Earphones and Headphones Market Size, Share & Industry Analysis, By Product (Earphones and Headphones), By Connectivity (Wired, Wireless (Bluetooth/RF), and True Wireless (TWS)), By Application (Fitness, Gaming, Virtual Reality, and Music & Entertainment), By Price Band (< USD 50, USD 50-100, and > USD 100), By Distribution Channel (Offline and Online), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

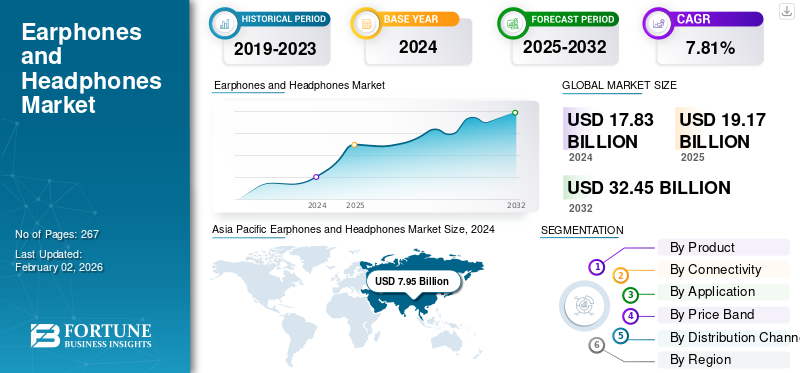

KEY MARKET INSIGHTS

The global earphones and headphones market size was valued at USD 19.17 billion in 2025. The market is projected to grow from USD 20.67 billion in 2026 to USD 37.05 billion by 2034, exhibiting a CAGR of 7.57% during the forecast period. Asia Pacific dominated the global earphones and headphones market with a market share of 44.89% in 2025.

The global earphones and headphones market has grown swiftly over the last decade. The market growth is primarily driven by steaming consumption, increasing smartphone penetration, and the transition toward wireless audio. According to the International Telecommunication Union (ITU), the number of global mobile subscriptions exceeded 8.6 billion in 2023, directly broadening the addressable base for personal spatialized audio devices. The shift toward wireless technology intensified after Apple stopped offering the 3.5 mm jack in 2016, pushing manufacturers to follow the trend and magnifying the demand for Bluetooth-enabled models. This was supported by Bluetooth SIG, which registered that the annual shipments of Bluetooth audio devices surpassed 1.3 billion units in 2023. On the other hand, advancements in headphones technology such as low-latency codecs, active noise cancellation (ANC), and AI-assisted sound tuning have positioned headphones as lifestyle and productivity tools, driving their adoption amongst consumers.

Few well established players in the market include Apple, Samsung (Harman/JBL), Sony, Bose, Sennheiser, and Xiaomi. These industry giants emphasize the advancement of wireless technologies, especially through ANC, improved Bluetooth performance, and AI-enhanced sound personalization. They also focus on widening portfolio, offering premium flagship models alongside affordable mass-market options to target multiple consumer segments.

Download Free sample to learn more about this report.

Earphones and Headphones Market Key Takeaways

- 2025 Market Size: USD 19.17 Billion

- 2026 Market Size: USD 20.67 Billion

- 2034 Forecast Market Size: USD 37.05 Billion

- CAGR: 7.57% from 2026–2034

- Asia Pacific dominated the earphones and headphones market with a 44.89% share in 2025.

- The earphones segment accounted for a 75.04% market share in 2026.

- The true wireless segment captured a 56.17% market share in 2026.

Asia Pacific

Asia Pacific generated USD 8.61 billion in 2025 and accounted for 44.89% of global market revenue.

North America

North America held a 23.11% market share and generated USD 4.43 billion in revenue in 2025.

Europe

Europe accounted for a 20.43% market share and reached USD 3.92 billion in 2025.

U.S.

The market is projected to reach USD 4.12 billion by 2026.

Japan

The market is projected to reach USD 0.78 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Soaring Wireless Audio Adoption Intensified by Smartphone Ecosystems to Drive Market Growth

The extreme shift from wired to wireless audio devices, amplified by increasing smartphone penetration and the eradication of traditional audio jacks across flagship devices is leading the growth of the earphones and headphones market. As prominent smartphone manufacturers including Google, Samsung, and Apple increasingly design ecosystems optimized for Bluetooth audio, consumers are prompted to adopt wireless alternatives that offer improved portability, convenience, and smart features. This shift is consolidated by swift developments in technologies such as Bluetooth LE Audio, advanced ANC, and low-latency codecs, which considerably enhance user experience and diminish performance gaps between wired and wireless models. The widespread use of gaming, streaming platforms, and remote work tools further magnifies the demand for high-quality wireless headphones, making product adoption one of the strongest and sustained growth factors in the market.

MARKET RESTRAINTS

Increased Product Cost Led by Advanced Technology Integration to Hamper Market Growth

The increasing cost of devices, especially those equipped with excellent features such as advanced audio processors, AI-based personalization, and multi-device connectivity, may hamper the expansion of the market. These technologies increase manufacturing and component expenses significantly, making high-performance models less accessible to budget-conscious consumers, particularly in emerging markets. Moreover, shorter innovation cycles and frequent product upgrades prompts brands to price new models at premium pricing, broadening the affordability gap and decelerating adoption among price-sensitive buyers. Thus, cost barrier can obstruct mass-market penetration and delay replacement cycles, hampering overall market expansion.

MARKET OPPORTUNITIES

Surging Demand for Health, Fitness, Wearable-Integrated Audio Solutions to Create New Growth Avenues

As consumers adopt smart lifestyle products such as wearables at a rapid pace, the convergence for audio devices with health and fitness technologies is increasing, thereby offering multiple growth opportunities to manufacturers. Earphones designed with heart-rate monitoring, biometric sensors, motion tracking, and real-time coaching capabilities are gaining popularity amongst consumers. This is further reinforced by the global surge in smart wearable adoption and fitness app users. As brands explore deeper integration between smartwatches, headphones, and health platforms, wireless audio devices are progressing into multifunctional wellness tools rather than standalone accessories. This transition has opened new growth streams and revenue pockets, especially in sports and wellness segments and positions audio makers to tap into the expanding digital health ecosystems.

EARPHONES AND HEADPHONES MARKET TRENDS

AI-Enhanced Audio Personalization Becoming Mainstream

One of the major influential trends in the market is the swift adoption of AI-enabled personalization, catering sound output and device behavior to individual user preferences. Contemporary models increasingly feature environment-aware noise cancellations, adaptive EQ, and voice assistant controls that mimic user’s habits to optimize audio performance in real time. Brands such as Sony, Apple, and Bose are combining AI and machine learning algorithms that analyze listening patterns, ear shape, and ambient sound to deliver customized acoustic profiles. This transition toward intelligent audio uplifts user experience and also consolidates brand differentiation, making AI-powered personalization a defining trend in the coming generation of personal audio devices.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product

Affordability and Wide Accessibility to Drive Earphones Segment Growth

On the basis of product, the market is segmented into earphones and headphones.

The earphones segment dominated the global market share 75.04% in 2026 owing to their affordability, portability, compact design, and solid alignment with mobile-first consumer behavior. The surge in True Wireless Stereo (TWS) adoption augmented this domination. Well-recognized brands such as Apple, Samsung, and Xiaomi have popularized wireless earphones through ecosystem integration and frequent software-driven feature upgrades. Furthermore, earphones are widely accessible to mass population due to their economic price points and are preferred for multiple daily activities, including fitness, commute, and online meetings, fueling their large scale market penetration.

To know how our report can help streamline your business, Speak to Analyst

The headphones segment is projected to expand at the fastest CAGR of 5.20% over the projected years. Growth factors propelling the segment’s expansion include rising demand for premium audio experience, advanced noise-cancellation capabilities, and immersive listening experiences. Both over-ear and on-ear headphones are experiencing growth momentum among gamers, professionals, and audiophiles who prioritize soundstage, comfort, and longer battery life along with improved audio performance.

By Connectivity

Strong Ecosystem Integration Capabilities to Drive True Wireless Segment Dominance

By connectivity, the market is segmented into wired, wireless, and true wireless.

The true wireless segment captured the largest share 56.17% of the market in 2026. In 2025, the segment is anticipated to dominate with a 55.00% share. The growing adoption of truly wire-free earbuds and novel innovation from brands such as Apple, Samsung, Sony, and Xiaomi are driving the segmental growth. Their benefits such as enhanced ANC, technological upgrades including LE Audio, and health/fitness integrations has largely upgraded user experience, leading to increased demand for true wireless earphones.

The wireless segment is the second-fastest growing segment. Wireless earphones and headphones are used prominently across different consumer segments due to their improved Bluetooth performance, cable-free convenience, and strong ecosystem integration with laptops, smartphones, tablets, and wearables. Moreover, wireless systems offer a wide price range from economic and affordable models to premium flagships, heightening adoption rate across all demographics.

By Application

Surge in Music Industry and Entertainment-Driven Product Consumption to Support Music & Entertainment Segment Growth

Based on application, the market is segmented into fitness, gaming, virtual reality, and music & entertainment.

The music & entertainment segment accounts for the largest earphones and headphones market share since it represents the fundamental and most frequent use case for personal audio devices globally. The surge in podcast consumption, music-streaming subscribers, and video content across platforms such as Netflix, YouTube, and Spotify has considerably grown the daily usage of audio accessories. In addition, individuals also opt for headphones and earphones for leisure listening, commuting, and remote work activities that fall largely under entertainment-driven consumption. The Gaming segment is projecteed to dominate the market with a share of 17.95% in 2026.

The virtual reality segment is projected to grow at the fastest CAGR, boosted by enterprise-level VR training solutions, expansion of immersive gaming, and metaverse platforms. Moreover, companies are increasingly developing VR-optimized audio solutions to support fitness experiences, interactive simulations, and virtual collaborations. This rapid adoption, together with ongoing investments in AR/VR ecosystems, places the virtual reality segment for the strongest future growth.

By Price Band

Availability of Budget-friendly Brands with Multi-Functionality Features to Drive <USD 50 Segment Growth

Based on price band, the market is segmented into <USD 50, USD 50-100, and >USD 100.

The <USD 50 price band segment accounted for the largest market share 58.54% in 2026 as it caters to the widest consumer base. This segment benefits from high-volume sales through online platforms, solid demand in developing regions, and the availability of several pocket-friendly brands. Further, the growing adoption of entry-level TWS and wired earphones often priced under USD 25 further amplify the segment’s share.

The > USD 100 segment is the fastest growing segment and is projected to flourish at the highest CAGR over the projected years. Advanced features such as multipoint connectivity, spatial audio, ANC, and AI-enhanced sound tuning are among the few factors leading segmental growth.

By Distribution Channel

Wide Product Assortments and Affordable Mass-Market Options to Drive Supermarkets & Hypermarkets Segment Growth

Based on distribution channel, the market is segmented into offline and online.

In 2024, the global market was dominated by offline distribution channel. Consumers prefer to test earphones and headphones physically, especially comfort, sound quality, fit, and build which significantly impacts purchase decisions. Brand-exclusive outlets, electronics stores, and multi-brand retail stores offer expert assistance, hands-on trials, and immediate product availability that help build consumer trust and prompt higher-value purchases.

In addition, the online segment is the fastest-growing channel and is projected to grow at a CAGR of 8.67% during the study period. The segment’s growth is propelled by the convenience of home delivery, aggressive pricing, wide product assortment, product review, and frequent discount cycles.

Earphones and Headphones Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Earphones and Headphones Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 8.61 Billion, contributing 44.89% to global market revenue, and is projected to grow to USD 9.34 Billion in 2026. The regional market growth is majorly driven by the world’s largest smartphone user population, with countries including China, India, and Indonesia leading huge demand for audio accessories. Moreover, digitally active demographic heavily engaged in gaming, social media, and streaming significantly fuels the demand for wireless audio devices. In addition, competitive pricing and large-scale production make TWS devices more accessible to mass consumers as compared to other regions. The Japan market is projected to reach USD 0.78 billion by 2026, the China market is projected to reach USD 3.20 billion by 2026, and the India market is projected to reach USD 2.91 billion by 2026.

North America

North America is anticipated to witness considerable growth in the coming years. During the forecast period, The North America region captured 23.11% of the global market in 2025, generating USD 4.43 Billion in revenue, and is projected to reach USD 4.75 Billion in 2026. The regional growth is driven by the high adoption of premium audio devices, strong penetration of podcasts, streaming platforms, and digital media, along with the increasing prevalence of hybrid work and remote communication across countries such as the U.S. and Canada. The U.S. market is projected to reach USD 4.12 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 3.92 Billion in 2025, accounting for 20.43% share, and is expected to reach USD 4.18 Billion in 2026. securing its position as the third-largest regional market. The region benefits from a well-established audio culture, with consumers demonstrating a strong preference for Hi-Fi, premium, and ANC-enabled headphones. In addition, the presence of leading manufacturers such as Beyerdynamic, Sennheiser, Sony, and Bose, coupled with the growing adoption of hybrid working arrangements across the region, continues to drive demand for professional-grade headsets and support market expansion. The UK market is projected to reach USD 0.56 billion by 2026, while the Germany market is projected to reach USD 0.80 billion by 2026.

South America

The South America market was valued at USD 1.6 Billion in 2025, capturing 8.35% of global revenue, and is estimated to reach USD 1.73 Billion in 2026. The growth is supported by the rapid adoption of true wireless earbuds, increasing availability of affordable consumer electronics, and the strong presence of leading brands such as Xiaomi, JBL, and Motorola. Demand across key countries including Brazil, Argentina, Colombia, and Chile continues to contribute to the expansion of the regional earphones and headphones market.

Middle East & Africa

The Middle East & Africa market recorded a size of USD 0.62 billion in 2025, accounting for 3.22% of the global market share, and is projected to reach USD 0.67 billion in 2026. The region is expected to experience steady growth over the forecast period, driven by rising consumer demand for personal audio devices, increasing smartphone penetration, and expanding retail distribution networks. In addition, the UAE market is set to reach a valuation of USD 0.06 billion in 2025, supporting the region’s overall market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Product Differentiation, Digital Presence, and Marketing Partnerships to Outpace Competitors

The global headphones and earphones market faces intense competition due to the presence of multinational players including Apple, Sony, Bose, Samsung, and Sennheiser competing alongside fast-growing regional brands. Key players in the industry distinguish themselves through focusing on product innovation, spatial audio quality, ANC features, AI-driven personalization, and longer battery life. Moreover, price competitiveness is decisive, particularly in emerging economies where brands including boAt and Xiaomi dominate through value-driven offerings. Companies also strengthen their positions through ecosystem integration, bundling audio devices with smartphones and wearables for seamless user experiences. Aggressive online presence, marketing partnerships, product diversification, and frequent model refreshes help brands maintain visibility and retain users. Premium brands emphasize build quality and acoustic performance, while mass-market players compete based on affordability and design appeal.

LIST OF KEY EARPHONES AND HEADPHONES COMPANIES PROFILED

- Apple Inc. (U.S.)

- Sony Corporation (Japan)

- Samsung Electronics (South Korea)

- Bose Corporation (U.S.)

- Sennheiser Electronic GmbH Co KG (Germany)

- Skullcandy Inc.(U.S.)

- Xiaomi Corporation (China)

- Audio-Technica Corporation (Japan)

- Beat Electronics (Apple subsidiary) (U.S.)

- Plantronics/Poly (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Sony India introduced flagship audio technology for competitive gamers by launching the INZONE H9 II (WH-G910N) gaming headset. This newly launched headgear would be available for sale from November 22 on online platforms including Shopatsc.com, Amazon, and Flipkart. These second gen headphones feature 30mm drivers making it significantly more affordable than the XM6s.

- October 2025: Chinese brand QCY unveiled a range of audio devices in the Indian market, including headphones, earbuds, TWS, and Bluetooth speakers. The newly launched product range is made available for sales via leading online channels including Amazon and Flipkart and with offline expansion planned soon.

- October 2025: AIAIAI collaborated with musician Blood Orange to launch a limited-edition “Artist Series” of its headphones (Tracks and TMA-2 Wireless). The company blended audio hardware with creative branding, appealing to lifestyle-conscious consumers.

- September 2025: QCY, Chinese budget-focused audio brand, introduced the new true-wireless earbuds QCY MeloBuds N70, among the first to leverage a hybrid driver design combining a traditional dynamic driver with a MEMS-based microspeaker tweeter, delivering wider frequency response and better fidelity at budget prices.

- August 2025: Sony undertook a notable expansion by broadening its audio product footprint into the gaming ecosystem through the launch of its INZONE lineup, including premium gaming headsets and accessories. This move represents a strategic diversification beyond traditional consumer audio, allowing Sony to strengthen its presence in the rapidly growing gaming and e-sports market.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.57% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Connectivity, Application, Price Band, Distribution Channel, and Region |

|

By Product |

· Earphones · Headphones |

|

By Connectivity |

· Wired · Wireless (Bluetooth / RF) · True Wireless (TWS) |

|

By Application |

· Fitness · Gaming · Virtual Reality · Music & Entertainment |

|

By Price Band |

· <USD 50 · USD 50-100 · > USD 100 |

|

By Distribution Channel |

· Offline · Online |

|

By Geography |

· North America (By Product, Connectivity, Application, Price Band, Distribution Channel, and Country) o U.S. (Product) o Canada (Product) o Mexico (Product) · Europe (By Product, Connectivity, Application, Price Band, Distribution Channel, and Country/Sub-region) o Germany (Product) o U.K. (Product) o France (Product) o Spain (Product) o Italy (Product) o Rest of Europe (Product) · Asia Pacific (By Product, Connectivity, Application, Price Band, Distribution Channel, and Country/Sub-region) o China (Product) o Japan (Product) o India (Product) o Australia (Product) o Rest of Asia Pacific (Product) · South America (By Product, Connectivity, Application, Price Band, Distribution Channel, and Country/Sub-region) o Brazil (Product) o Argentina (Product) o Rest of South America (Product) · Middle East & Africa (By Product, Connectivity, Application, Price Band Distribution Channel, and Country/Sub-region) o South Africa (Product) o UAE (Product) o Rest of the Middle East & Africa (Product) |

Frequently Asked Questions

Fortune Business Insights says that the global market value reached USD 19.17 billion in 2025 and is projected to reach USD 37.05 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 8.61 billion.

The market is expected to exhibit a CAGR of 7.57% during the forecast period of 2026-2034.

The earphones segment led the market by product in 2026.

Steaming consumption, increasing smartphone penetration, and the transition toward wireless audio are key factors driving the global market growth.

Apple, Samsung (Harman/JBL), Sony, Bose, Sennheiser, and Xiaomi are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Advancements in earphones and headphones technology such as low-latency codecs, active noise canceling (ANC), and AI-assisted sound tuning have positioned them as productivity tools, favoring their adoption amongst consumers.

- 2021-2034

- 2025

- 2021-2024

- 267

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us