Diver Detection Sonar (DDS) Market Size, Share & Industry Analysis, By Application (Commercial and Defense), By Solution (Hardware (Transmitter, Receiver, Control units, Displays, Sensors (Ultrasonic Diffuse Proximity Sensors, Ultrasonic Retro-Reflective Sensors, Ultrasonic Through-Beam Sensors, VME-ADC, and Others), and Others), Software, and Others), By End-user (Line Fit and Retro Fit), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

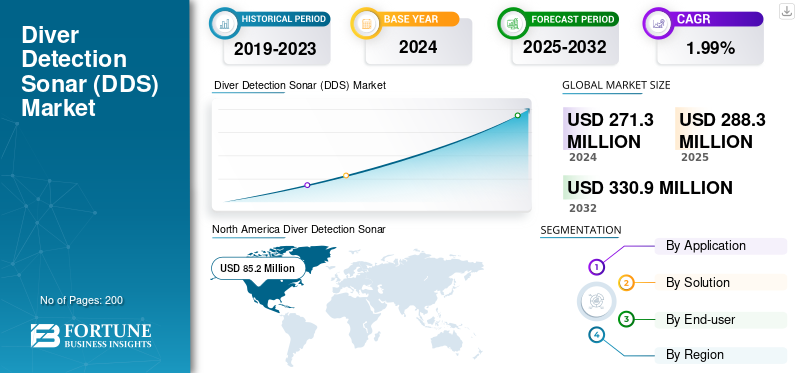

The global Diver Detection Sonar (DDS) market size was valued at USD 271.3 million in 2024. The market is projected to grow from USD 288.3 million in 2025 to USD 330.9 million by 2032, exhibiting a CAGR of 1.99% during the forecast period. North America dominated the global market with a share of 31.4% in 2024.

Diver Detection SONAR (DDS) are highly sensitive sonars used to detect, monitor, and track underwater penetrations such as divers, swimmer delivery vehicles (SDVs), and unmanned submersibles in real-time. Diffusions are identified by utilizing acoustic waves for guarding sensitive installations such as naval bases, ports, offshore oil platforms, and sea boundaries. High-frequency sonar (70-130 kHz) and AI processing are applied in more sophisticated DDS systems such as ATLAS ELEKTRONIK's Cerberus that provide 4.5 km² detection capability and less than 0.0001% false alarm. Transportable systems employing Defense Research and Development Organization, DRDO's PDDS-Portable Diver detection Sonar are used in shallow-water military defense, police security, commercial applications such as surveillance on underwater construction operations, and conservation. Generic, shipborne, and transportable sets are applied in specialized defense, energy, and marine services.

The DDS market expands with increasing maritime security threats in the form of terrorism, piracy, and submarine sabotage. Growing defense spending globally for underwater monitoring drives its adoption as fusion with AI reduces false alarms and improves detection rates. Small-form, low-power architectures and radar/LiDAR fusion technology are emerging as new technologies that improves portability and situational awareness. Commercial use increases with offshore energy operations that call for pipeline protection and ports/terminals guard with 24/7 intrusion detection needs. Major companies operating in the market, such as Thales Group, Lockheed Martin Corporation, and Raytheon Technologies are ensuring a substantial market growth in the forthcoming years. Particularly driven by the rise in military applications, technological advancements, and innovations to maintain a competitive edge over other players is a major driver of the major OEMs in the market.

Download Free sample to learn more about this report.

Diver Detection Sonar (DDS) Market Key Takeaways

- 2024 Market Size: USD 271.3 million

- 2025 Market Size: USD 288.3 million

- 2032 Forecast Market Size: USD 330.9 million

- CAGR: 1.99% from 2026–2034

- North America dominated the Diver Detection Sonar (DDS) market with a 31.4% share in 2024.

- The defense segment accounted for a dominating market share.

- The hardware segment accounted for the largest share of the market in 2024.

North America

North America dominates the global market with a major market share. Growing maritime security threats, massive defense spending, and the local critical infrastructure base drives the demand for the Diver Detection System (DDS) in North America.

Europe

Europe is the second-largest market for Diver Detection System (DDS). Europe's DDS market is opening up due to increased geopolitical tensions, naval fleet modernization, and strict regulations required for maritime security.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region with highest CAGR during the forecast period. Naval modernization, sea boundary disputes, and more sea trade are propelling strong growth in the DDS market across the Asia Pacific region.

U.S.

The market is supported by significant investments from defense and homeland security agencies in underwater surveillance systems to protect naval bases, ports, and offshore assets.

Japan

Growing maritime security requirements, naval modernization efforts, and investments in underwater monitoring technologies are driving DDS adoption across strategic coastal and offshore infrastructure.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Military Modernization Programs Contributes to Substantial Market Growth

The DDS market is expanding majorly due to the maritime threat of terrorism, underwater sabotage, and illegal assault on strategic targets, including naval bases, ports, and oil platforms. Governments and military sectors are major underwater monitoring spenders, and global military spending on the systems in 2023 was substantial.

Emerging technologies such as AI-driven analytics and high-definition sonar enhance detection rates, reduce false alarms, and enable real-time monitoring of divers and unmanned submersibles. For instance, AI applications sort sonar returns to distinguish threats from fish and trash so they can respond more quickly. Offshore oil and gas exploration and maritime commerce create a commercial motive for DDS implementation since DDS protects ports and pipelines from incursions.

Moreover, geopolitical competitions, particularly in regions including the Indian Ocean, require advanced systems to counter threats such as China's expansion at sea and piracy. DDS integration with unmanned underwater vehicles (UUVs) and hybrid sensor networks also drives the market growth as there is 24/7 surveillance and multi-domain threat detection. Additionally, the market is expected to grow due to modernization and the requirement for defense and protection of infrastructure.

MARKET RESTRAINTS

Environmental Issues and Technical-Operational Limitations to Limit Market Expansion

The market for DDS is confronted with several restraining factors that would be unfavorable for its operations and development. These may include natural aspects such as shallow and complicated underwater environments, such as harbors, ports, and shorelines that introduce enormous levels of ambient noise, reverberation, and acoustic clutter, thereby degrading the performance of sonar as well as improving the false alarm rate. Variation in the underwater environment, for example, temperature, salinity, and turbidity, further complicates effective detection and finding divers and small underwater threats.

Technical and operational limitations also restrain the Drive Detection Sonar (DDS) market growth. Active sonar systems, for all their capabilities, are delayed by their respective platforms; e.g., mobile platforms have limited range or endurance, and fixed sites are expensive and bulky to maintain. Besides this, sensitive detection equipment and sophisticated data processing requirements (usually on the basis of deep learning and AI) also contribute to growing expenses as well as human resource needs.

MARKET OPPORTUNITIES

Implementation AI, ML, AUVs, and Advanced Surveillance Systems Foster Sector Growth

Artificial Intelligence (AI) and Machine Learning (ML) in association with underwater monitoring are revolutionizing naval security and diver detection by processing vast volumes of sophisticated acoustic data in real-time. AI-based algorithms including deep neural networks classify genuine threats (divers or submarines) and noise with a much higher detection accuracy rate and low false alarms. This technology is unique as there is increasing demand for advanced underwater surveillance systems owing to increasing maritime security risks, critical infrastructure protection needs, as well as environmental surveillance demands.

Autonomous Underwater Vehicle (AUV) capability also enables such abilities through the operation of persistent wide-area surveillance within threat-risk or hostile terrain environments without endangering human operators. AI-driven AUVs with hybrid sensors and navigation are able to sweep autonomously along coastal boundaries, ports, and offshore platforms, with real-time situational awareness and warning about approaching threats. AI/ML and AUVs in combination are shattering the undersea surveillance barrier with more effective, scalable, and reliable systems to protect coastal and maritime assets.

Diver Detection Sonar (DDS) Market Trends

Growing Need for Advanced Maritime Security is a Major Growth Factor

The emerging trend driving the expansion of the Diver detection Sonar (DDS) market share is increasing demand for enhanced maritime security in light of escalating underwater and terror threats. With more international maritime activity and instances of illegal intrusion, governments and commercial owners are turning their sights to new-generation detection gear as a solution for their investments in securing critical infrastructure such as seaports, naval bases, and oil rigs offshore.

The incidence of underwater dangers such as marauding divers and submersible drones has brought into focus the need for robust sonar systems that can identify and eliminate dangers in real time with greater urgency. The trend is most visible in regions of high seaborne traffic and geopolitical significance, where security trade-offs can have disastrous consequences. As a result, next-generation DDS technology adoption is increasing with government regulatory mandates, defense modernization programs, and AI-based analytics integrations, further enhancing detection accuracy and performance and operational effectiveness.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

Growing International Security Threats Drive Defense Segment Growth

Based on application, the market is classified into commercial and defense.

The defense segment accounted for a dominating market share and is expected to grow at the highest CAGR in the forthcoming years. The defense sector has been driving DDS development due to growing international security threats, increasing military budgets, and the dynamic nature of submarine threats such as terrorism and sabotage. Militaries are spending higher amounts on new-generation sonar technologies to protect naval bases, submarines, and important coastal regions against stealthy underwater incursions. The convergence of AI, advanced signal processing, and multi-beam sonar technologies has greatly improved detection range and precision. DDS has now emerged as an indispensable part of contemporary naval defense strategy. In addition, the necessity to respond in a timely fashion to underwater threats and safeguard strategic infrastructure is driving ongoing innovation and adoption of DDS. With increasing geopolitical tensions and naval operations, defense officials are focusing on underwater monitoring, guaranteeing strong DDS adoption and development.

The commercial segment is expected to witness steady growth in the forecast period. The DDS business segment sector is evolving at a very fast pace with rising security needs at large infrastructures such as harbors, seafloor production platforms for oil and gas, and submarine pipelines. With the growth in global sea trade and offshore operations, there is a high demand for guarding valuable assets against unauthorized divers' intrusion, sabotage, and ecosystem attacks. Technological improvements, such as high-definition imaging, artificial intelligence-based detection, and real-time detection, have improved DDS efficiency and availability for use in businesses. Legal requirements and insurance are also creating demand through a need to reduce risk and meet safety regulations on behalf of business organizations. Multidisciplinary knowledge of DDS in security monitoring and environment, as well as diverse protection, enhances its utility across industries to discover market potential.

By Solution

Growing Need for Enhanced Security and Advancing Sonar Technology boosted Hardware Segment

Based on solution, the market is divided into hardware, software and others.

The hardware segment accounted for the largest share of the market in 2024 and is expected to grow at the highest CAGR in the forthcoming years. The need for enhanced security demands and advancing sonar technology drives hardware production of the Diver Detection System (DDS). The growing threats against submarine bases and naval facilities place a demand for high-capacity, hardy sonar equipment to locate divers in adverse conditions and at greater distances. Technologies such as high-quality transducers, multi-beam sonar arrays, and advanced signal processing units have made detection more accurate and operations more reliable. Naval, commercial, and environmental operators are keen to invest in these advanced hardware systems for port protection, oil rig protection, and naval facility protection. This interfacing with other observation vehicles and AUVs expands their scope of application.

Software will continue to account for a considerable share of the market. The need for smart, flexible, and intuitive detection solutions drives software development in the DDS market. Machine learning, advanced algorithms, and artificial intelligence are employed by contemporary DDS software to eliminate background noise, minimize false alarms, and process sonar data in real-time. Advanced software capabilities facilitate enhanced detection and identification of sea threats during challenging, noisy, or cluttered environments. Furthermore, modern software solutions provide seamless integration with command and control systems, remote monitoring, and automatic alerting, which enhance operations and decision-making by security personnel. With increasing underwater threats in the form of cyberattacks, investment in state-of-the-art software solutions is necessary to enable DDS deployment to be streamlined for effectiveness and efficiency, setting the market on a positive growth trajectory.

By End-user

Rising Demand for New Naval Ships boosted Growth of Line Fit Segment

Based on end-user, the market is divided into line fit and retrofit.

The line fit segment accounted for the largest share of the market in 2024 and is expected to grow at the highest CAGR in the forthcoming years. The growth of this segment is largely driven by rising demand for new naval ships and sea-going facilities with first-class underwater protection at the earliest opportunity. With rising risks from sea and threat of underwater sabotage, governments and business owners are turning their attention to DDS technology integration in maiden ship design, port, and offshore platform construction. This allows seamless system compatibility, reduces future retrofitting costs, and accommodates evolving security policy. Defense modernization and a focus on "future-proofing" assets also drive the trend, with line fit installations noticing a greater CAGR as new constructions feature complex and security-oriented designs.

Retrofit will continue to account for a considerable share of the market due to the vast fleet of ships and facilities present on the planet which must be updated in order to eliminate impending underwater dangers. Most fleets of navies and commerce are extending the lives of older platforms by retrofitting with available DDS technology, enhancing detection rates and deployability for less than the cost of new construction. The retrofit segment’s growth is supported by technologies that make integration with existing equipment simpler, with support for quick deployment and new security standard compliance. The alternative is particularly attractive to cost-sensitive governments and organizations with big fleets, generating steady demand for retrofit DDS solutions.

Diver Detection Sonar (DDS) Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Diver Detection Sonar (DDS) Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the global market with a major market share. Growing maritime security threats, massive defense spending, and the local critical infrastructure base drives the demand for the Diver Detection System (DDS) in North America. The U.S. alone is heavily investing in advanced underwater surveillance to defend naval bases, ports, and offshore assets against growing threats including terrorism and sabotage. In the U.S., the DDS market is growing rapidly with strategic investment by the Department of Defense and Homeland Security in underwater surveillance technology. With growing instances of underwater attacks and accidents on vital infrastructure, advanced sonar systems are utilized on a large scale. The growing demand for providing anti-intrusion capability on behalf of U.S. Commercial for protecting the Navy and offshore oil and gas platforms is another driving force.

Europe

Europe is the second-largest market for Diver Detection System (DDS). Europe's DDS market is opening up due to increased geopolitical tensions, naval fleet modernization, and strict regulations required for maritime security. The U.K., French, and German economies are purchasing sophisticated sonar technologies to secure ports, naval bases, and offshore facilities. The region is concentrating on AI and hybrid detection system integration in order to improve detection capability and operational efficiency.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region with highest CAGR during the forecast period. Naval modernization, sea boundary disputes, and more sea trade are propelling strong growth in the DDS market across the Asia Pacific region. China, India, Japan, and South Korea are giving underwater surveillance top priority to guard strategic maritime sea lanes and economic interests. With new ports, offshore energy installations, and coastal infrastructure, historic demand is growing in terms of expenditure for advanced diver detection solutions.

Rest of the World

The market in the rest of the world region is expected to witness considerable growth in the near future. The Middle East & Africa are experiencing growth in DDS markets as governments attempt to acquire major sea infrastructure such as ports, oil terminals, and desalination plants. Terrorism, piracy, and smuggling are still haunting the region, and thus governments are investing in underwater security systems. Latin American DDS market growth is being driven by the need to protect long coastlines, harbors, and offshore assets from illegal fishing, smuggling, and environmental assault. Brazil and others are investing in seafloor monitoring to protect vital infrastructure and enable expanded maritime trade. Environmental monitoring and enforcement of security rules are also a driving factor in the region's growing product adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Introduction of New Products by Key Companies Result in Their Dominating Position

The competition in the DDS market is fueled by high-speed technological advancement, cooperation and partnership, and simultaneous emphasis on business efficiency as well as ecologism. Sonardyne, Wavefront, NORBIT Security, HIROLAB, SAES, Armelsan, Westminster Group, KoçSavunma, ATLAS ELEKTRONIK, Forcys, Marine Electronics, and DSIT Solutions compete to develop sonar technology, particularly with 3D imaging and artificial intelligence to identify divers in real-time with high accuracy. Firms are also developing cleaner sonar systems to meet environmental and regulatory requirements, opening up market opportunities. Partnerships between research centers and the use of modular, scalable systems allow firms to meet varying end-user requirements in military, commercial, and environmental markets. Green R&D expenditures and intuitive interfaces are also differentiating market leaders, with global demand for advanced, adaptive underwater security on the rise.

LIST OF KEY DIVER DETECTION SYSTEM (DDS) COMPANIES PROFILED

- ASELSAN A.Ş. (Turkey)

- ATLAS ELEKTRONIK INDIA Pvt. Ltd. (India)

- DSIT Solutions Ltd. (Israel)

- EdgeTech (U.S.)

- FURUNO ELECTRIC CO., LTD. (Japan)

- Japan Radio Co. (Japan)

- KONGSBERG (Norway)

- Lockheed Martin Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- NAVICO (Norway)

- Raytheon Technologies Corporation (U.S.)

- SONARDYNE (U.K.)

- Teledyne Technologies Incorporated. (U.S.)

- Thales Group (France)

- Ultra (U.K.)

KEY INDUSTRY DEVELOPMENTS

- June 2024: The U.S. Naval force integrated machine learning (ML) models to support underwater target threat detection by unmanned underwater vehicles (UUV), however it needs a way to monitor and rapidly improve post-deployment performance to preserve the models' operational utility at scale. Earlier to this venture, systems depended on ML models that can be moderate, adjusted to changing conditions or enemy tactics.

- June 2024: NATO unveiled the study of Arctic Ocean SONAR properties with respect to the effects of warming on aquatic life. The Arctic Ocean is steadily transforming into a geopolitical and military theatre, and therefore, NATO took the initiative.

- June 2024: U.S. Naval force submarine warfare experts unveiled a contract to Science Application International Corp. (SAIC) in Reston, Va., to construct and repair components for the MK 48 heavyweight torpedo under terms of a USD 143.3 million order.

- April 2024: Authorities of the Naval Surface Warfare Center Crane Division in Crane, Ind., reported a USD 78.5 million contract for TR-343 connectorized sonar transducers for updates to Arleigh Burke-class destroyers and select Ticonderoga-class cruisers.

- March 2024: China unveiled the development of an advanced sonar system, which is compact and precise. The said technology can fit onto an unmanned submersible. A low-cost, technologically advanced system is expected to give China a maritime power edge over the U.S.'s unmanned smart weapons.

REPORT COVERAGE

The global Diver Detection Sonar (DDS) market analysis provides market size & forecast by all the segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on key regions/countries, key industry developments, new product launches, details on partnerships, mergers & acquisitions, and service providers in key countries. The report covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 1.99% from 2025-2032 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Solution

|

|

By End-user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 271.3 million in 2024 and is projected to reach USD 330.9 million by 2032.

In 2024, the market value stood at USD 85.2 million.

The market is expected to exhibit a CAGR of 1.99% during the forecast period of 2025-2032.

The defense segment led the market by application.

Military modernization programs is a crucial factor pushing the markets growth.

Major companies operating in the market include, Thales Group, Lockheed Martin Corporation, and Raytheon Technologies.

North America dominated the market in 2024 and holds majority of the market share.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us