Drone Detection Market Size, Share & Industry Analysis, By Platform (Ground-based and Handheld), By Technology (Radar Systems, RF Detection, Optical Systems, Acoustic Systems, and Others), By Range (Short Range (Up to 1 Km), Medium Range (1 Km to 5 Km), and Long Range (Above 5 Km)), By End Use (Military & Defense, Commercial, Government, and Others), and Regional Forecast, 2026-2034

Drone Detection Market Size and Future Outlook

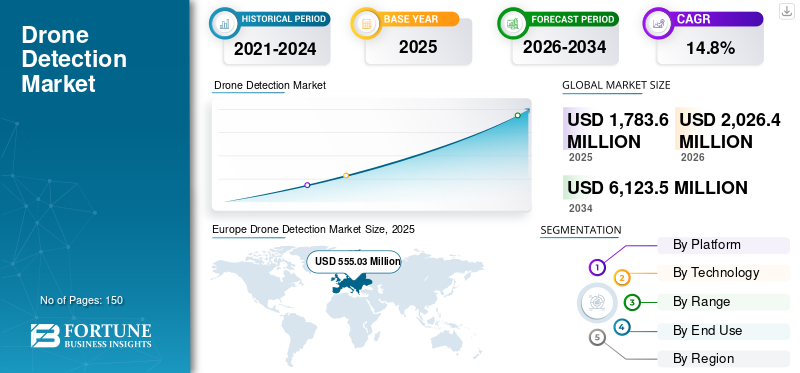

The global drone detection market size was valued at USD 1,783.6 million in 2025. The market is projected to grow from USD 2,026.4 million in 2026 to USD 6,123.5 million by 2034, exhibiting a CAGR of 14.8% during the forecast period. Europe dominated the global drone detection market with a market share of 31.12% in 2025.

Drone detection is the process of identifying, locating, and tracking Unmanned Aircraft Systems (UAS) commonly called drones within a defined airspace so that operators can assess risk and respond appropriately. Drone detection typically relies on one or more sensing methods. RF (radio-frequency) detection scans for control links and telemetry to spot drones and sometimes the pilot location. Radar detects and tracks flying objects, including small drones, in various weather and lighting conditions. Electro-optical/infrared (EO/IR) cameras provide visual confirmation and classification, while acoustic sensors listen for drone motor signatures in quieter environments. Modern systems increasingly combine these inputs through sensor fusion and AI analytics to reduce false alarms and improve confidence.

Key players include Airbus SE (Netherlands), Dedrone (U.S.), DroneShield Group Pty Ltd (Australia), Leonardo S.p.A. (Italy), Lockheed Martin Corporation (U.S.), Raytheon Company (U.S.) and others. Airbus Defence and Space develops counter-UAV systems including LUNA, integrating radar, EO/IR sensors, and jammers for drone detection up to 10km, focusing on military and perimeter security with low false positives. Dedrone provides Dedrone Defender 2, an AI-powered counter-drone platform using RF, radar, cameras, and ML for real-time detection, tracking, and mitigation, deployed at airports and stadiums globally.

Download Free sample to learn more about this report.

Drone Detection MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1,783.6 million

- 2026 Market Size: USD 2,026.4 million

- 2034 Forecast Market Size: USD 6,123.5 million

- CAGR: 14.8% from 2026–2034

- Europe dominated the drone detection market with a 31.12% share in 2025.

- The ground-based segment held the largest share due to demand for 24/7 fixed-site surveillance.

- The long range (above 5 km) segment accounted for 19.64% of the market share in 2025.

North American

North America reached USD 582.3 million in 2026, supported by defense modernization and strong C-UAS investments.

Europe

Europe led the market with USD 555.0 million in 2025, driven by critical infrastructure protection and strict airspace regulations.

Asia Pacific

Asia Pacific is expanding rapidly, reaching USD 622.1 million in 2026, driven by urban security and border monitoring needs.

U.S.

Estimated at USD 502.7 million in 2026, driven by homeland security, military bases, and airport protection demand.

Japan

Market reached USD 92.5 million in 2026, supported by strict safety requirements for airports and public infrastructure.

Read More

DRONE DETECTION MARKET TRENDS

AI Integration and Multi-Sensor Fusion to be a Latest Trend in Market

A prominent trend is the shift toward multi-layered detection combining radar, RF, acoustic, optical, and AI/ML for enhanced accuracy, reduced false positives, and broader coverage in diverse settings. Advancements in sensor fusion, cloud monitoring, and ground-based systems enable automated threat assessment and countermeasures such as jamming. Innovation focuses on modular, mobile solutions for urban and remote areas, with R&D emphasizing precision and interoperability amid rising counter-UAV needs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Drone Threats around High-Value Assets are Driving Market Growth

The drone detection market growth is propelled by rising unauthorized drone activities, including smuggling, surveillance, and terrorism threats near critical infrastructure including airports and military bases. Heightened geopolitical tensions and regional conflicts further boost demand, alongside increasing commercial UAV adoption in sectors including logistics and agriculture. Governments, especially in North America, are ramping up homeland security budgets and FAA regulations, fostering investments in advanced counter-drone technologies integrated with AI and IoT for real-time threat mitigation.

MARKET RESTRAINTS

High Costs and Regulatory Hurdles to Limit Market Growth

Key restraints include elevated initial deployment and operational expenses for sophisticated radar, RF, and sensor systems, limiting adoption by smaller entities and cost-sensitive regions. Evolving regulatory frameworks on airspace, RF usage, privacy, and signal interception create compliance challenges, approval delays, and operational uncertainties across regions. Frequent policy shifts raise costs for manufacturers, while input inflation for sensors adds margin pressure, slowing global market penetration despite strong demand in defense sectors.

MARKET OPPORTUNITIES

Emerging Markets and Tech Advancements to Create Lucrative Opportunities in Market

Lucrative opportunities arise from Asia Pacific, Middle East & Africa, where drone proliferation drives demand for airport, infrastructure, and public safety protections. Rising defense budgets, AI/IoT expansions, and hybrid systems offer growth, particularly in North America and Latin America via regulatory support and counter-UAS innovations. Strategic partnerships, certifications, and affordable tech developments enable vendors to scale.

MARKET CHALLENGES

Technological and Cybersecurity Limitations to Challenge Market Growth

Detection systems face accuracy issues from sensor limitations such as limited range, unreliable connectivity, environmental interference, and false alarms in complex urban or cluttered environments. Cybersecurity risks in IoT-connected platforms, including hacking, jamming, and data manipulation, threaten system integrity. Rapid drone tech evolution, such as frequency-hopping and encryption, demands constant adaptation, compounded by skilled talent shortages for deployment and maintenance.

Segmentation Analysis

By Platform

Persistent 24/7 Protection for Fixed and High-Value Sites Led to Ground-Based Segment Dominance

Based on platform, the market is segmented into ground-based and handheld.

The ground-based segment is anticipated to account for the largest drone detection market share. Demand remains strongest as fixed sites bases, airports, borders, power plants need persistent 24/7 coverage. Buyers prefer scalable networks with centralized C2, multi-sensor fusion, and upgrades that extend detection envelopes over time.

The handheld segment is anticipated to rise with a CAGR of 16.0% over the forecast period.

By Technology

Radar Systems Technology Necessary for All-weather Detection Led to its Dominance

Based on technology, the market is segmented into radar systems, RF detection, optical systems, acoustic systems, and others.

In 2025, the radar systems segment dominated the global market. Demand is rising where reliable all-weather detection is mandatory, especially against low-RCS drones and swarms. Radar is increasingly bought as part of fused stacks with RF and EO/IR to cut false alarms.

The optical systems segment is projected to grow at a CAGR of 16.1% over the forecast period.

By Range

Medium Range (1–5 Km) Detection Segment to Dominate Due to Best-Fit Coverage for Perimeter Security and Events

Based on range, the market is segmented into short range (up to 1 km), medium range (1 km to 5 km), and long range (above 5 km).

The medium range (1 Km to 5 Km) segment is anticipated to witness a dominating market share over the forecast period. Demand is high as 1–5 km coverage matches most perimeter-security and event-protection needs without long-range cost and complexity. It fits airports, prisons, ports, and industrial campuses needing early warning and cueing.

The long range (above 5 Km) segment is projected to grow at a high CAGR of 15.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End Use

Due to Operational Force Protection and Integrated C-UAS Readiness, Military & Defense Segment is Dominant

Based on end use, the market is segmented into military & defense, commercial, government, and others.

The military & defense segment dominated the segmental market share. Demand is driven by operational threats at forward bases, airfields, convoys, and ammunition depots. Militaries prioritize integrated C-UAS layers, rapid deployability, electronic resilience, and sustainment support for high-tempo environments.

In addition, commercial segment is projected to grow at a CAGR of 15.7% during the study period.

Drone Detection Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Europe

Europe Drone Detection Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2024, valuing at USD 476.5 million, and also maintained the leading share in 2025, with USD 555.0 million. Demand is shaped by elevated security posture, protection of critical infrastructure, and evolving airspace rules. Buyers prefer integrated, networked systems with identification, tracking, and compliance features for civil and defense sites.

U.K. Drone Detection Market

The U.K. market growth in 2026 is estimated at around USD 99.7 million, representing roughly 14.6% CAGR during the forecast period. Demand centers on airports, government facilities, and major events. Buyers prioritize detection-first solutions due to legal constraints on mitigation, pushing investment into RF, radar, and analytics tied to incident response workflows.

Germany Drone Detection Market

Germany’s market is projected to reach approximately USD 122.7 million in 2026. Demand is driven by critical infrastructure protection, industrial sites, and airports. Procurement favors high-reliability systems with strong integration and data governance, plus layered sensing to reduce false alarms in dense electromagnetic environments.

North America

North America is estimated to reach USD 582.3 million in 2026 and secure the position of second largest region in the market. Demand is driven by base protection, border security, airports, and large public events. Strong budgets and active trials accelerate multi-sensor deployments, especially RF and radar, with software fusion and recurring sustainment.

U.S. Drone Detection Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 502.7 million in 2026, accounting for roughly 14.1% CAGR during the projected period. Demand is fueled by homeland security, military bases, airports, and stadium protection. Procurement emphasizes integrated C-UAS architectures, sensor fusion, and networked command-and-control, with strong focus on compliance, testing, and sustainment.

Asia Pacific

Asia Pacific is projected to record a growth rate during the forecast period of 15.6%, which is the third highest among all regions, and reach a valuation of USD 622.1 million by 2026. Demand rises from border tensions, dense urban infrastructure, and rapid drone proliferation. Governments and operators invest in scalable detection around airports, ports, power assets, and smart cities, increasingly pairing sensors with AI analytics.

Japan Drone Detection Market

Japan’s market share in 2026 is estimated at around USD 92.5 million, accounting for roughly 14.8% of CAGR during the forecast period. Demand focuses on airport safety, critical infrastructure, and public-event protection, with strict operational discipline. Purchases lean toward precision detection, low false-alarm rates, and integration with existing security and airspace-management systems.

China Drone Detection Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 222.6 million. Demand is propelled by expansive urban security programs, border monitoring, and protection of strategic facilities. Large-scale deployments emphasize radar-RF fusion, centralized command systems, and rapid manufacturing scaling for nationwide coverage.

India Drone Detection Market

The Indian market in 2026 is estimated at around USD 133.1 million. Demand is rising sharply due to border threats, high-profile events, and protection of airports and sensitive sites. Customers seek rugged, cost-effective detection with scalable coverage, increasingly adding AI classification and mobile units.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 199.0 million and USD 70.8 million in 2026. The Middle East & Africa representing roughly 13.0% CAGR during the forecast period. Demand concentrates in the Middle East for site security and defense readiness, while Latin America focuses on prisons, airports, and VIP protection. Budgets favor modular systems, rapid deployment kits, and managed services.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Accelerate Innovation While Security Needs Outpace Solutions

Airbus SE and Dedrone lead in scalable counter-UAS platforms, with demand surging for AI-driven detection at airports and critical infrastructure, maintaining full order backlogs and rapid deployment timelines. DroneShield and Leonardo S.p.A. dominate multi-mission systems for military and border security, capitalizing on regional conflicts and regulatory mandates. Lockheed Martin, Raytheon, and Saab focus on integrated defense solutions with radar and jamming tech, while Thales, Azur Drones, and Skyfend-Europe target urban and commercial applications via portable, cost-effective sensors. Overall, expansion hinges on AI integration, supply chain resilience for RF components, and partnerships to meet global counter-drone mandates.

LIST OF KEY DRONE DETECTION COMPANIES PROFILED IN REPORT

- Airbus SE (Netherlands)

- Dedrone (U.S.)

- DroneShield Group Pty Ltd (Australia)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Raytheon Company (U.S.)

- Saab AB (Sweden)

- Thales Group (France)

- Azur Drones (France)

- Skyfend-Europe (Germany)

KEY INDUSTRY DEVELOPMENTS

- December 2025: DroneShield won an USD 8.2 million contract to provide counter-drone equipment and associated services to a Western military customer via a regional reseller. The scope includes handheld counter-drone devices, accessories, spare-parts kits, and ongoing software updates.

- September 2025: Taiwan-based Tron Future Tech and Canada’s AiNOS AI signed an MoU focused on drone management, AI-enabled defense, and smart-city innovation. Under the arrangement, Tron will provide drone-detection radar and integrated interception technologies, while AiNOS AI will contribute AI software expertise through teams across Canada, the U.S., and South Korea.

- July 2025: Metis secured a contract from a NATO customer to supply multiple Skyperion drone-detection systems. The systems will support the detection layer within a broader integrated Counter-Uncrewed Air Systems (C-UAS) capability.

- March 2023: Unifly and SkeyDrone both prominent players in UAS traffic management announced the signing of a strategic partnership. As part of the deal, Unifly will supply SkeyDrone with its automated, interoperable UTM platform, designed to be compliant with the latest U-space regulatory requirements.

- March 2023: Thales and Drone XTR entered into a Memorandum of Understanding to jointly deliver an integrated drone-detection solution, combining their respective capabilities into a unified offering.

REPORT COVERAGE

The drone detection market report presents a structured view of current market size and future projections across all key segments. To assess industry dynamics, it uses Porter’s Five Forces to evaluate competitive pressure and the negotiating leverage of both suppliers and customers. The report also examines retrofit and upgrade activity that can expand aftermarket revenue potential, and it tracks major competitive moves such as partnerships, strategic agreements, mergers and acquisitions, and other notable developments. It compares regional footprints across major geographies and closes with a competitive landscape section featuring estimated market shares and detailed profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.8% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Platform, By Technology, By Range, By End Use, and Region |

|

By Platform |

· Ground-based · Handheld |

|

By Technology |

· Radar Systems · RF Detection · Optical Systems · Acoustic Systems · Others |

|

By Range |

· Short Range (Up to 1 Km) · Medium Range (1 Km to 5 Km) · Long Range (Above 5 Km) |

|

By End Use |

· Military & Defense · Commercial · Government · Others |

|

By Region |

· North America (By Platform, Technology, Range, End Use, and Country) o U.S. (Platform) o Canada (Platform) · Europe (By Platform, Technology, Range, End Use, and Country) o U.K. (Platform) o Germany (Platform) o France (Platform) o Russia (Platform) o Rest of Europe (Platform) · Asia Pacific (By Platform, Technology, Range, End Use, and Country) o China (Platform) o India (Platform) o Japan (Platform) o Rest of Asia Pacific (Platform) · Rest of the World (By Platform, Technology, Range, End Use, and Country/Sub-region) o Middle East & Africa (Platform) o Latin America (Platform) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,783.6 million in 2025 and is projected to reach USD 6,123.5 million by 2034.

In 2025, Europes market value stood at USD 555.03 million.

The market is expected to exhibit a CAGR of 14.8% during the forecast period of 2026-2034.

By ground based platform segment is expected to dominate the market.

Rapid expansion of drone threats around high-value assets are driving market growth.

Airbus SE (Netherlands), Dedrone (U.S.), DroneShield Group Pty Ltd (Australia), Leonardo S.p.A. (Italy), Lockheed Martin Corporation (U.S.), Raytheon Company (U.S.) are few major players in the global market.

Europe held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us