EV Battery Materials Market Size, Share & Industry Analysis, By Material (Anode Material, Cathode Material, Separator, Electrolyte, and Others), By End-use (Passenger Vehicles, Commercial Vehicles, and Others), and Regional Forecast, 2026-2034

EV BATTERY MATERIALS MARKET SIZE AND FUTURE OUTLOOK

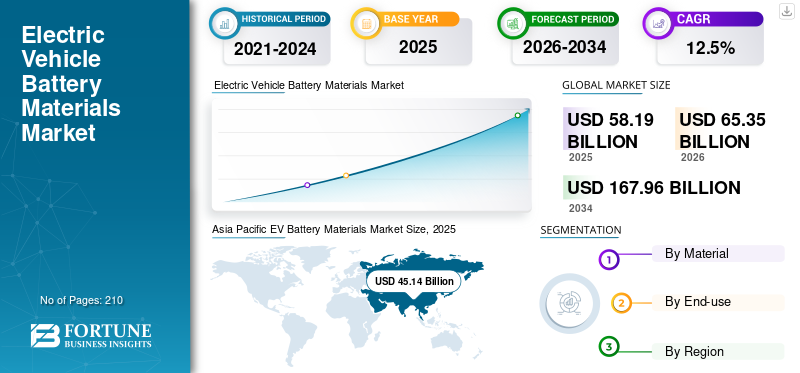

The global EV battery materials market size was valued at USD 58.19 billion in 2025. The market is projected to grow from USD 65.35 billion in 2026 to USD 167.96 billion by 2034, exhibiting a CAGR of 12.5% during the forecast period. Asia Pacific dominated the EV battery materials market with a market share of 77.57% in 2025.

EV battery materials are the key raw, processed, and engineered materials used to manufacture rechargeable batteries for electric vehicles, including cathode materials, anode materials, separators, electrolytes, and supporting cell materials such as binders, additives, current collectors, and packaging components. These materials directly influence battery energy density, safety, charging performance, lifecycle, and overall vehicle cost. A major demand driver is the rapid expansion of electric vehicle production, supported by stricter emission norms, government incentives, automaker electrification strategies, and consumer shift toward low-carbon mobility. As EV adoption rises globally, battery cell manufacturing expands, directly increasing the consumption of battery materials. CNGR Advanced Material, Huayou Cobalt, POSCO Future M, LG Chem, and Umicore are the key players operating in the market.

Download Free sample to learn more about this report.

EV Battery Materials Market Key Takeaways

- 2025 Market Size: USD 58.19 billion

- 2026 Market Size: USD 65.35 billion

- 2034 Forecast Market Size: USD 167.96 billion

- CAGR: 12.5% from 2026–2034

- Asia Pacific dominated the EV battery materials market with a 77.57% share in 2025.

- The Passenger Vehicles segment is anticipated to hold the dominant market share.

- The Electrolytes segment is projected to grow at the highest CAGR of 13.1% during the forecast period.

Asia Pacific

Strong battery manufacturing ecosystems continue to drive regional market leadership.

North America

Expanding domestic battery manufacturing is accelerating demand for battery materials.

Europe

Localized battery production and decarbonization initiatives support material demand growth.

U.S.

The market reached approximately USD 6.66 billion in 2025, accounting for 11.4% of global sales.

Japan

The market reached approximately USD 1.16 billion in 2025, representing around 2.0% of global sales.

Read More

EV BATTERY MATERIALS MARKET TRENDS

Cost-Efficient Chemistries to Reshape Battery Material Demand

A major global trend in the market is the shift toward lower-cost, safer, and less mineral-intensive battery chemistries. Automakers and cell manufacturers are increasingly adopting chemistries that reduce dependence on expensive or supply-sensitive metals while maintaining acceptable driving range and safety. This is reshaping demand across cathode materials, anode materials, electrolytes, and separators. Material suppliers are responding by diversifying product portfolios, investing in chemistry-specific production lines, and improving performance at lower cost. The trend is also changing value pools, as the material demand shifts from premium high-metal-content chemistries toward more cost-competitive alternatives.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising EV Production Accelerates Battery Material Consumption to Drive Market Growth

The strongest demand driver for market growth is the continued expansion of electric vehicle production globally. As automakers scale EV platforms across passenger cars, commercial vehicles, and fleet applications, the demand increases for cathode materials, anode materials, separators, electrolytes, and other supporting cell materials. Government electrification policies, emission reduction targets, charging infrastructure expansion, and the consumer acceptance of EVs are reinforcing this growth. Battery material consumption is directly tied to battery cell manufacturing. Hence, every increase in EV output creates incremental demand across the material value chain. This makes vehicle electrification the central factor driving long term EV battery materials market growth.

MARKET RESTRAINTS

Material Price Volatility May Create Margin and Planning Risk

A key restraint for market expansion is volatility in raw material and processed chemical prices. Materials such as lithium, nickel, cobalt, graphite, and electrolyte inputs are exposed to changing supply-demand balances, geopolitical risk, inventory cycles, and investment timing. Sharp price movements create uncertainty for material suppliers, battery manufacturers, and automakers. High prices can pressure battery costs and slow affordability gains, while sudden price declines can weaken supplier margins and delay upstream investments. This volatility makes long term contracting, capacity planning, and procurement strategy more complex across the EV battery materials value chain.

MARKET OPPORTUNITIES

Supply Chain Localization and Recycling to Create New Market Growth Opportunities

A major opportunity is the localization of EV battery material supply chains and the growth of battery recycling. Automakers, cell manufacturers, and governments are seeking more secure, regional, and traceable supply networks to reduce dependence on concentrated sourcing hubs. This creates opportunities for new investments in battery materials and refining capacity across emerging battery clusters. At the same time, recycling can recover valuable materials from production scrap and end-of-life batteries, creating a secondary supply stream. Together, localization and circularity can improve resilience, reduce environmental impact, and open new revenue pools for material suppliers.

MARKET CHALLENGES

Supply Chain Concentration to Constrain Market Growth

A major challenge is the high concentration of battery material production and processing in a limited number of countries and companies. Established suppliers benefit from scale, mature battery technology, integrated supply chains, customer qualifications, and cost effectiveness. New entrants in other regions often face high capital requirements, long permitting timelines, technical know-how barriers, and the need to qualify with major battery manufacturers. Even when governments support domestic battery ecosystems, building competitive material capacity takes time. As a result, supply chain diversification is strategically important but commercially difficult, especially in cost-sensitive battery segments where buyers prioritize reliability, quality, and price.

SEGMENTATION ANALYSIS

By Material

Rising Need for Higher Energy Density Chemistries to Drive Cathode Material Segment

Based on material, the market is segmented into anode material, cathode material, separator, electrolyte, and others.

The cathode material segment is anticipated to hold the dominant EV battery materials market share during the forecast period. The material demand is being driven by the need to improve EV range, battery performance, and cost competitiveness. As automakers scale electric models across mass-market and premium segments, they require cathode chemistries that balance energy density, safety, lifecycle, and affordability. This is increasing the demand for both nickel-rich cathodes used in long range vehicles and cost-efficient alternatives used in mainstream EVs. Since cathodes strongly influence battery cost and performance, they remain a central focus of material innovation and procurement strategy.

The electrolytes segment is anticipated to rise at a CAGR of 13.1% over the forecast period. The demand for electrolytes is being driven by the industry’s push for faster charging, improved safety, and longer battery life. As EV users expect shorter charging times and high performance across different climates, battery manufacturers need advanced electrolyte formulations that enhance ion transport, thermal stability, and cycle life. Electrolytes also play a critical role in supporting new battery chemistries and higher-voltage systems. This makes electrolyte innovation increasingly important as automakers compete on charging speed, durability, and overall battery performance.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Mass EV Adoption Drives Battery Material Demand in Passenger Vehicles Segment

Based on the end-use, the market is segmented into passenger vehicles, commercial vehicles, and others.

The passenger vehicles segment is anticipated to hold the dominant EV battery materials market share during the forecast period. The material demand in these vehicles is being driven by the rapid shift from internal combustion vehicles to electric cars, SUVs, and crossovers. Automakers are expanding EV model portfolios across premium and mass-market price points, increasing battery cell requirements at scale. The consumer demand for longer driving range, faster charging, and improved vehicle affordability is pushing higher material consumption and battery chemistry innovation. As passenger vehicles represent the largest EV production base, they remain the primary demand engine for battery materials.

The commercial vehicles segment is anticipated to rise at a CAGR of 15.1% over the forecast period. The demand for EV battery materials in commercial vehicles is being driven by fleet electrification across delivery vans, buses, and medium- and heavy-duty trucks. Logistics companies, public transport operators, and corporate fleets are adopting EVs to reduce operating costs, meet emission targets, and comply with urban clean-mobility regulations. Commercial EVs typically require larger and more durable battery packs than passenger cars, increasing material intensity per vehicle. As fleet operators scale electrification, commercial vehicles are becoming a high-growth demand pool for battery materials.

EV BATTERY MATERIALS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific EV Battery Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounts for the largest market share and is expected to maintain its dominance during the forecast period. In this region, the main demand driver is the region’s dominant position in EV battery manufacturing. China, South Korea, and Japan already have mature battery ecosystems, while India and Southeast Asia are emerging as new manufacturing hubs. This creates large and sustained demand for battery and supporting cell materials. Asia Pacific also benefits from integrated supply chains, strong cell manufacturing expertise, and proximity to key battery-material processors. Both domestic EV demand and export-oriented battery production are anticipated to support the regional market growth.

Japan EV Battery Materials Market

The Japan market reached approximately USD 1.16 billion in 2025, equivalent to around 2.0% of the global sales.

China EV Battery Materials Market

The China market is projected to be one of the largest markets worldwide. The 2025 market revenues in this country stood at around USD 39.34 billion, representing roughly 67.6% of global sales.

India EV Battery Materials Market

The India market is projected to reach approximately USD 0.94 billion in 2025, equivalent to around 1.6% of the global sales.

North America

In North America, the product demand is being driven by the rapid localization of battery manufacturing. Automakers and cell producers are investing in regional battery plants to reduce import dependence, improve supply security, and qualify for policy-linked incentives. As battery cell capacity expands, the product demand will rise in parallel, driving market growth.

U.S. EV Battery Materials Market

The U.S. market can be analytically approximated at around USD 6.66 billion in 2025, accounting for roughly 11.4% of the global sales.

Europe

In Europe, the product demand is being driven by the region’s strong decarbonization agenda and the push to build a localized battery supply chain. European automakers are accelerating EV production to meet emission targets, while governments are supporting domestic battery manufacturing to reduce reliance on imported cells and materials. This is expected to increase the product demand.

Poland EV Battery Materials Market

The Poland market reached approximately USD 2.37 billion in 2025, equivalent to around 4.1% of the global sales.

Germany EV Battery Materials Market

The Germany market reached approximately USD 0.73 billion in 2025, equivalent to around 1.3% of global sales.

Rest of the World

In the rest of world, the product demand is being driven by the emergence of new battery manufacturing hubs in countries such as Morocco and Brazil. These markets are attracting investment due to proximity to automotive export markets, access to raw materials, improving industrial policy support, and growing EV assembly activity. As local battery production develops, the demand will rise for battery materials. Although the current base is small, future growth is anticipated to be strong as supply chains diversify beyond established regions.

Brazil EV Battery Materials Market

The Brazil market reached approximately USD 0.15 billion in 2025, equivalent to around 0.3% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on Long-term Offtake Agreements for a Strong Foothold

The global EV battery materials industry is highly competitive but remains concentrated across Asia, particularly China, South Korea, and Japan, due to their strong battery manufacturing ecosystems, integrated supply chains, and scale advantages. Competition is shaped by access to critical minerals, cathode and anode technology, customer qualification with cell manufacturers, regional localization, pricing pressure, and recycling capability. Suppliers are increasingly expanding into higher-value materials, securing long-term offtake agreements, and building regional production footprints near battery giga factories. Key producers include CNGR Advanced Material, Huayou Cobalt, POSCO Future M, LG Chem, and Umicore, among others.

LIST OF KEY EV BATTERY MATERIALS COMPANIES PROFILED

- Arkema (France)

- BASF SE (Germany)

- CNGR Advanced Material Co., Ltd (China)

- Huayou Cobalt Co., Ltd. (China)

- LG Chem (South Korea)

- Mitsubishi Chemical Group Corporation (Japan)

- NICHIA CORPORATION (Japan)

- POSCO FUTURE M (South Korea)

- UBE Corporation (Japan)

- Umicore (Belgium)

KEY INDUSTRY DEVELOPMENTS

- March 2026: POSCO Future M, Kumho Petrochemical, and BEI signed an MoU for jointly developing anode-free lithium metal battery technology, targeting 30–50% higher energy density and faster charging than conventional lithium-ion batteries. The collaboration will combine POSCO Future M’s cathode expertise, Kumho Petrochemical’s high-performance CNT technology, and BEI’s cell manufacturing capabilities, with commercialization opportunities in drones, robotics, advanced air mobility, and high-performance EVs.

- March 2026: Arkema announced a 20% expansion of Kynar® PVDF production capacity at its Changshu site in China, scheduled to start up in 2028. The investment supports the rising Asia Pacific demand across EV batteries, energy storage, coatings, semiconductors, water filtration, and wire & cable. Backed by Arkema’s global R&D network, the project strengthens supply reliability, innovation capabilities, and the company’s leadership in advanced PVDF applications.

- December 2025: POSCO Future M signed a joint venture agreement with CNGR and its Korean subsidiary FINO to advance its LFP cathode materials business. The company plans to build a plant at Pohang’s Yeongil Bay General Industrial Complex 4, targeting groundbreaking in 2026 and mass production in 2027. The annual capacity may expand to 50,000 tons, supporting the rising ESS and entry-level EV demand.

- August 2025: BASF Battery Materials, through BASF Shanshan Battery Materials, delivered its first mass-produced cathode active materials for semi-solid-state batteries in collaboration with Beijing WELION New Energy. The ultra-high nickel NCM material with composite coating improves energy density, cycling performance, and battery life. The milestone supports the commercialization and industrialization of safer, high-performance next-generation solid-state battery technologies.

- March 2024: CNGR and Doosan Recycling Solution, a Doosan Enerbility subsidiary, signed a cooperation agreement in Frankfurt to collaborate on lithium extraction from battery black mass. The partnership aims to establish a stable long-term off-take arrangement, combining Doosan’s high-efficiency lithium recovery technology with CNGR’s global recycling network to strengthen circular battery material use, support regulatory compliance, and promote sustainable development across the battery value chain.

- September 2023: LG Chem partnered with Huayou Cobalt to establish an EV battery materials joint venture in Morocco. The facility, expected to start operations in 2026, will produce 50,000 metric tons of lithium iron phosphate cathode materials annually for the North American market. LG Chem also plans lithium conversion capacity in Morocco and a precursor plant in Indonesia to strengthen its global battery materials supply chain.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading end-uses of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 12.5% during 2026-2034 |

| Segmentation | By Material, By End-use, and By Region |

| By Material |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 58.19 billion in 2025 and is projected to record a valuation of USD 167.96 billion by 2034.

In 2025, Asia Pacific market stood at a value of USD 45.14 billion.

The market will exhibit steady growth at a CAGR of 12.5% during the forecast period of 2026-2034.

By end-use, the passenger vehicles segment is expected to lead this market during the forecast period.

Rising electric vehicle production accelerates battery material consumption, driving the market growth.

CNGR Advanced Material, Huayou Cobalt, POSCO Future M, LG Chem, and Umicore are the major players operating in the market.

Asia Pacific dominates the market in terms of share.

The rising EV adoption accelerates battery manufacturing, driving the product demand worldwide.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us