EV Solid-state Battery Market Size, Share & Industry Analysis, By Electrolyte Type (Sulfide-based, Oxide-based, Polymer-based, and Hybrid/Composite), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Battery Capacity (Below 50 kWh, 50-80 kWh, 80-120 kWh, and Above 120 kWh), By Anode Material (Lithium Metal, Silicon-based, Graphite-based, and Anode-free), By Cell Architecture (Thin-film, Bulk-type, and 3D-structured), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

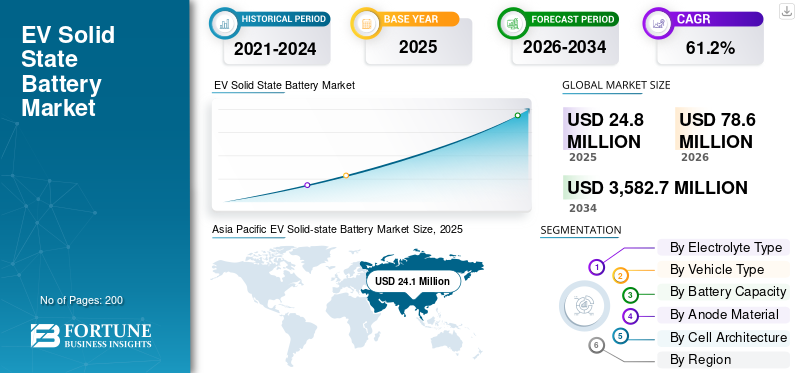

EV Solid-state Battery Market Size and Future Outlook

The global EV solid-state battery market size was valued at USD 24.8 million in 2025. The market is projected to grow from USD 78.6 million in 2026 to USD 3,582.7 million by 2034, exhibiting a CAGR of 61.2% during the forecast period. Asia Pacific dominated the EV solid-state battery market with a market share of 97.17% in 2025.

An EV solid-state battery is an advanced energy storage system using solid electrolytes instead of liquid electrolytes, offering higher energy density, improved safety, faster charging, and longer lifespan for electric vehicles. Key drivers in the market include rising electric vehicle adoption, demand for higher energy density, safety improvements over lithium-ion batteries, supportive government policies, technological advancements, and increasing investments in next-generation battery research and manufacturing.

Major players in the market include Toyota, QuantumScape, Solid Power, Samsung SDI, CATL, and Panasonic, competing through advanced solid electrolyte technologies, strategic partnerships, pilot-scale production expansion, and innovations in energy density, safety, and fast-charging capabilities.

Download Free sample to learn more about this report.

EV Solid-state Battery Market Key Takeaways

- 2025 Market Size: USD 24.8 million

- 2026 Market Size: USD 78.6 million

- 2034 Forecast Market Size: USD 3,582.7 million

- CAGR: 61.2% from 2026–2034

- Asia Pacific dominated the EV solid-state battery market with a 97.17% share in 2025.

- The oxide-based segment is projected to register a 61.3% CAGR during the forecast period.

- The HCV segment is projected to expand at a 66.2% CAGR over the forecast period.

Asia Pacific

Asia Pacific held a 97.17% market share in 2025 and is projected to record the fastest CAGR during the forecast period.

Europe

Europe accounted for the second-largest market share and is projected to expand at a 58.1% CAGR through 2034.

North America

North America represents the third-largest regional market, driven by technological innovation and increasing private-sector investments.

U.S.

U.S. The market is estimated at USD 0.7 million in 2026, accounting for approximately 0.9% of global market revenue.

Japan

Japan: The market is estimated at USD 1.8 million in 2026, accounting for approximately 2.3% of global market revenue.

Read More

EV SOLID-STATE BATTERY MARKET TRENDS

Accelerated Electrification to Strengthen Solid-State Battery Adoption is a Major Market Trend

The rapid electrification of the automotive industry is a major market trend. Automakers are increasingly investing in next- generation battery technologies to enhance vehicle range, reduce charging time, and improve safety performance. Solid-state batteries are gaining attention due to their potential to outperform conventional lithium-ion systems. Strategic collaborations between OEMs and battery developers, pilot production lines, and prototype vehicle testing are reinforcing this trend, positioning solid-state technology as a transformative innovation during the market forecast period.

- In 2025, electric vehicle sales are projected to exceed 20 million units, representing more than 25% of total global car sales. During the first quarter of 2025, worldwide EV sales increased by 35% compared to the same period last year.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High Energy Density to Drive Market Growth

Increasing consumer expectations for longer driving range and improved vehicle performance are key drivers accelerating market growth. Solid-state batteries offer significantly higher energy density compared to traditional lithium-ion batteries, enabling extended range without increasing battery size or weight. As EV adoption expands globally, automakers are prioritizing battery innovations that enhance efficiency and reduce range anxiety. Supportive regulatory policies, emission reduction targets, and funding for advanced battery research further stimulate EV solid-state battery market demand and strengthen the overall market analysis outlook.

- In February 2026, FAW achieved 500 Wh/kg energy density using a low-cost hybrid lithium-manganese solid-state battery pack, enabling 500 miles of range. The system integrates semi-solid architecture, enhanced cathode chemistry, and improved thermal stability for electric vehicles.

MARKET RESTRAINTS

High Production Costs and Scalability Constraints to Limit Immediate Commercialization

Despite strong potential, high manufacturing costs and scalability challenges remain significant restraints in the market. Solid electrolytes require complex material processing and advanced manufacturing techniques, increasing capital expenditure. Limited large-scale production capabilities and supply chain uncertainties for specialized materials further constrain widespread adoption. These factors may slow early commercialization during the initial years of the market forecast period, particularly when compared to the established lithium-ion battery ecosystem, which benefits from economies of scale and mature infrastructure.

MARKET OPPORTUNITIES

Strategic Partnerships and Gigafactory Investments to Create Growth Opportunities

Growing collaboration between automotive OEMs, battery manufacturers, and technology startups presents a substantial opportunity for the market. Joint ventures and long-term supply agreements are accelerating product development and facilitating knowledge transfer. Investments in pilot production facilities and next-generation gigafactories are expected to enhance manufacturing efficiency and reduce costs over time. As commercialization milestones are achieved, companies can capture greater market share by securing early contracts and strengthening their competitive positioning in emerging EV platforms.

- In February 2026, ProLogium broke ground on a 12 GWh solid-state battery gigafactory in France, designed to manufacture next-generation ceramic electrolyte cells for EVs. The facility will support high energy density architectures, improved thermal safety, and scalable automated production processes.

MARKET CHALLENGES

Material Stability and Interface Compatibility Challenges to Impact Performance Optimization

One of the primary challenges in the market is achieving stable interfaces between solid electrolytes and electrode materials. Technical issues such as dendrite formation, limited ionic conductivity at room temperature, and mechanical degradation during charge cycles can impact battery performance and longevity. Continuous research is required to improve material stability and ensure consistent performance under real-world driving conditions. Overcoming these technical barriers is essential to meeting safety standards and achieving reliable large-scale deployment in electric vehicles.

Segmentation Analysis

By Electrolyte Type

Superior Ionic Conductivity and Scalable Processing to Reinforce Sulfide-Based Segment Leadership

Based on electrolyte type, the market is segmented into sulfide-based, oxide-based, polymer-based, and hybrid/composite.

The sulfide-based segment dominates the market owing to its high ionic conductivity and compatibility with high-energy-density electrode materials. These electrolytes enable improved charge transfer efficiency and support enhanced battery performance at relatively lower operating pressures. Additionally, sulfide-based materials are easier to process into thin layers, supporting scalable manufacturing approaches. Ongoing pilot projects and OEM partnerships further strengthen their commercial readiness, reinforcing segmental leadership during the EV solid-state battery market forecast period.

- In February 2026, BYD announced progress toward deploying sulfide-based solid-state batteries solid-state batteries in electric vehicles, aiming for introduction around 2027. The development focuses on high energy-density architectures, enhanced electrolyte stability, improved thermal safety, and optimized integration with advanced EV drivetrains to support longer range and durability.

The oxide-based segment is projected to expand at a CAGR of 61.3% over the forecast period. Rising research focus on superior thermal stability, enhanced safety characteristics, and long lifecycle performance is accelerating adoption, particularly in premium EV platforms seeking long-term durability and structural battery integration advantages.

By Vehicle Type

High Production Volumes and Mainstream EV Adoption to Strengthen Hatchbacks & Sedans Leadership

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

The hatchbacks & sedans segment dominates the market due to high global production volumes and early electrification across compact and mid-size passenger vehicles. Automakers prioritize these models for next-generation battery integration to enhance driving range, safety, and efficiency. Strong urban adoption, supportive emission norms, and large-scale OEM investments in passenger EV platforms sustain consistent battery demand, reinforcing the segment’s leading market share throughout the market forecast period.

- In September 2024, MG announced plans to launch an electric vehicle equipped with a solid-state battery in 2025. The model is expected to feature enhanced energy density, improved safety characteristics, faster charging capability, and optimized pack integration to deliver extended driving range and improved efficiency.

The HCV segment is projected to expand at a CAGR of 66.2% over the forecast period. Growing electrification of long-haul and heavy-duty fleets, combined with increased demand for high energy density and extended range capabilities, is accelerating solid-state battery adoption in commercial transport applications.

To know how our report can help streamline your business, Speak to Analyst

By Battery Capacity

High Energy Requirements and Long-Range Performance to Accelerate Above 120 kWh Segment Leadership

By battery capacity, the market is divided into Below 50 kWh, 50-80 kWh, 80-120 kWh, and Above 120 kWh.

The above 120 kWh segment dominates the market due to increasing demand for extended driving range, higher payload capacity, and premium vehicle performance. Large-capacity batteries are particularly critical for SUVs, luxury EVs, and heavy-duty commercial vehicles requiring sustained power output. As solid-state battery technology enhances energy density and safety, automakers are prioritizing higher-capacity battery packs to differentiate offerings. This trend supports both dominant market share and the fastest EV solid-state battery market growth within the segment during the market forecast period.

- In February 2026, China’s FAW deployed its first semi-solid-state EV battery, advancing next-generation chemistry aimed at lowering costs and improving safety. The system delivers over 500 Wh/kg solid state cell energy density with a 142 kWh pack, enabling a CLTC range exceeding 1,000 km (620 miles), and highlighting progress toward high-density, long-range electrification despite mass-production challenges.

The 80-120 kWh segment accounts for the second-largest market share at 60.3%. This capacity range balances efficiency and cost optimization, making it suitable for mid-size passenger vehicles and fleet applications seeking competitive pricing and dependable performance.

By Anode Material

Higher Energy Density and OEM Compatibility to Strengthen Silicon-Based Segment Dominance

By anode material, the market is categorized into lithium metal, silicon-based, graphite-based, and anode-free.

The silicon-based segment dominates the market due to its ability to significantly enhance energy density while maintaining compatibility with evolving battery architectures. Silicon anodes improve charge capacity compared to conventional graphite, supporting longer driving range and better performance efficiency. Additionally, ongoing advancements in silicon stabilization techniques and integration with solid electrolytes are accelerating commercial viability. Strong OEM adoption in next-generation EV platforms further reinforces the segment’s leading market share during the market forecast period.

The lithium metal segment is projected to expand at a CAGR of 65.8% over the forecast period. Superior theoretical energy density and potential for ultra-lightweight battery designs are driving rapid research investments and pilot-scale commercialization in high-performance EV applications.

By Cell Architecture

Manufacturing Simplicity and Early Commercial Viability to Propel Bulk-Type Architecture Leadership

By cell architecture, the market comprises various sub-segments such as thin-film, bulk-type, and 3D-structured.

The bulk-type segment dominates the market due to its relatively simpler design, established material compatibility, and ease of integration into existing battery manufacturing lines. Bulk-type cells offer structural stability and scalable production potential, making them attractive for early-stage commercialization. Automakers favor this architecture for pilot deployment and near-term EV platforms, supporting both dominant market share and the fastest growth trajectory during the EV solid state battery market forecast period.

The 3D-structured segment holds the second-largest market share and is projected to grow at a CAGR of 55.5% over the forecast period. Its enhanced surface area and improved ion transport pathways support performance optimization in advanced, high-efficiency EV battery designs.

EV Solid-state Battery Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific dominates the market and is projected to register the fastest CAGR during the market forecast period. The region benefits from a robust battery manufacturing ecosystem, strong government incentives for EV adoption, and significant investments in next-generation battery R&D. Countries such as China, Japan, and South Korea are leading innovation and pilot-scale production. Expanding EV production volumes, supply chain integration, and rising domestic market demand collectively reinforce sustained market growth and regional market share expansion.

Asia Pacific EV Solid-state Battery Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

- In January 2026, Idemitsu Kosan announced plans to construct a pilot facility to manufacture sulfide-based solid electrolytes for Toyota’s EV solid-state batteries. The plant will focus on scalable synthesis processes, high ionic conductivity materials, and improved interfacial stability to support next-generation battery performance and commercialization.

China EV Solid-state Battery Market

The China market size in 2026 is estimated at around USD 73.3 million, accounting for roughly 93.4% of global market revenues. Strong domestic manufacturing, government-backed R&D funding, and aggressive EV production targets sustain dominance and continued commercialization momentum.

Japan EV Solid-state Battery Market

The Japan market value in 2026 is estimated at around USD 1.8 million, accounting for roughly 2.3% of global market revenues. Advanced material innovation, strong OEM collaboration, and early pilot deployments support steady technological leadership and structured growth.

India EV Solid-state Battery Market

The India market size in 2026 is estimated at around USD 0.3 million, accounting for roughly 0.3% of global market revenues. Rapid EV adoption policies, localization incentives, and expanding clean mobility investments drive the fastest-growing national outlook.

Europe

Europe holds the second-largest EV solid-state battery market share and is projected to expand at a CAGR of 58.1% over the market forecast period. Stringent emission regulations, carbon neutrality targets, and strong policy frameworks are accelerating EV adoption across the region. European automakers are actively investing in solid-state battery partnerships to strengthen technological competitiveness. Growing demand for premium electric vehicles and localized gigafactory investments further support market growth, while strategic collaborations enhance the region’s position in the global market analysis landscape.

- In January 2026, Syensqo and Axens launched Argylium, a joint venture focused on developing and scaling advanced materials for solid-state battery commercialization in Europe. The initiative aims to accelerate pilot-scale production, enhance material performance, and reinforce Europe’s leadership in next-generation battery innovation.

Germany EV Solid-state Battery Market

The Germany market in 2026 is estimated at around USD 0.4 million, accounting for roughly 0.5% of global market revenues. Strong automotive engineering capabilities, EU battery alliances, and premium EV demand accelerate structured market expansion.

U.K. EV Solid-state Battery Market

The U.K. market size in 2026 is estimated at around USD 0.1 million, accounting for roughly 0.1% of global market revenues. Government decarbonization commitments, research funding initiatives, and strategic technology partnerships support gradual commercialization progress.

North America

North America represents the third-largest market, supported by strong technological innovation and increasing private-sector investments. The presence of leading EV manufacturers and solid-state battery startups fosters a dynamic research environment. Government funding programs, clean energy incentives, and domestic battery manufacturing initiatives contribute to rising market demand. Additionally, strategic collaborations between automotive OEMs and technology firms are accelerating commercialization efforts, strengthening the region’s competitive positioning and contributing to consistent market growth over the forecast period.

- In February 2026, Factorial launched what it describes as the first U.S. solid-state battery production program for passenger vehicles. In partnership with Karma Automotive, the initiative will integrate Factorial’s proprietary FEST (Factorial Electrolyte System Technology) into Karma’s next-generation vehicle platform.

U.S. EV Solid-state Battery Market

The U.S. market value in 2026 is estimated at around USD 0.7 million, accounting for roughly 0.9% of global market revenues. Federal clean energy incentives, private-sector innovation, and startup-led solid-state advancements strengthen long-term competitive positioning.

Rest of the World

The rest of the world region is witnessing gradual growth in the market, driven by increasing EV adoption in South America, the Middle East, and selected African economies. Government electrification initiatives, improving charging infrastructure, and growing environmental awareness are supporting long-term demand. Although manufacturing capabilities remain limited compared to established regions, rising foreign investments and import partnerships are expected to enhance accessibility, contributing to steady market expansion throughout the market forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Alliances, Pilot Commercialization, and Material Innovation Define Competitive Intensity

The market is moderately consolidated, with a mix of established battery manufacturers and emerging solid-state technology startups competing for early commercialization leadership. Key players such as Toyota, QuantumScape, Solid Power, Samsung SDI, CATL, and Panasonic focus on proprietary solid electrolyte chemistries, lithium metal integration, and pilot-scale production expansion. Companies are strengthening OEM partnerships, securing long-term supply agreements, and investing in gigafactory-scale facilities to capture market share. Strategic joint ventures, intellectual property development, and government-backed funding programs are central to accelerating commercialization and technological differentiation.

- In February 2026, Idemitsu partnered with Toyota to advance commercialization of next-generation all-solid-state batteries, supporting Toyota’s objective to introduce electric vehicles equipped with solid-state technology between 2027 and 2028 through coordinated material development and supply integration efforts.

LIST OF KEY EV SOLID-STATE BATTERY COMPANIES PROFILED

- QuantumScape (U.S.)

- Solid Power, Inc. (U.S.)

- ProLogium Technology Co., Ltd. (Taiwan)

- Toyota Motor Corporation (Japan)

- Contemporary Amperex Technology Co., Ltd. – CATL (China)

- Samsung SDI Co., Ltd. (South Korea)

- LG Energy Solution (South Korea)

- BYD Company Ltd. (China)

- Nissan Motor Co., Ltd. (Japan)

- Panasonic Holdings Corporation (Japan)

- Hitachi Zosen Corporation (Japan)

- Ilika PLC (U.K.)

- Blue Solutions (France)

- Ampcera Inc. (U.S.)

- Factorial Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: CATL outlined its solid-state battery roadmap, prioritizing semi-solid batteries before transitioning to all-solid-state cells. The company targets small-scale production by 2027, advancing sulfide-based electrolytes, high-nickel cathodes, and lithium-metal anodes to achieve higher energy density, improved safety, and scalable manufacturing readiness.

- January 2026: Dongfeng developed a 350 Wh/kg solid-state battery and started a test fleet for intensive winter calibration in Mohe. The article cites claims of 620 miles range and 72% capacity retention at about -22°F (-30°C).

- December 2025: Ilika began shipping 10 Ah Goliath solid-state prototypes (five times capacity vs prior 2 Ah). The cells use a proprietary oxide coating for safety, were built on an automated pilot line, and Ilika also sampled larger 50 Ah formats.

- September 2025: Mercedes-Benz Group details an EQS test car using a lithium-metal solid-state battery completing 1,205 km from Stuttgart to Malmö without charging. The company positions the demo as proof of everyday usability potential, following an end-August long-distance run.

- April 2025: Stellantis announces validation of Factorial’s automotive-sized FEST solid-state cells at 375 Wh/kg, with fast charging from 15% to 90% in 18 minutes. It also cites an operating range 30°C to 45°C and states Stellantis plans to place the tech into a demo fleet by 2026.

- February 2025: BYD targeted solid-state batteries by 2027, framing it as a next step beyond current lithium-ion. The article positions the timeline as part of wider industry competition, with commercialization pacing dependent on scaling, validation, and cost reduction across supply chains.

- September 2024: Japan’s METI validates Toyota’s plan to begin solid-state battery production by 2026, with mass production projected around 2030. It cites potential 1,000 km range and 10-minute charging claims in early narratives, plus a gradual scale-up through 2027-2028.

- September 2024: SAIC-owned MG targeted EV with a solid-state battery as early as Q2 2025, and claims SAIC expects its solid-state packs could become 30% cheaper than LFP over time. The article notes the specific vehicle details were not fully disclosed in the report.

REPORT COVERAGE

The global EV solid-state battery market analysis provides an in-depth study of the market size & forecast by all the market segments included in the vehicle security components market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 61.2% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Electrolyte Type, Vehicle Type, Battery Capacity, Anode Material, Cell Architecture, and Region |

| By Electrolyte Type |

|

| By Vehicle Type |

|

| By Battery Capacity |

|

| By Anode Material |

|

| By Cell Architecture |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 24.8 million in 2025 and is projected to reach USD 3,582.7 million by 2034.

In 2025, the Asia Pacific market value stood at USD 24.1 million.

The market is expected to exhibit a CAGR of 61.2% during the forecast period.

The hatchback & sedans segment leads the market in terms of vehicle type.

Rising demand for high energy density to drive market growth

Major players in the market include Toyota, QuantumScape, Solid Power, Samsung SDI, CATL, and Panasonic, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us