Engineered Stone Market Size, Share & Industry Analysis, By Type (Quartz-Based Engineered Stone, Engineered Marble, and Others), By Form (Slab, Tiles, and Others), By Application (Residential and Non-Residential), and Regional Forecast, 2026-2034

Engineered Stone Market Size & Future Outlook

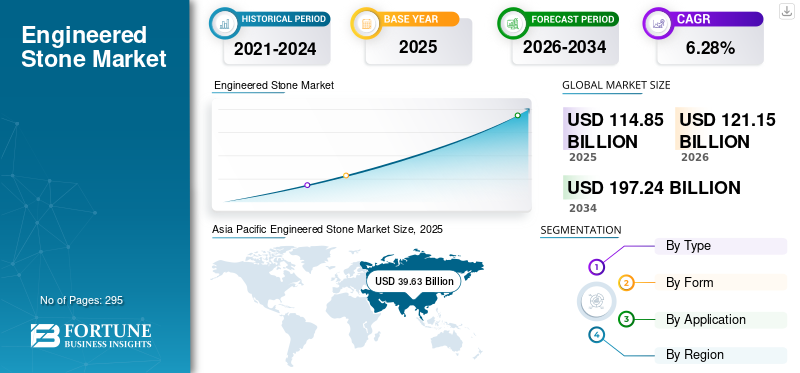

The global engineered stone market size was valued at USD 114.85 billion in 2025. The market is projected to grow from USD 121.15 billion in 2026 to USD 197.24 billion by 2034, exhibiting a CAGR of 6.28% during the forecast period. Asia Pacific dominated the engineered stone market with a market share of 34.50% in 2025.

Engineered stone is a manufactured composite material made by binding crushed natural stone, most commonly quartz or marble, with polymer resins, pigments, and additives under high pressure and vibration to form slabs, tiles, or custom shapes used in architectural applications. Typically composed of 85–95% stone aggregates (in quartz-based products) and 5–15% resins and pigments, these stones are designed to replicate the appearance of natural stone while offering improved consistency, durability, and lower porosity.

Furthermore, many key industry players, including Cosentino S.A., Caesarstone Ltd., LX Hausys, and VICOSTONE, operating in the market, are focusing on developing innovative engineered stone products to meet the increasing demand.

Download Free sample to learn more about this report.

ENGINEERED STONE MARKET TRENDS

Shift Toward Premium, Design-Driven Surfaces Paired With Sustainability and Health-Focused Innovation Is the Latest Trend

A key market trend shaping the industry today is the shift toward premium, design-driven solid surfaces paired with sustainability and health-focused innovation. Buyers, especially in residential renovation and high-end commercial segments, are increasingly choosing engineered stone not just for durability and consistency, but for aesthetic variety (marble-looks, large veining, ultra-thin formats, jumbo slabs) that rival natural stone. At the same time, regulatory and health concerns around crystalline silica exposure in fabrication have pushed manufacturers to develop low-silica or silica-free composite alternatives, driving R&D investment and new product lines. This trend toward design diversity, safer, environmentally considerate materials is accelerating adoption across mature markets (North America, Europe) and expanding appeal in fast-growing regions (Asia Pacific, Middle East & Africa), influencing pricing, branding, and competitive positioning industry-wide.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Steady Expansion of Residential Construction and Renovation to Boost Market Growth

The primary driver of the market is the steady expansion of residential construction and renovation, particularly in kitchens and bathrooms. Such stones, especially quartz-based slabs, are widely used for countertops and vanities, two of the most frequently upgraded elements in a home. As housing starts increase and homeowners invest in remodeling projects, demand for durable, aesthetically appealing surface materials rises. In mature markets such as North America and Western Europe, a strong remodeling culture plays a major role. Homeowners regularly upgrade kitchens to enhance property value, functionality, and design appeal, thereby driving demand for quartz surfaces.

At the same time, rapid urbanization in regions such as Asia Pacific and parts of the Middle East is fueling large-scale apartment construction, further boosting demand for interior finishing materials. Beyond construction activities, consumer preferences are shifting from natural stone to engineered quartz. Buyers favor quartz as it is non-porous, stain- and scratch-resistant, easy to maintain, and offers consistent color and pattern compared to natural marble or granite. Its perceived hygiene advantages and modern aesthetic also strengthen its appeal. Together, housing growth, renovation trends, and material substitution drive the market.

Rising Demand for Premium Interior Aesthetics and Lifestyle-Driven Home Upgrades to Bolster Market Growth

As disposable incomes increase, particularly in emerging economies, consumers are placing greater emphasis on the visual appeal and perceived luxury of their living spaces. Kitchens and bathrooms are no longer viewed purely as functional areas but as central design features of modern homes. Engineered stone, especially quartz-based surfaces, offers a wide range of colors, patterns, and marble-look finishes that align with contemporary interior design trends. The ability to replicate high-end natural stone aesthetics with improved durability and uniformity makes it an attractive and popular choice for both homeowners and developers.

Real estate developers are also incorporating engineered stone into mid- to high-end residential projects to differentiate properties and command higher selling prices. Premium finishes help position apartments and villas as modern, upscale offerings, increasing the adoption of quartz surfaces in new developments.

Social media influence, home improvement shows, and digital design platforms have amplified consumer awareness of surface materials and design trends. This growing aspiration for stylish, durable, and low-maintenance interiors continues to drive demand for engineered stone, supporting long-term market expansion.

MARKET RESTRAINTS

Growing Health and Regulatory Concerns Related to Crystalline Silica Exposure to Hamper Market Growth

A key restraint in the market is the growing health and regulatory concerns related to crystalline silica exposure. Quartz-based engineered stone typically contains a high percentage of crystalline silica (often 85–95%). During cutting, grinding, and fabrication, fine silica dust can be released. Prolonged exposure to this dust has been linked to serious respiratory diseases such as silicosis. As awareness of these health risks has increased, several countries have strengthened workplace safety regulations, imposed stricter dust-control standards, and, in some cases, proposed or implemented restrictions on high-silica products.

These regulatory developments create multiple challenges for the industry. Manufacturers face higher compliance costs due to required investments in safer production processes and reformulated low-silica products. Fabricators must invest in improved ventilation systems, water-based cutting equipment, and protective measures, increasing operational expenses. In some markets, regulatory uncertainty can also slow adoption and create reputational concerns among end users.

MARKET OPPORTUNITIES

Development and Commercialization of Low-Silica and Silica-Free Surface Materials May Create Lucrative Opportunities

As health regulations around crystalline silica exposure become stricter, manufacturers have a strong opportunity to innovate safer formulations that reduce or eliminate silica content while maintaining durability, aesthetics, and performance. Companies that successfully launch certified low-silica or alternative composite products can gain a competitive advantage, particularly in regulated markets such as North America, Europe, and Australia. This shift addresses compliance concerns, enhances brand reputation, and opens doors to new customer segments, while prioritizing workplace safety and sustainability.

Another significant opportunity is expanding into emerging residential markets across Asia Pacific, Latin America, and parts of Africa. Rapid urbanization, rising middle-class income, and growing real estate development create long-term demand for modern interior materials. As engineered stone penetration is still relatively low in several of these regions, there is substantial room for market expansion.

MARKET CHALLENGES

Intensifying Competition from Substitute Surface Materials Poses a Critical Challenge to Market Growth

A key market challenge in the industry is the intensifying competition from substitute surface materials, particularly sintered stone, porcelain slabs, and other ultra-compact surfaces.

Over the past few years, large-format porcelain and sintered stone products have gained traction in both residential and commercial applications. These materials offer high heat resistance, UV stability (suitable for outdoor use), and, in some cases, lower crystalline silica content than traditional quartz-based engineered stone. As architects and designers increasingly specify these alternatives, engineered stone manufacturers face pressure to defend market share, especially in premium and commercial segments.

Price competition from lower-cost producers, particularly from Asia, puts pressure on branded manufacturers' margins. With many regional and OEM suppliers offering competitively priced quartz slabs, global brands must balance premium positioning with affordability.

Segmentation Analysis

By Type

Quartz-based Engineered Stone Dominated Market Due to Its Superior Mechanical Strength

Based on type, the market is segmented into quartz-based engineered stone, engineered marble, and others.

The quartz-based engineered stone segment accounted for the largest market share in 2025 as it typically contains 85–95% natural quartz aggregates combined with polymer resins and pigments. This high quartz content gives the material superior mechanical strength, scratch resistance, stain resistance, and low porosity compared to engineered marble. As a result, quartz surfaces are widely preferred for kitchen countertops, bathroom vanities, and high-traffic commercial applications, which represent the largest demand segments in the overall market.

The engineered marble segment represents the second major category within the market, positioned primarily as a cost-effective alternative to quartz-based surfaces. The segment is anticipated to grow at a CAGR of 5.2% over the forecast period.

By Form

Slab Segment Led Market as It Offers a Seamless Appearance

Based on form, the market is segmented into slab, tiles, and others.

The slab segment dominated the engineered stone market share as it is directly linked to the high demand for quartz countertops in residential remodeling and new housing construction, particularly in North America and Europe. Slabs provide a seamless appearance, minimal joints, high structural strength, and premium aesthetic appeal. Additionally, the introduction of jumbo slabs and advanced digital veining technology has further strengthened this segment, allowing manufacturers to replicate natural marble aesthetics while maintaining durability and consistency.

Tiles are the second-largest segment and are more common in cost-sensitive and large-scale commercial applications, especially in Asia Pacific and the Middle East. The segment is expected to grow with a CAGR of 6.1% in the coming years.

To know how our report can help streamline your business, Speak to Analyst

By Application

Residential Segment to Lead Market Due to Increasing Renovation Trends

Based on application, the market is segmented into residential and non-residential.

The residential segment is expected to dominate the market, driven by strong housing construction activity, renovation trends, and growing consumer preference for premium interior finishes. The dominance of this segment is closely linked to the global growth in residential construction and remodeling. In mature markets such as North America and Western Europe, kitchen renovation cycles significantly boost demand for quartz-based slabs. Homeowners increasingly prefer engineered stone over natural granite and marble as it offers better stain resistance, lower maintenance, uniform appearance, and enhanced durability.

The non-residential segment is expected to grow with a CAGR of 5.8% over the forecast period.

Engineered stone is used in non-residential applications such as reception counters, restroom vanities, flooring, wall panels, and other interior surfaces where durability and aesthetic appeal are important. Growth in this segment is supported by expanding commercial construction, particularly in Asia Pacific and the GCC. Hospitality and retail projects often prefer such stone due to its uniformity, ease of maintenance, and long service life.

Engineered Stone Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Engineered Stone Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific represents the largest and most structurally dynamic region in the market. The Asia Pacific market was valued at USD 39.63 billion in 2025. The region’s dominance is primarily supported by rapid urbanization, large-scale residential development, and a strong domestic manufacturing base. China plays a central role, acting both as a major producer and consumer of engineered quartz surfaces. Its expansive housing construction and export-oriented production capacity significantly influence regional supply and pricing dynamics. India is emerging as a high-growth market driven by rising middle-class incomes, rising apartment construction, and the gradual premiumization of interior finishes.

Japan Engineered Stone Market

The Japan market in 2026 is estimated at around USD 3.24 billion, accounting for roughly 2.7% of global revenues. Stringent quality expectations and strong competition from alternative surface materials such as stainless steel and porcelain panels characterize Japan’s market. Despite slower population growth, steady renovation demand, and a preference for long-lasting interior materials, these factors support a stable, incremental rise in the engineered stone sector.

China Engineered Stone Market

China’s market in 2026 is estimated at around USD 18.78 billion, representing roughly 15.5% of global sales. The country’s market strength is closely tied to its vast construction sector, rapid urbanization, and large-scale residential development. China is also a global manufacturing hub for engineered quartz slabs, supported by cost-efficient production, strong export networks, and integrated supply chains. Domestic manufacturers supply both local projects and international markets, particularly North America, Europe, and Southeast Asia.

To know how our report can help streamline your business, Speak to Analyst

The India market in 2026 is estimated at around USD 9.14 billion, accounting for roughly 7.5% of global revenues. India is an emerging, high-potential market, supported by rapid urbanization, expanding residential construction, and rising middle-class incomes. The country is witnessing steady growth in demand for modern interior materials, particularly in urban housing projects across Tier 1 and Tier 2 cities.

North America

North America held the second-largest share in 2025, valued at around USD 37.33 billion. North America is one of the most mature and value-intensive markets globally. The region is strongly driven by residential remodeling, particularly kitchen renovations, which are a core component of household upgrade spending in the U.S. Quartz countertops have largely replaced laminate and are increasingly substituting for natural granite in mid- to high-end homes due to their durability, design consistency, and low maintenance. The U.S. accounts for the vast majority of regional demand, supported by high per-capita home improvement spending.

U.S. Engineered Stone Market

The U.S. market can be analytically approximated at around USD 36.19 billion in 2026. The U.S. is the largest and most value-intensive market globally, driven primarily by strong residential remodeling activity and high quartz countertop penetration. The market is mature, well-structured, and characterized by premium pricing and established distribution networks.

Europe

Europe is projected to grow at a CAGR of 5.87% over the coming years, reaching a valuation of USD 27.82 billion by 2026. Europe maintains a stable, design-oriented engineered stone market growth, shaped by renovation demand and architectural preferences. Western European countries such as Germany, the U.K., France, and Italy account for the majority of consumption. A strong emphasis on aesthetics, sustainability, and product certification standards characterizes the region. Quartz surfaces are widely adopted in kitchen remodeling projects, while engineered marble maintains relevance in certain decorative and flooring applications.

European demand is supported by steady residential refurbishment activity rather than rapid new construction growth. Sustainability considerations and environmental regulations also play a greater role in material selection than in many other regions.

U.K. Engineered Stone Market

The U.K. market in 2026 is estimated at around USD 5.12 billion, representing roughly 4.2% of global revenues.

Germany Engineered Stone Market

Germany’s market is projected to reach approximately USD 6.17 billion in 2026, equivalent to around 5.1% of global sales.

Latin America and Middle East & Africa

Latin America represents an emerging but steadily expanding market for engineered stone. Brazil and Mexico are the primary contributors, supported by urban housing development and gradual interior modernization trends. Rising middle-class incomes and greater exposure to global design standards are encouraging the adoption of quartz countertops in new residential projects. The Latin America market is set to reach a valuation of USD 4.47 billion in 2026.

The Middle East & Africa market is largely influenced by oil and gas drilling activities, especially in GCC countries such as Saudi Arabia and the UAE, where Engineered Stone is used in drilling and completion fluids. The Middle East & Africa reached a valuation of USD 7.43 billion in 2026.

GCC Engineered Stone Market

The GCC market is projected to reach around USD 3.88 billion in 2026, representing roughly 3.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Innovations by Key Players to Propel Market Progress

The market is moderately fragmented, led by a group of strong global branded players such as Cosentino, Caesarstone, LX Hausys, and VICOSTONE, which compete primarily on premium design, brand strength, distribution networks, and product innovation, especially in quartz-based countertop slabs. Competition is driven by product differentiation (marble-look designs, jumbo slabs, surface performance), pricing strategy, fabricator partnerships, and expanding distribution footprints, with increasing emphasis on low-silica and regulatory-compliant products shaping the next phase of competitive dynamics. Other notable market players include Technistone A.S., Quartzforms, Belenco, Stone Italiana S.p.A., and Quarella Group Ltd.

LIST OF KEY ENGINEERED STONE COMPANIES PROFILED

- LX Hausys (South Korea)

- Johnson Marble & Quartz (India)

- Technistone A.S. (Czech Republic)

- Caesarstone Ltd. (Israel)

- Belenco (Turkey)

- Quarella Group Ltd. (Italy)

- Quartzforms (Germany)

- Stone Italiana S.p.A. (Italy)

- Cosentino S.A. (Spain)

- VICOSTONE (Vietnam)

KEY INDUSTRY DEVELOPMENTS

- February 2025: At The International Surface Event (TISE) in Las Vegas, LX Hausys America unveiled “Splendor”, a new premium VIATERA quartz surface design crafted at its U.S. facility, demonstrating the company’s localized manufacturing and premium design focus.

- May 2023: Cosentino Group announced plans to establish its first U.S. manufacturing facility in Jacksonville, Florida, marking its first production site outside Spain and Brazil, with ground expected by January 2025 and completion targeted by 2028 at an estimated USD 270 million investment. The new facility will help streamline distribution channels across North America and better serve the region, which now accounts for more than half of the company’s global sales, while adhering to the group’s long-standing commitments to innovation, sustainability, and safety, including production using HybriQ technology that reduces crystalline silica and incorporates recycled materials.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, along with their regional prevalence. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.28% from 2026 to 2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Type, Form, Application, and Region |

| By Type |

|

| By Form |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 114.85 billion in 2025 and is projected to reach USD 197.24 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 39.63 billion.

The market is expected to grow at a CAGR of 6.28% over the forecast period of 2026-2034.

By type, the quartz-based engineered stone segment led the market.

The growth in residential construction & renovation is driving the market.

Caesarstone Ltd., LX Hausys, and VICOSTONE are the major players in the global market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 295

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us