Embedded AI Market Size, Share & Industry Analysis, By Component (Hardware and Software & Services), By Deployment Mode (Edge, Cloud, and Hybrid), By Data Type (Sensor Data, Image and Video Data, Numeric Data, Categorical Data, Text and Audio Data, and Others), By End-user (BFSI, Automotive, Healthcare, Consumer Electronics, Manufacturing, Retail & E-commerce, IT & Telecom, and Others), and Regional Forecast, 2026-2034

Embedded AI Market Size & Share

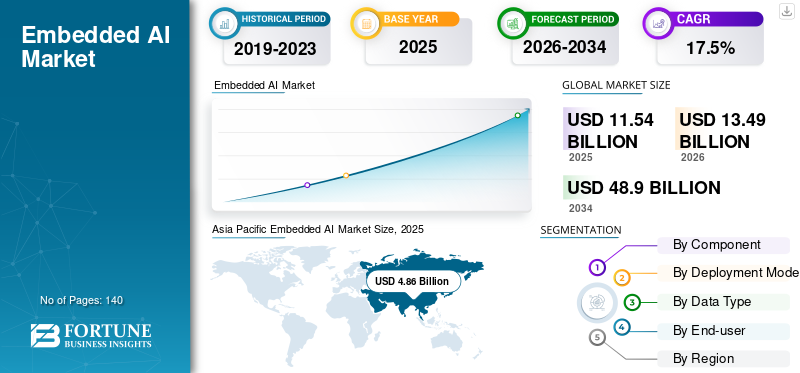

The global embedded AI market size was valued at USD 11.54 billion in 2025 and is projected to grow from USD 13.49 billion in 2026 to USD 48.90 billion by 2034, exhibiting a CAGR of 17.5% during the forecast period. Asia Pacific dominated the embedded AI market, accounting for 42.11% of the market share in 2025. Industry growth driven by edge computing expansion, real time data processing demand, and increasing integration of intelligent systems across connected smart devices.

The market refers to the ecosystem of hardware, software, and integrated technologies. It enables artificial intelligence processing to be performed directly on devices and edge systems, rather than relying solely on cloud-based computation. These components are deployed across a wide range of end-users, including BFSI, automotive, healthcare, consumer electronics, manufacturing, retail and e-commerce, IT and telecom, and other sectors that require localized, real-time intelligence. These solutions are being increasingly integrated into embedded devices and resource constrained devices, which play a crucial role in advanced AI and machine learning capabilities at the edge.

The embedded AI market represents a rapidly advancing segment of the broader artificial intelligence ecosystem, characterized by the integration of AI capabilities directly into hardware devices for real time data processing. Unlike centralized AI architectures, embedded AI systems enable localized decision-making, reducing latency and enhancing operational efficiency across diverse industries.

Embedded AI market size continues expanding as enterprises prioritize edge computing infrastructure to process data closer to its source. This shift is particularly evident in sectors requiring immediate responsiveness, including autonomous vehicles, industrial automation, and healthcare diagnostics. The ability to execute AI algorithms locally reduces dependency on cloud infrastructure while improving system reliability.

Several structural factors influence embedded AI market growth. The proliferation of smart devices, increasing adoption of machine learning models in constrained environments, and advancements in semiconductor technologies collectively support market expansion. Chip-level innovation, including AI accelerators and low-power processors, enables efficient deployment of embedded AI systems across consumer and industrial applications.

Key structural elements shaping embedded AI market trends include:

- Increasing deployment of edge AI across industrial and consumer applications

- Rising demand for real time data processing in mission-critical environments

- Integration of AI capabilities into smart home and smart city infrastructure

- Expansion of predictive maintenance solutions in manufacturing and energy sectors

Institutional buyers evaluate embedded AI solutions based on performance efficiency, scalability, and energy consumption. Decision-making often prioritizes hardware-software integration capabilities and compatibility with existing digital ecosystems. Regionally, North America leads in AI research and semiconductor innovation, while Asia-Pacific drives manufacturing and consumer electronics adoption. Europe emphasizes industrial automation and regulatory-compliant AI deployment.

Further, leading players in this market include NVIDIA Corporation, Qualcomm Incorporated, NXP Semiconductors N.V., STMicroelectronics N.V., Texas Instruments Incorporated, Renesas Electronics Corporation, Arm Holdings plc, Intel Corporation, MediaTek Inc., and Hailo Technologies Ltd.

Download Free sample to learn more about this report.

Embedded AI Market Key Takeaways

- 2025 Market Size: USD 11.54 billion

- 2026 Market Size: USD 13.49 billion

- 2034 Forecast Market Size: USD 48.90 billion

- CAGR: 17.5% from 2026-2034

- Asia Pacific dominated the embedded AI market with a 42.11% share in 2025.

- The hardware segment held the largest share in 2025.

- The edge deployment mode accounted for the largest market share in 2025.

Asia Pacific

Asia Pacific leads the market due to strong semiconductor manufacturing and increasing adoption of smart devices.

North America

North America maintains a significant market position driven by advanced AI research and innovation ecosystems.

Europe

Europe's market growth is supported by Industry 4.0 initiatives and rising factory automation.

U.S.

Strong semiconductor capabilities and enterprise investments in edge computing drive market growth.

Japan

Advanced robotics and automotive industries support the adoption of embedded AI solutions.

Read More

MARKET DYNAMICS

Embedded AI Market Trends

Increasing Integration of Embedded AI into Edge IoT and Autonomous Systems to Emerge as a Key Market Trend

A major trend shaping the market is the rapid convergence of embedded AI applications with edge IoT platforms and autonomous technologies. For instance,

- The Ericsson Mobility Report forecasts that short-range IoT connections will increase from 10.2 billion in 2022 to 28.7 billion by 2028, reflecting the rapid proliferation of edge and IoT endpoints where technology can be deployed.

Organizations are deploying compact AI accelerators and optimized processors within distributed devices to enhance local analytics and system responsiveness. Advances in lightweight AI models and power-efficient chip architectures support this trend. As adoption expands, the technology is becoming central to next-generation smart infrastructure, robotics, and intelligent mobility solutions.

The embedded AI market is evolving through a series of technological and operational shifts that reflect broader changes in digital infrastructure. One of the most prominent embedded AI market trends involves the convergence of edge computing and machine learning, enabling decentralized intelligence across connected environments.

Another important trend is the integration of AI capabilities directly into smart devices. Consumer electronics, industrial systems, and urban infrastructure increasingly incorporate embedded AI systems to enable real time data processing and automation. Advancements in low-power AI hardware also shape market trends. Specialized processors designed for embedded environments improve performance efficiency while maintaining energy constraints.

Key trends shaping the embedded AI market include:

- Expansion of edge AI architectures across industries

- Increasing adoption of AI-enabled smart devices

- Development of energy-efficient AI chipsets

- Growing use of embedded AI in predictive maintenance

Market Drivers

Growing Demand for Real-Time, On-Device Intelligence to Drive Market Growth

The market is benefiting from the growing demand for instant AI processing that does not rely on cloud connectivity. Industries such as automotive, manufacturing, and consumer electronics increasingly rely on embedded intelligence to enable faster decision-making and enhanced operational efficiency. For instance,

- Industry experts project that more than 90% of vehicles sold in 2030 will be connected, up from about 50% today, highlighting the growing need for real-time, on-board intelligence in automotive systems.

The shift toward autonomy and smart device ecosystems continues to drive the market growth. As a result, these solutions play a crucial role in delivering low-latency, secure, and reliable performance across critical applications. The embedded AI market is driven by increasing demand for real time data processing across distributed digital environments. Organizations require immediate insights from data generated by connected devices, particularly in industrial automation, autonomous vehicles, and healthcare monitoring systems.

Edge computing plays a central role in supporting embedded AI market growth. Processing data at the device level reduces latency and enhances responsiveness, which is critical for time-sensitive applications. This approach also reduces bandwidth usage and dependence on centralized cloud infrastructure. The rapid expansion of smart devices further accelerates adoption. Smart home systems, wearables, and connected industrial equipment increasingly integrate AI capabilities to improve user experiences and operational efficiency.

Key drivers supporting the embedded AI market expansion include:

- Growing deployment of edge AI in latency-sensitive applications

- Increasing use of machine learning in embedded environments

- Expansion of smart cities and connected infrastructure

- Rising demand for predictive maintenance in industrial sectors

Market Restraints

High Complexity and Cost of Developing Specialized Embedded AI Hardware and Software to Hamper Market Growth

Developing embedded AI systems requires substantial investment in specialized processors, firmware optimization, and tightly integrated software stacks. For instance,

- Cisco’s Annual Internet Report had projected 3.6 networked devices and connections per person globally in 2023, underscoring the massive scale of hardware and software that needed to be engineered and maintained, adding to the complexity and cost for embedded AI deployments.

The need for advanced engineering expertise and long development cycles increases the overall cost for manufacturers and solution providers. Limited standardization across hardware architectures further complicates development efforts and integration processes. These challenges collectively restrict wider adoption, particularly among small and mid-sized enterprises with constrained budgets.

Despite strong demand, the embedded AI market faces structural limitations that influence scalability and adoption. Hardware constraints remain a primary challenge, as embedded systems operate within restricted power, memory, and processing capacities.

Complexity in system integration also presents barriers. Developing embedded AI systems requires expertise in both machine learning and hardware engineering. This dual requirement increases development time and costs, particularly for organizations without specialized technical capabilities.

Data security and privacy concerns further impact the embedded AI industry. While edge computing reduces data transmission, sensitive data processed locally must still meet regulatory requirements. Ensuring secure processing within embedded environments adds to system design complexity.

Key constraints affecting embedded AI market growth include:

- Limited computational capacity in resource-constrained devices

- High complexity in integrating AI algorithms with hardware systems

- Data privacy and cybersecurity requirements

- Elevated development and deployment costs

Market Opportunities

Rising Adoption of Embedded AI in Safety-Critical Automotive and Healthcare Applications to Present Lucrative Growth Opportunities

Embedded AI technologies are being increasingly incorporated into advanced driver-assistance systems, medical diagnostics, and monitoring devices, where reliability and real-time decision-making are essential. For instance,

- Remote patient monitoring statistics indicate that nearly 50 million people in the U.S. already use remote monitoring devices and approximately 69% of healthcare organizations are utilizing or planning to use such tools, illustrating strong momentum for technology in medical diagnostics and monitoring.

These sectors are investing in high-performance, energy-efficient AI accelerators to enhance operational safety and improve accuracy. Regulatory support for intelligent, safety-enhancing technologies is further reinforcing demand. As a result, automotive and healthcare deployments represent high-value growth avenues for technology providers.

The embedded AI market presents significant opportunities as industries adopt decentralized computing architectures. One of the most promising opportunities lies in expanding edge AI deployment across sectors requiring immediate decision-making capabilities.

Smart cities offer a major opportunity for embedded AI systems. Urban infrastructure increasingly integrates AI for traffic management, energy optimization, and public safety monitoring, all requiring real time data processing at the edge.

Healthcare also represents a strong growth area. Embedded AI systems support wearable devices, diagnostic tools, and remote monitoring solutions, enabling timely and data-driven clinical decisions.

Key opportunities supporting embedded AI market growth include:

- Expansion of embedded AI systems in smart city infrastructure

- Growth of autonomous vehicles and intelligent transportation

- Increasing adoption of AI-enabled healthcare devices

- Rising demand for predictive maintenance in industrial operations

SEGMENTATION ANALYSIS

By Component

Hardware Segment Dominated Due to its Foundational Role in AI Enabled Edge Intelligence

Based on component, the market is divided into hardware and software & services.

Hardware

The hardware segment led the market in 2025. This has been recorded as AI-enabled processors, sensors, accelerators, and system-on-chip solutions form the foundational layer required to integrate intelligence directly into devices and edge systems.

Hardware represents the foundational layer of the embedded AI market, enabling execution of AI algorithms within constrained computing environments. This segment includes microcontrollers, system-on-chip processors, neural processing units, and dedicated AI accelerators optimized for edge computing applications.

Demand for embedded AI hardware continues rising as industries require real time data processing without dependence on centralized infrastructure. Autonomous vehicles, industrial robotics, and smart devices rely heavily on efficient hardware architectures capable of supporting machine learning inference at low latency.

Key demand drivers for hardware adoption include:

- Development of low-power AI chipsets for edge AI applications

- Increasing deployment of embedded AI systems in autonomous environments

- Rising need for compact, high-performance processing units

Software & Services

The software & services segment is expected to grow at the highest CAGR of 19.0% during the forecast period. This is owing to the rising demand for AI model optimization, deployment platforms, lifecycle management tools, and consulting services that help enterprises customize and maintain embedded AI solutions.

Software and services form a critical enabling layer within the embedded AI market. This segment includes machine learning frameworks, model optimization tools, deployment platforms, and lifecycle management services.

AI algorithms must be adapted for embedded environments with limited computational resources. Developers increasingly utilize lightweight models, quantization techniques, and edge-specific frameworks to ensure efficient deployment.

Service providers support implementation, integration, and ongoing system optimization. Enterprises often rely on specialized vendors to design and maintain embedded AI systems tailored to operational requirements.

Key drivers influencing this segment include:

- Increasing demand for optimized machine learning deployment frameworks

- Need for integration between hardware and AI software ecosystems

- Growth of managed services for embedded AI system maintenance

By Deployment Mode

Edge Deployment Leads Owing to its Ability to Support Low Latency, Privacy, and Offline AI Processing

Based on deployment mode, the market is classified into edge, cloud, and hybrid.

Edge

The edge deployment mode accounts for the largest share of the market, owing to the embedded AI workloads, which are executed locally on devices to meet stringent requirements for low latency, data privacy, and offline operation.

Edge deployment dominates the embedded AI market due to its ability to deliver real time data processing directly at the source. This approach minimizes latency and enhances responsiveness, making it essential for mission-critical applications.

Industries such as automotive, manufacturing, and healthcare rely on edge AI systems for immediate decision-making. Autonomous vehicles, for instance, require continuous processing of sensor data to ensure safe navigation.

Key advantages of edge deployment include:

- Reduced latency and faster response times

- Lower bandwidth requirements due to localized processing

- Enhanced data privacy through on-device computation

Cloud

Cloud deployment complements embedded AI systems by enabling centralized data processing, model training, and large-scale analytics. While real time inference occurs at the edge, cloud infrastructure supports continuous learning and model updates.

Organizations use cloud platforms to manage distributed embedded AI systems and deploy updates remotely. This capability ensures that AI models remain adaptive and relevant.

Cloud deployment remains essential for data-intensive applications requiring large computational resources for training machine learning models.

Hybrid

The hybrid segment is projected to record the maximum CAGR of 18.6% over the forecast period. This has been estimated as organizations increasingly combine on-device inference with cloud-based training, updates, and orchestration to balance performance, scalability, and cost.

Hybrid deployment models combine edge and cloud capabilities, offering flexibility in system architecture. This approach allows organizations to process critical data locally while leveraging cloud resources for advanced analytics and model refinement.

Hybrid systems are increasingly adopted in complex environments where both performance and scalability are required. This model supports efficient workload distribution across computing layers.

By Data Type

Sensor Data Dominates Driven by its Central Role in Real Time Device Decision Making

Based on data type, the market is divided into sensor data, image and video data, numeric data, categorical data, text and audio data, and others.

Sensor Data

The sensor data segment dominates the market since a majority of use cases, particularly in industrial, automotive, and consumer devices, rely on continuous streams of signals from motion, pressure, temperature, and other physical sensors for real-time decision-making.

Sensor data represents a primary input for embedded AI systems. Industrial equipment, autonomous vehicles, and smart devices generate continuous streams of data that require real time analysis.

Embedded AI systems process sensor data to enable predictive maintenance, anomaly detection, and operational optimization. This capability reduces downtime and improves system efficiency.

Image and Video Data

The image and video data segment is anticipated to grow at the highest CAGR of 19.5% during the forecast period. This is due to the expanding adoption of embedded computer vision in surveillance, ADAS, robotics, smart retail, and consumer imaging applications.

Image and video data processing is a critical segment within the embedded AI market. Applications include surveillance systems, healthcare diagnostics, and autonomous navigation.

Embedded AI systems analyze visual data locally, enabling rapid interpretation without transmitting large data volumes to centralized servers. This approach enhances both efficiency and privacy.

Numeric Data

Numeric data supports structured analytics within embedded AI systems. Applications include financial monitoring, industrial performance tracking, and environmental analysis.

Embedded AI systems use numeric data to identify patterns, forecast trends, and support decision-making processes in real time.

Categorical Data

Categorical data is widely used in classification and decision-making tasks. Embedded AI systems process this data to support applications such as customer segmentation and operational categorization within industrial systems.

Text and Audio Data

Text and audio data enable advanced user interaction capabilities within embedded AI systems. Voice recognition, natural language processing, and command-based interfaces are increasingly integrated into smart devices.

By End-user

To know how our report can help streamline your business, Speak to Analyst

Rapid Adoption of Embedded AI Drives Consumer Electronics Segmental Growth

The end-user market is subdivided into BFSI, automotive, healthcare, consumer electronics, manufacturing, retail & e-commerce, IT & telecom, and others.

BFSI

The banking, financial services, and insurance sector utilizes embedded AI systems for fraud detection, transaction monitoring, and risk assessment. Real time data processing enhances decision-making and operational efficiency. Embedded AI systems enable continuous monitoring of financial activities, reducing exposure to fraud and operational risks.

Automotive

The automotive segment is expected to register the highest CAGR of 20.6% during the forecast period. This expansion is driven by the increasing deployment of technology in advanced driver-assistance systems, autonomous driving platforms, in-vehicle infotainment, and predictive maintenance solutions.

Automotive applications represent a major contributor to embedded AI market growth. Autonomous vehicles rely on embedded AI systems for perception, navigation, and safety features. Embedded AI systems process data from sensors, cameras, and radar systems to enable real time decision-making in dynamic environments.

Healthcare

Healthcare institutions deploy embedded AI systems for diagnostics, patient monitoring, and medical imaging. Real time analysis supports faster and more accurate clinical decisions. Wearable devices and remote monitoring systems further expand adoption within this sector.

Consumer Electronics

The consumer electronics segment leads the market. This has been observed as smartphones, wearables, smart home devices, and personal gadgets have rapidly integrated technology features to enhance user experience, personalize services, and facilitate on-device processing.

Consumer electronics represent a significant segment within the embedded AI market. Smart home devices, wearables, and personal electronics integrate AI capabilities to enhance functionality and user experiences. Embedded AI enables automation, personalization, and intelligent interaction across connected devices.

Manufacturing

Manufacturing environments utilize embedded AI systems for predictive maintenance, quality control, and process optimization. These applications improve operational efficiency and reduce downtime. Embedded AI systems enable real time monitoring of production processes, enhancing productivity and reliability.

Retail & E-commerce

Retail organizations deploy embedded AI systems for inventory management, customer analytics, and automated checkout systems. Real time insights support improved customer experiences and operational efficiency. Embedded AI systems also enable demand forecasting and supply chain optimization.

IT & Telecom

The IT and telecommunications sector leverages embedded AI for network optimization, traffic management, and cybersecurity. Real time data processing supports efficient network operations and threat detection. Embedded AI systems enhance service quality and reduce operational disruptions.

Embedded AI Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

Asia-Pacific Embedded AI Market Analysis

Asia Pacific Embedded AI Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest embedded AI market share due to its strong concentration of electronics and semiconductor manufacturing, particularly in China, Japan, South Korea, and Taiwan. The rapid adoption of smart consumer devices, automotive electronics, and industrial automation significantly boosts the demand for on-device intelligence in the region. Continued investments in 5G, IoT infrastructure, and national AI initiatives are expected to sustain the region’s position as the fastest-growing market over the forecast period.

Asia-Pacific represents a rapidly expanding embedded AI market driven by large-scale manufacturing and consumer electronics production. Countries across the region deploy embedded AI systems in smart devices, automotive applications, and industrial automation. Strong semiconductor manufacturing capabilities support hardware innovation. Increasing investments in smart cities and digital infrastructure continue driving embedded AI market growth across Asia-Pacific economies.

Japan Embedded AI Market

Japan’s embedded AI market is supported by advanced robotics, automotive technologies, and consumer electronics industries. Embedded AI systems are widely used in industrial automation and smart devices. Strong research in machine learning and robotics drives innovation. Government initiatives promoting digital transformation and intelligent infrastructure further support embedded AI market growth within Japan’s highly technology-driven economy.

China Embedded AI Market

China represents a major contributor to the embedded AI market due to its extensive manufacturing base and rapid adoption of smart devices. Embedded AI systems are deployed across consumer electronics, smart cities, and industrial sectors. Government initiatives supporting artificial intelligence development accelerate adoption. Domestic technology companies play a significant role in advancing embedded AI capabilities and expanding market share.

Download Free sample to learn more about this report.

North America Embedded AI Market Analysis

North America accounts for the second-largest share in the adoption of embedded AI, supported by early adoption of advanced AI technologies and the presence of leading chipmakers, cloud providers, and embedded system vendors. High R&D spending and strong innovation ecosystems in sectors such as automotive, industrial, and healthcare foster the rapid integration of technology into products and platforms. In addition, the robust demand for edge analytics and autonomous systems across enterprises reinforces the region’s sizeable market position.

North America holds a leading position in the embedded AI market due to strong innovation in semiconductor design and artificial intelligence research. Enterprises deploy embedded AI systems across autonomous vehicles, healthcare, and industrial automation. High investment in edge computing infrastructure and advanced analytics supports embedded AI market growth. Mature digital ecosystems and strong institutional adoption reinforce North America’s dominant embedded AI market share.

United States Embedded AI Market

The United States dominates the North American embedded AI market, driven by advanced research capabilities and strong presence of semiconductor and technology companies. Embedded AI systems are widely deployed across consumer electronics, automotive, and industrial sectors. High enterprise investment in edge computing and machine learning supports embedded AI market growth. Government-backed AI initiatives further strengthen innovation and commercialization within the U.S. embedded AI industry.

To know how our report can help streamline your business, Speak to Analyst

Europe Embedded AI Market Analysis

Europe holds a significant share of the market, largely due to its established automotive, industrial machinery, and healthcare industries. Ongoing Industry 4.0 programs and factory automation initiatives drive the deployment of AI at the edge within production lines and equipment. Furthermore, stringent data protection and safety regulations encourage on-device processing, thereby supporting the adoption of these solutions across EU member states.

Europe demonstrates steady growth in the embedded AI market, supported by strong industrial automation and smart infrastructure initiatives. Regulatory frameworks emphasizing data protection and ethical AI influence deployment strategies. Automotive and manufacturing sectors drive adoption of embedded AI systems for predictive maintenance and efficiency improvements. Continued investment in digital transformation and edge computing supports consistent embedded AI market growth across European economies.

Germany Embedded AI Market

Germany plays a central role in Europe’s embedded AI market due to its advanced manufacturing and engineering ecosystem. Embedded AI systems are widely adopted in industrial automation, robotics, and automotive applications. Predictive maintenance and process optimization drive demand across industries. Strong government support for Industry 4.0 initiatives and continuous innovation in machine learning contribute to Germany’s growing embedded AI market share.

United Kingdom Embedded AI Market

The United Kingdom embedded AI market benefits from strong research institutions and a dynamic technology startup ecosystem. Embedded AI systems are increasingly deployed in healthcare, financial services, and smart city projects. Investment in artificial intelligence research and digital infrastructure supports market expansion. Collaboration between academia and industry accelerates innovation and strengthens the United Kingdom’s position in the global embedded AI market.

Middle East & Africa Embedded AI Market Analysis

The Middle East & Africa market is expected to expand rapidly as governments and enterprises accelerate smart city, security, and infrastructure modernization projects that rely on this technology. Large-scale investments in surveillance, utilities, transportation, and oil and gas automation are creating new demand for edge intelligence. Although the current revenue base is relatively small, the increasing number of digital transformation initiatives positions the Middle East & Africa among the rapidly-growing regional markets.

The Middle East and Africa embedded AI market is evolving as digital transformation initiatives expand across the region. Governments and enterprises deploy embedded AI systems in smart cities, energy management, and infrastructure projects. Increasing investment in digital infrastructure supports adoption. Growing demand for real time data processing is expected to gradually strengthen embedded AI market growth across regional economies.

Latin America & South America Embedded AI Market Analysis

South America is also expected to experience strong embedded AI market growth as Brazil, Mexico, and Argentina scale up digitalization across telecom, banking, retail, and public services. The increasing adoption of smartphones, smart consumer devices, and connected industrial equipment is driving the demand for embedded AI capabilities in the region. The expanding use of AI-driven automation in agriculture, mining, and logistics further supports a robust growth outlook, given its comparatively low installed base.

Latin America’s embedded AI market is developing gradually, supported by increasing digitalization and adoption of connected technologies. Industries such as manufacturing and retail are beginning to implement embedded AI systems for efficiency improvements. Expanding internet connectivity and infrastructure development support adoption. Although market maturity varies, rising awareness of AI capabilities is expected to drive future embedded AI market growth.

Embedded AI Industry Competitive Landscape

Key Industry Players

Key Players Emphasize Innovation through Product Launches to Strengthen Market Positioning

Players launch new products to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, as well as acquisitions and partnerships, to strengthen their offerings. Such strategic launches enable the technology companies to maintain and expand their market share in a rapidly evolving landscape.

The embedded AI market features a competitive landscape shaped by semiconductor manufacturers, software developers, and system integrators. Market participants compete on performance efficiency, power optimization, and integration capabilities across diverse embedded AI systems.

Semiconductor companies occupy a central position within the embedded AI industry. These firms design processors and AI accelerators optimized for edge computing environments. Competitive differentiation is largely driven by the ability to deliver high computational performance within strict power and thermal constraints.

Software providers contribute by developing machine learning frameworks and deployment platforms tailored for embedded environments. Compatibility with heterogeneous hardware architectures is critical for enabling scalable embedded AI solutions. Vendors offering integrated hardware-software ecosystems maintain strong positioning.

Emerging players focus on niche applications such as autonomous vehicles, robotics, and smart home ecosystems. These companies often specialize in optimizing AI algorithms for resource-constrained environments.

Collaborative partnerships are increasingly shaping market dynamics. Semiconductor firms, software developers, and system integrators work together to create unified embedded AI platforms. These collaborations enhance interoperability and accelerate adoption across industries. Institutional buyers evaluate vendors based on reliability, scalability, and long-term support capabilities. Security and compliance also play critical roles, particularly in healthcare and industrial applications.

LIST OF KEY EMBEDDED AI COMPANIES PROFILED

- NVIDIA Corporation (U.S.)

- Qualcomm Incorporated (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Renesas Electronics Corporation (Japan)

- Arm Holdings plc (U.K.)

- Intel Corporation (U.S.)

- MediaTek Inc. (Taiwan)

- Hailo Technologies Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Qualcomm introduced its AI200 and AI250 rack-scale inference accelerator cards targeting demanding embedded and edge AI workloads. These products demonstrate the company’s continued investment in high-performance, scalable AI infrastructure solutions.

- In August 2025, Hailo detailed the Hailo-10H as the first edge-AI chip capable of running on-device large language and vision language models. This development significantly reduces reliance on cloud processing by enabling sophisticated generative AI tasks to be performed locally.

- In July 2025, Hailo Technologies Ltd. commenced commercial shipments of the Hailo-10H edge-AI accelerator, designed to support advanced on-device generative AI workloads. This release marks a major milestone in bringing high-performance inference capabilities to compact embedded systems.

- In May 2025, Qualcomm announced its intention to expand into the data-center processor market with custom CPUs designed for compatibility with NVIDIA’s AI platforms. This move underscores the company’s strategy to extend its embedded and enterprise AI footprint beyond mobile solutions.

- In April 2025, Qualcomm Incorporated completed the acquisition of Edge Impulse Inc. and introduced new developer kits specifically designed for edge AI applications. This initiative enhances its embedded AI ecosystem, particularly within IoT and low-power device environments.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, By Deployment Mode, By Data Type, By End-user, and By Region |

|

By Component |

· Hardware o CPUs o GPUs o ASICs o FPGAs o NPUs/TPUs o Neuromorphic Chips o Others · Software & Services |

|

By Deployment Mode |

· Edge · Cloud · Hybrid |

|

By Data Type |

· Sensor Data · Image and Video Data · Numeric Data · Categorical Data · Text and Audio Data · Others |

|

By End-user |

· BFSI · Automotive · Healthcare · Consumer Electronics · Manufacturing · Retail & E-commerce · IT & Telecom · Others (Government) |

|

By Geography |

· North America (By Component, By Deployment Mode, By Data Type, By End-user, and By Country) o U.S. (End-user) o Canada (End-user) o Mexico (End-user) · South America (By Component, By Deployment Mode, By Data Type, By End-user, and By Country) o Brazil (End-user) o Argentina (End-user) o Rest of South America · Europe (By Component, By Deployment Mode, By Data Type, By End-user, and By Country) o U.K. (End-user) o Germany (End-user) o France (End-user) o Italy (End-user) o Spain (End-user) o Russia (End-user) o Benelux (End-user) o Nordics (End-user) o Rest of Europe · Middle East & Africa (By Component, By Deployment Mode, By Data Type, By End-user, and By Country) o Turkey (End-user) o Israel (End-user) o GCC (End-user) o North Africa (End-user) o South Africa (End-user) o Rest of the Middle East & Africa · Asia Pacific (By Component, By Deployment Mode, By Data Type, By End-user, and By Country) o China (End-user) o India (End-user) o Japan (End-user) o South Korea (End-user) o ASEAN (End-user) o Oceania (End-user) o Rest of Asia Pacific |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.54 billion in 2025 and is projected to reach USD 48.90 billion by 2034.

In 2025, the market value stood at USD 4.86 billion.

The market is expected to exhibit a CAGR of 17.5% during the forecast period of 2026-2034.

In 2025, the hardware segment led the market in terms of components.

The growing demand for real-time, on-device intelligence is a key factor driving market growth.

NVIDIA Corporation, Qualcomm Incorporated, and NXP Semiconductors N.V. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

Rising demand for real-time on-device intelligence, growing use of smart connected devices, increased focus on data privacy and security, and advances in power-efficient AI hardware are expected to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us