Firefighting Foam Market Size, Share & Industry Analysis, By Type (AFFF (Aqueous Film Forming Foam), AR-AFFF (Alcohol-Resistant Aqueous Film Forming Foam), Fluorine-Free Foams, Synthetic Foams, and Others), By End-Use Industry (Aviation, Oil & Gas, Marine & Shipping, Industrial & Manufacturing, Municipal & Fire Services, and Others), and Regional Forecast, 2026-2034

Firefighting Foam Market Size and Future Outlook

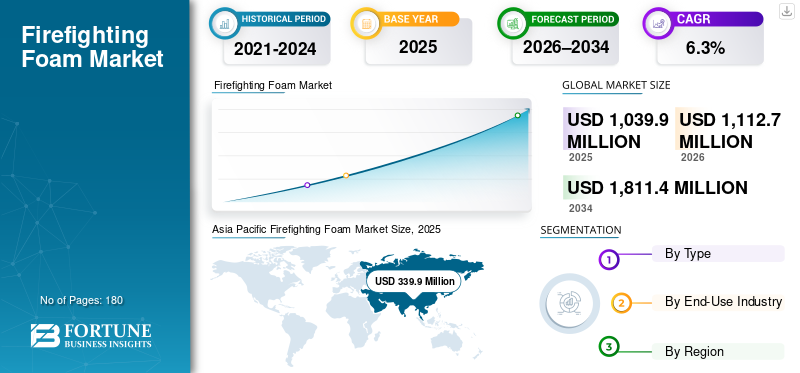

The global firefighting foam market size was valued at USD 1,039.9 million in 2025. The market is projected to grow from USD 1,112.7 million in 2026 to USD 1,811.4 million by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the global firefighting foam market with a market share of 32.68% in 2025.

Firefighting foam is a key fire suppression material used to control and extinguish fires, particularly those involving flammable liquids, fire, and hazardous sites. Demand for firefighting foam is closely tied to safety requirements across oil and gas facilities, airports, chemical plants, marine operations, and municipal fire services, where increasing fire control and reliable performance are critical. The market is primarily supported by regulatory compliance, routine replacement, and training activities rather than strong growth in new installations. Globally, tightening environmental regulations are influencing demand patterns and encouraging a gradual shift away from fluorinated foams toward fluorine-free alternatives.

A limited group of established firefighting foam manufacturers with strong formulation expertise and long-standing relationships with end users dominates the market. Major players such as Angus Fire, Dafo Fomtec AB, Stamer, National Foam, and BIOEX, focus on product performance, regulatory compliance, and fire testing certifications, resulting in a moderately consolidated market characterized by stable demand, high qualification and approval requirements, and controlled product substitution.

Download Free sample to learn more about this report.

Firefighting Foam Market Key Takeaways

- 2025 Market Size: USD 1,039.9 Million

- 2026 Market Size: USD 1,112.7 Million

- 2034 Forecast Market Size: USD 1,811.4 Million

- CAGR: 6.3% from 2026–2034

- Asia Pacific dominated the firefighting foam market with a 32.68% share in 2025.

- Fluorine-free foams accounted for the largest market share in 2025.

- Oil & gas held the largest end-use industry share in 2025.

Asia Pacific

Asia Pacific led the market with USD 339.9 million in 2025 and is projected to reach USD 363.7 million in 2026.

North America

North America accounted for USD 244.0 million of the global market in 2025.

Europe

Europe generated USD 236.3 million in revenue in 2025, supported by strict fire safety regulations.

U.S.

The market was valued at USD 201.0 million in 2025, driven by oil & gas, aviation, and industrial demand.

Japan

Demand is supported by stringent fire safety standards and industrial infrastructure development.

Read More

FIREFIGHTING FOAM MARKET TRENDS

Product Reformulation and Portfolio Shift Toward Fluorine-Free Foams is a Key Market Trend

A key trend in the market is manufacturers' gradual shift toward fluorine-free foam formulations. Companies are investing in reformulation, improved surfactant systems, and performance optimization to meet fire safety and certification requirements without using fluorinated chemicals. This reflects a strategic change in product development and portfolio focus as suppliers adapt to long-term environmental regulations and customer expectations. Rather than driving immediate volume growth, this trend is reshaping competitive positioning and influencing how products are designed, tested, and supplied across regulated end-use sectors.

- According to the U.S. Environmental Protection Agency (EPA), proposed drinking water limits for certain PFAS (Per- and polyfluoroalkyl substances) compounds are set at 4 parts per trillion (ppt), reinforcing regulatory pressure to eliminate PFAS sources, such as firefighting foams.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Mandatory Fire Safety Requirements in High-Risk Industrial Facilities to Boost Market Growth

The demand for firefighting foam is primarily driven by strict fire safety regulations in oil and gas production facilities, refineries, and petrochemical complexes. These sites handle large volumes of flammable hydrocarbons, making rapid fire suppression systems mandatory for operational safety. It is a non-discretionary input, as facilities must maintain approved foam stocks to meet regulatory, insurance, and emergency response requirements. Regular inspections, training drills, and mandatory replacement of degraded foam concentrates create recurring demand. As global energy infrastructure continues to operate at scale, compliance-led consumption remains a stable, long-term driver of the market.

- According to a U.S. Government Accountability Office (GAO) report, the U.S. Department of Defense has identified at least 687 military installations with known or suspected PFAS releases from firefighting foams, which are under investigation for environmental contamination and remediation.

MARKET RESTRAINTS

Fragmented Standards and High System Transition Costs Restrict Market Growth

The firefighting foam market growth is restrained by fragmented fire safety standards and the high cost of transitioning existing fire suppression systems. Different certification and approval requirements across industrial facilities, airports, and defense installations limit easy substitution between foam formulations. In many cases, switching to alternative foams requires system flushing, equipment compatibility checks, re-testing, and operator training, which increases costs and delays procurement decisions, slowing short-term market adoption.

- According to the U.S. Government Accountability Office (GAO), the U.S. Department of Defense estimates transition costs exceeding USD 2.1 billion to replace PFAS-based firefighting foams across its land-based facilities, highlighting how high system conversion costs can act as a significant restraint on market transition.

MARKET OPPORTUNITIES

PFAS Phase-Out Policies Are Creating Replacement-Led Growth Opportunities

PFAS phase-out regulations are creating new growth opportunities for the market by requiring the replacement of existing foam inventories rather than supporting only routine demand. Airports, industrial facilities, and defense sites are under pressure to shift from legacy fluorinated foams to approved fluorine-free alternatives within defined timelines. This transition leads to additional purchases, system re-qualification, and rebuilding of foam stocks. As a result, demand increases beyond regular replacement cycles, supporting incremental market growth over the medium term.

- According to the U.S. Government Accountability Office (GAO), the National Defense Authorization Act for Fiscal Year 2020 required the Department of Defense to discontinue the use of PFAS-containing aqueous film-forming foam (AFFF) at its installations after October 1, 2024, driving widespread efforts to transition to fluorine-free alternatives.

MARKET CHALLENGES

Raw Material Cost Volatility and Higher Reformulation Costs Pressure Margins

Manufacturers face ongoing challenges due to fluctuations in the prices of key raw materials, such as surfactants, solvents, and specialty additives. The move toward fluorine-free formulations often requires more complex, higher-cost ingredients, thereby increasing production costs. At the same time, long-term contracts and fixed pricing in regulated end-use sectors limit the ability to pass these cost increases on to customers. As a result, manufacturers experience margin pressure even when overall demand remains stable.

- According to the U.S. Environmental Protection Agency (EPA), over 650 PFAS chemicals are now subject to mandatory reporting under the Toxics Release Inventory (TRI) program, increasing compliance and reporting costs for manufacturers linked to firefighting foam supply chains.

Segmentation Analysis

By Type

Fluorine-Free Foams Segment Led Market Due to Regulatory Transition

Based on type, the market is segmented into AFFF (aqueous film forming foam), AR-AFFF (alcohol-resistant aqueous film forming foam), fluorine-free foams, synthetic foams, and others.

The fluorine-free foams segment accounted for the largest firefighting foam market share in 2025, supported by a clear shift away from fluorinated formulations. Environmental regulations, PFAS restrictions, and growing liability concerns across airports, industrial sites, defense facilities, and fire services drive demand. These foams are increasingly used for replacing existing foam stocks and for new fire protection systems. As performance standards and certifications continue to improve, fluorine-free foams are becoming the preferred choice, strengthening their position as the dominant segment in the market.

The synthetic foams segment is expected to grow at a CAGR of about 6.1% over the forecast period, supported by its cost efficiency and continued use in municipal firefighting, training activities, and lower-risk fire applications.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Oil & Gas Segment Dominated Due to High Fire Risk and Mandatory Safety Compliance

By end-use industry, the market is segmented into aviation, oil & gas, marine & shipping, industrial & manufacturing, municipal & fire services, and others.

The oil & gas segment accounted for the largest share of the market in 2025. Oil and gas facilities handle large volumes of flammable hydrocarbons, making effective fire suppression systems essential for operational safety. Refineries, production sites, storage terminals, and pipelines must maintain approved firefighting foam systems to control fuel fires and prevent escalation. Regular safety audits, emergency preparedness requirements, and routine replacement of foam stocks create a strong, compliance-driven demand base, positioning oil and gas as the dominant end-use industry.

- According to the U.S. Energy Information Administration (EIA), the U.S. has over 500 natural gas processing plants, all of which require firefighting systems due to their high fire risk.

The aviation segment is expected to grow at a CAGR of 6.8% over the forecast period.

Firefighting Foam Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Firefighting Foam Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market in 2025, with a value of USD 339.9 million, and is expected to retain its leading position in 2026, reaching USD 363.7 million. Regional leadership is supported by extensive oil and gas operations, expanding industrial and manufacturing bases, and a growing number of airports and port facilities. Strong enforcement of fire safety regulations across refineries, petrochemical complexes, aviation hubs, and marine operations sustains consistent demand, while ongoing infrastructure development and safety compliance initiatives further reinforce the Asia Pacific’s dominant market position.

China Firefighting Foam Market

Based on Asia Pacific’s strong contribution and China’s large industrial and energy infrastructure, the China market was valued at USD 149.57 million in 2025, representing approximately 44.01% of global revenues. Demand is driven by extensive oil and gas facilities, petrochemical complexes, and refineries, as well as a growing aviation sector. Strict fire safety regulations and ongoing industrial and infrastructure development continue to support steady consumption nationwide.

India Firefighting Foam Market

The India market in 2025 was valued at USD 53.9 million. Growth is supported by expanding oil and gas infrastructure, rising industrial activity, and increasing airport development. Stronger fire safety regulations across refineries, ports, and municipal fire services continue to support demand.

North America

The North America market was valued at USD 244.0 million in 2025. Extensive oil and gas operations, a high concentration of airports, and well-established industrial facilities support demand. Strict fire safety regulations and routine replacement requirements sustain consumption. However, growth remains moderate due to market maturity and the gradual shift from legacy fluorinated foams to alternative formulations.

U.S. Firefighting Foam Market

The U.S. market in 2025 was valued at USD 201.0 million, accounting for approximately 82.36% of global revenues. Demand is driven by extensive oil and gas operations, a large network of commercial and military airports, and widespread industrial and manufacturing facilities requiring certified fire suppression systems.

Europe

Europe was valued at USD 236.3 million in 2025 and is projected to record modest market growth in the coming years. Strict environmental regulations on fluorinated foams and strong enforcement of fire safety standards characterize the region. Despite regulatory pressure, increasing demand from oil and gas facilities, industrial sites, airports, and municipal fire services continues to support consumption across the key European economies.

Germany Firefighting Foam Market

Germany’s market was valued at USD 56.6 million in 2025, representing approximately 23.94% of global demand. Consumption is supported by strong industrial manufacturing and chemical processing facilities, as well as a large network of airports that require certified fire suppression systems.

U.K. Firefighting Foam Market

The U.K. market in 2025 was valued at USD 45.8 million, accounting for roughly 19.36% of global revenues. Consumption is concentrated in oil and gas installations, airports, industrial facilities, and municipal fire services that require certified fire suppression and emergency response systems.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are expected to experience moderate market growth over the forecast period. Latin America was valued at USD 79.7 million in 2025, supported by expanding oil and gas activities, growing industrial infrastructure, and increasing airport development across key economies. Demand is further supported by stricter fire safety enforcement at refineries, terminals, and logistics hubs. In the Middle East & Africa, demand is driven by large-scale oil and gas operations, petrochemical complexes, ports, and aviation infrastructure. The Middle East & Africa market was valued at USD 140.0 million in 2025.

GCC Firefighting Foam Market

The GCC market accounted for around USD 88.6 million in 2025, representing approximately 63.27% of regional revenues. Extensive oil and gas operations, petrochemical complexes, airport infrastructure, and strict fire safety requirements across industrial facilities drive demand.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in Market

The market is relatively consolidated and formulation-intensive, as strict certification requirements, long approval cycles, and performance validation standards create significant barriers to entry. These factors limit new participation and concentrate supply among a small group of established manufacturers with strong formulation expertise and long-standing relationships with regulated end users.

Key players, such as Angus Fire, Dafo Fomtec AB, Stamer, National Foam, and BIOEX, focus primarily on optimizing existing product portfolios and maintaining regulatory compliance rather than pursuing aggressive capacity expansion. Recent activities highlight a strategic emphasis on fluorine-free reformulation, certification readiness, and incremental product improvements to support long-term market positioning.

LIST OF KEY FIREFIGHTING FOAM COMPANIES PROFILED

- Perimeter Solutions (U.S.)

- Angus Fire (U.K.)

- Foamtech Antifire (India)

- Dafo Fomtec AB (Sweden)

- Sthamer (U.K.)

- Jiangsu Suolong Fire Science and Technology Co., Ltd. (China)

- National Foam (U.S.)

- Johnson Controls International plc (Ireland)

- BIOEX (France)

- Kerr Fire (U.K.)

KEY INDUSTRY DEVELOPMENTS

- June 2021: Perimeter Solutions announced that it will become a publicly traded company through acquisition by EverArc Holdings, providing stronger financial backing to invest in firefighting foam solutions and global fire suppression offerings.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The firefighting foam market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.3% from 2026 to 2034 |

|

Unit |

Value (USD Million) Volume (Kiloton) |

|

Segmentation |

By Type, End-Use Industry, and Region |

|

By Type |

· AFFF (Aqueous Film Forming Foam) · AR-AFFF (Alcohol-Resistant Aqueous Film Forming Foam) · Fluorine-Free Foams · Synthetic Foams · Others |

|

By End-Use Industry |

· Aviation · Oil & Gas · Marine & Shipping · Industrial & Manufacturing · Municipal & Fire Services · Others |

|

By Region |

· North America (By Type, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Type, End-Use Industry, and Country) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Spain (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Type, End-Use Industry, and Country) o China (By End-Use Industry) o India (By End-Use Industry) o Japan (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Type, End-Use Industry, and Country) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Type, End-Use Industry, and Country) o GCC (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1,039.9 million in 2025 and is projected to reach USD 1,811.4 million by 2034.

Recording a CAGR of 6.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By end-use industry, the oil & gas segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Mandatory fire safety regulations and compliance requirements to boost market growth.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us