Edge Computing Hardware Market Size, Share & Industry Analysis, By Hardware Type (Edge Servers/Micro Data Centers, Edge Gateways, Industrial PCs/Embedded Edge Devices, Smart Sensors & Edge Nodes, Edge Networking Equipment, and Others), By Enterprise Type (Small & Medium Enterprises (SMEs) and Large Enterprises), By End-user (Industrial, Security & Surveillance, Automotive, Energy & Utilities, Retail & Commercial, Healthcare, and Others), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

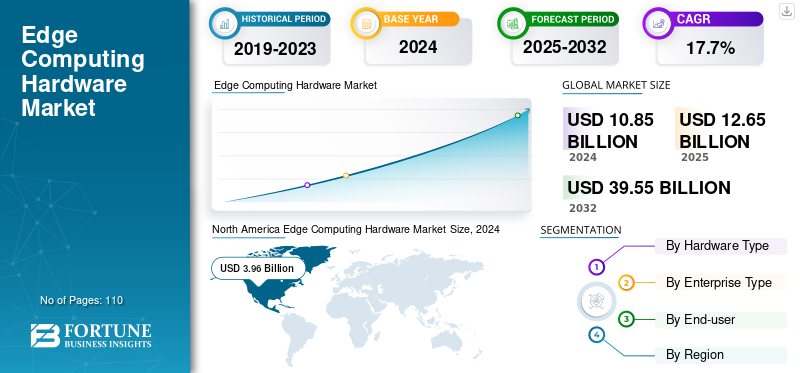

The global edge computing hardware market size was valued at USD 12.65 billion in 2025 and is projected to grow from USD 14.82 billion in 2026 to USD 49.38 billion by 2034, exhibiting a CAGR of 16.05% during the forecast period. North America dominated the global edge computing hardware market with a share of 36.05% in 2025.

Edge computing hardware refers to all the physical equipment deployed near the source of data generation rather than in centralized cloud data centers to enable local processing, storage, and real-time decision-making. It includes every hardware component that makes edge computing possible across industries like industrial, retail, automotive, healthcare, energy & utilities, and others. Market growth is driven by the explosion of data at the edge, the growth of AI inference at the edge, and the increasing adoption of Industry 4.0 and industrial automation worldwide.

Furthermore, many key industry players, such as Dell Technologies Inc., Hewlett Packard Enterprise Company, Cisco Systems, Inc., Huawei Technologies Co., Ltd., and Lenovo, operating in the market, are focusing on investing in regional data hubs, AI factories, and industrial edge labs to support customers locally and reduce latency.

Download Free sample to learn more about this report.

IMPACT OF RECIPROCAL TARIFF

Rising Tariffs on Edge Computing Devices Increase Material Costs for Market Vendors

The reciprocal tariffs imposed by major world economies contribute to a higher landed cost of many of the key inputs, such as semiconductor chips, printed circuit boards, power modules, and other networking components, which edge computing hardware manufacturers use. For edge computing hardware vendors, this raises the bill of materials for servers, gateways, and industrial PCs, squeezing margins or forcing price hikes for enterprise buyers. Moreover, higher duties on ICT and electronics also reduce demand sensitivity in some price-conscious segments. The analysis by the Information Technology and Innovation Foundation shows that a 25 percent tariff on semiconductor imports would effectively act as a broad price increase on ICT goods, lowering ICT consumption and slowing capital formation in digital infrastructure, which includes servers and network equipment used at the edge.

EDGE COMPUTING HARDWARE MARKET TRENDS

Increasing Shift from Centralized Cloud to Hybrid Edge Architectures Strengthens Market Momentum

A growing number of businesses are shifting from "cloud-first" strategies to hybrid edge solutions that separate time-critical or sensitive tasks operating at the edge from mass storage and analysis done primarily via the central cloud. This architectural shift increases demand for edge servers, gateways, and micro data centers that act as local execution points. Hybrid edge architectures help organizations cut latency, keep critical operations running during network outages, and retain greater control over regulated data, while still leveraging cloud scale for AI training and long-term storage. For instance,

- According to a study conducted by industry experts, around 10 percent of enterprise-generated data was processed outside central data centers a few years ago. This proportion is expected to reach 75 percent by 2025, underlining how rapidly workloads are shifting to edge and hybrid environments.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Volume of IoT and Video Data Drives Edge Hardware Deployment

A key driving force behind the rapid increase in demand for edge computing hardware is the explosive growth of data being generated outside of traditional data center facilities. This is occurring due to the widespread adoption of sensors, connected devices, cameras, machines, and autonomous systems that continuously produce large volumes of information in real operational environments. In addition, high-volume video data from smart cities, factories, and retail environments further accelerates this growth, requiring local AI processing to reduce bandwidth strain and deliver real-time insights. Therefore, the growing volume of IoT and video data is expected to propel the edge computing hardware market growth over the forecast period. For instance,

- In September 2024, according to IoT Analytics’ State of IoT 2024 report, the number of connected IoT devices reached 16.6 billion at the end of 2023 and is expected to grow 13 percent to 18.8 billion by the end of 2024, with a forecast of roughly 40 billion devices by 2030, illustrating how data creation is rapidly shifting from central data centers to billions of edge endpoints.

MARKET RESTRAINTS

High Initial Costs and Complex ROI May Hinder Market Growth

Edge Computing Hardware often requires significant initial investments in servers, gateways, industrial PCs, and rugged networking, making large-scale deployments difficult for many SMEs. Costs associated with integration and on-site setup, along with ongoing maintenance, increase overall expenditures and lengthen payback periods for these solutions. In developing countries, many smaller businesses are delaying their adoption due to financial limitations and dependence on outdated technology, for instance.

- In June 2024, according to an OECD survey, the limited financial resources and high hardware or software costs remain the biggest obstacles for digital adoption in small and medium enterprises in multiple countries.

MARKET OPPORTUNITIES

Expansion of 5G and Private Networks Creates Strong Opportunities for Edge Computing Hardware

The launch of 5G networks and private cellular networks has created a dense network of high-speed, low-latency connectivity, making it perfect for the installation of edge servers, gateways, and multi-access edge computing (MEC) platforms close to the locations of users and devices. Telecom companies and businesses are investing significantly in private 5G to support smart factories, ports, logistics hubs, and other critical infrastructure. These networks require dedicated compute, storage, and networking capabilities at the edge to run applications such as predictive maintenance, autonomous vehicles, and computer vision, creating significant demand for rugged edge servers, industrial PCs, and AI accelerators. For instance,

- According to GSMA Intelligence’s Mobile Economy 2024 report, the number of 5G connections reached 1.6 billion at the end of 2023 and is forecast to climb to 5.5 billion by 2030, when 5G will account for more than half of all mobile connections worldwide, underscoring the scale of 5G-driven edge opportunities.

Segmentation Analysis

By Hardware Type

Increasing Demand for Edge Servers/Micro Data Centers to Propel Segment’s Growth

Based on the hardware type, the market is divided into edge servers/micro data centers, edge gateways, industrial PCs/embedded edge devices, smart sensors & edge nodes, edge networking equipment, and others (including edge AI accelerators, etc.).

Edge servers/micro data centers are anticipated to account for the largest edge computing hardware market share. The edge servers/micro data centers segment will account for 30.05% market share in 2026. This is due to, they act as the primary compute layer at the edge, hosting virtualized workloads, local databases, and AI inference that gateways and end devices alone cannot handle. They also have a compact, modular design that allows them to be rapidly deployed close to users/devices, which is why micro data centers hold a leading share of the market.

Smart sensors & edge nodes are anticipated to rise with the highest CAGR of 19.5% over the forecast period. This is due to the surge in the number of connected IoT devices and intelligent endpoints across homes, factories, cities, and vehicles. According to IoT Analytics, estimates that connected IoT devices will rise from 16.6 billion at the end of 2023 to 18.8 billion in 2024 and exceed 40 billion by 2030, which directly boosts demand for smarter, compute-enabled sensors at the network edge.

To know how our report can help streamline your business, Speak to Analyst

By Enterprise Type

Financial Capacity Invested in Full-Scale Edge Computing Infrastructures Drives Adoption in Large Enterprises

Based on enterprise type, the market is segmented into small & medium enterprises (SMEs) and large enterprises.

In 2024, the large enterprises dominated the global market as they possess the financial capacity to invest in full-scale edge computing infrastructures, including edge servers, industrial PCs, AI accelerators, and secure on-site micro data centers. Global operations of these large firms require high-performance, low-latency computing for automation, robotics, advanced analytics, and compliance-heavy workloads, making them early adopters of edge hardware across manufacturing, energy, logistics, retail chains, and telecom. The large enterprises segment is expected to lead the market, contributing 67.91% globally in 2026.

Small & medium enterprises (SMEs) are projected to grow at the highest CAGR of 18.1% during the forecast period, as they increasingly adopt lightweight edge solutions, compact gateways, and cloud-managed edge devices that require lower upfront investment.

By End-user

Rising Need for Deployment of Industry 4.0 Drives Industrial Sector Growth

Based on the end-user, the market is segmented into industrial, security & surveillance, automotive, energy & utilities, retail & commercial, healthcare, and others (agriculture, etc.).

The industrial sector is anticipated to witness a dominating market share over the forecast period. As factories and warehouses are at the forefront of Industry 4.0, deploying industrial PCs, edge servers, and gateways to support predictive maintenance, robotics, machine vision, and real-time process control. These users typically have large capital budgets and multi-year automation programs, allowing them to roll out extensive on-site or hybrid edge infrastructures across multiple plants and production lines. The industrial segment is expected to account for 31.9% of the market in 2026.

The healthcare sector is projected to grow at the highest CAGR of 21.0% over the forecast period, as hospitals and clinics increasingly adopt edge computing for medical imaging analysis, real-time patient monitoring, and smart hospital operations while keeping sensitive patient data on premises for compliance and privacy.

Edge Computing Hardware Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Edge Computing Hardware Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 4.56 Billion in 2025, representing 36.05% of the global industry, and is expected to reach USD 5.27 Billion in 2026. The market in North America is expected to increase owing to the strong presence of hyperscale cloud and server vendors, early 5G and private network deployments, and high adoption of Industry 4.0 across the region. For instance,

- In February 2024, Dell Technologies and Nokia extended a strategic partnership in which Nokia adopted Dell as its preferred infrastructure partner, transitioning AirFrame customers to Dell PowerEdge servers.

Also, Strong government and industry initiatives are fostering the adoption of edge hardware. These factors play a significant role in fueling the market growth.

U.S Edge Computing Hardware Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.42 billion in 2026, accounting for roughly 23.5% of global edge computing hardware sales.

Europe

Europe recorded a market size of USD 3.05 Billion in 2025, capturing 24.14% of the global market share, and is projected to reach USD 3.54 Billion in 2026. In the region, the presence of strict data protection rules, energy efficiency targets, and sustainability policies is encouraging enterprises to adopt localized edge computing architectures that minimize data movement and optimize resource use.

U.K Edge Computing Hardware Market

The U.K. edge computing hardware market in 2025 is estimated at around USD 0.66 billion, representing roughly 4.5% of global edge computing hardware revenues.

Germany Edge Computing Hardware Market

Germany’s edge computing hardware market is projected to reach approximately USD 0.78 billion in 2026, equivalent to around 5.4% of global edge computing hardware sales.

Asia Pacific

In 2025, Asia Pacific represented USD 3.39 Billion, accounting for 26.76% of the worldwide market, and is projected to grow to USD 4.08 Billion in 2026. This is owing to rapid industrialization, large-scale urbanization, and government-backed digital initiatives in countries such as China, India, Japan, and South Korea. In the region, India and China are both estimated to reach USD 0.58 billion and USD 0.82 billion, respectively, in 2026. For instance,

- In February 2024, Huawei signed an MoU with CelcomDigi to collaborate on 5G-enabled digital business initiatives, integrating Huawei solutions in 5G access, 5G core, and multi-access edge computing. The partnership aims to deliver private network connectivity and edge computing services for Chinese and Malaysian enterprises.

Japan Edge Computing Hardware Market

The Japan edge computing hardware market in 2026 is estimated at around USD 0.8 billion, accounting for roughly 5.3% of global edge computing hardware revenues. The rise of smart cities, industrial IoT, and 5G rollouts across the country necessitates the deployment of edge servers and micro data centers to handle local data storage, network management, and enable real-time data processing and analytics.

China Edge Computing Hardware Market

China’s edge computing hardware market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.82 billion, representing roughly 5.5% of global edge computing hardware sales.

India Edge Computing Hardware Market

The India edge computing hardware market in 2026 is estimated at around USD 0.58 billion, accounting for roughly 3.7% of global edge computing hardware revenues.

South America

South America is expected to witness moderate growth in this market space during the forecast period. The South America market is set to reach a valuation of USD 1.02 billion in 2025. The telecom operators in the region continue to deploy 4G, 5G, and fiber networks, enabling new edge use cases in sectors such as oil and gas, mining, logistics, and urban security that depend on reliable, low-latency hardware at remote sites and city edges. These factors drive the market growth across the region.

Middle East & Africa

Middle East & Africa contributed 5.00% to the global market in 2025, with a valuation of USD 0.63 Billion, and is projected to reach USD 0.75 Billion in 2026. The region’s adoption of 5G and fiber optic networks is driving demand for edge computing at cell sites, logistics hubs, ports, and transport corridors, as low-latency applications and AI-driven workloads become essential for autonomous vehicles, smart grid management, and traffic optimization. In the Middle East & Africa, the GCC is set to reach a value of USD 0.25 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Portfolio by Key Players to Propel Market Progress

The global edge computing hardware market holds a semi-consolidated market structure, constituting prominent players such as Dell Technologies, Inc., Hewlett Packard Enterprise Company, Huawei Technologies Co., Ltd., Cisco Systems, Inc., and Lenovo. The significant market share of these companies is due to numerous strategic activities, including collaboration with cloud providers, chipmakers, and telecom operators to deliver integrated edge platforms.

- For instance, in November 2024, Dell Technologies announced new capabilities for its Dell NativeEdge edge operations platform, adding more automation and AI features so customers can deploy, scale, and manage edge infrastructure more easily.

Other notable players in the global market include Intel Corporation, NVIDIA Corporation, Advantech Co., Ltd., ADLINK Technology Inc., and Schneider Electric SE. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY EDGE COMPUTING HARDWARE COMPANIES PROFILED

- Dell Technologies Inc. (U.S.)

- Hewlett-Packard Enterprise Company (U.S.)

- Cisco Systems, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Lenovo (China)

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Advantech Co., Ltd. (Taiwan)

- ADLINK Technology Inc.(Taiwan)

- Schneider Electric SE(France)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Cisco unveiled new AI-ready data center infrastructure and struck deeper integration with NVIDIA, combining networking and compute to help enterprises scale AI workloads across data centers and edge sites.

- May 2025: Dell introduced new Dell AI Factory infrastructure and services, including enhancements for edge and data center systems that support AI workloads from model training to edge inference.

- March 2025: Intel unveiled Intel AI Edge Systems, Edge AI Suites, and Open Edge Platform, providing reference systems and software to simplify the deployment of AI workloads at the edge across sectors such as retail, manufacturing, and smart cities.

- December 2024: Verizon announced a new solution built with NVIDIA that combines Verizon private 5G and Mobile Edge Compute with NVIDIA AI Enterprise and NIM microservices so enterprises can run real-time AI applications on premises at the edge.

- December 2024: Schneider Electric and NVIDIA formed a strategic partnership to co-develop AI-focused data center reference architectures and digital twin-based designs that improve energy efficiency and cooling for high-density AI and edge clusters.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.05% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Hardware Type, Enterprise Type, End-user, and Region |

|

By Hardware Type |

· Edge Servers/Micro Data Centers · Edge Gateways · Industrial PCs/Embedded Edge Devices · Smart Sensors & Edge Nodes · Edge Networking Equipment · Others (Edge AI Accelerators, etc.) |

|

By Enterprise Type |

· Small & Medium Enterprises (SMEs) · Large Enterprises |

|

By End-user |

· Industrial · Security & Surveillance · Automotive · Energy & Utilities · Retail & Commercial · Healthcare · Others (Agriculture, etc.) |

|

By Region |

· North America (By Hardware Type, Enterprise Type, End-user, and Country) o U.S. o Canada o Mexico · South America (By Hardware Type, Enterprise Type, End-user, and Country) o Brazil o Argentina o Rest of South America · Europe (By Hardware Type, Enterprise Type, End-user, and Country) o U.K. o Germany o France o Italy o Spain o Russia o Benelux o Nordics o Rest of Europe · Middle East & Africa (By Hardware Type, Enterprise Type, End-user, and Country) o Turkey o Israel o GCC o North Africa o South Africa o Rest of Middle East & Africa · Asia Pacific (By Hardware Type, Enterprise Type, End-user, and Country) o China o India o Japan o South Korea o ASEAN o Oceania o Rest of Asia Pacific |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 12.65 billion in 2025 and is projected to reach USD 49.38 billion by 2034.

In 2025, the market value stood at USD 4.56 billion.

The market is expected to exhibit a CAGR of 17.7% during the forecast period of 2026-2034.

By end-user, the industrial segment is expected to lead the market.

Rising volume of IoT and video data drives edge hardware deployment.

Dell Technologies Inc., Hewlett-Packard Enterprise Company, Cisco Systems, Inc., Huawei Technologies Co., Ltd., and Lenovo are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us