Environmental Remediation Market Size, Share & Industry Analysis, By Site (Soil, Groundwater, Surface Water, and Sediment), By Method (In situ and Ex situ), By End User (Oil & Gas, Defense & Military, Chemical & Petrochemical, Manufacturing & Industrial, and Others), Regional Forecast, 2026-2034

Environmental Remediation Market Size and Future Outlook

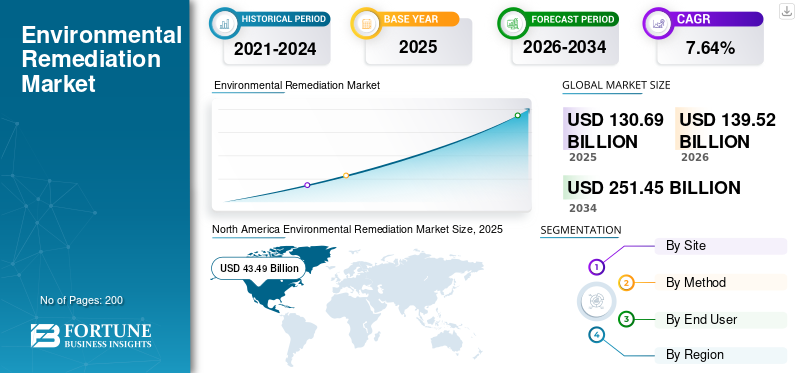

The global environmental remediation market size was valued at USD 130.69 billion in 2025. The market is projected to grow from USD 139.52 billion in 2026 to USD 251.45 billion by 2034, exhibiting a CAGR of 7.64% during the forecast period. North America dominated the global environmental remediation market with a market share of 33.28% in 2025.

The growing remediation requirement stems from legacy industrial contamination associated with brownfield redevelopment initiatives. Across developed and emerging economies, governments and private developers are increasingly prioritizing the reuse of abandoned industrial sites to address land scarcity, urban expansion, and infrastructure renewal. However, these sites are often affected by long-term contamination from hydrocarbons, heavy metals, chlorinated solvents, and persistent organic pollutants, making remediation a prerequisite for redevelopment approvals. Environmental remediation focuses on restoring contaminated site types by removing or neutralizing pollutants to protect human health and ecosystems.

The rising number of brownfield redevelopment projects, particularly in North America and Europe, is directly increasing demand for specialized environmental protection and remediation services, as well as advanced treatment technologies, thereby driving sustained market growth. Environmental remediation involves the safe cleanup and management of hazardous waste to restore contaminated environments and prevent risks to human health and nature.

- For instance, in January 2025, Clean Harbors’ remediation team completed a media replacement and cleanup project at a potable water filtration plant on the Guantanamo Bay Naval Base in Cuba. The scope included removal and replacement of filter media in multiple large tanks, as well as repairs to underdrain assemblies, ensuring uninterrupted delivery of safe drinking water on the base. This complex remediation work involved detailed logistics, site-specific technical adjustments, and strict execution under challenging conditions.

Tetra Tech, Inc. is a leading global consulting and engineering services firm headquartered in Pasadena, California, with extensive expertise in environmental remediation and sustainable infrastructure solutions. The company is widely recognized for its “Leading with Science®” approach, which combines advanced technical methods, rigorous site investigation, and engineering design to help clients address complex contamination challenges, achieve regulatory compliance, and reduce environmental liability. Veolia Environment S.A., Clean Harbors, Inc., AECOM, Jacobs Solutions Inc., and others are the key players operating in the environmental remediation industry.

Download Free sample to learn more about this report.

ENVIRONMENTAL REMEDIATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 130.69 billion

- 2026 Market Size: USD 139.52 billion

- 2034 Forecast Market Size: USD 251.45 billion

- CAGR: 7.64% from 2026–2034

- North America dominated the global environmental remediation market with a market share of 33.28% in 2025.

- The groundwater segment is experiencing the highest growth and is expected to grow at a CAGR of 8.34% over the forecast period.

- The ex situ segment is expected to grow at a CAGR of 6.94% during the forecast period.

North America

North America held the dominant share in 2025, valued at USD 43.49 billion, and is expected to reach USD 46.14 billion in 2026.

Europe

Europe is projected to grow at 7.92% over the coming years, the third-highest among all regions. It reached a valuation of USD 34.49 billion in 2025.

Asia Pacific

Asia Pacific reached a valuation of USD 40.17 billion in 2025 and secured the position of the second-largest region in the market.

U.S.

The U.S. market was estimated at around USD 38.61 billion in 2025, accounting for roughly 29.54% of the global market.

Japan

The Japan environmental remediation market in 2025 was valued at USD 6.01 billion, accounting for roughly 4.60% of global environmental remediation revenues.

Read More

ENVIRONMENTAL REMEDIATION MARKET TRENDS

Growing Demand for Advanced and Sustainable Remediation Technologies is the Key Market Trend

The environmental remediation market is experiencing a pronounced shift toward advanced, sustainable remediation technologies driven by heightened regulatory pressure, increasing contamination complexity, and an intensified focus on Environmental, Social, and Governance (ESG) commitments.

Governments and regulatory bodies worldwide are tightening cleanup standards and expanding liability frameworks for contaminated sites, particularly for emerging contaminants such as Per- and Polyfluoroalkyl Substances (PFAS), chlorinated solvents, and heavy metals, compelling site owners and developers to adopt more robust, innovative remediation solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Infrastructure Redevelopment and Land Reuse Constraints in Urban Areas to Drive the Market Growth

A significant driver for the global environmental remediation market is the increasing pressure to redevelop and reuse land in densely populated urban and industrial regions, where the availability of uncontaminated land is limited. As cities expand and infrastructure ages, governments and private developers are prioritizing the redevelopment of underutilized and strategically located sites to support transportation projects, renewable energy installations, logistics hubs, and mixed-use developments. Many of these sites, particularly former industrial zones, ports, rail yards, and utility facilities, are affected by historical contamination, making remediation a prerequisite for redevelopment.

Additionally, the transition toward renewable energy and electrification infrastructure, such as solar parks, battery storage facilities, and electric vehicle charging corridors, is increasingly reliant on repurposing legacy industrial land. This growing dependence on land reuse is creating sustained demand for site investigation, soil and groundwater treatment, and risk-based remediation solutions, making redevelopment-driven remediation a key market growth driver independent of regulatory pressure.

MARKET RESTRAINTS

High Capital Intensity and Uncertainty in Remediation Outcomes to Restrain the Market Growth

One of the major restraints on the environmental remediation market growth is the high capital intensity of remediation projects, combined with uncertainty about cleanup outcomes and timelines. Environmental remediation often requires substantial upfront investment in site assessment, sampling, laboratory analysis, technology selection, and project execution, particularly for sites affected by complex or mixed contamination. Costs can escalate further due to the need for specialized equipment, skilled technical personnel, long-duration treatment processes, and ongoing monitoring activities, making remediation financially challenging for small landowners, municipalities, and private developers.

MARKET OPPORTUNITIES

Commercialization of Emerging Remediation Technologies and Data-Driven Solutions to Create Market Opportunities

A key market opportunity lies in the commercial adoption of emerging remediation technologies combined with data-driven site management solutions. Advances in treatment methods such as electrokinetic remediation, thermal desorption, nano-enabled sorbents, and engineered bioremediation are enabling faster, more targeted cleanup of complex contaminants that were previously difficult or cost-prohibitive to address. These technologies are gaining traction as site owners seek solutions that reduce remediation timelines, minimize land disturbance, and lower long-term operational costs.

In parallel, the integration of digital tools, including high-resolution site characterization, real-time monitoring sensors, predictive modeling, and artificial intelligence–based decision platforms, is transforming the execution of large-scale remediation projects. Environmental remediation emphasizes cost-effectiveness by applying efficient cleanup strategies that reduce environmental impact while optimizing remediation expenses.

MARKET CHALLENGES

Technical Complexity and Site-Specific Variability in Remediation Projects Present Significant Challenges for Market Growth

One of the key challenges facing the market is the high level of technical complexity driven by site-specific variability in contamination characteristics and subsurface conditions. Unlike standardized infrastructure or construction projects, remediation efforts must be customized for each site based on factors such as contaminant type, concentration, depth, geological composition, hydrogeology, and proximity to sensitive receptors. This variability limits the applicability of uniform remediation solutions and increases reliance on detailed site investigations and iterative treatment designs.

Segmentation Analysis

By Site

Soil Segment Dominated the Market Due to Widespread Land Contamination

Based on site, the market is classified into soil, groundwater, surface water, and sediment.

In 2025, the soil segment accounted for approximately 40% of the market share. The dominant position in environmental remediation and testing is primarily due to its direct exposure to historical and ongoing industrial, agricultural, and waste-disposal activities. Industrial operations such as manufacturing, mining, oil refining, and chemical processing have led to long-term accumulation of contaminants, including heavy metals, hydrocarbons, pesticides, and persistent organic pollutants in soil.

The groundwater segment is experiencing the highest growth and is expected to grow at a CAGR of 8.34% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Method

In Situ Segment Dominated the Market Due to its Utilization in Real-Time Site Assessment

Based on the method, the market is classified into in situ and ex situ.

In 2025, the in situ segment dominated the global market. In situ techniques accounted for approximately 61.50% of the share in 2025, due to their ability to assess contamination directly at the site without extensive sample extraction or disturbance. These methods enable real-time measurement of contaminant concentrations, plume behavior, and subsurface conditions, which is critical for accurate site characterization and decision-making. In situ testing reduces the need for large-scale excavation, drilling, or transport of samples to off-site laboratories, lowering operational complexity and minimizing secondary environmental impacts.

The ex situ segment is expected to grow at a CAGR of 6.94% during the forecast period.

By End User

Oil & Gas Segment Dominated the Market Due to Extensive Hydrocarbon Operations Driving Testing Demand

Based on end user, the market is classified into oil & gas, defense & military, chemical & petrochemical, manufacturing & industrial, and others.

In 2025, the oil & gas segment held approximately 32% of the environmental remediation market share. The oil & gas sector dominates environmental testing due to the scale, intensity, and risk profile of upstream, midstream, and downstream operations. Exploration, drilling, refining, storage, and transportation activities involve continuous handling of hydrocarbons, chemicals, and by-products that pose significant contamination risks to soil, groundwater, and surface water.

The chemical & petrochemical segment is expected to grow at a CAGR of 8.14% during the forecast period.

Environmental Remediation Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Environmental Remediation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 43.49 billion, and is expected to reach USD 46.14 billion in 2026.

Environmental remediation in North America is primarily driven by stringent environmental regulations, increased enforcement of contaminated-site cleanup, and heightened public and corporate awareness of environmental and health risks. Industrial legacy pollution, urban redevelopment of brownfield sites, and growing investments in sustainable infrastructure further accelerate demand. Additionally, government funding programs and stricter standards for soil, groundwater, and air quality support continued remediation activities across the region.

U.S. Environmental Remediation Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was estimated at around USD 38.61 billion in 2025, accounting for roughly 29.54% of the global market.

Europe

Europe is projected to grow at 7.92% over the coming years, the third-highest among all regions. It reached a valuation of USD 34.49 billion in 2025. Environmental remediation in Europe is driven by strict EU environmental regulations, such as the Soil Strategy and the Water Framework Directive, as well as strong enforcement by national authorities. The presence of legacy industrial contamination, increasing redevelopment of brownfield sites, and growing focus on sustainable land use support remediation demand.

Germany Environmental Remediation Market

The German environmental remediation market in 2025 was valued at USD 8.76 billion and is expected to reach USD 9.48 billion in 2026, representing roughly 6.70% of global environmental remediation revenues.

Asia Pacific

Asia Pacific reached a valuation of USD 40.17 billion in 2025 and secured the position of the second-largest region in the market. In the region, India and China reached the valuations of USD 9.82 billion and USD 16.29 billion, respectively, in 2025.

Environmental remediation in the Asia Pacific region is driven by rapid industrialization, urbanization, and expanding infrastructure, which have led to widespread contamination of soil, water, and air. Governments across the region are strengthening environmental regulations and enforcement to address pollution and protect public health. Increasing foreign investment, redevelopment of contaminated industrial land, and rising awareness of environmental sustainability further support market growth.

Japan Environmental Remediation Market

The Japan environmental remediation market in 2025 was valued at USD 6.01 billion, accounting for roughly 4.60% of global environmental remediation revenues.

In Japan, environmental remediation is driven by strict environmental regulations, legacy industrial contamination, and a strong government focus on land reuse, public health protection, and sustainable urban development.

China Environmental Remediation Market

China’s environmental remediation market was projected to be significant worldwide, with 2025 revenues valued at USD 16.29 billion, roughly 12.47% of the global market.

India Environmental Remediation Market

The Indian environmental remediation market in 2025 was estimated at around USD 9.82 billion, accounting for roughly 7.51% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 7.61 billion in 2025.

Environmental remediation in Latin America is driven by mining and oil & gas contamination, rapid urbanization, and increasing enforcement of environmental regulations, along with growing government and private investment in the cleanup of soil and water resources to protect public health and ecosystems.

Brazil Environmental Remediation Market

Brazil's environmental remediation market reached USD 4.29 billion in 2025, accounting for roughly 3.29% of the global market. Environmental remediation supports long-term environmental recovery by systematically restoring contaminated land and water to safe and sustainable conditions.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market is set to reach USD 4.94 billion in 2025.

In the Middle East & Africa, environmental remediation is driven by oil & gas activities, mining operations, water scarcity concerns, and increasing government initiatives to address soil and groundwater contamination and meet environmental sustainability goals. Environmental remediation in the oil and gas sector focuses on cleaning up contaminated soil, water, and sites to minimize environmental impact and ensure regulatory compliance.

GCC Environmental Remediation Market

The GCC environmental remediation industry reached a valuation of USD 2.30 billion in 2025, representing roughly 1.76% of the global environmental remediation market.

COMPETITIVE LANDSCAPE

Key Industry Players

VENDORS are Actively Expanding their Market Share through Partnerships, Business Expansion, and Technological Advancements

The global environmental remediation market is highly consolidated, with prominent players including Veolia Environnement S.A., Clean Harbors, Inc., AECOM, and others. Companies operating in this industry are adopting targeted growth strategies focused on strengthening their product portfolios, technical capabilities, expanding their manufacturing presence, and more.

- For instance, in November 2025, Veolia announced it would acquire Clean Earth from Enviri for USD 3 billion (cash). The deal expands Veolia’s hazardous-waste footprint in the U.S. and is positioned to strengthen end-to-end remediation support (collection, treatment, disposal) for contaminated-site and industrial cleanup projects. Veolia informed that the transaction should materially increase hazardous-waste turnover and generate targeted cost synergies over time, with the closing expected by mid-2026.

Other key players in the global market include Jacobs Solutions Inc., Tetra Tech, Inc., WSP Global,

Arcadis NV, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY ENVIRONMENTAL REMEDIATION COMPANIES PROFILED:

- Veolia Environment S.A. (France)

- Clean Harbors, Inc. (U.S.)

- AECOM (U.S.)

- Jacobs Solutions Inc. (U.S.)

- Tetra Tech, Inc. (U.S.)

- WSP Global (Canada)

- Arcadis NV (Netherlands)

- RSK Group Ltd (U.K.)

- Montrose Environmental Group, Inc. (U.S.)

- Antea Group (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- June 2025: RSK Group announced the acquisition of AGEA, an environmental consulting firm with a strong presence in Latin America. While broader than remediation alone, AGEA’s permitting, environmental management, and evaluation work directly supports remediation project pipelines, especially where cleanup, redevelopment, and regulatory approvals intersect (e.g., mining, water, and renewables sites with legacy impacts). RSK presented the acquisition as part of its continued expansion of environmental capabilities and regional reach.

- May 2024: ECOM disclosed a five-year, multiple-award contract from the U.S. Army Environmental Command to provide environmental remediation services across the U.S., Puerto Rico, Hawaii, and Alaska. The scope includes investigation and cleanup of hazardous and toxic waste, specifically calling out PFAS (per- and polyfluoroalkyl substances). AECOM highlighted its PFAS experience across hundreds of sites, aligning the award with the Department of Defense’s expanding PFAS response needs.

- April 2025: Jacobs reported selection by the U.S. Air Force Civil Engineer Center (AFCEC) under a global IDIQ/MATOC vehicle supporting environmental restoration and related services. Jacobs’ work spans planning, investigation, assessment, design, and field inspection capabilities commonly used in contaminated land and groundwater remediation programs. The Air Force valued the ceiling at USD 1.5 billion, with a five-year base and one five-year option, creating a long runway for remediation task orders worldwide.

- March 2025: Arcadis reported winning a share of a USD 1.5 billion. U.S. Air Force MATOC focused on conservation, compliance, and cleanup activities across installations globally. The company framed the contract as planning and engineering environmental services, which may include support for remediation programs. Public details indicated the contract period began around March 2025, with a multi-year ordering structure that can extend the overall program window for up to a decade.

- March 2025: Montrose was selected as one of the firms on the U.S. Air Force’s USD 1.5 billion MATOC, supporting environmental restoration and planning work at Air Force installations worldwide. The release notes that the work includes remediation of both traditional and emerging contaminants, including PFAS, as well as environmental planning/support services. Montrose indicated no immediate financial impact in 2025 until purchase orders are issued, which is typical for IDIQ/MATOC frameworks.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.64% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Site, Method, End User, and Region |

|

By Site |

· Soil · Groundwater · Surface Water · Sediment |

|

By Method |

· In Situ · Ex Situ |

|

By End User |

· Oil & Gas · Defense & Military · Chemical & Petrochemical · Manufacturing & Industrial · Others |

|

By Geography |

· North America (By Site, Method, End User, and Country) o U.S. o Canada · Europe (By Site, Method, End User, and Country) o U.K. o Germany o France o Spain o Italy o Rest of Europe · Asia Pacific (By Site, Method, End User, and Country) o China o India o Japan o Australia o South Korea o Rest of Asia Pacific · Latin America (By Site, Method, End User, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Site, Method, End User, and Country) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 130.69 billion in 2025 and is projected to reach USD 251.45 billion by 2034.

In 2025, North America market value stood at USD 43.49 billion.

The market is expected to grow at a CAGR of 7.64% over the forecast period of 2026-2034.

The soil segment led the market by site in 2025.

Rising infrastructure redevelopment and land reuse constraints in urban areas are the key factors driving the market.

Veolia Environnement S.A., Clean Harbors, Inc., AECOM, and others are some of the prominent players in the market.

North America dominated the market in 2025.

Environmental remediation adoption is driven by stricter regulations, increased funding, heightened awareness of risks, and technological advancements.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us