Fiberglass Fabric Market Size, Share & Industry Analysis, By Fiber Type (E Glass and Specialty Glass), By Fabric Type (Woven and Non-Woven), By Application (Construction and Infrastructure, Transportation, Wind Energy, Electrical & Electronics, and Others), and Regional Forecast, 2026-2034

Fiberglass Fabric Market Size and Future Outlook

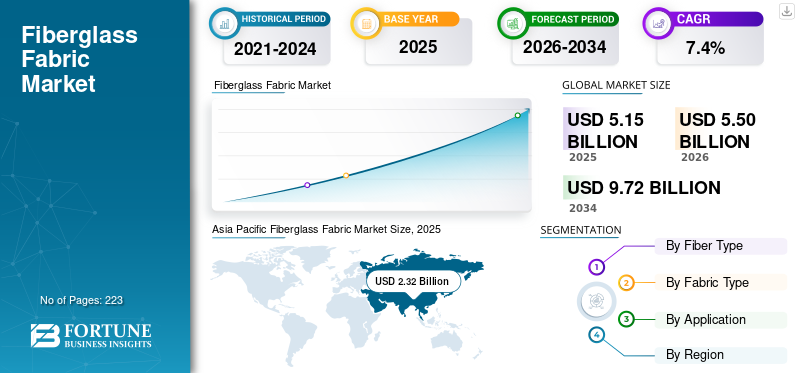

The global fiberglass fabric market size was valued at USD 5.15 billion in 2025. The market is projected to grow from USD 5.50 billion in 2026 to USD 9.72 billion by 2034 at a CAGR of 7.4% during the forecast period (2026-2034). Asia Pacific dominated the fiberglass fabric market with a market share of 45.05% in 2025.

Fiberglass fabric is a technical reinforcement material made from glass fiber yarns in woven, stitched, or other fabric constructions. It is used across composite structures, electrical laminates, construction reinforcement systems, industrial insulation, and engineered transport applications as it offers a practical balance of strength, dimensional stability, corrosion resistance, electrical insulation, and cost efficiency. Major suppliers and converters position fiberglass fabrics around end use sectors such as building and construction, transportation, wind energy, industrial infrastructure, marine, and electrical and electronics, highlighting the market’s broad industrial relevance.

The market is structurally linked to three key demand pillars. First, fiberglass fabric benefits from steady demand in reinforcement in construction and infrastructure, where technical textiles and coated fiberglass systems are used in wall reinforcement, waterproofing, repair, and industrial building materials. Second, it is tied to composite-intensive applications such as wind energy, transportation, and marine, where lightweighting, corrosion resistance, and durability remain critical. Third, it holds a higher-value position in electrical and electronics, especially in electronic glass cloth used in printed wiring board materials and other advanced electrical applications.

China Jushi, Nippon Electric Glass, Nittobo, Owens Corning, and Saint-Gobain are the key players operating in the market.

Download Free sample to learn more about this report.

Fiberglass Fabric MARKET Key Takeaways

- 2025 Market Size: USD 5.15 billion

- 2026 Market Size: USD 5.50 billion

- 2034 Forecast Market Size: USD 9.72 billion

- CAGR: 7.4% from 2026–2034

- Asia Pacific dominated the fiberglass fabric market with a market share of 45.05% in 2025.

- The E glass segment holds the dominant market share.

- The woven segment holds the dominant market share.

Asia Pacific

The region led the global market in 2025, driven by major fiberglass manufacturers, a strong electronics industry, and extensive downstream composite manufacturing.

North America

The market is supported by steady demand from transportation, industrial infrastructure, marine, and wind energy applications, along with growing adoption of advanced composite materials.

Europe

Europe remains a key market, benefiting from strong demand for technical textiles, engineered composites, and construction reinforcement systems across industrial sectors.

U.S.

The U.S. fiberglass fabric market was valued at USD 0.79 billion in 2025, accounting for approximately 15.3% of global market sales, supported by robust construction sector demand.

Japan

Japan continues to strengthen the fiberglass fabric market through its advanced electronics manufacturing ecosystem and high-value electrical insulation and composite applications.

Read More

Fiberglass Fabric MARKET TRENDS

Shift Toward Application-Specific and Higher-Performance Glass Fabric Systems Boosts Industry Growth

A major trend in the fiberglass fabric market is the shift from purely standard reinforcement fabrics toward more application-specific, performance-engineered formats. Suppliers are increasingly emphasizing multiaxial, unidirectional, electronic-grade, coated, and specialty reinforcement fabrics that are optimized for specific load paths, dielectric requirements, dimensional stability, or process efficiency. SAERTEX highlights multiaxial and unidirectional fabrics for high-performance composite solutions, while Hexcel positions its woven reinforcements for aerospace and industrial markets. This reflects a broader shift toward engineered, high-value fabric offerings rather than commodity products.

This trend is especially visible in electronics and advanced composites. Nittobo emphasizes high-performance glass cloth for electronic materials as digital devices continue to demand thinner, lighter, and more functional devices. Its broader electronic materials business is also tied to 5G, 6G, and semiconductor infrastructure. Meanwhile, wind and structural composite applications continue to increasingly adopt advanced fabric architectures that improve load transfer, resin efficiency, and part performance. As a result, differentiation in fiberglass fabric is increasingly driven by weave design, glass composition, finishing chemistry, and process compatibility, rather than fiber supply alone.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Composite Use in Wind Energy, Transportation, and Construction Reinforcement Supports Market Growth

Composite reinforcement demand across wind energy, transportation, and infrastructure remains a key driver for the fiberglass fabric market. Owens Corning directly markets fiberglass composite solutions into building and construction, transportation, industrial infrastructure, wind energy, and marine, while SAERTEX specifically highlights reinforcement materials for wind turbines that improve efficiency and service life. These end markets depend on fiberglass fabrics as they provide mechanical reinforcement at a lower cost than many advanced fibers, making them suitable for large-volume and large-structure applications.

The construction industry also serves as a durable volume anchor, as fiberglass technical textiles are widely used in reinforcement and building material systems. Saint-Gobain ADFORS positions itself as a leader in reinforcement technical textiles for construction and industrial markets, offering solutions based on fiberglass yarns and coating technologies. This supports the broader market dynamic in which demand for fiberglass fabric is not dependent on a single end-use segment. Instead, it is sustained by a diversified base spanning civil construction, repair, industrial, and composite manufacturing, providing resilience even when demand for one segment temporarily weakens.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Energy-Intensive Production and Margin Pressure from Industrial Cost Volatility Restrain Market Expansion

A key restraint in the fiberglass fabric market growth is the industry’s exposure to volatility in energy, logistics, and broader industrial input costs. Fiberglass manufacturing is energy-intensive, and rising costs can impact both fiber production and downstream fabric conversion economics. This is not just theoretical: recent commentary around Nippon Electric Glass’s UK fiberglass operation pointed to pressure from energy, raw materials, logistics, weak demand, and competition from Chinese suppliers. That illustrates how cost inflation and regional competitiveness can directly affect market profitability and capacity viability.

Another restraint is the strong cost-sensitivity in downstream sectors. In construction reinforcement, industrial materials, and mainstream transport composites, customers tend to be highly price-conscious, which limits suppliers' ability to pass on higher production or conversion costs. At the same time, technical buyers may resist reformulation or supplier changes once a fabric has been qualified for a specific application, slowing product substitution and making the market more conservative. This cost-and-qualification balance can compress margins, particularly in standard E-glass fabric categories.

MARKET OPPORTUNITIES

Electronics Upgrading and Specialty Reinforcement Demand Create Higher-Value Growth Potential

A major opportunity lies in the expansion of higher-value fiberglass fabrics for electronics and advanced industrial systems. Nittobo’s electronic materials business and glass cloth portfolio are directly tied to printed wiring board applications. At the same time, the company also links its special glass development to future communications and semiconductor technologies. This indicates a clear growth path for specialty glass cloth and electronic-grade fiberglass fabrics, where performance requirements are more stringent and pricing power is stronger than in commodity reinforcement fabrics.

A second opportunity comes from the continued rise of engineered reinforcement formats in wind, aerospace, industrial, and transport composites. SAERTEX’s multiaxial fabrics and Hexcel’s woven reinforcement solutions show that customers increasingly value fabrics that improve structural efficiency, reduce process waste, and deliver better component-level performance. This shift creates room for suppliers to move beyond plain commodity woven cloth toward more differentiated, specification-driven product portfolios with stronger margins and deeper customer integration.

MARKET CHALLENGES

Qualification Requirements and End-Use Specificity Slow New Product Penetration

A persistent challenge with fiberglass fabric is that downstream applications are highly specification-dependent. In electronics, changes in glass cloth characteristics can affect dielectric performance, thickness control, and laminate behavior. In transport, wind, marine, and industrial composites, changes in fabric architecture or surface treatment can alter resin uptake, layup behavior, load distribution, and finished-part reliability. Due to this, customers often require qualification cycles before shifting to a new fabric grade or supplier, which slows commercialization even when a technically improved option is available.

The challenge is even greater for specialty glass and premium reinforcement systems, where performance requirements are stricter, and the risk of end-use failure is significantly higher. Aerospace, electronics, and high-load composite applications compared to mainstream construction markets. This means growth in higher-value fabrics is attractive, but it also requires strong process control, technical support, and customer validation capability. As a result, market expansion is not driven only by capacity additions; it also depends on the supplier’s ability to meet demanding qualification and consistency requirements.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

The market is exposed to trade realignment, as supply is concentrated among a mix of large Asian producers and specialized regional converters. China Jushi Group positions itself as a global fiberglass leader, offering glass yarns and electronic fabrics, underscoring the scale of Asian supply in the broader value chain. When trade barriers, anti-dumping actions, freight disruptions, or geopolitical tensions affect glass fiber and technical textile flows, downstream buyers often respond by diversifying sourcing, rebalancing regional inventory, or favoring suppliers with localized conversion footprints.

Geopolitical tension also influences the market indirectly through industrial investment cycles, energy prices, and manufacturing confidence. Large composite and construction markets are sensitive to policy, capex, and infrastructure trends. At the same time, electronics- and aerospace-linked fabrics are affected by supply-chain reshoring and shifts in strategic material qualification. While demand remains intact, these dynamics can reshape where capacity is added, which suppliers gain approvals, and how aggressively buyers pursue regional supply resilience.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Current R&D in fiberglass fabric is focused less on basic material substitution and more on performance optimization through fiber composition, textile architecture, and end-use functionality. Nittobo highlights the continued development of glass composition and textile processing technology for high-performance electronic glass cloth. At the same time, SAERTEX emphasizes fabric structures aligned with load direction to improve load absorption. These examples show that innovation is increasingly focused on the precision engineering of the fabric itself rather than simply increasing generic fiberglass output.

Another clear R&D direction is improving specialty reinforcements for demanding structural applications. Hexcel’s reinforcement portfolio for aerospace and industrial markets, and NEG’s special glass and E-glass, highlights the importance of application-tuned fiber systems with improved strength, dimensional stability, and process compatibility. Over time, this is expected to support a broader mix shift from standard E-glass woven fabrics toward higher-value electronic, specialty, coated, and engineered reinforcement formats, particularly where customers are willing to pay for performance and reliability gains.

SEGMENTATION ANALYSIS

By Fiber Type

E-Glass Segment Dominates Due to Its Widespread Usage in Automotive Parts

Based on fiber type, the market is segmented into e glass and specialty glass.

E glass segment holds the dominant market share as it is the most established fiberglass type across mainstream composite and reinforcement applications, offering a strong balance of mechanical performance, electrical insulation, dimensional stability, and cost efficiency. NEG specifically notes that E-glass fiber improves resin-based properties, such as strength, heat resistance, hardness, and dimensional stability, and is widely used in automotive parts and housing equipment, reflecting its broad industrial acceptance. This versatility supports its dominance across construction reinforcement, transportation, wind energy, marine, and many industrial fabric applications.

Specialty glass is also expected to grow at a positive pace. Growth is supported by increasing demand for electronic-grade glass cloth, higher-performance reinforcements, and advanced industrial applications where standard E-glass may not fully meet dielectric, structural, or durability requirements. Nittobo explicitly links special glass and electronic glass cloth to advanced communications and semiconductor applications, indicating that specialty glass fabrics are increasingly important in the high-value segment of the market.

By Fabric Type

Woven Segment Dominates Due to Broader Structural Reinforcement Use

Based on fabric type, the market is segmented into woven and non-woven.

The woven segment holds the dominant market share. Woven fiberglass fabric is widely used across structural reinforcement, composite laminates, electrical insulation systems, and construction applications as it offers better dimensional stability, mechanical strength, and load-bearing performance than many non-woven formats. Owens Corning’s fabrics portfolio highlights multiaxial and non-crimp reinforcement fabrics for composite applications, while ADFORS positions woven fabrics within structural and surface reinforcement systems for construction markets. This broad applicability across transportation, wind energy, industrial infrastructure, marine, and construction makes woven fabric type the leading segment in both volume and value.

The non-woven segment also accounts for a notable share, supported by its use in mats, insulation layers, surface finishing, filtration, and certain pultrusion and building applications. Owens Corning’s continuous filament and chopped strand mat products illustrate how non-woven fiberglass materials remain important in applications that require conformability, process flexibility, surface uniformity, and compatibility with complex molded shapes. However, non-woven fiberglass fabrics generally serve more application-specific or secondary reinforcement roles than woven products, limiting their share relative to woven formats in the overall market.

By Application

To know how our report can help streamline your business, Speak to Analyst

Construction and Infrastructure Segment to Lead Due to Reinforcement Technical Textile Demand

Based on application, the market is segmented into construction and infrastructure, transportation, wind energy, electrical & electronics, and others.

The construction and infrastructure segment is expected to dominate the market during the forecast period. Segment leadership is tied to the widespread use of fiberglass technical textiles in reinforcement, repair, wall systems, waterproofing, coated textiles, and industrial building materials. Saint-Gobain ADFORS directly positions itself around reinforcement technical textiles for construction markets and offers solutions using fiberglass yarns and coating technologies, making construction one of the most visible and repeatable demand bases for fiberglass fabric.

The transportation segment is expected to record solid growth, supported by lightweighting, corrosion resistance, and the use of composite reinforcements in automotive and related mobility applications. Owens Corning identifies transportation as a core market for its composite solutions, while NEG notes the use of E-glass in automotive parts. This combination supports steady transportation demand, especially for manufacturers that need durable reinforcement materials without the cost premium associated with more expensive advanced fibers. The segment is expected to register 7.7% growth rate during the forecast period.

The wind energy segment represents a strong growth area, as fiberglass fabrics remain a fundamental reinforcement material in wind blade structures and related composite systems. Owens Corning and SAERTEX both explicitly position reinforcement materials in wind energy, with SAERTEX emphasizing improved turbine efficiency and service life. This makes wind energy one of the most strategically important application segments for fiberglass fabric suppliers, although demand can be cyclical depending on project timelines and policy support.

The electrical & electronics segment holds a smaller share by volume than construction, but is among the most attractive on the basis of value. Nittobo’s glass cloth business confirms growing demand for high-performance fiberglass fabrics used in printed wiring board materials and electronics infrastructure. This segment benefits from higher technical barriers, tighter specifications, and stronger product differentiation than many standard reinforcement categories.

FIBERGLASS FABRIC MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Fiberglass Fabric Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading fiberglass fabric market share in 2025. The region benefits from the presence of major fiberglass and electronic fabric producers, extensive downstream composite manufacturing, and a strong electronics and industrial base. China Jushi positions itself as a global leader offering products such as electronic fabrics and glass yarns. In contrast, Nittobo’s electronic glass cloth business underscores the region’s importance in higher-value electrical and electronics applications. This combination supports both high-volume and high-value demand across Asia Pacific.

China Fiberglass Fabric Market

China’s market is one of the largest worldwide, with 2025 revenue at USD 1.19 billion, representing roughly 16.9% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a significant market, supported by mature demand for composites across transportation, industrial infrastructure, marine, and wind applications. Owens Corning and Hexcel have strong positions in composite reinforcements for industrial and structural end uses, indicating the region’s importance in performance-oriented fiberglass fabric demand. The market also benefits from specification-driven consumption in advanced materials applications, where technical support and product consistency are critical.

U.S. Fiberglass Fabric Market

In 2025, the U.S. market stood at USD 0.79 billion within North America, driven by strong demand from the construction sector. The U.S. accounts for roughly 15.3% of global market sales.

Europe

Europe is an important market driven by technical textiles, industrial applications, construction reinforcement systems, and engineered composites. Saint-Gobain ADFORS has a strong presence in reinforcement technical textiles for construction and industrial markets, while SAERTEX’s specialization in multiaxial composite fabrics highlights Europe’s strength in advanced reinforcement formats. This positions Europe as a key region for value-added fabric categories rather than only commodity volumes.

Germany Fiberglass Fabric Market

The Germany market in 2025 stood at around USD 0.38 billion, representing roughly 7.4% of global market revenues.

U.K. Fiberglass Fabric Market

The U.K. market in 2025 stood at around USD 0.18 billion, representing roughly 3.5% of global market revenues.

Latin America

Latin America remains a smaller but developing market, supported by gradual growth in construction materials, industrial maintenance, transport production, and imported reinforcement fabrics for composites and repair applications. Demand is more fragmented than in Asia Pacific or Europe, but infrastructure and industrial end uses continue to create a stable base for fiberglass fabric consumption. The market is likely to remain selective, with growth concentrated in countries that combine industrial activity with downstream manufacturing and repair demand.

Brazil Fiberglass Fabric Market

Brazil market in 2025 stood at around USD 0.08 billion, representing roughly 1.5% of global market revenues.

Middle East & Africa

The Middle East & Africa region shows targeted growth linked to construction, industrial projects, infrastructure reinforcement, and maintenance-driven demand for durable materials. Market development is supported by project-led activity and the use of fiberglass fabrics in industrial and construction systems. However, the overall market size remains smaller than in Asia Pacific, North America, and Europe. Demand also varies across countries, with stronger opportunities concentrated in industrial hubs and construction-intensive markets.

GCC Fiberglass Fabric Market

The GCC market in 2025 stood at around USD 0.12 billion, representing roughly 2.4% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Capability-led Downstream Differentiation Shapes Competitive Dynamics

The market is moderately consolidated at the upstream fiber and yarn level but becomes more differentiated at the fabric conversion and application stages. Competition is shaped by three main capabilities: large-scale glass fiber supply, technical textile conversion know-how, and specialization in high-value end-use sectors such as electronics, wind energy, aerospace industry, and construction reinforcement. This results in a market where scale is critical for standard E-glass products, while product engineering, finishing chemistry, and customer qualification strength matter more in premium segments. China Jushi, Nippon Electric Glass, Nittobo, Owens Corning, and Saint-Gobain are among the key players in the broader fiberglass fabric value chain.

LIST OF KEY FIBERGLASS FABRIC MARKET PLAYERS PROFILED IN THE REPORT

- China Jushi Co., Ltd. (China)

- Nippon Electric Glass Co., Ltd. (Japan)

- Nitto Boseki Co., Ltd. (Japan)

- Owens Corning (U.S.)

- Saint-Gobain (France)

- Hexcel Corporation (U.S.)

- SAERTEX GmbH & Co. KG (Germany)

- Porcher Industries (France)

- VALMIERA GLASS GROUP (Latvia)

- Ahlstrom (Finland)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Porcher Industries highlighted a new multilayer hybrid fabric range for faster consolidation of complex thermoplastic composite parts. Although not limited only to fiberglass fabric, the development reflects the broader market shift toward higher-performance, application-engineered textile reinforcements rather than purely standard woven cloth.

- February 2025: Owens Corning agreed to sell its glass reinforcements business to Praana Group for an enterprise value of USD 755 million. This is a meaningful structural development for the fiberglass fabric market as it reshapes one of the better-known participants in glass reinforcements and may lead to a more specialized ownership structure around the business. Owens Corning stated that the transaction follows its strategic review of the business.

- June 2024: Owens Corning and Composite Recycling signed a letter of intent to explore the use of reclaimed glass fibers in Owens Corning’s glass fiber products portfolio. This is important from a competitive standpoint as circularity is becoming a differentiator in composites and reinforcement materials, and recycled content could gradually influence product positioning in fiberglass-based materials.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, fiber type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 7.4% from 2026 to 2034 |

| Segmentation | By Fiber Type, By Fabric Type, By Application, and By Region |

| By Fiber Type |

|

| By Fabric Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.15 billion in 2025 and is projected to reach USD 9.72 billion by 2034.

Recording a CAGR of 7.4%, the market is slated to exhibit steady growth during the forecast period.

The construction and infrastructure segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

5) What is the key factor driving the market growth?

- 2021-2034

- 2025

- 2021-2024

- 223

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us