Electric Vehicle Adhesives Market Size, Share & Industry Analysis, By Type (Structural Adhesives, Sealants & Gasketing, and Thermal Management Materials), By End-Use (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), and Regional Forecast, 2026-2034

Electric Vehicle Adhesives Market Size and Future Outlook

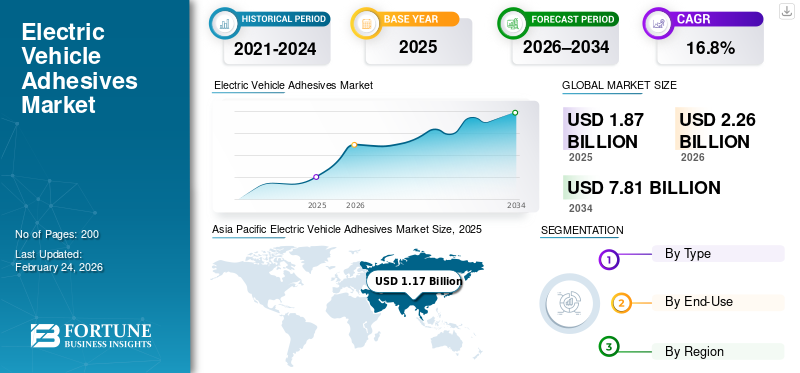

The global electric vehicle adhesives market size was valued at USD 1.87 billion in 2025. The market is projected to grow from USD 2.26 billion in 2026 to USD 7.81 billion by 2034, exhibiting a CAGR of 16.8% during the forecast period. Asia Pacific dominated the electric vehicle adhesives market with a market share of 62.56% in 2025.

The electric vehicle adhesives market is supported by rising demand from EV battery manufacturing and vehicle assembly, where strong, lightweight, and reliable bonding solutions are needed. EV adhesives are specialty materials used to join, seal, and protect components, helping automakers reduce mechanical fasteners, improve structural strength, and manage vibration and noise. They are widely used in battery pack assembly, cell bonding, module and tray sealing, thermal management interfaces, and bonding of lightweight materials. The shift toward higher-volume EV production, larger battery packs, and more advanced vehicle designs is increasing the need for consistent, high-performance adhesive solutions, driving market growth.

Key players in the market include Henkel, 3M, Sika AG, Dow, and BASF, which compete through broad product portfolios, global manufacturing footprints, and reliable supply capabilities to support EV battery assembly, lightweight vehicle bonding, sealing, and thermal management requirements.

Download Free sample to learn more about this report.

ELECTRIC VEHICLE ADHESIVES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.87 billion

- 2026 Market Size: USD 2.26 billion

- 2034 Forecast Market Size: USD 7.81 billion

- CAGR: 16.80% from 2026–2034

- Asia Pacific dominated the electric vehicle adhesives market with a market share of 62.56% in 2025.

- The thermal management materials segment is expected to grow at a CAGR of 17.5% over the forecast period.

- The light commercial vehicles segment is expected to grow at a CAGR of 26.5% over the forecast period.

North America

North America remains an important regional market for EV adhesives, reaching USD 0.24 billion in 2025.

Europe

Europe is expected to record steady growth in the market, reaching an estimated value of USD 0.43 billion in 2025.

Asia Pacific

Asia Pacific holds the dominant position in the market in 2025, valued at USD 1.17 billion, and is expected to maintain its leading role in 2026, reaching USD 1.39 billion.

U.S.

The U.S. market in 2025 stood at USD 0.20 billion, accounting for approximately 85.9% of regional revenues.

Japan

Demand is supported by established automotive manufacturing, growing battery production, and increased use of advanced bonding solutions.

Read More

ELECTRIC VEHICLE ADHESIVES MARKET TRENDS

Rising Shift Toward Multi-Functional Adhesives Systems to Boost Market Growth

A key trend in the electric vehicle adhesives market is the growing shift toward multi-functional, high-performance adhesive systems designed for battery packs and lightweight vehicle structures. EV manufacturers are increasingly looking for adhesives that can do more than bonding, such as providing sealing, vibration control, and support for thermal management in a single solution. This is driving higher demand for advanced chemistries that deliver strong adhesion to mixed materials such as aluminum, composites, and engineered plastics, while maintaining durability under heat, moisture, and repeated charging cycles.

- According to Springer Nature, adhesives play an essential role in EV battery packs for bonding and for electrical protection, sealing, and thermal management, supporting the shift toward multi-functional, higher-performance EV adhesive systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising EV Production and Battery Manufacturing to Drive Electric Vehicle Adhesives Demand

Demand for EV adhesives is strongly driven by the rapid increase in EV production and the scale-up of battery manufacturing, where bonding and sealing materials are essential for safe and durable assembly. EV adhesives are widely used for battery pack assembly, module and tray sealing, cell bonding, and structural joining of lightweight materials as they help improve strength, reduce the need for mechanical fasteners. As automakers expand EV platforms and invest in higher-volume battery pack production, the need for reliable, consistent adhesive solutions across multiple vehicle components continues to rise, which is boosting the electric vehicle adhesives market growth.

- According to the International Energy Agency (IEA), global electric car sales reached around 17 million units in 2024, accounting for more than one-fifth of total car sales worldwide, significantly increasing demand for adhesives used in EV battery packs, structural bonding, and sealing applications.

MARKET RESTRAINTS

High Material Costs and Processing Complexity to Restrain Market Expansion

The market faces restraints due to the relatively high cost of advanced adhesive formulations and the complexity involved in their application and curing processes. Many EV adhesives are engineered to meet strict performance requirements related to heat resistance, electrical insulation, and long-term durability, which often requires specialized raw materials and controlled manufacturing conditions. In addition, the need for precise dispensing equipment, surface preparation, and quality control during battery and vehicle assembly increases operational complexity and manufacturing costs.

- According to Charged EVs, advanced EV battery adhesives require controlled dispensing, curing, and process precision to meet durability, thermal management, and safety requirements in modern battery pack designs. This increases manufacturing complexity and adds to overall production costs for EV manufacturers.

MARKET OPPORTUNITIES

Expanding Advanced Battery Designs and Lightweight EV Platforms to Create New Opportunities

The market presents strong growth opportunities as EV manufacturers move toward advanced battery designs and increasingly lightweight vehicle platforms. New battery architectures, including larger packs and cell-to-pack designs, require higher volumes of adhesives for bonding, sealing, and protection across multiple components. In parallel, the growing use of aluminum, composites, and engineered plastics in EV structures is increasing demand for adhesive solutions that can replace traditional mechanical fastening.

- According to Charged EVs, the shift toward advanced EV battery designs such as cell-to-pack and cell-to-body architectures is increasing reliance on adhesives for structural bonding, thermal management, and safety, as these designs remove traditional modules and parts, making high-performance adhesives critical for durability, efficiency, and next-generation battery assembly.

MARKET CHALLENGES

Volatility in Resin and Polymer Input Costs to Limit Market Stability

The market faces a key challenge in managing cost uncertainty caused by frequent fluctuations in the prices of resins and specialty polymers used in adhesive formulations. Since many of these materials are derived from petrochemical feedstocks, their pricing is highly sensitive to changes in crude oil markets, supply chain disruptions, and shifts in global demand. Sudden increases in raw material costs can compress margins for adhesive manufacturers and create pricing instability for EV producers.

- According to the U.S. Energy Information Administration (EIA), prices of petrochemical feedstocks used to produce resins and polymers closely track crude oil and natural gas market volatility, with supply disruptions and energy price fluctuations directly impacting polymer production costs.

Segmentation Analysis

By Type

Broad Application Across EV Structures and Battery Systems Supports the Dominance of Structural Adhesives

Based on type, the market is segmented into structural adhesives, sealants & gasketing, and thermal management materials.

Structural adhesives hold the largest electric vehicle adhesives market share due to their extensive use in vehicle body assembly and battery pack construction. They are widely applied for bonding body-in-white components, battery enclosures, modules, and lightweight materials such as aluminum and composites, where high strength, durability, and crash resistance are required. Structural adhesives help reduce vehicle weight by replacing mechanical fasteners, improve load distribution, and enhance overall structural integrity.

- According to Vehicle Body Building UK, structural adhesives are increasingly replacing traditional fasteners in vehicle manufacturing because they enable lightweight designs, bond dissimilar materials, and significantly reduce assembly time, supporting their widespread use in modern electric vehicles EV.

To know how our report can help streamline your business, Speak to Analyst

The thermal management materials segment is expected to grow at a CAGR of 17.5% over the forecast period.

By End-Use

High-Volume EV Production Supports Passenger Cars' Dominance

In terms of end-use, the market is categorized into passenger cars, light commercial vehicles, and heavy commercial vehicles.

Passenger cars hold the largest share of the market due to their high production volumes and widespread adoption across global automotive markets. EV adhesives are extensively used in passenger EVs for battery pack assembly, body-in-white bonding, interior components, and lightweight material joining, where strength, safety, and durability are essential. As automakers increasingly standardize EV platforms for mass-market passenger cars, adhesive usage per vehicle continues to rise to support structural integrity, noise and vibration reduction, and thermal management.

- According to the Observatory of Economic Complexity (OEC), Germany is the largest exporter of electric motor vehicles with an exporting value of USD 41.0 billion and a market share of 29.3%.

The light commercial vehicles segment is expected to grow at a CAGR of 26.5% over the forecast period.

Electric Vehicle Adhesives Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Electric Vehicle Adhesives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant position in the market in 2025, valued at USD 1.17 billion, and is expected to maintain its leading role in 2026, reaching USD 1.39 billion. The region’s leadership is supported by strong EV manufacturing activity, large-scale battery production, and a well-established automotive supply chain across major economies. Rapid growth in electric passenger car production, expanding battery gigafactory capacity, and increasing localization of EV components continue to support high consumption of EV adhesives across structural bonding, sealing, and thermal management applications.

China Electric Vehicle Adhesives Market

Based on Asia Pacific’s strong contribution and China’s extensive EV manufacturing base, the China market stood at USD 1.0 billion in 2025, accounting for approximately 88.3% of regional revenues. Demand is driven by large-scale electric passenger car production, battery pack assembly, and the presence of domestic and global EV OEMs. China also benefits from an integrated chemical and materials supply ecosystem, enabling high-volume production and widespread use of structural and functional adhesives across EV platforms.

To know how our report can help streamline your business, Speak to Analyst

India Electric Vehicle Adhesives Market

The India market in 2025 reached around USD 0.03 billion. Demand is supported by the gradual expansion of domestic EV manufacturing, rising investments in battery assembly, and increasing adoption of electric two-wheelers and passenger cars. Government support for EV localization, coupled with growth in automotive component manufacturing and lightweight material usage, continues to drive steady adoption of EV adhesives across emerging EV platforms in the country.

North America

North America remains an important regional market for EV adhesives, reaching USD 0.24 billion in 2025. Demand is supported by strong EV adoption, ongoing investments in battery manufacturing, and advanced automotive production across the region. The presence of established OEMs, battery developers, and a mature chemicals and materials industry supports consistent demand for structural, sealing, and thermal management adhesives. In addition, focus on lightweight vehicle type, safety standards, and domestic EV supply chains continues to reinforce adhesive usage across passenger and commercial EV platforms.

U.S. Electric Vehicle Adhesives Market

The U.S. market in 2025 stood at USD 0.20 billion, accounting for approximately 85.9% of regional revenues. Demand is driven by large-scale electric passenger car production, expanding battery pack and gigafactory investments, and strong adoption of advanced vehicle assembly technologies. The presence of leading adhesive manufacturers, automotive OEMs, and battery technology companies further supports steady consumption of EV adhesives across structural bonding, battery assembly, and thermal interface applications in the U.S. market.

Europe

Europe is expected to record steady growth in the market, reaching an estimated value of USD 0.43 billion in 2025. The region is shaped by strong EV adoption targets, strict emissions regulations, and a clear shift toward sustainable and lightweight vehicle technologies. Demand is supported by established automotive manufacturing, growing battery production, and increased use of advanced bonding solutions to meet safety, efficiency, and recyclability requirements across the EV market.

Germany Electric Vehicle Adhesives Market

Germany’s market reached approximately USD 0.077 billion in 2025, accounting for around 18.2% of regional demand. Consumption is supported by high electric passenger car production, strong presence of global OEMs, and advanced engineering practices that rely on structural adhesives for lightweight body structures and battery pack assembly.

Italy Electric Vehicle Adhesives Market

The Italy market in 2025 stood at USD 0.016 billion, representing roughly 3.8% of regional revenues. Demand is driven by growing EV manufacturing, increasing adoption of electric passenger vehicles, and continued use of adhesive solutions in battery systems, interiors, and lightweight structural applications across the automotive value chain.

Latin America and Middle East and Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in the market during the forecast period. The Latin America market reached USD 0.018 billion in 2025, supported by gradual growth in EV adoption, expanding automotive component manufacturing, and early-stage investments in EV batteries assembly and charging infrastructure. The Middle East & Africa market reached USD 0.013 billion in 2025, driven by emerging EV programs, industrial diversification efforts, and increasing focus on localized vehicle assembly and lightweight automotive materials.

Brazil Electric Vehicle Adhesives Market

The Brazil market in 2025 is estimated at around USD 0.013 billion, accounting for approximately 72.0% of Latin America revenues. Demand is supported by strong automotive manufacturing and assembly activity, increasing adoption of electric and hybrid passenger vehicles, and rising use of adhesives in vehicle body structures, lightweight components, and battery-related applications.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity to Shape Competition in the Market

The market is relatively consolidated and capital-intensive, as large-scale participation depends on access to advanced formulation capabilities, specialized production equipment, and stringent quality and regulatory compliance systems. Significant upfront investment in R&D, manufacturing, application testing, and global supply infrastructure, along with long qualification and validation cycles with automotive OEMs, limits the entry of new players.

Major companies such as Henkel, 3M, Sika AG, Dow, and BASF primarily focus on improving operational efficiency, strengthening supply chain reliability, and enhancing product performance and consistency, rather than pursuing aggressive capacity expansion, as OEM approvals and long-term supply agreements remain key competitive factors in the market.

LIST OF KEY ELECTRIC VEHICLE ADHESIVES COMPANIES PROFILED

- Henkel (Germany)

- 3M (U.S.)

- Sika AG (Switzerland)

- B. Fuller Company. (U.S.)

- Arkema (France)

- Dow (U.S.)

- DuPont (U.S.)

- BASF (Germany)

- Huntsman International LLC. (U.S.)

- PPG Industries, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: BASF co-developed and unveiled a solid-state battery pack concept with Welion, highlighting new battery-pack integration approaches where bonding, sealing, and pack materials performance are critical.

- November 2025: Henkel introduced new LOCTITE thermal potting solutions aimed at protecting and improving the reliability of EV components, strengthening its e-mobility adhesives and encapsulation portfolio.

- September 2025: Huntsman launched a new range of ARALDITE epoxy adhesive solutions positioned around improved safety/sustainability and performance for demanding industrial bonding applications relevant to transportation electrification supply chains.

- May 2024: Dow started commercial operations of an adhesive and gap-filler production line in Ahlen, Germany, explicitly positioned to support growth in battery assembly solutions for the e-mobility

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The electric vehicle adhesives market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.8% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, End-Use, and Region |

| By Type |

|

| By End-Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.87 billion in 2025 and is projected to reach USD 7.81 billion by 2034.

Recording a CAGR of 16.8%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

By end-use, the passenger cars segment leads the market.

Asia Pacific holds the highest market share.

Rising EV production and battery manufacturing demand for structural bonding, sealing, and thermal management adhesives is the key factor driving the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us