Edge AI Processor Market Size, Share & Industry Analysis, By End-user (Consumer Electronics, Healthcare, Automotive, Retail and E-commerce, Government and Defense, Others (Manufacturing, etc.)), By Type (Central Processing Unit (CPU), Graphics Processing Unit (GPU), Field Programmable Gate Array (FPGA), and Application Specific Integrated Circuits (ASIC)), By Device Type (Consumer Devices and Enterprise Devices), By Application (Computer Vision, Speech & Audio, NLP / On-device LLMs, Time-series & Control, Multimodal, and Others (Recommendation/Ranking, etc.)), and Regional Forecast, 2025-2032

EDGE AI PROCESSOR MARKET SIZE AND FUTURE OUTLOOK

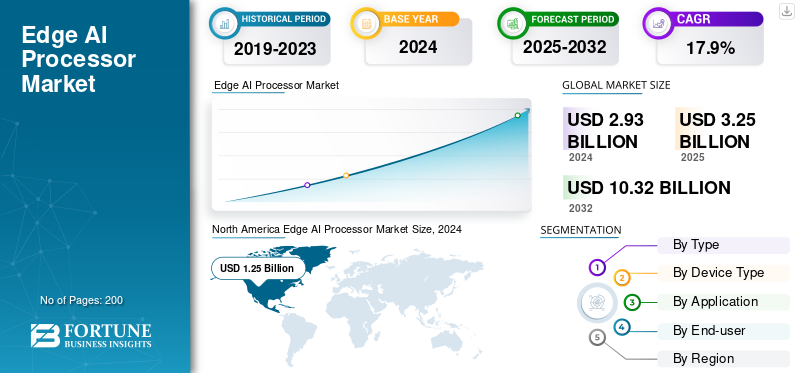

The global edge AI processor market size was valued at USD 2.93 billion in 2024. The market is projected to grow from USD 3.25 billion in 2025 to USD 10.32 billion by 2032, exhibiting a CAGR of 17.9% during the forecast period. North America dominated the edge AI processor market with a market share of 42.66% in 2024.

An edge AI processor is a specific kind of central processing unit (CPU) or chip made to handle machine learning (ML) and artificial intelligence (AI) functions locally on a device instead of depending on a centralized cloud or data center. A few of the main benefits of this strategy, called edge computing, include decreased latency, improved data privacy, and less bandwidth consumption.

The growing need for real-time processing, low-latency, and privacy-compliant solutions in AI applications is causing a major shift in the global industry. In addition, a large number of consumer companies are propelling the market with new product releases and product revisions to boost the industry's performance. Such developments and innovations in the industries are further expected to create enormous opportunities for the global industry in the coming years.

NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Advanced Micro Devices, Inc., Apple, Inc., and Mythic AI are some of the leading companies in the industry.

Impact of Reciprocal Tariffs

Reciprocal Tariffs Increased Costs Slowing the Market Growth

Reciprocal tariffs between the U.S. and China can raise prices of key AI components. This could create increased costs for edge AI processors which can suppress adoption of these devices. Tariffs can also adversely affect global supply chains and drive companies to explore alternate sourcing. All of this results in uncertainty and delays in production. Although this situation can slow innovation and investment, it may also encourage manufacturers to develop new, stronger strategies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Explosion of IoT Devices Drives Market Growth

The boom in Internet of Things (IoT) devices is the key catalyst for the rapid growth of the edge AI processor market. Billions of smart devices such as cameras and wearables, and industrial sensors are expanding and generating massive volumes of data, which creates inefficiencies when offloaded to the cloud introducing latency, increasing costs, and raising privacy concerns. Edge AI processors can enable on-device data processing in real time, which is crucial to use cases such as autonomous vehicles and predictive maintenance in factories. Increase in low-power high-performance chips and 5G connectivity are also facilitating edge AI processor market growth.

According to the National Institute of Standards and Technology, it is estimated that there will be over 75 billion IoT devices around the world by the year 2025.

Market Restraints

High Development and Integration Cost Hinder Market Growth

The increase of the market faces barriers, the reason being elevated development and integration costs. The design and customization of the AI processors for specific edge applications necessitate large amounts of research, specialized engineering skills, and fabrication techniques, all of which contribute to increased manufacturing costs. The time and cost of integrating these processors into hardware ecosystem and platforms (i.e. vehicles, IoT devices, and industrial systems) compounds and adds more complexity and cost. These financial and technical barriers may limit scalability and increase the competitive weight on smaller companies. As a byproduct, only certain organizations with substantial R&D capacity and funding are able to capitalize on the growth opportunities within the Edge AI landscape.

Market Opportunities

Edge AI in Autonomous Vehicles Creates New Growth Opportunities in the Market

The edge AI processor market is positioned for fast growth, supported by the rise of autonomous vehicles, drones, and intelligent robots. These technologies rely on the processing of data in real-time and on-the-spot decision-making capabilities at the edge of the network, leading to reduced latency and enhanced responsiveness. As industries become more automated and continue to embrace autonomous intelligence in mobility, there will be a growing demand for powerful, high-performance processors that can operate in energy-efficient ways. This growth will also create plentiful opportunities for innovation in chip design, architecture, and more broadly in integration. Companies that can provide low latency, secure, and scalable edge AI technology will be in a strong position to capture a significant portion of the market opportunities in this emerging new technological space.

EDGE AI PROCESSOR MARKET TRENDS

Customized AI Chips for Specific Application Emerges as a Major Trend

The market for edge AI processors is witnessing a notable trend toward the creation of domain-specific designs or customized AI processors chips for various narrow applications. Companies are developing processors that are domain specific to markets including, consumer electronics, smart cameras, industrial robotics, and automotive. These custom-designed chips have greater operational efficiency by balancing low power usage, compact form factor, and computational power.

As edge applications become more diverse, customizing specific edge applications allows devices to process data faster and more accurately. The shift to custom AI hardware is driving innovation in the semiconductor and technology sectors while helping companies create differentiation in the market, and seek new partnerships.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Versatility and Strong Performance Boosts Graphics Processing Unit Segment Growth

In terms of type, the market is divided into Graphics Processing Unit (GPU), Central Processing Unit (CPU), Field Programmable Gate Array (FPGA), and Application Specific Integrated Circuits (ASIC).

The graphics processing unit segment held the largest revenue share of USD 1.16 billion in the year 2024. The growth is attributable to their versatility and strong performance in handling a wide range of AI workloads across various applications.

Of all the segments, Application Specific Integrated Circuits (ASIC) holds the highest CAGR of 22.2% in the global market. The segment’s growth is attributed to its ability to offer highly efficient, customized solutions for specific edge AI tasks, propelling adoption in specialized markets.

By Device Type

Consumer Devices Dominates Market Owing to Its Widespread Use in Smartphones and Wearables

Based on the device type, the market is divided into consumer devices and enterprise devices.

The consumer devices segment dominates with a market share of USD 1.68 billion. The segment due to its widespread use in smartphones, wearables, and smart home products with integrated AI features.

Enterprise devices holds the highest CAGR of 19.9% in the global market. The segment’s growth is attributable to the increasing adoption of AI in industries such as manufacturing, healthcare, and retail for automation and analytics.

By Application

High Demand in Surveillance and Autonomous Vehicles Enhances the Computer Vision Segment Growth

Based on the application, the market is divided into computer vision, speech & audio, NLP/On-device LLMs, time-series & control, multimodal, and others (recommendation/ranking, etc.).

The computer vision segment accounted for the largest edge AI processor market share at USD 1.59 billion in 2024. The growth is attributable to strong demand in surveillance, autonomous vehicles, and quality inspection.

Multimodal represent the largest CAGR at 27.3% in the global market. Multimodal AI, which combines data types such as vision, speech, and text, is growing fastest as it allows for more sophisticated and context-aware edge applications.

By End-user

Massive Volumes of AI-enabled Smartphones Augments the Consumer Electronics Segment Growth

To know how our report can help streamline your business, Speak to Analyst

In terms of end-user, the market is segmented into consumer electronics, healthcare, automotive, retail and e-commerce, government and defense, and others (manufacturing, etc.).

The consumer electronics segment dominates with a market share of USD 0.79 billion in 2024. The segment’s growth is attributable to massive volumes of AI-enabled smartphones, cameras, and smart appliances .

Automotive represent the largest CAGR at 22.2% in the global market. The growth is due to advancements in ADAS and autonomous driving requiring powerful edge AI processing.

EDGE AI PROCESSOR MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America Edge AI Processor Market Size, 2024 ( USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America region is leading the global industry, with a majority share. The region held the market value of USD 1.14 billion and USD 1.25 billion in 2023 and 2024 respectively. The growth is attributable to the region’s advanced technology infrastructure, strong presence of top edge AI processor companies, and widespread adoption of AI-driven applications.

The U.S. is at the forefront of the North American market, with expected revenue of USD 1.09 billion in 2025. The growth is attributable to the growing demand for real-time processing in various sectors such as autonomous vehicles, healthcare, and consumer electronics.

Europe

The European market is substantially growing and is likely to contribute to a revenue share of USD 0.58 billion in 2025. The new AI Act and the GDPR, two European regulations that promote privacy-preserving on-device data processing, are accountable for this growth.

The U.K., Germany, and France are some of the leading contributors to the growth in the market, with the required revenue stake of USD 0.13 billion, USD 0.13 billion and USD 0.07 billion respectively by 2025.

Asia Pacific

Asia Pacific is also expected to have the highest CAGR of 19.3%, solidifying the market as the fastest growing. The market size was valued at USD 0.99 billion in 2025. The region’s growth is attributable to rapid industrialization, increasing IoT deployments, growing investments in smart cities, and increasing demand for affordable AI solutions.

India and China are major contributors to the market growth with an expected revenue share of USD 0.13 billion, and USD 0.40 billion respectively by 2025.

South America and Middle East & Africa

The markets of South America and Middle East & Africa are growing with an expected share of USD 0.11 billion and USD 0.16 billion respectively in 2025. The growth is attributable to the rise of IoT devices, smart cities, and the need for local, real time data processing. GCC countries are predicted to have a market share of USD 0.05 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus On Low-Power, High-Efficiency Solutions to Lead the Industry

Among the leading companies in the sector are Mythic AI, Apple, Inc., Advanced Micro Devices, Inc., Qualcomm Technologies, Inc., NVIDIA Corporation, and Intel Corporation. These businesses provide a variety of chips and processors, ranging from specialist ASICs to general-purpose CPUs and GPUs, that allow AI functions to operate directly on edge devices rather than in the cloud. Specialized startups that concentrate on low-power, high-efficiency solutions are also driving the industry.

LIST OF KEY EDGE AI PROCESSOR COMPANIES PROFILED:

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Apple, Inc. (U.S.)

- Mythic AI (U.S.)

- Hailo Technologies (Israel)

- Axelera AI (Netherlands)

- Ambarella (U.S.)

- MediaTek Inc. (Taiwan)

- Lattice Semiconductor (U.S.)

- Synaptics (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025- Synaptics Incorporated introduced the Astra SL2600 Series of multimodal Edge AI processors, which aim to revolutionize intelligent device capabilities for the cognitive Internet of Things (IoT). The series launches with the SL2610 product line, encompassing five processor families tailored for various applications, including smart appliances, automation systems, healthcare devices, and autonomous robotics.

- September 2025- In an effort to speed up the creation and implementation of cutting-edge AI and IoT solutions, Grinn, an expert in advanced IoT and embedded systems, announced a strategic alliance with MediaTek. For both businesses, this partnership is a big step toward launching high-performance, scalable embedded computer modules.

- June 2025- Axelera AI launched the Axelera Partner Accelerator Network, a global partner program designed to accelerate the development of customer-ready solutions at the edge using Axelera technology. The program will provide training, co-marketing and technical support for a broad range of partners, creating a rich ecosystem of solution providers for customers in a variety of markets who want to transition proof-of-concept (POC) edge AI inference projects into full production.

- June 2025- Advantech, a provider of embedded computing solutions, announced a collaboration with Edge Impulse to accelerate edge AI innovation using Qualcomm Dragonwing QCS6490 processor. The partnership aims to simplify the development and deployment of edge AI applications through an integrated, user-friendly platform.

- March 2025- Intel unveiled its new Intel® AI Edge Systems, Edge AI Suites and Open Edge Platform initiatives. These offerings help streamline and speed up AI adoption at the edge across industries such as retail, manufacturing, smart cities, and media and entertainment by simplifying integration with existing infrastructure.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the edge AI processor market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Growth Rate | CAGR of 17.9% from 2025-2032 |

| Historical Period | 2019-2023 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Device Type, Application, End-user and Region |

| By Type |

|

| By Device Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 2.93 billion in 2024 and is projected to reach USD 10.32 billion by 2032.

The market is expected to exhibit steady growth at a CAGR of 17.9% during the forecast period.

The explosion of IoT devices is speeding up the market growth.

NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Advanced Micro Devices, Inc., Apple, Inc., and Mythic AI are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 1.25 billion in 2024.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us