EV Platform Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Car and Commercial Vehicle), By Propulsion Type (BEV and HEV), By Component (Battery Systems, Electric Motor Systems, Chassis & Structural Frame, Power Electronics, and Others), By Voltage Architecture (400V EV Platforms and 800V EV Platforms), and Regional Forecast, 2026-2034

EV Platform Market Size and Future Outlook

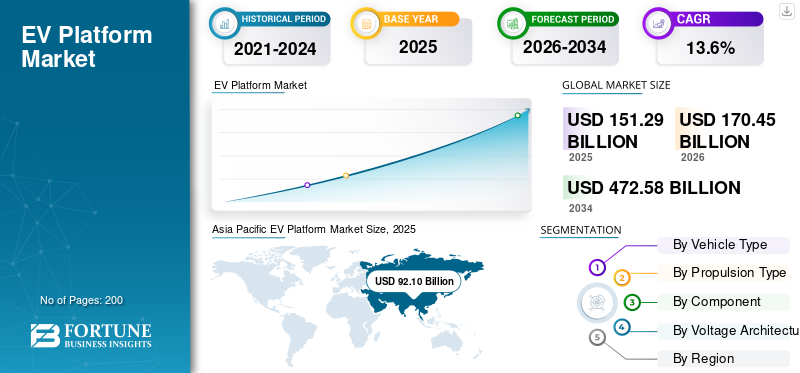

The global EV platform market size was valued at USD 151.29 billion in 2025. The market is projected to grow from USD 170.45 billion in 2026 to USD 472.58 billion by 2034, exhibiting a CAGR of 13.6% during the forecast period. Asia Pacific dominated the ev platform market with a market share of 60.88% in 2025.

The market refers to the industry focused on designing, developing, and supplying dedicated vehicle architectures used to manufacture Electric Vehicles (EVs). The EV platform industry integrates key components such as battery packs, electric motors, power electronics, and chassis systems into a modular structure that supports multiple vehicle models. These platforms enable automakers to reduce development costs, improve manufacturing efficiency, and accelerate the production of battery electric and hybrid vehicles across different vehicle segments.

Key drivers include the rising global electric vehicle adoption, stringent government emission regulations, and increasing investments by automakers in dedicated EV architectures. Advancements in battery technology, demand for scalable modular platforms, and the need to reduce vehicle development costs while accelerating EV production also significantly support market growth.

Major players include Volkswagen Group, Hyundai Motor Group, General Motors, Toyota Motor Corporation, Stellantis, and BYD. These companies compete through dedicated EV architectures, modular platform development, battery integration technologies, and scalable vehicle designs that support multiple models while improving efficiency, reducing production costs, and accelerating global electric vehicle deployment.

Download Free sample to learn more about this report.

EV Platform Market Trends

Shift Toward Dedicated Skateboard Platforms to Transform Vehicle Architecture

A prominent trend in the EV platform market is the growing adoption of dedicated skateboard-style vehicle architectures. These platforms place the battery pack within a flat structure integrated into the vehicle floor, with electric motors, power electronics, and other components arranged around it. This configuration improves vehicle stability, lowers the center of gravity, and enhances interior space compared to traditional vehicle architectures. Automakers are increasingly designing EV-specific platforms rather than modifying internal combustion engine structures, enabling improved energy efficiency and better packaging flexibility. Dedicated EV platforms also support advanced technologies such as over-the-air updates, software-defined vehicle systems, and autonomous driving features. As competition in the EV market intensifies, manufacturers are prioritizing innovative platform designs that enhance performance, safety, and overall vehicle functionality.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Global EV Adoption to Accelerate EV Platform Development

The rapid growth in global EV adoption is a key driver for the EV platform market. Governments across major economies are implementing stringent emission regulations and offering incentives to accelerate the transition from internal combustion engine vehicles to electric mobility. As automakers expand their EV portfolios, the demand for electric vehicles and scalable EV platforms is increasing significantly. These platforms enable manufacturers to build multiple vehicle models on a single architecture, reducing development time and production costs. Additionally, consumer demand for longer driving ranges, improved performance, and faster charging capabilities is pushing automakers to invest heavily in advanced EV platforms. As a result, companies are focusing on modular platform designs that can support various vehicle types, including passenger cars, SUVs, and light commercial vehicles, thereby strengthening market growth.

- For instance, in August 2025, Ford announced a new Universal EV Platform and production system backed by a USD 5 billion investment, designed to enable affordable EV manufacturing and support multiple future models, including a midsize electric pickup planned for 2027.

MARKET RESTRAINTS

Supply Chain Dependence on Critical Battery Materials to Restrict Platform Expansion

The EV platform market faces constraints due to the strong dependence on critical battery materials such as lithium, cobalt, nickel, and graphite. These materials are essential for manufacturing high-performance batteries that form the core of electric vehicle platforms. Supply disruptions, geopolitical tensions, and fluctuating commodity prices can significantly impact battery production costs and platform development plans. Since battery packs account for a large portion of EV manufacturing expenses, instability in raw material supply directly affects the cost structure of EV platforms. Automakers must also secure long-term supply agreements and invest in alternative battery chemistries to mitigate these risks. Consequently, uncertainty in the battery materials supply chain can slow the large-scale deployment of new EV platforms and increase financial risks for manufacturers expanding their electric vehicle production.

MARKET OPPORTUNITIES

Emergence of Scalable and Modular Architectures to Create Growth Opportunities

The development of scalable and modular EV architectures presents a significant opportunity for the EV platform market growth. Automakers are increasingly focusing on flexible platform designs that can accommodate multiple vehicle segments, battery sizes, and drivetrain configurations. This modular approach allows manufacturers to produce various models from compact cars to SUVs using a single underlying architecture, improving production efficiency and reducing overall development costs. In addition, scalable platforms allow companies to quickly adapt to evolving consumer preferences and technological advancements. Partnerships between automakers and technology providers are also expanding, enabling shared platform development and faster innovation cycles. As global EV production continues to rise, modular EV platforms are expected to play a critical role in supporting high-volume manufacturing while ensuring design flexibility and cost optimization across different vehicle categories.

MARKET CHALLENGES

Complex Battery Integration and Thermal Management to Challenge Platform Efficiency

One of the major challenges in the EV platform market is the complexity associated with battery integration and thermal management. Battery packs are the most critical and expensive component of electric vehicles, and integrating them efficiently into vehicle platforms requires advanced engineering and design optimization. Maintaining optimal battery temperature is essential for performance, safety, and longevity, which necessitates sophisticated thermal management systems. Additionally, variations in battery cell chemistry, size, and configuration can complicate platform standardization across multiple vehicle models. Manufacturers must also ensure structural safety and crash protection while maintaining lightweight vehicle design. Addressing these engineering challenges often requires continuous technological innovation and collaboration with battery manufacturers, which can increase development timelines and costs for EV platform developers.

Segmentation Analysis

By Vehicle Type

High Global Passenger EV Production and Platform Standardization Drive Passenger Car Segment

Based on vehicle type, the market is classified into passenger car and commercial vehicle.

The passenger car segment dominates the EV platform market share due to the rapid expansion of electric passenger vehicle production worldwide. Automakers prioritize dedicated EV platforms for passenger cars to support high-volume manufacturing, cost optimization, and model diversification across hatchbacks, sedans, and SUVs. Increasing consumer demand for electric mobility and government incentives supporting passenger EV adoption further strengthen platform deployment in this segment. Major automakers are launching multiple passenger EV models on shared architectures, ensuring strong and sustained demand for scalable EV platforms.

The commercial vehicle segment is projected to grow at a CAGR of 16.3% during the forecast period. Rising electrification of delivery vans, trucks, and fleet vehicles is driving the adoption of dedicated EV platforms designed for higher payload capacity, longer driving range, and improved operational efficiency in logistics and transportation applications.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Growing Adoption of Dedicated Electric Architectures Lead BEV Segment’s Dominance

In terms of propulsion type, the market is categorized into BEV and HEV.

The BEV segment dominates the EV platform market as most dedicated electric vehicle platforms are specifically designed for battery electric vehicles. Automakers increasingly focus on BEV platforms to support fully electric powertrains, larger battery packs, and longer driving ranges. Government incentives, emission regulations, and expanding EV model portfolios further strengthen BEV adoption globally. Major manufacturers are launching multiple BEV models on shared modular architectures, ensuring strong and sustained demand for dedicated EV platforms.

The HEV segment is projected to grow at a CAGR of 16.7% during the forecast period. Increasing consumer preference for fuel-efficient vehicles and the gradual transition toward electrification are encouraging automakers to integrate hybrid powertrains on flexible vehicle platforms that balance performance, efficiency, and reduced emissions.

By Component

Central Role of Energy Storage Systems to Drive Battery Systems Segment’s Dominance

In terms of component, the market is categorized into battery systems, electric motor systems, chassis & structural frame, power electronics, and others.

The battery systems segment dominates the EV platform market as batteries form the core component of electric vehicle architectures. EV platforms are primarily designed around battery integration, capacity optimization, and thermal management to support vehicle range, safety, and performance. Automakers increasingly invest in advanced battery packaging technologies, including structural battery packs and modular battery systems, to improve vehicle efficiency and scalability. As battery packs represent the largest cost component in EVs and determine driving range and charging performance, demand for advanced battery systems remains consistently high across next-generation EV platforms.

The power electronics segment is projected to grow at a CAGR of 15.4% during the forecast period. Increasing integration of inverters, converters, and onboard chargers in EV platforms is driving demand for advanced power management systems that enhance energy efficiency, enable faster charging, and support high-voltage EV architectures.

By Voltage Architecture

Established Infrastructure and Cost Efficiency to Drive 400V EV Platform Dominance

Based on voltage architecture, the market is segmented into 400V EV platforms and 800V EV platforms.

The 400V EV platform segment dominates the market due to its widespread adoption across mass-market electric vehicles. Most existing EV models are built on 400-volt architectures as they offer balanced performance, cost efficiency, and compatibility with current charging infrastructure. Automakers prefer 400V systems for high-volume passenger EV production as they support reliable battery performance while maintaining manageable component costs. Additionally, the majority of global charging networks are optimized for 400V systems, further supporting their continued dominance in mainstream EV platform development.

The 800V EV platform segment is projected to grow at a CAGR of 15.1% during the forecast period. Increasing demand for ultra-fast charging, improved energy efficiency, and high-performance electric vehicles is encouraging automakers to adopt advanced high-voltage architectures in next-generation EV platforms.

EV Platform Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific EV Platform Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to the strong presence of leading electric vehicle manufacturers, large-scale EV production, and supportive government policies promoting electrification. China, Japan, and South Korea are investing heavily in EV platform development to support expanding electric vehicle portfolios. China, in particular, leads global EV production and platform innovation with companies such as BYD and SAIC focusing on scalable EV architectures. Rapid growth in EV adoption, expanding battery manufacturing capacity, and strong government incentives continue to drive demand for advanced EV platforms across the region.

China EV Platform Market

In 2026, China is estimated at around USD 98.68 billion, accounting for a dominant share of global revenues. Massive EV production volumes, strong government incentives, and rapid innovation by manufacturers such as BYD and SAIC drive large-scale platform deployment.

Japan EV Platform Market

Japan will achieve USD 0.95 billion in 2026, accounting for a smaller share of the global revenues. Increasing electrification strategies by Japanese automakers and gradual expansion of EV models are expected to support steady EV platform development in the country.

Europe

Europe represents the second-largest market and is projected to grow at a CAGR of 13.2% during the forecast period. Stringent emission regulations, ambitious decarbonization targets, and strong government incentives for electric vehicles are accelerating EV platform development in the region. Automakers such as Volkswagen, Stellantis, and BMW are heavily investing in dedicated EV architectures to expand their electric vehicle portfolios. Additionally, increasing consumer adoption of electric vehicles and expanding charging infrastructure are encouraging manufacturers to develop scalable EV platforms to support future vehicle models.

U.K. EV Platform Market

The U.K. market is projected to capture USD 6.26 billion in 2026, accounting for a notable share of global revenues. Strong government electrification policies, expanding EV production, and investments by automakers in dedicated EV architectures continue to support steady market growth.

Germany EV Platform Market

In 2026, Germany’s market is expected to hit USD 12.01 billion, accounting for a significant share of global revenues. The presence of major automakers, rapid EV model launches, and investments in next-generation vehicle architectures drive platform development across passenger and premium EV segments.

North America

North America holds the third-largest share, driven by increasing investments in electric vehicle manufacturing and platform development. Automakers in the U.S. and Canada are expanding EV production facilities and introducing new electric models built on dedicated platforms. Tesla, General Motors, and Ford are focusing on modular EV architectures designed to support multiple vehicle segments. Government incentives, investments in battery manufacturing, and the expansion of EV charging infrastructure are further contributing to the growth of product adoption across the region.

U.S. EV Platform Market

The U.S. is projected to hit USD 16.60 billion in 2026, accounting for a strong share. Increasing EV manufacturing investments, supportive federal incentives, and platform development by Tesla, Ford, and General Motors accelerate market expansion.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, is gradually emerging as governments begin to promote electric mobility and sustainable transportation solutions. Increasing urbanization, rising fuel costs, and growing awareness of environmental sustainability are encouraging the adoption of electric vehicles in these regions. Automakers are also expanding EV model availability in developing markets, which is gradually increasing demand for EV platforms. However, limited charging infrastructure and lower EV adoption rates compared to developed regions continue to moderate the pace of market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Investments and Modular Platform Development Intensifying Market Competition

The global EV platform market is characterized by intense competition among established automotive manufacturers and emerging electric vehicle companies focused on developing scalable and modular EV architectures. Leading players such as Volkswagen Group, Hyundai Motor Group, General Motors, Toyota Motor Corporation, Stellantis, and BYD are investing heavily in dedicated EV platforms to support expanding electric vehicle portfolios. These companies prioritize platform standardization to enable the production of multiple vehicle models on a single architecture, reducing manufacturing costs and development timelines. Continuous investments in battery integration technologies, software-defined vehicle systems, and advanced power electronics are further strengthening the competitive landscape.

Additionally, companies are forming strategic partnerships and joint ventures to accelerate EV platform development and expand global production capabilities. Automakers are collaborating with battery manufacturers, semiconductor suppliers, and technology companies to improve platform efficiency, energy management, and vehicle performance. Several manufacturers are also focusing on next-generation EV platforms designed to support high-voltage architectures, autonomous driving technologies, and over-the-air software updates. As competition intensifies, companies are emphasizing innovation, platform scalability, and manufacturing efficiency to gain a competitive advantage and strengthen their presence in the rapidly expanding electric vehicle ecosystem.

LIST OF KEY EV PLATFORM MARKET COMPANIES PROFILED

- Tesla, Inc. (U.S.)

- Volkswagen Group (Germany)

- Hyundai Motor Group (South Korea)

- BYD Company Ltd. (China)

- General Motors (U.S.)

- Ford Motor Company (U.S.)

- Renault Group (France)

- Nissan Motor Co., Ltd. (Japan)

- SAIC Motor Corporation (China)

- Mahindra & Mahindra Ltd. (India)

- Toyota Motor Corporation (Japan)

- BMW Group (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Toyota premiered the three-row Highlander BEV for North America, expanding its battery-electric lineup and signaling broader use of dedicated EV architectures in large passenger vehicles, a move that strengthens Toyota’s platform strategy for regional model diversification and electrified portfolio expansion.

- August 2025: Ford unveiled its Universal EV Platform and production system, backed by about USD 5 billion in U.S. investments, aiming to launch a midsize electric pickup in 2027 while cutting platform complexity, lowering assembly time, and improving affordability of future EVs.

- July 2025: Kia detailed the PV5 built on Hyundai Motor Group’s E-GMP.S platform, highlighting a modular body system supporting up to 16 variants, underscoring how dedicated service-oriented EV platforms are expanding platform applications beyond passenger cars into commercial and fleet mobility.

- May 2025: Volkswagen confirmed its upgraded MEB+ platform will debut in 2026 with LFP cell-to-pack batteries, improving cost efficiency and performance while extending the life of its core EV architecture before the broader SSP transition across future group electric models.

- March 2025: BMW announced four advanced Superbrains for the Neue Klasse, along with a zonal wiring architecture that is 30% lighter and uses 600 meters less wiring, reinforcing software-defined, efficiency-led EV platform engineering across future BMW model generations.

- February 2025: Hyundai Motor Group unveiled E-GMP.S, a dedicated PBV platform derived from E-GMP, tailored for business mobility applications and designed around customer and partner requirements, highlighting the shift toward specialized EV architectures for logistics, fleet, and service-based transportation use cases.

- January 2025: Honda introduced the 0 Saloon and 0 SUV prototypes at CES, confirming both for 2026 production in Ohio and introducing the ASIMO OS, showing Honda’s push toward a new EV platform ecosystem centered on software-defined mobility.

REPORT COVERAGE

The global EV platform market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Propulsion Type, Component, Voltage Architecture, and Region |

| By Vehicle Type |

|

| By Propulsion Type |

|

| By Component |

|

| By Voltage Architecture |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 151.29 billion in 2025 and is projected to reach USD 472.58 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 92.10 billion.

The market is expected to exhibit a CAGR of 13.6% during the forecast period of 2026-2034

The battery electric vehicle segment led the market by propulsion type.

Rising global EV adoption is expected to accelerate the EV platform development.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us