Electric Vehicle (EV) Taxi Market Size, Share & Industry Analysis, By Operating Model (Ride-Hailing / App-Based Platforms, Traditional Street-Hail / Dispatch Taxi, and Corporate / Institutional Contract Mobility), By Vehicle Type (Hatchbacks & Compact Cars, Sedans, and SUVs, MPVs & Vans), By Ownership Structure (Fleet-Owned (Company-Owned Fleet), Driver-Owned / Owner-Operator, and Leased / Subscription-Based Models), By Vehicle Range (Up to 250 km Range, 251-400 km Range, and Above 400 km Range), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

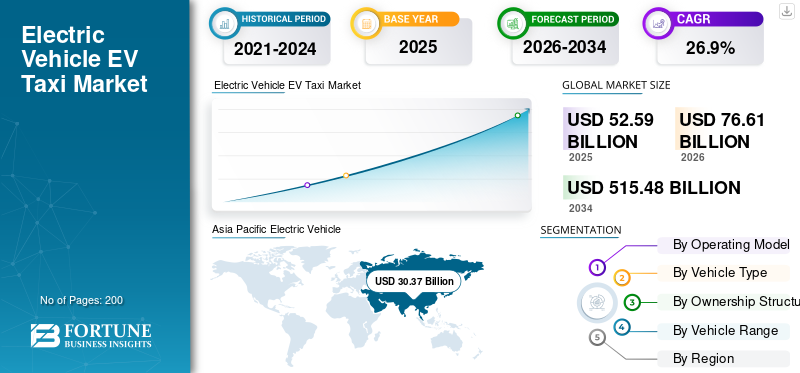

Electric Vehicle (EV) Taxi Market Size and Future Outlook

The global Electric Vehicle (EV) taxi market size was valued at USD 52.59 billion in 2025. The market is projected to grow from USD 76.61 billion in 2026 to USD 515.48 billion by 2034, with a CAGR of 26.9% over the forecast period. Asia Pacific dominated the electric vehicle taxi market with a market share of 57.75% in 2025.

An Electric Vehicle (EV) taxi is a battery-powered taxi used for passenger transport via ride-hailing apps, street hail, dispatch, or contracted services. It runs on electricity instead of petrol or diesel, offers lower operating and maintenance costs, and produces zero tailpipe emissions. Key drivers include stricter urban emission rules, government incentives, and rising fuel costs that improve EV total cost of ownership for high-mileage taxis. Expanding fast-charging networks, improving battery range, and lowering EV prices also support adoption. Ride hailing platforms and fleet operators accelerate electrification to meet sustainability targets and secure long-term cost effective.

Major players include OEMs supplying fleet-ready EVs (e.g., BYD, Tesla, SAIC/MG, Geely, Hyundai-Kia, Tata) and mobility platforms (Uber, DiDi, and Grab). Trends include bulk fleet procurement, growth in leasing/subscription models, the rollout of depot fast charging, a shift toward SUVs/MPVs and longer-range models, and tighter platform-led EV targets.

Download Free sample to learn more about this report.

Electric Vehicle (EV) Taxi Market Key Takeaways

- 2025 Market Size: USD 52.59 billion

- 2026 Market Size: USD 76.61 billion

- 2034 Forecast Market Size: USD 515.48 billion

- CAGR: 26.9% from 2026–2034

- Asia Pacific dominated the electric vehicle taxi market with a 57.75% share in 2025.

- The SUVs, MPVs & vans segment is projected to grow at the fastest CAGR of 35.0% during the forecast period.

- The leased/subscription-based models segment is anticipated to expand at a CAGR of 30.1% over the study period.

Asia Pacific

Asia Pacific led the global market in 2025, supported by large-scale EV production, strong charging infrastructure, and rapid ride-hailing electrification initiatives.

North America

North America is experiencing steady market expansion due to strong ride-hailing penetration, government EV incentives, and increasing adoption of leasing models for drivers.

Europe

Europe remains a key growth region, driven by stringent emission regulations, expanding zero-emission zones, and increasing electrification of urban taxi fleets.

U.S.

The U.S. market is witnessing rising EV taxi adoption supported by fleet partnerships, urban sustainability initiatives, and expanding fast-charging infrastructure.

Japan

Japan’s electric vehicle taxi market was valued at USD 2.00 billion in 2025, supported by fleet modernization initiatives and expanding public charging infrastructure.

Read More

ELECTRIC VEHICLE (EV) TAXI MARKET TRENDS

Platform-Led Fleet Electrification Accelerates EV Taxi Adoption

Ride-hailing platforms are increasingly shaping the pace of electric vehicle taxi deployment by setting electrification targets and influencing driver vehicle choices. As app-based fleets operate at high daily mileage, EVs deliver strong fuel and maintenance savings, making them economically attractive for platform partners. This platform-led push also standardizes vehicle requirements, encourages bulk procurement, and stimulates charging partnerships. As more cities introduce zero-emission zones, digital platforms become central coordinators of fleet transition, aggregating demand and accelerating EV penetration faster than fragmented traditional taxi industry. The trend reflects a structural shift in which mobility companies actively guide vehicle technology choices rather than remain neutral intermediaries.

- In September 2020, Uber announced a commitment to become a zero-emission mobility platform in the U.S., Canada, and Europe by 2030, requiring a full transition of its vehicles to electric.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Strengthening Urban Emission Regulations Drive EV Taxi Deployment

Urban air-quality mandates and carbon-reduction policies are significantly influencing taxi electrification. Governments are introducing zero-emission zones, stricter vehicle standards, and incentives that favor electric fleets over internal combustion vehicles. Taxis, due to their high visibility and high mileage, are often prioritized in regulatory frameworks. Electrifying taxi fleets delivers disproportionately reduced carbon emissions compared to private vehicles as taxis operate for longer daily hours. Regulatory clarity also reduces uncertainty for fleet investors and encourages infrastructure expansion. As cities intensify climate commitments, electric vehicle taxis become a practical and symbolic step toward cleaner urban and consumer preference for ecofriendly transport systems.

- In October 2021, London introduced stricter Ultra Low Emission Zone (ULEZ) standards, affecting taxis and private hire vehicles operating in the city.

MARKET RESTRAINTS

High Upfront Vehicle and Infrastructure Costs Restrain Rapid Scale-Up

Although operating costs are lower, EV taxis require a higher initial investment than conventional vehicles. Battery-electric vehicles and Plug in Hybrid Electric Vehicles (PHEVs) typically have higher purchase prices, and fleet operators must also invest in charging infrastructure or secure reliable public charging access. For independent drivers, access to financing remains a barrier in many markets. Infrastructure gaps can reduce operational flexibility, particularly in regions with limited fast-charging coverage. These financial constraints slow adoption in price-sensitive or emerging economies despite strong long-term savings potential. The mismatch between short-term capital burden and long-term benefits remains a structural restraint in the global Electric Vehicle (EV) taxi market growth.

MARKET OPPORTUNITIES

Expansion into Emerging Markets Creates Significant Growth Opportunities

Emerging markets in Southeast Asia, Latin America, the Middle East, and parts of Africa present substantial opportunities for market growth. Rapid urbanization, growing ride-hailing penetration, advances in hybrid electric vehicles PHEVs and increasing smartphone adoption create favorable conditions for electrified mobility services. As battery costs decline and affordable EV models expand, fleet operators in these regions can bypass legacy combustion-dominated transitions and adopt electric platforms directly. International climate financing and development bank support for clean transport infrastructure further strengthens this opportunity. Scaling electric vehicle taxis in high-density cities within emerging economies can significantly reduce urban emissions while modernizing mobility services.

- In December 2025, Germany’s national taxi association (Bundesverband Taxi und Mietwagen e.V.) partnered with SMART/LAB to support fleet electrification, focusing on practical needs such as charging access, billing systems, and everyday operational integration. This type of industry-IT collaboration is critical for EV taxi deployment beyond early adopters and into broader operator bases.

MARKET CHALLENGES

Charging Infrastructure Reliability and Grid Capacity Pose Operational Challenges

Reliable charging access is critical for electric vehicle taxi operations, especially for vehicles operating multiple shifts per day. Insufficient availability of fast charging can reduce vehicle uptime and affect driver earnings. In addition, large-scale fleet electrification increases electricity demand, placing pressure on local grid capacity and distribution systems. Coordinating depot charging schedules, avoiding peak tariffs, and ensuring grid resilience require planning and investment. Without synchronized infrastructure and energy planning, fleet expansion may outpace charging readiness, limiting operational efficiency and slowing broader EV taxi adoption in certain regions.

Segmentation Analysis

By Operating Model

Platform-Led Electrification Expands Ride-Hailing Segment Leadership

Based on operating model, the market is segmented into ride-hailing/app-based platforms, traditional street-hail/dispatch taxi, and corporate/institutional contract mobility.

Ride-hailing/app-based platforms dominate the global Electric Vehicle (EV) taxi market share due to high vehicle utilization, centralized fleet coordination, and faster electrification targets set by mobility platforms. Digital platforms aggregate demand, enable bulk EV procurement, and partner with charging providers, accelerating adoption compared to fragmented traditional taxi systems.

The corporate / institutional contract mobility segment is projected to grow at a 28.3% CAGR over the forecast period, driven by corporate sustainability commitments and fleet decarbonization goals.

- In April 2022, Uber launched the expansion of “Uber Green” across multiple global cities to increase electric ride options on its platform.

By Vehicle Type

Affordable Urban Mobility Solutions Strengthen Hatchback & Compact Segment Dominance

Based on vehicle type, the market is segmented into hatchbacks & compact cars, sedans, and SUVs, MPVs & vans.

Hatchbacks & compact cars dominate the market due to lower acquisition costs, high energy efficiency, and suitability for dense urban environments. These vehicles offer lower total cost of ownership and easier maneuverability in congested cities, making them preferred choices for high-frequency ride-hailing operations, transportation solutions especially in the Asia Pacific and emerging markets.

The SUVs, MPVs & vans segment is projected to grow at a CAGR of 35.0% over the forecast period, supported by rising demand for premium rides and airport transfers.

- In January 2023, BYD announced expanded deliveries of its Dolphin compact EV to fleet operators in multiple Asian markets.

To know how our report can help streamline your business, Speak to Analyst

By Ownership Structure

Centralized Fleet Operations Enhance Fleet-Owned Segment Expansion

Based on ownership structure, the market is segmented into fleet-owned (company-owned fleet), driver-owned/owner-operator, and leased/subscription-based models.

Fleet-Owned (company-owned fleet) dominates the market as large operators can finance vehicles in bulk, negotiate charging partnerships, and optimize maintenance operations. Centralized fleet management reduces downtime and improves vehicle lifecycle efficiency, which is critical for high-mileage EV taxi operations.

The leased / subscription-based models segment is projected to grow at a 30.1% CAGR over the forecast period, driven by flexible financing solutions for independent drivers transitioning to EVs.

- In March 2023, Hertz announced plans to expand its EV fleet available for ride-hailing drivers through partnerships with Uber.

By Vehicle Range

Balanced Performance and Operational Efficiency Support Mid-Range EV Adoption

Based on vehicle range, the market is segmented into up to 250 km range, 251-400 km range, and above 400 km range.

The 251-400 km range segment dominates the market as it balances affordability and sufficient driving range for daily urban duty cycles. This range band minimizes charging interruptions while avoiding the higher costs associated with long-range batteries.

The above 400 km range segment is projected to grow at a CAGR of 33.5% over the forecast period, supported by expanding intercity and premium ride services.

- In August 2023, Hyundai introduced upgraded battery options for its Kona Electric, with extended-range configurations targeting fleet applications.

ELECTRIC VEHICLE (EV) TAXI MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Electric Vehicle (EV) Taxi Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market, primarily due to China’s large EV production scale and rapid fleet electrification. High urban density, strong ride-hailing penetration, and competitive EV pricing accelerate adoption. Governments in several countries provide incentives and industrial support for EV manufacturing. India and Southeast Asia are emerging growth markets as affordable EV models expand. The region is also witnessing rapid growth in higher-end and fleet-owned EV taxis, reflecting improving battery performance and professional fleet management.

China Electric Vehicle (EV) Taxi Market

China led the market with share of 70.6% in 2025, globally in electric vehicle taxi deployment, supported by large-scale EV production, municipal electrification mandates, and platform-driven ride-hailing growth. Many cities prioritize electric public transport fleets. Competitive domestic EV pricing and strong charging infrastructure density enable rapid scaling of taxi electrification across urban centers.

Japan Electric Vehicle (EV) Taxi Market

Japan’s adoption of electric vehicle taxis is steady but moderate. Technological advancements, government carbon-neutral targets, and fleet modernization initiatives support growth. Urban taxi operators are gradually transitioning to electric models, particularly in metropolitan areas, as public charging infrastructure expands. Japan was valued at USD 2.00 billion in 2025.

India Electric Vehicle (EV) Taxi Market

India represents one of the fastest-growing markets with CAGR of 31.6% during the forecast period. Ride-hailing demand, cost-sensitive compact EV models, and supportive state-level policies are key drivers. Government incentive schemes and fleet financing models are encouraging the adoption of electric vehicles among commercial operators in major cities.

North America

North America’s market is expanding steadily, supported by strong ride-hailing penetration, federal and state EV incentives, and improving fast-charging infrastructure. Fleet partnerships, corporate sustainability commitments, and urban zero-emission initiatives strengthen adoption. Growth is also supported by leasing models that reduce upfront vehicle costs for drivers. Canada shows moderate but stable expansion driven by clean-transport policies, while Mexico represents an emerging growth pocket as affordable EV options increase and charging infrastructure gradually expands.

U.S. Electric Vehicle (EV) Taxi Market

The U.S. led North America with a valuation of USD 5.46 billion in 2025, due to its large ride-hailing ecosystem and expanding EV supply. Major mobility platforms promote electric transitions, while federal tax credits and state-level incentives improve fleet economics. Urban sustainability mandates and corporate ESG targets also accelerate adoption. High vehicle utilization in app-based fleets enhances total cost of ownership benefits.

Europe

Europe market benefits from stringent emission regulations, expanding zero-emission zones, and strong EV supply chains. Urban air-quality standards in major cities are accelerating the electrification of taxi fleets. Balanced adoption across ride-hailing and traditional regulated taxi systems characterizes the region. The shift toward longer-range EVs supports extended duty cycles. Western Europe leads growth, while Central and Eastern Europe are gradually increasing penetration as EV affordability improves and charging infrastructure becomes more widespread.

U.K. Electric Vehicle (EV) Taxi Market

The U.K. market value of USD 2.38 billion in 2025, was driven by London’s emission standards and national decarburization targets. Electric taxis are increasingly adopted within regulated fleets, supported by government grants and charging expansion. Ride-hailing electrification targets also contribute. Strong policy clarity and urban clean-air initiatives make the U.K. one of Europe’s leading adopters of EV taxis.

Germany Electric Vehicle (EV) Taxi Market

Strong domestic EV manufacturing and government incentives support Germany’s growth. Municipal sustainability programs and corporate fleet electrification strategies are boosting demand. Ride-hailing services and airport transfer fleets are gradually transitioning to EVs, while improvements in long-range battery models enhance operational viability for high-mileage taxi services. Germany contributed share of 20.9% in 2025.

Rest of the World

The rest of the world region shows gradual but accelerating electric vehicle taxi adoption, particularly in Middle Eastern and Latin American metropolitan areas. Growth is supported by rising urbanization, expanding ride-hailing platforms, and falling battery costs. However, infrastructure gaps and financing challenges remain constraints. Countries with strong renewable energy capacity and government clean mobility strategies are expected to lead electrification within this region over the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Fleet Electrification Strategies, Platform Integration, and Charging Partnerships Define EV Taxi Competitiveness

The global market trends are shaped by large-scale fleet electrification, strong collaboration between OEMs and mobility platforms, and the development of an integrated charging ecosystem. Leading vehicle manufacturers such as BYD, Tesla, SAIC, Hyundai, Kia, Tata Motors, and Geely compete by offering high-range, fleet-optimized EV models with lower total cost of ownership and fast-charging capability. Mobility platforms, including Uber, DiDi, Grab, and Lyft, influence competitiveness by setting electrification targets, facilitating bulk procurement, and integrating EV-focused incentives for drivers. Companies strengthen market positioning by improving battery technology, adopting subscription-based fleet models, and partnering with charging network operators to ensure high vehicle uptime. Strategic alliances among automakers, leasing firms, and energy providers are increasingly critical to reducing upfront costs and expanding access to infrastructure. Competitive differentiation is increasingly based on vehicle range efficiency, lifecycle cost optimization, charging accessibility, and the ability to scale electrified fleets across major urban markets.

LIST OF KEY ELECTRIC VEHICLE (EV) TAXI COMPANIES PROFILED IN REPORT

- BYD Company Ltd. (China)

- Tesla, Inc. (U.S.)

- SAIC Motor Corporation Ltd. (MG Motor) (China)

- Geely Auto Group (China)

- BAIC Group (China)

- Tata Motors Ltd. (India)

- Hyundai Motor Company (South Korea)

- DiDi Global Inc. (China)

- Grab Holdings Ltd. (Singapore)

- Lyft, Inc. (U.S.)

- Toyota Motor Corporation (Japan)

- Volkswagen AG (Germany)

- BMW Group (Germany)

- Mercedes-Benz Group AG (Germany)

- Stellantis N.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The Federal Airports Authority of Nigeria (FAAN) partnered with a private firm to deploy electric vehicle taxis across Nigerian airports. The initiative supports airport decarbonization goals, introduces zero-emission ground transport services, and marks a significant step toward electrifying high-visibility, high-frequency commercial passenger transport hubs in the country.

- February 2026: Octopus Electroverse partnered with Freenow by Lyft to offer taxi and PHV drivers charging discounts (40%+) and subscription benefits across around 180 European cities. The partnership directly targets EV taxi economics by reducing one of the largest daily operating costs and improving access to compatible public charging networks.

- January 2026: Uber, Lucid, and Nuro unveiled a production-intent electric robotaxi at CES and confirmed that autonomous on-road testing had begun. The program highlights EV taxi competitiveness shifting toward purpose-built platforms, sensor suites, and compute stacks designed for high-uptime ride service, with launch targeted later in 2026.

- January 2026: Freenow by Lyft and the City of Hamburg signed an MoU to build a public-private framework for integrating Level-4 autonomous taxis into German cities. The announcement emphasizes structured cooperation across city regulators, taxi stakeholders, and technology partners, an important pathway for scaling EV taxi services as autonomy and electrification converge.

- January 2026: Grab announced a partnership with GAC to enhance the electric vehicle ride-hailing experience across Southeast Asia. The collaboration focuses on deploying GAC’s EV models within Grab’s platform, integrating vehicle connectivity and driver-focused features, and accelerating the electrification of high-utilization ride-hailing fleets in key regional markets.

REPORT COVERAGE

The global Electric Vehicle (EV) taxi market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 26.9% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Operating Model, By Vehicle Type, By Ownership Structure, By Vehicle Range, and By Region |

| By Operating Model |

|

| By Vehicle Type |

|

| By Ownership Structure |

|

| By Vehicle Range |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 52.59 billion in 2025 and is projected to reach USD 515.48 billion by 2034.

In 2025, the Asia Pacific’s market value stood at USD 30.37 billion.

The market demand is expected to grow at a CAGR of 26.9% during the forecast period from 2026 to 2034.

The ride-hailing/app-based platforms segment led the market share in the operating model segment.

Strengthening urban emission regulations drives the deployment of EV taxis.

Key market players include BYD, Tesla, SAIC/MG, Geely, Hyundai-Kia, Tata, mobility platforms such as Uber and DiDi.

Asia Pacific held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us