Downstream Processing Market Size, Share & Industry Analysis, By Offering (Product {Instruments [Chromatography Systems, Filters & Filtration Systems, Centrifuges & Separation Systems, & Others], and Consumables}, & Services), By Technique (Separation, Filtration, Concentration, Viral Inactivation, Buffer Exchange, Purification, & Others), By Application (mAbs & Recombinant Proteins, Vaccines, Cell & Gene Therapies, Blood & Plasma Products, & Others), By End User (Pharmaceutical & Biotechnology Companies, CMOs/CDMOs, Academic & Research Institutes, & Others), and Regional Forecast, 2026-2034

Downstream Processing Market Size and Future Outlook

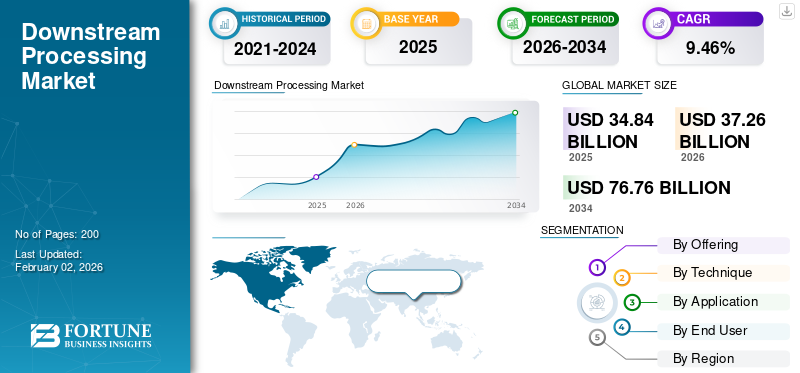

The global downstream processing market size was valued at USD 34.84 billion in 2025. The market is projected to grow from USD 37.26 billion in 2026 to USD 76.76 billion by 2034, exhibiting a CAGR of 9.46% during the forecast period. North America dominated the global downstream processing market with a market share of 42.16% in 2025.

The downstream processing market refers to all the technologies and systems utilized to purify and separate biological products after production. They transform crude biological mixtures into high-purity and therapeutically active biopharmaceutical products. The market is poised for significant growth during forecast years due to its irreplaceable need in biopharmaceutical manufacturing. The biopharmaceutical products are confronted with rigid standards of purity and safety. Advanced therapeutics such as viral vectors, cell therapies, and mRNA vaccines, among others, depend on these downstream processing technologies for quality assurance. These factors enable scalable production of next-generation treatments. With a rise in pharmaceutical manufacturing coupled with expanding manufacturing capacity, the market is poised for significant growth.

- For instance, in November 2025, AstraZeneca invested USD 2.0 billion to expand its manufacturing footprint in Maryland. The development includes the expansion of its biologics manufacturing facility in Frederick and a new facility in Gaithersburg for the development and clinical supply of innovative molecules to be used in clinical trials.

Additionally, the market is dominated by various key operating players, including Merck KGaA, METTLER TOLEDO, Thermo Fisher Scientific Inc., and Sartorius AG, which direct their resources toward strategic mergers and acquisitions and capacity expansion to strengthen their market position.

Download Free sample to learn more about this report.

Downstream Processing Market Key Takeaways

- 2025 Market Size: USD 34.84 billion

- 2026 Market Size: USD 37.26 billion

- 2034 Forecast Market Size: USD 76.76 billion

- CAGR: 9.46% from 2026–2034

- North America dominated the global downstream processing market with a 42.16% share in 2025.

- The services segment is expected to grow at a CAGR of 11.86% during the forecast period.

- The cell and gene therapy production segment is expected to grow at a CAGR of 12.18% during the forecast period.

North America

North America maintained its leading position in the market, reaching a valuation of USD 14.69 billion in 2025.

Europe

Europe is anticipated to grow at a CAGR of 9.10% and reach a market value of USD 9.94 billion by 2026.

Asia Pacific

Asia Pacific is projected to reach USD 8.73 billion by 2026, securing its position as the third-largest regional market.

U.S.

The U.S. downstream processing market is projected to reach a valuation of USD 14.10 billion.

Japan

Japan remains an important market in Asia Pacific, supported by ongoing investments in biopharmaceutical manufacturing and processing technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Exponential Growth of Biologics and Biosimilars Augments Market Demand and Drives Market Growth

The global rise in biologics and biosimilars development is directly accelerating the demand for downstream processing technologies. With the increasing production of biologics to cater to the rising disease burden, the global downstream processing market demand also increases in volume. Biologics and biosimilars undergo multiple filtration and purification steps to meet high-grade regulatory purity and safety requirements. With an increasing number of key companies expanding their manufacturing facility for biologics production, the demand for these downstream services and products also increases.

- For instance, in September 2025, Eli Lilly constructed a USD 6.5 billion manufacturing facility in Texas. The facility focuses on manufacturing the company's pipeline of small molecule medicines across therapeutic areas, including cardiometabolic health, oncology, immunology, and neuroscience. With such increasing production, the downstream purification processes also expand. Such factors are expected to boost the market's growth.

MARKET RESTRAINTS:

High Operational Costs of Advanced DSP Equipment and Consumables to Restrain Market Growth

The high cost of advanced downstream processing equipment and consumables remains one of the most significant restraints on the market. As the biologics grow more complex, the necessity of advanced downstream process increases. These innovative processes have a substantially high cost due to complex manufacturing processes and stringent quality standards. Such a high cost creates a financial and resource burden for biopharmaceutical manufacturers. These factors slow the expansion of and create hesitancy among biopharma manufacturers to invest in new systems that result in restraining the growth of the downstream processing market.

- For instance, in October 2025, 53Biologics reported scalability issues due to high resin costs and limited reusability in downstream processing.

MARKET OPPORTUNITIES:

Advances in Single-Use Technologies for Wider Availability of Innovative Solutions Offer Lucrative Growth Opportunities

Rapid advances in single-use downstream processing technologies are creating significant revenue opportunities for operating players. As biologics become more diverse, manufacturers are increasingly shifting from stainless-steel systems to flexible and lower-risk single-use systems. These benefits are critical for global downstream processing market growth. These single-use innovations provide various benefits over other traditional systems, such as pre-packed columns, single-use viral clearance modules, and automation assemblies, further expanding the market. These factors mitigate the concerns in regards with high-cost offering market growth. As manufacturing decentralizes and moves toward smaller, multi-product facilities, demand for single-use DSP components is expected to surge globally.

- For instance, in October 2021, Thermo Fisher Scientific Inc. launched the Thermo Scientific HyPeak chromatography system, the single-use chromatography system for bioprocessing services offered by the company, with key applications in therapeutic protein and vaccine development. Such development offers a market growth opportunity.

MARKET CHALLENGES:

Incompatibility of Certain Downstream Processing Steps with Continuous Bioprocessing Models

One of the principal challenges faced by key operating players in the company is the incompatibility of downstream processing steps with continuous bioprocessing models. The downstream processing steps, such as viral inactivation, centrifugation, precipitation, and final sterilizing filtration, require large buffer volumes that do not naturally integrate with a constant-flow continuous sequence. This results in manufacturers facing process interruptions and hybrid workflows where only certain steps are continuous while others remain batch-dependent. These factors create complexity, synchronization issues, and increased risk of bottlenecks ultimately limiting the full efficiency benefits promised by continuous manufacturing.

- For instance, in February 2025, Bioprocess International reported Eli Lilly and Company had embraced hybrid manufacturing, combining continuous and batch operations at its biologics facility in Limerick, Ireland.

DOWNSTREAM PROCESSING MARKET TRENDS:

Shift toward Continuous and Intensified Downstream Processing is a Prominent Market Trend Observed

One of the prominent global downstream processing market trends observed is a shift from traditional batch purification methods to continuous and intensified downstream processing. This shift allows high throughput and reduced processing times, significantly increasing the efficiency of these processes. As biologics portfolios expand and facilities move toward modular, flexible designs, continuous and intensified DSP is becoming one of the most prominent modernization trends in the industry.

- For instance, in May 2024, Sartorius AG collaborated with Sanofi to commercialize an end-to-end platform for downstream process intensification. The collaboration offered a modular platform to combine the highest flexibility with standardization that promotes lower resource consumption and higher productivity.

Download Free sample to learn more about this report.

Downstream Processing Market Segmentation Analysis

By Offering

Based on offering, the global downstream processing market is segmented into products and services.

To know how our report can help streamline your business, Speak to Analyst

Extensive Applications of Product to Drive Segmental Growth

In 2025, the product segment dominated the global downstream processing market. The dominance of the segment is attributed to the vast applications of these products in every step of downstream processing. Also, innovative product launches by key companies for applications, such as filters and resins, further strengthen the dominance of the segment. Such factors drive the growth of the market.

- For instance, in October 2024, Asahi Kasei Corporation launched the Planova FG1, a next-generation virus removal filter featuring higher flux for the manufacture of Biotherapeutics. These filters are used in the manufacturing process of bio therapeutic products such as biopharmaceuticals and plasma derivatives, biosafety testing services, and biopharmaceutical CDMO operations. Such development supports segmental growth.

On the other hand, the services segment is expected to grow at a CAGR of 11.86% during the forecast period.

By Technique

Expanding Application of Filtration for Various Biologics to Propel Segmental Growth

Based on technique, the market is classified into separation, filtration, concentration, viral inactivation, buffer exchange, and others.

Among these, the filtration segment accounted for the largest downstream processing market share in 2025. In 2026, the segment is projected to lead with a 35.0% share. The filtration segment dominates the market due to high utilization in multiple stages of the downstream process workflow. Also, the rapid innovation and commercialization of ultra-filtration, depth filtration, and a virus filtration provide target-specific filtrations to cater to the needs of pharmaceutical manufacturing. These factors have encouraged many key players to invest in new product launches, research and development, and drive the growth of the segment.

- For instance, in December 2023, TeraPore Technologies launched the IsoBlock VF product line for parvovirus removal from biopharmaceuticals and support simplified downstream processing.

The viral inactivation segment is anticipated to grow at a CAGR of 9.78% over the forecast period.

By Application

Widespread Usage of mAbs to Drive Segmental Growth

Based on application, the market is segmented into mAb and recombinant protein production, polishing & viral clearance, vaccine production, cell & gene therapy production, blood & plasma production, and others.

The mAbs & recombinant proteins production segment accounted for the major share of the market in 2025, based on application. In 2026, the segment is predicted to lead with a 38.4% share. These products require multiple chromatography and filtration steps, which results in higher utilization of the downstream process. As their demand increases, many key companies are focusing on their resources toward new product development for the segments to capitalize on demand, driving the growth of the segment.

- For instance, in February 2024, Purolite, an Ecolab company in collaboration with Repligen Corporation, launched Praesto CH1, an agarose-based affinity resin specialized for the purification of mAbs. Such advancement in purification technology for mAb supports the segmental growth.

The cell and gene therapy production segment is expected to grow at a CAGR of 12.18% over the forecast period.

By End User

Increasing Bioprocessing Activities to Drive Segmental Growth

In terms of end-user, the market is categorized into pharmaceutical & biotechnology companies, CMOS/CDMOS, academic & research institutes, and others.

The pharmaceutical and biotechnology companies segment dominated the market based on end user in 2025. In 2026, the segment is expected to lead with a 47.5% share. These companies are primary manufacturers of biologics and utilize various downstream processes. They invest heavily in these processes to support internal production and process intensification projects. Such factors reinforce the dominance of the segment. Also, with the expansion of manufacturing capacities by key players, the demand for downstream processing also increases at a larger scale, driving growth in the segment.

- For instance, in August 2024, WuXi Biologics inaugurated four manufacturing facilities and the Suzhou Biosafety Testing Center in China, and received Good Manufacturing Practice (GMP) certificates from the European Medicines Agency (EMA).

The CMOs/CDMOs segment is estimated to grow at a CAGR of 11.11% over the global downstream processing market projected period.

Downstream Processing Market Regional Outlook

By geography, the market is segmented into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

NORTH AMERICA

North America held the leading share in 2024, estimating at USD 13.79 billion, and also maintained the leading share in 2025, with USD 14.69 billion. The region is dominated due to a robust biopharmaceutical manufacturing ecosystem and the rapid expansion of CDMOs and CMOs. Also, large investment by key companies expanding their manufacturing capabilities consequently promotes market growth. In 2026, the U.S. market is projected to reach USD 14.10 billion. In the U.S., strategic activities by key companies such as mergers and acquisitions to expand their product offering in the market are drive market growth and supporting the country’s dominance in the region.

- For instance, in September 2025, Thermo Fisher Scientific Inc. acquired the Purification & Filtration business of Solventum. The development strengthened the company’s bio production offerings with advanced filtration technologies that improve quality and efficiency across upstream and downstream workflows. Such developments boost the market growth.

EUROPE and ASIA PACIFIC

Regions including Europe and the Asia Pacific, are expected to experience notable growth in the coming years. During the projected period, the European region is anticipated to record a growth rate of 9.10%, the second-highest among all regions, and reach a valuation of USD 9.94 billion by 2026. The growth in Europe is attributed to the high manufacturing capabilities of vaccines and other biologics. Such high manufacturing capacity further boosts the demand for downstream processing. Supported by these elements, nations including the U.K. anticipates to record the valuation of USD 2.14 billion, Germany to record USD 1.55 billion, and France to record USD 1.37 billion in 2026. After Europe, the market in Asia Pacific is projected to reach USD 8.73 billion in 2026 and secure the position of the third-largest region in the market. In areas, India and China are both estimated to reach USD 1.60 billion and USD 1.55 billion each in 2026.

LATIN AMERICA and MIDDLE EAST & AFRICA

During the projected period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space. The Latin America market in 2026 is set to reach a valuation of USD 1.69 billion. The growth in this region is supported by increasing government and private sector initiatives aimed at improving biologics self-sufficiency. In the Middle East & Africa, the GCC is set to reach a value of USD 0.49 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations and Acquisitions by Key Players Maintained their Top Position

The global downstream processing market exhibits a semi-consolidated structure, with a few businesses actively operating globally. These players are actively involved in numerous strategic activities such as capacity expansion, innovative product launches, and strategic acquisitions. They actively invest in technology advancement and offer a wide array of product offerings for innovative computer vision systems.

Merck KGaA, Cytiva, Thermo Fisher Scientific Inc., Waters Corporation, and METTLER TOLEDO are some of the significant players in the market. These companies offer a wide range of systems for the various stages of downstream processing to improve efficiency. They participate in strategic acquisitions to strengthen market positions.

- For instance, in October 2025, Merck KGaA acquired the chromatography business of JSR Life Sciences. The acquisition expanded the company’s downstream processing portfolio with advanced Protein A chromatography capabilities, supporting more efficient and scalable production of biopharmaceutical therapies, including monoclonal antibodies.

Other notable players in the market include ALFA LAVAL, PHYTON LTD, Sartorius AG, Repligen Corporation, and others. These businesses are undertaking various strategic initiatives, such as investments to expand their product offering.

LIST OF KEY DOWNSTREAM PROCESSING COMPANIES PROFILED:

- Sartorius AG (Germany)

- Repligen Corporation (U.S.)

- Merck KGaA (Germany)

- Danaher (U.S.)

- METTLER TOLEDO. (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- Waters Corporation

- ALFA LAVAL (Sweden)

- PHYTON LTD (Canada)

- WuXi Biologics (China)

KEY INDUSTRY DEVELOPMENTS:

- January 2025: Bio-Rad Laboratories, Inc. launched Nuvia wPrime 2A Media, a weak anion exchange and hydrophobic interaction (AEX-HIC) mixed-mode chromatography resin for small- to large-scale biomolecule purification used in downstream processing.

- November 2025: Enquyst Technologies showcased first-in-class, chromatography-free downstream processing of a monoclonal antibody (mab) with its patented isoelectric point purification (IPP) technology platform.

- December 2024: Repligen Corporation launched AVIPure dsRNA Clear OPUS columns, a chromatography solution designed to enhance the production and simplify purification of mRNA therapeutics and vaccines.

- September 2024: Sartorius AG launched Vivaflow Tangential Flow Filtration (TFF) Cassettes, aimed to streamline tangential flow filtration (TFF) in the laboratory downstream processes.

- November 2022: Alfa Laval launched a new membrane filtration. A new cross-flow skid-mounted membrane filtration system connects both up and upstream and downstream operations to increase flexibility across a range of process applications.

REPORT COVERAGE

The global downstream processing market analysis provides a detailed study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers & acquisitions, and strategic insights into market growth. The global downstream processing market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.46% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Technique, Application, End User, and Region |

| By Offering |

|

| By Technique |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 34.84 billion in 2025 and is projected to reach USD 76.76 billion by 2034.

In 2025, the market value stood at USD 14.69 billion.

The market is expected to exhibit a CAGR of 9.46% during the forecast period of 2026-2034.

The product segment is expected to lead the market in terms of offering.

The increasing biopharmaceutical production to increasing the demand and driving market growth.

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc., and Repligen Corporation are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us