Finished Vehicles Logistics Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Vehicle Propulsion (ICE and Electric), By Transport Mode (Road, Rail, Waterways, and Air), By Distribution (Domestic and International), By Service Type (Primary Transport, Secondary/Last-mile Distribution, Port & Terminal Services, Storage & Yard Management, and Value-added Services), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

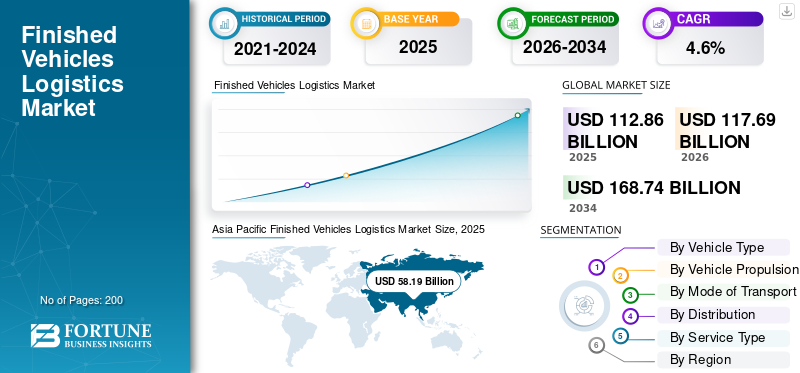

The global finished vehicles logistics market size was valued at USD 112.86 billion in 2025. The market is projected to grow from USD 117.69 billion in 2026 to USD 168.74 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. Asia Pacific dominated the global finished vehicles logistics market with a market share of 51.56% in 2025.

The finished vehicles logistics market is experiencing steady growth, driven by rising global vehicle production, expanding cross-border automotive trade, and increasing demand for efficient distribution of passenger and commercial vehicles. Automakers are increasingly outsourcing logistics operations to specialized providers to optimize costs, reduce delivery times, and manage complex multimodal transport networks. Growing adoption of electric vehicles is also reshaping logistics requirements, with a higher focus on battery handling, safety compliance, and dedicated transport infrastructure. Additionally, investments in digital fleet management, real-time vehicle tracking, and yard automation are improving operational efficiency and visibility across the supply chain. Government investments in port infrastructure, rail connectivity, and road networks further support market expansion, particularly in emerging economies.

- For instance, in December 2025, Wallenius Wilhelmsen secured a USD 500 million contract extension with automotive and heavy equipment manufacturers, strengthening long-term vehicle logistics services, fleet utilization, and global RoRo shipping capacity networks.

Furthermore, major players such as CEVA Logistics, DHL Supply Chain, Kuehne+Nagel, and DB Schenker are focusing on capacity expansion, sustainability initiatives, and technology-driven logistics solutions to meet evolving automotive OEM requirements and regulatory standards.

Download Free sample to learn more about this report.

Finished Vehicles Logistics Market KEY TAKEAWAYS

- 2025 Market Size: USD 112.86 billion

- 2026 Market Size: USD 117.69 billion

- 2034 Forecast Market Size: USD 168.74 billion

- CAGR: 4.6% from 2026–2034

- Asia Pacific dominated the finished vehicles logistics market with a 51.56% share in 2025.

- The LCVs segment is anticipated to be the fastest-growing, registering a CAGR of 5.5% during the forecast period.

- The electric vehicle segment is anticipated to be the fastest-growing, registering a CAGR of 9.2% over the forecast period.

Asia Pacific

Valued at USD 58.19 billion in 2025, driven by high vehicle production, expanding exports, and growing EV manufacturing.

Europe

Valued at USD 25.59 billion in 2025, driven by robust automotive manufacturing and extensive multimodal logistics networks.

North America

Projected to reach USD 25.31 billion by 2026, supported by strong automotive production and advanced transport infrastructure.

U.S.

Projected to reach USD 16.54 billion by 2026, supported by high vehicle production and strong domestic distribution networks.

Japan

Expected to witness steady growth, driven by strong vehicle exports and advanced automotive logistics infrastructure.

Read More

FINISHED VEHICLES LOGISTICS MARKET TRENDS

Rising Government Investment in Transport Infrastructure is a Key Trend in Market

Rising government investment in transport and logistics infrastructure has emerged as one of the key finished vehicles logistics market trends. Governments across developed and emerging economies are prioritizing upgrades of ports, highways, rail corridors, and inland logistics hubs to support growing automotive production and exports. These initiatives aim to reduce transit times, lower logistics costs, and ease congestion at key vehicle handling points. Additionally, policy support for multimodal transportation and incentives for rail- and sea-based vehicle movement are strengthening finished vehicle distribution networks and improving supply chain resilience, thereby supporting market growth.

- In November 2025, the Government of India reported logistics cost reductions and multimodal infrastructure improvements, boosting road, rail, and waterways connectivity, enhancing vehicle transport efficiency, and supporting faster finished vehicle movement nationwide.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Vehicle Production is Accelerating Market Growth

The increasing volume of global vehicle production is a major factor driving the market. Automakers are expanding manufacturing capacities to meet rising demand for passenger cars, SUVs, and commercial vehicles across domestic and export markets. As production volumes increase, the need for efficient transportation, storage, and distribution of finished vehicles intensifies. This growth directly expands demand for specialized logistics services, including road rail sea and air movement, as well as port handling and yard management. Consequently, logistics providers are investing in capacity expansion, fleet optimization, and digital tracking solutions to manage higher throughput and complex distribution networks. These combined factors are accelerating the adoption of outsourced finished vehicle logistics services globally.

- In September 2025, SIAM reported passenger vehicle exports at 2.42 lakh units, up 23% year-on-year, boosting finished vehicle logistics market demand, infrastructure and export transport efficiency in India’s automotive supply chain.

MARKET RESTRAINTS

High Logistics Costs and Infrastructure Constraints to Restrict Market Growth

High logistics costs combined with infrastructure constraints pose a significant restraint on the finished vehicles logistics market growth. Transporting finished vehicles requires specialized carriers, dedicated handling equipment, secure storage yards, and multimodal coordination, all of which substantially increase operational costs. Rising fuel prices, labor shortages, and insurance expenses further pressure profit margins for logistics firms. In addition, inadequate port capacity, rail bottlenecks, and congested road networks in several regions lead to delays, vehicle damage risks, and higher turnaround times. These challenges reduce operational efficiency and increase costs for automotive OEMs, limiting their ability to scale distribution networks efficiently and restraining overall market expansion.

- In June 2024, IRU reported European road freight contract rates rose 3.7% year-on-year, while spot rates declined 0.3%, impacting finished vehicle road logistics costs and carrier capacity planning across Europe.

MARKET OPPORTUNITIES

Expansion of Automotive Exports from Emerging Economies to Create Market Growth Opportunities

The rapid expansion of automotive exports from emerging economies is expected to create significant growth opportunities in the market of finished vehicles logistics. Countries in Asia, Eastern Europe, and Latin America are strengthening their positions as global vehicle manufacturing and export hubs due to cost advantages and favorable trade agreements. This trend is increasing demand for international vehicle transportation, port-based vehicle handling, storage yards, and multimodal logistics solutions. To support rising export volumes, logistics providers are expanding port capacities, developing dedicated export corridors, and enhancing cross-border coordination. These developments are enabling logistics companies to capture new business from OEMs seeking reliable and scalable export-focused logistics partners.

- In August 2025, Thailand’s revised EV export incentives could boost annual vehicle exports from 12,500 to 52,000 units by 2026, strengthening finished vehicle logistics industry and positioning Thailand as a key export hub.

MARKET CHALLENGES

Supply Chain Disruptions and Capacity Imbalances to Pose a Critical Challenge to Market Growth

Supply chain disruptions and capacity imbalances continue to pose a critical challenge to the market. The market is highly sensitive to geopolitical tensions, trade policy changes, port congestion, and labor shortages, which can abruptly disrupt vehicle flows across regions. Sudden production shifts, uneven vehicle demand, and limited availability of specialized carriers often lead to bottlenecks, delayed deliveries, and inventory pile-ups at ports and storage yards. These disruptions reduce logistics reliability, increase dwell times, and elevate costs for automotive OEMs, undermining distribution efficiency and long-term planning.

Segmentation Analysis

By Vehicle Type

Rising Demand for SUVs and Expanding LCV Applications to Drive Segmental Growth

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

The SUVs segment is anticipated to account for the largest finished vehicle market share. The dominance of this segment is primarily attributed to the strong global shift in consumer preference toward SUVs due to their higher seating position, enhanced safety perception, and versatility across urban and semi-urban usage. Increasing SUV production volumes across North America, Europe, and the Asia Pacific have significantly raised the demand for large-scale vehicle transportation, port handling, and storage services. Additionally, SUVs typically occupy more space and require specialized carriers, which further increases logistics demand per unit, strengthening the segment’s market position. Continuous SUV model launches and export-oriented production are expected to sustain this dominance.

- In December 2024, Mahindra reported 22% year-on-year growth in November SUV sales, increasing outbound finished vehicle movements and strengthening demand for domestic road and rail vehicle logistics across India.

The LCVs segment is anticipated to be the fastest growing, registering a CAGR of 5.5% over the finished vehicles logistics market forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Propulsion

Established ICE Vehicle Base Sustains High Finished Vehicle Logistics Demand

Based on vehicle propulsion, the market is segmented into internal combustion engine (ICE) vehicles and electric.

The ICE segment is anticipated to account for the largest share in 2025. This dominance is driven by the vast installed base of ICE-powered passenger and commercial vehicles globally, supported by mature manufacturing ecosystems and extensive fuel infrastructure. Continuous production of ICE vehicles for domestic use and exports ensures consistent demand for road, rail, and maritime vehicle transportation, as well as port handling and storage services. As a result, logistics providers continue to allocate the majority of their capacity toward ICE vehicle movements, reinforcing the segment’s leadership in the market.

- In July 2025, ICE vehicles dominated 4W sales, led by Maruti Suzuki’s 128,737 units. Most OEMs reported negligible or zero EV sales, underscoring continued ICE prevalence despite selective EV penetration.

The electric vehicle segment is anticipated to be the fastest-growing, registering a CAGR of 9.2% over the forecast period.

By Distribution

Strong Domestic Vehicle Flows Anchor Finished Vehicle Logistics Operations

Based on distribution, the market is segmented into domestic and international.

The domestic segment dominated the market in 2025. This dominance is primarily driven by high volumes of intra-country vehicle movement from manufacturing plants to regional distribution centers, dealerships, and fleet customers. Large automotive markets such as the U.S., China, India, and Germany rely heavily on road and rail networks for domestic vehicle distribution due to shorter lead times, lower regulatory complexity, and cost efficiency. Continuous vehicle production to meet local demand ensures stable and recurring domestic logistics activity, reinforcing the segment’s leading market position.

- In March 2024, Hyundai Motor committed USD 21 billion to U.S. vehicle manufacturing, supply chain, and logistics, strengthening domestic finished vehicle flows, port usage, and inland transport networks across North America.

The international segment is anticipated to be the fastest-growing, registering a CAGR of 5.6% over the forecast period.

By Transport Mode

Extensive Road Transport Networks Form Backbone of Finished Vehicle Logistics

Based on transport mode, the market is segmented into road, rail, waterways, and air transport.

The road segment is anticipated to account for the largest share of the market. This dominance is driven by the flexibility, door-to-door connectivity, and wide availability of specialized car carriers and truck fleets. Road transport is extensively used for short- and medium-distance vehicle movement from manufacturing plants to distribution centers, ports, and dealerships. Its ability to serve last-mile delivery requirements with minimal infrastructure dependency makes it the preferred transport mode across major automotive markets, thereby sustaining high utilization levels for road-based finished vehicle logistics.

- In November 2024, Autozi launched a China–Europe cross-border supply chain platform, enhancing finished vehicle logistics efficiency, reducing delivery timelines, and supporting growing automotive trade volumes between Asian and European markets.

The air transport segment is anticipated to be the fastest-growing, registering a CAGR of 6.8% over the forecast period.

By Service Type

Primary Transport Services Anchor Core Finished Vehicle Logistics Operations

Based on service type, the market is segmented into primary transport, secondary/last-mile distribution, port & terminal services, storage & yard management, and value-added services.

The primary transport segment is anticipated to dominate the market. This dominance is driven by the high volume of vehicle movements from manufacturing plants to regional distribution centers, ports, and major hubs. Primary transport forms the backbone of finished vehicle logistics, relying heavily on road, rail, and waterways to handle large-scale, long-distance shipments efficiently. Consistent vehicle production levels and export-oriented manufacturing further sustain strong demand for primary transport services, reinforcing the segment’s leading market position.

The port & terminal services segment is anticipated to be the fastest growing, registering a CAGR of 6.0% over the forecast period.

Finished Vehicles Logistics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific Finished Vehicles Logistics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant finished vehicles logistics market share, valuing at USD 56.34 billion in 2024, and also maintained the leading share in 2025, with USD 58.19 billion. The regional market is driven by high automotive production volumes, expanding vehicle exports from China, Japan, South Korea, and India, and rising domestic vehicle demand. Rapid industrialization, improving port and rail infrastructure, growing EV manufacturing, and government-led logistics and trade facilitation initiatives further strengthen regional finished vehicles logistics and reverse logistics distribution networks.

China Finished Vehicles Logistics Market

Based on Asia Pacific’s strong contribution and China's dominance within the region, the China finished vehicles logistics market can be analytically approximated at around USD 35.49 billion in 2025, accounting for roughly 7.40% of global finished vehicles logistics sales.

Rest of the World

Rest of the World, comprising of South America, Middle East and Africa, is projected to record a growth rate of 4.8% in the coming years, which is the second highest among all regions, and reach a valuation of USD 5.76 billion by 2026. The growth is driven by rising vehicle imports, expanding assembly plants, infrastructure investments, and improving port connectivity across emerging markets.

North America

North America market of finished vehicles logistics is estimated to reach USD 25.31 billion in 2026 and secure the position of the third-largest region in the market. The market is driven by high vehicle production and sales, strong domestic distribution networks, and significant automotive import-export activity. Well-developed road, rail, and port infrastructure, early adoption of digital logistics solutions, growing EV shipments, and continued investments in intermodal connectivity further support efficient finished vehicle transportation across the region.

U.S. Finished Vehicles Logistics Market

U.S dominated the region, and is estimated to reach USD 16.54 billion in 2026, representing around 14.1% of the global sales. The U.S. finished vehicles logistics market is driven by high vehicle production, strong domestic distribution, robust imports, and advanced transport infrastructure.

Europe

Europe is expected to witness moderate growth in this market during the forecast period. The European market is set to reach a valuation of USD 25.59 billion in 2025. The European market is driven by strong automotive manufacturing in Germany, France, and Eastern Europe, and high intra-regional vehicle trade. Extensive road, rail, and port infrastructure, rising vehicle exports, adoption of multimodal transport, and sustainability-focused logistics investments further support efficient finished vehicles logistics across the region.

U.K Finished Vehicles Logistics Market

The U.K. Finished Vehicles Logistics market in 2026 is estimated at around USD 1.35 billion, representing roughly 1.1% of global finished vehicles logistics revenues.

Germany Finished Vehicles Logistics Market

Germany’s Finished Vehicles Logistics market is projected to reach approximately USD 5.98 billion in 2026, equivalent to around 5.1% of global finished vehicles logistics sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Capacity Expansion and Partnerships by Key Players to Strengthen Market Position

The global finished vehicles logistics market exhibits a moderately consolidated structure, with prominent market players such as CEVA Logistics, DHL Supply Chain, Kuehne+Nagel, and DB Schenker holding significant market share. Their strong positioning is supported by extensive global networks, long-term contracts with automotive OEMs, and continuous investments in fleet expansion, port terminals, and digital logistics platforms. Strategic partnerships and infrastructure investments are key approaches adopted by these players to enhance operational efficiency and service coverage.

- In June 2024, CEVA Logistics expanded special finished vehicle transport services across 15+ European countries, enhancing capacity for oversized, high-value vehicles and strengthening cross-border automotive logistics

Other notable players operating in the global market of finished vehicles logistics include Maersk Logistics & Services, Toll Group, Nippon, and others. These companies are expected to focus on terminal automation, sustainability initiatives, and EV-ready logistics solutions to strengthen their competitive position during the forecast period.

LIST OF KEY FINISHED VEHICLES LOGISTICS COMPANIES PROFILED

- CEVA Logistics (France)

- DP World (UAE)

- DSV (Denmark)

- Kuehne Nagel (Switzerland)

- DHL Supply Chain (Germany)

- Maersk (Denmark)

- United Parcel Service (U.S.)

- Toll Group (Australia)

- Wallenius Wilhelmsen (Sweden/Norway)

- Hyundai Glovis (South Korea)

- VASCOR Logistics (U.S.)

- Sphere Global (U.S.)

- BLG Logistics (Germany)

- Gefco Group (France)

- Nippon Express (Japan)

- Wallenius Wilhelmsen (Norway)

- NYK Global (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Dighi Port in Navi Mumbai set to handle 200,000 cars annually through a new automotive export facility with Adani Ports and Motherson’s joint venture, enhancing India’s vehicle logistics infrastructure.

- August 2025: DP World expanded vehicle logistics capacity at Jebel Ali Port with a 2.6 million sq ft storage yard and RoRo quay to meet growing demand, boosting throughput 28% in early 2025.

- July 2025: Beibu Gulf Port launched a new Ro-Ro link to UAE, enhancing vehicle export logistics in Asia-Middle East trade routes.

- April 2025: BYD takes delivery of the world’s largest car carrier, boosting global RoRo vehicle transport capacity.

- January 2025: Wallenius Wilhelmsen wins a 12-year Gothenburg RoRo terminal contract to boost vehicle logistics operations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Vehicle Propulsion, Mode of Transport, Distribution, Service Type, and Region |

|

By Vehicle Type |

· Hatchback & Sedans · SUVs · LCVs · HCVs |

|

By Vehicle Propulsion |

· ICE · Electric |

|

By Transport Mode |

· Road · Rail · Waterways · Air |

|

By Distribution |

· Domestic · International

|

|

By Service Type |

· Primary Transport · Secondary/Last-mile Distribution · Port & Terminal Services · Storage & Yard Management · Value-added Services |

|

By Region |

· North America (By Vehicle Type, Vehicle Propulsion, Mode of Transport, Distribution, Service Type, and Country) o U.S. o Canada o Mexico · Europe ( By Vehicle Type, Vehicle Propulsion, Mode of Transport, Distribution, Service Type, and Country/Sub-region) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Vehicle Propulsion, Mode of Transport, Distribution, Service Type, and Country/Sub-region) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World ( By Vehicle Type, Vehicle Propulsion, Mode of Transport, Distribution, Service Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 112.86 billion in 2025 and is projected to reach USD 168.74 billion by 2034.

In 2025, the market value stood at USD 58.19 billion.

The market is expected to exhibit a CAGR of 4.6% during the forecast period of 2026-2034.

By vehicle type, the SUVs segment is expected to lead the market.

Rising global vehicle production is accelerating market growth.

CEVA Logistics, DHL Supply Chain, Kuehne+Nagel, and DB Schenker are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us