrial automation and digital transformation initiatives across the region also support growth.

U.K. Distributed AI Infrastructure Market

The U.K. market was valued at around USD 8.72 billion in 2025, representing roughly 3.7% of global revenues.

Germany Distributed AI Infrastructure Market

Germany’s market reached approximately USD 8.95 million in 2025, equivalent to around 3.8% of global sales.

Middle East & Africa

The Middle East & Africa is expected to grow at the second-highest CAGR due to rising investments in AI, cloud infrastructure, and smart city projects. Governments across GCC countries and other regions are actively promoting digital transformation and AI adoption. Expanding telecom networks and public sector initiatives are further accelerating demand.

GCC Distributed AI Infrastructure Market

The GCC market reached around USD 5.44 billion in 2025, representing roughly 2.3% of global revenues.

South America

South America is expected to grow at an average rate due to the gradual adoption of AI and the improvement of digital infrastructure. Brazil and Argentina are increasing investments in cloud and enterprise technologies. However, economic challenges and limited large-scale infrastructure may moderate the overall growth pace.

Brazil Distributed AI Infrastructure Market

The Brazil market was valued at around USD 4.51 billion in 2025, accounting for roughly 1.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Solutions to Strengthen Market Positioning

Players launch new solutions to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They also prioritize portfolio enhancement, strategic collaborations, and acquisitions and partnerships to strengthen their offerings. Such strategic launches enable technology companies to maintain and expand their distributed AI infrastructure market share in a rapidly evolving landscape.

LIST OF KEY DISTRIBUTED AI INFRASTRUCTURE COMPANIES PROFILED IN REPORT

- NVIDIA Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Google LLC (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Intel Corporation (U.S.)

- Dell Technologies Inc. (U.S.)

- Hewlett Packard Enterprise Company (U.S.)

- Cisco Systems, Inc. (U.S.)

- Lenovo Group Limited (China)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Amazon announced plans to commercialize its Trainium AI chips for external enterprise and cloud customers. This move expands its presence in the AI hardware market and increases competition in accelerator technologies globally.

- March 2026: NVIDIA, AWS, and Google Cloud expanded collaboration to develop scalable AI infrastructure for training, inference, and distributed workloads. This initiative strengthens cloud-based AI capabilities and supports enterprise-scale deployments across global markets.

- March 2026: Meta signed a multi-year agreement with Amazon Web Services for large-scale AI compute infrastructure support. The partnership supports growing AI workloads using custom chips and scalable cloud-based platforms efficiently.

- March 2026: NVIDIA partnered with global telecom operators to launch distributed AI grids across telecom networks globally. These solutions enable real-time inference by integrating AI infrastructure with edge and network environments efficiently.

- March 2026: Hewlett Packard Enterprise introduced AI grid solutions powered by NVIDIA for enterprise deployments globally. These offerings deliver low-latency distributed AI infrastructure for real-time applications across industries and business environments.

- March 2026: NVIDIA, AWS, and Google Cloud expanded collaboration to develop scalable AI infrastructure for training, inference, and distributed workloads. This initiative strengthens cloud-based AI capabilities and supports enterprise-scale deployments across global markets.

- February 2026: Google Cloud launched eighth-generation Tensor Processing Units to enhance AI computing performance and efficiency. The new chips support large-scale training and inference workloads with improved scalability across cloud-based environments.

REPORT COVERAGE

The global distributed AI infrastructure market analysis provides an in-depth study of the size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, key developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Deployment, By Workload, By End-user, and By Region |

| By Component |

|

| By Deployment |

|

| By Workload |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 236.40 billion in 2025 and is projected to reach USD 819.93 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 85.78 billion.

The market is expected to grow at a CAGR of 14.7% over the forecast period.

By workload, the training segment led the market.

Growing AI adoption, cloud and edge expansion, and rising investment in high-performance infrastructure are driving the market growth.

NVIDIA Corporation, Microsoft Corporation, and Amazon Web Services, Inc. are the top players in the market.

Asia Pacific held the largest market share in 2025.

Need for real-time processing, scalable cloud and edge systems, and improved AI performance is driving adoption.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us